Summary:

- Visa’s stock price has increased by over 15% since the first time I published my bullish thesis, materializing my expectations.

- Visa reported 11.7% total revenue growth and 16% EPS growth, with stable cost growth and substantial shareholder rewards through buybacks and dividends.

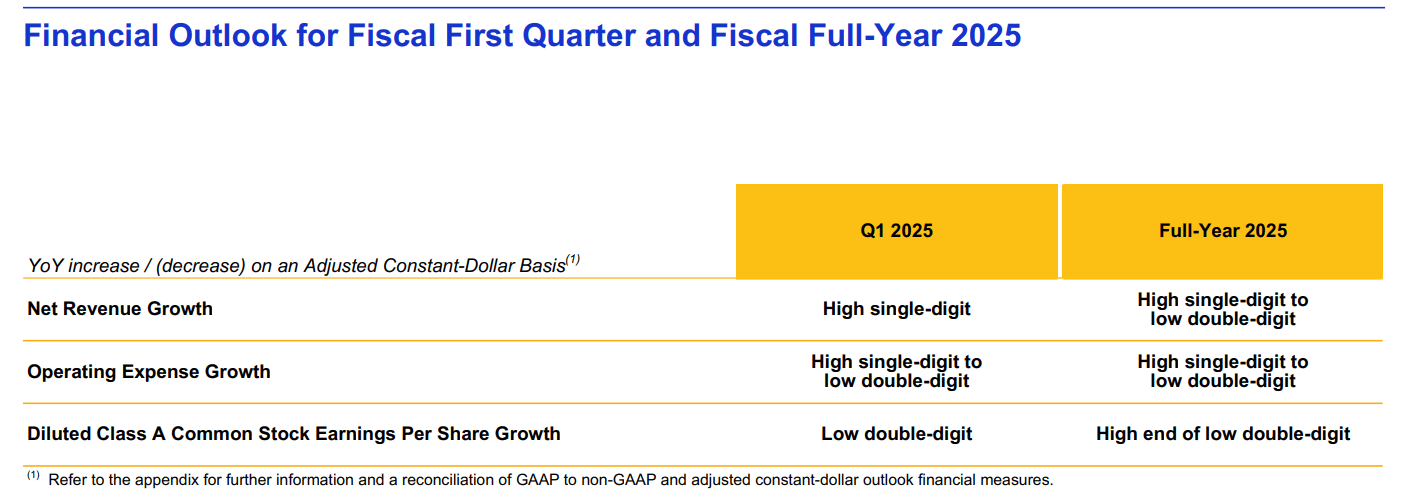

- Visa expects high single-digit to low double-digit revenue and operating expense growth for FY 2025, with high-end low double-digit EPS growth.

- Despite a less attractive entry-level, Visa remains a high-quality business with high profitability, strong cash flow, and leadership position, but I downgrade from ‘strong buy’ to ‘buy’.

BlackJack3D

Since the last time I covered VISA (NYSE:V), the company’s stock price has increased by over 15%, materializing the upside potential I indicated. V has recently published results for FY Q4 2024 (calendar Q3 2024), delivering attractive performance and a positive outlook for the years to come. To get a better grasp on the development of my views on V, please review my previous coverage linked below:

Visa: Global Payments Leader With Robust Dividend Growth Is Undervalued – Strong Buy

Seeking Alpha

Q4 2024 Overview: Solid Revenue Growth, Improved Profitability, Substantial Shareholder Rewards, And Solid Guidance

