Summary:

- Risk-on sentiment is back in the market, making mega-cap tech stocks like Netflix attractive again.

- The daily chart shows a potential breakout higher for Netflix, with the accumulation/distribution line indicating money flowing into the stock.

- The weekly chart looks even more bullish, with strong seasonality trends and potential for significant upside before encountering resistance.

Mario Tama

With risk-on sentiment now back in the market, mega-cap tech stocks that have been crushed since the July top look quite attractive. One that I like here is Netflix (NASDAQ:NFLX), which is seeing rapidly improving revenue and margin trends based on great content, monetization efforts, and spending discipline. The chart is improving as well, and I think we’re on the cusp of a big move. Let’s take a look.

Strong risk/reward means it’s a buy

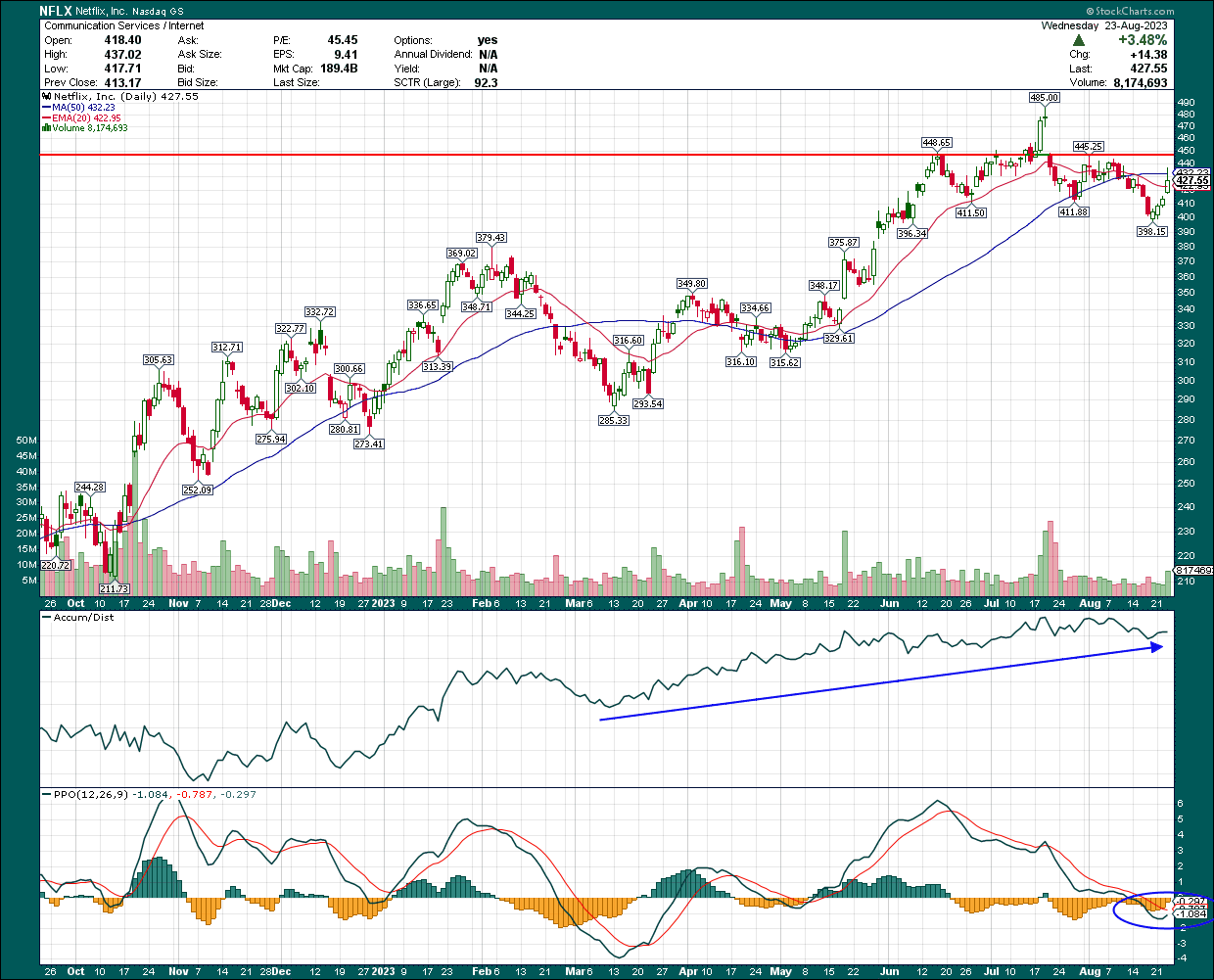

Let’s start with the daily chart, showing the big breakdown we’ve seen in the past couple of weeks. The loss of the moving averages was a big hit to the bulls, but the rally that started a few days ago has already retaken the 20-day exponential moving average and is on the cusp of the 50-day simple moving average. There’s some work for the bulls to do here, but I think Netflix is on the cusp of a breakout higher.

StockCharts

The critical levels here are the 20-day EMA (in red) and the low from a few days ago at $398. Any uptrend has to have higher highs and higher lows. We are close to a higher high, but the important thing here is to get a higher low when an eventual pullback does occur.

The reason I’m bullish is because the accumulation/distribution line is right at its highs during this consolidation/pullback, which means money is flowing into the stock during the day. That often portends an up move.

Second, the PPO is turning higher at just the right time after a much-needed reset from overbought conditions. I believe this is the start of a new uptrend given this slate of evidence. A loss of the 20-day EMA would be a sizable negative, but so long as we see a higher low on any pullback, this one is a buy.

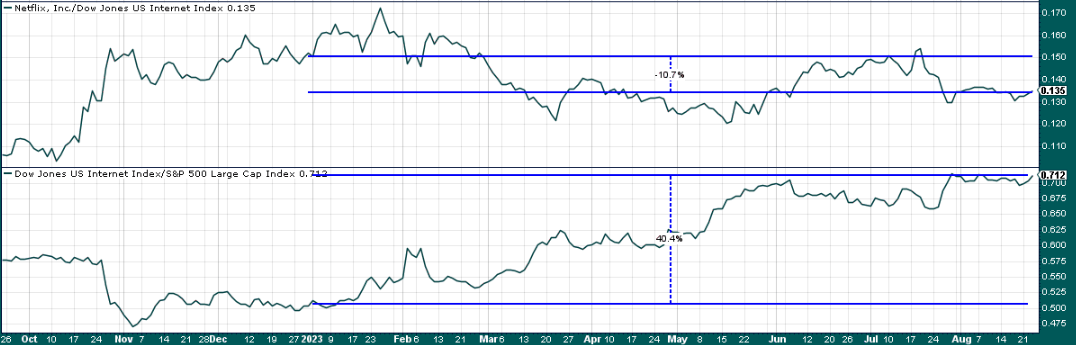

Now, relative strength has been good, but not great. Netflix is losing to its peer group so far this year, but much of that has been due to the past few weeks of pulling back.

StockCharts

On the plus side, its peer group is flying, beating the S&P 500 by 40% so far this year. Netflix is in a leading group, and I think it’s about to see its relative strength against its peers return.