Visa

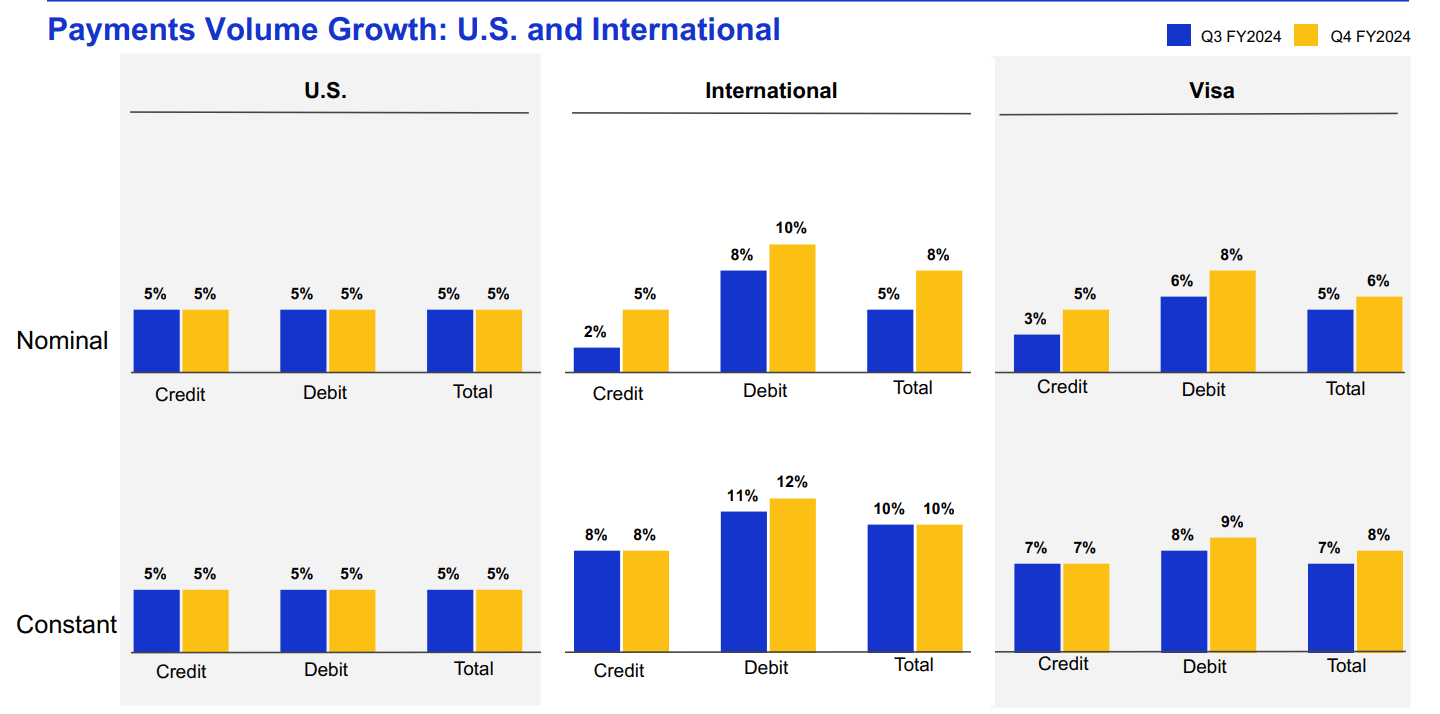

As the management indicated during the last Earnings Call, Visa’s key growth drivers remained stable. Constant dollar payment volumes grew by 8% for the whole business, while it recorded 5% and 10% growth in the US and Internationally, respectively.

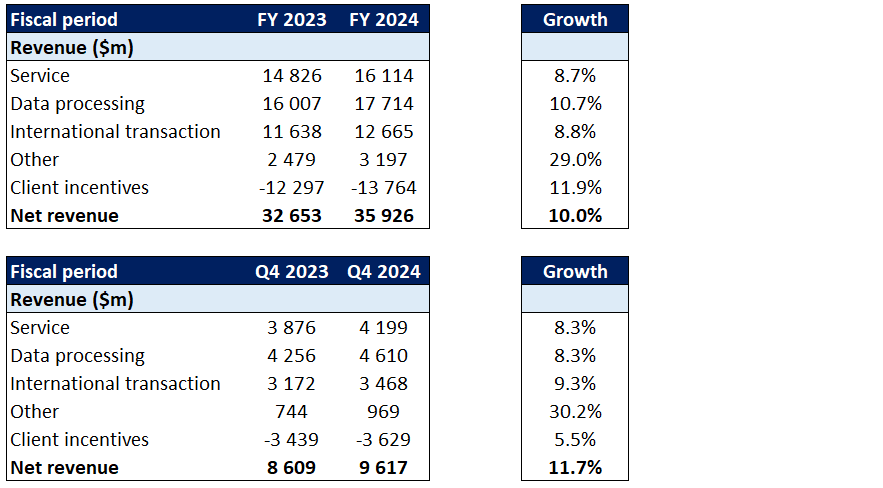

As a result, Visa recorded strong Q4 2024 performance, delivering 11.7% total revenue growth, driven by:

- 8.3% growth in the Service segment.

- 8.3% growth in the Data processing segment.

- 9.3% growth in the International transaction segment.

- Over 30% in the Other segment (however, that’s not as material as other segments).

- Partially offset by Client incentives’ growth of 5.5%.

Overall, despite some ‘misses’ regarding the expectations of the previous quarter (as commented in my last coverage), Visa provided a strong FY 2024 not only in terms of revenue growth but also above the management’s expectations of profitability:

EPS was up 16% year-over-year and 17% in constant dollars, higher than expected from the strong net revenue performance and a lower-than-expected tax rate.

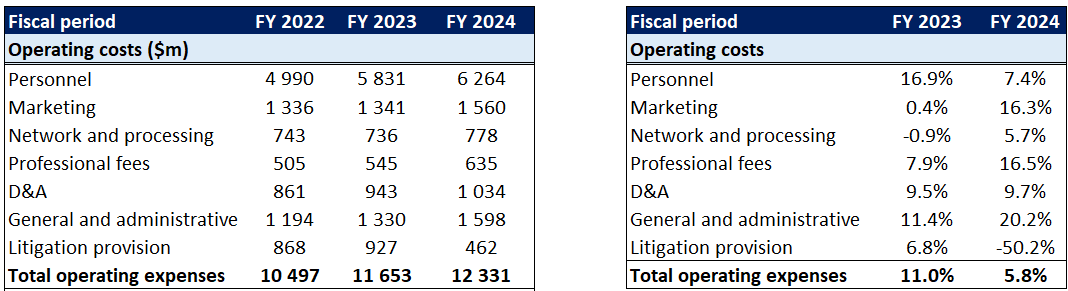

Visa also recorded relatively stable cost growth, with personnel expenses growing 7.4% (y/o/y) compared to 16.9% in the previous period. Marketing costs grew much more dynamically. Such a tendency should (hopefully) support further revenue growth. Overall, V’s costs grew by a mid-single-digit 5.8% vs 11% a year before due to less dynamic personnel expense growth, which holds a dominant share in V’s cost structure. Please review the details regarding V’s revenue and cost growth in the tables below.

Author Author

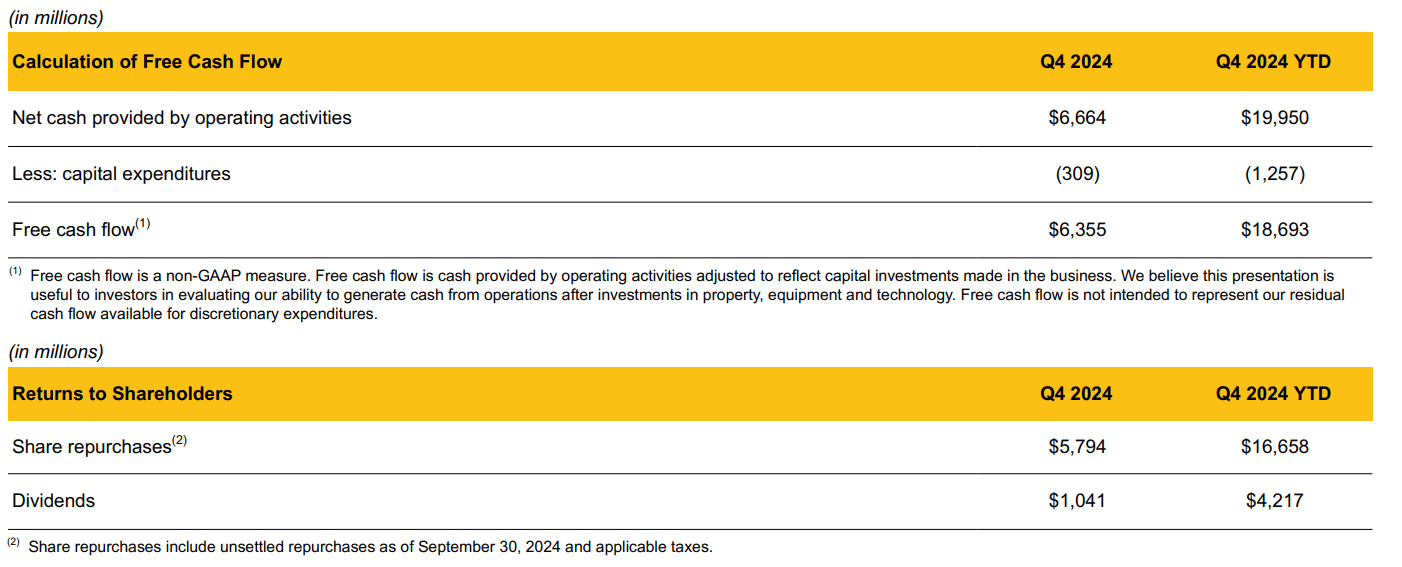

During 2024, V generated ~$18.7B of free cash flow, proving its cash-flow-machine status, and delivered substantial shareholder rewards through:

- Share repurchases ($16.7B)

- Dividends ($4.2B)

Visa

Moving onto the FY 2025 outlook, Visa expects high single-digit to low double-digit revenue and operating expense growth for the full fiscal year, with higher expectations for FY Q1 2025 regarding revenue growth. Overall, Visa expects a high end of low double-digit EPS growth for its diluted Class A Common Stock.

Visa

Valuation Outlook

As an M&A advisor, I usually rely on a multiple valuation method, a leading tool in transaction processes. This method allows for accessible and market-driven benchmarking. Numerous metrics are available for valuing a company, with EV/EBITDA being a rule of thumb for most sectors and transactions.

Over the last three years, Visa provided steady and impressive EBITDA growth while its valuation (according to Benjamin Graham’s Mr. Market metaphor) had its ups and downs but moved with a growing trajectory). As a result, attractive entry levels were possible for investors attracted to dynamically growing tech businesses offering impressive DPS growth.

The last time I published about V, its enterprise value took a dip and offered double-digit upside potential, resulting solely from the multiple expansions. Since then, the multiple has recovered.

With that said, the forward-looking EV/EBITDA multiple currently stands at:

Some may wonder why Mastercard enjoys such a high valuation multiple when compared to V. To put it briefly, Mastercard records higher revenue growth and provides a better growth outlook for the upcoming years, hence the premium.

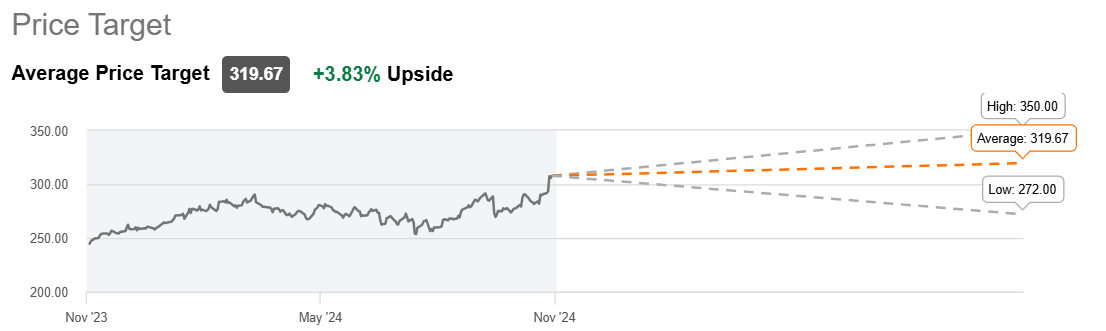

Nevertheless, V may still provide some upside potential. However, the potential is less prominent than it used to be. Even Wall Street Analysts’ average price target assumes quite a modest upside potential resulting from buying V. Still; I believe V can outperform Wall St. average expectations. Investors should be wary of potential stock price volatility, as the ‘bargain’ window has closed.

Seeking Alpha

My Conclusion: Your Takeaway

I am satisfied with V’s FY 2024 performance and 2025 outlook. However, one has to recognise that the entry-level is substantially less attractive than it was when I first covered Visa. The Company keeps me involved through its:

- High profitability.

- Cash flow machine status.

- Leadership position.

- High-quality business model and positive value drivers accompanying further growth.

Nevertheless, I am wary of my entry levels and always search for a sufficient margin of safety. Therefore, I downgraded my previously assigned ‘strong buy’ to ‘buy’.

Investors should be aware that, except for the valuation aspect that could lead to high stock price volatility, Visa is accompanied by several risk factors, including:

- Uncertainty regarding the state of the economy, technological landscape, regulatory environment, tax levels, and FED policy.

- FX fluctuations.

- Consumer behaviour regarding payment practices.

- V is a technological business supporting crucial infrastructure in the modern world. Therefore, it’s susceptible to major cyberattacks, data leakages, or payment network blackouts.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of V, MA either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

The information, opinions, and thoughts included in this article do not constitute an investment recommendation or any form of investment advice.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.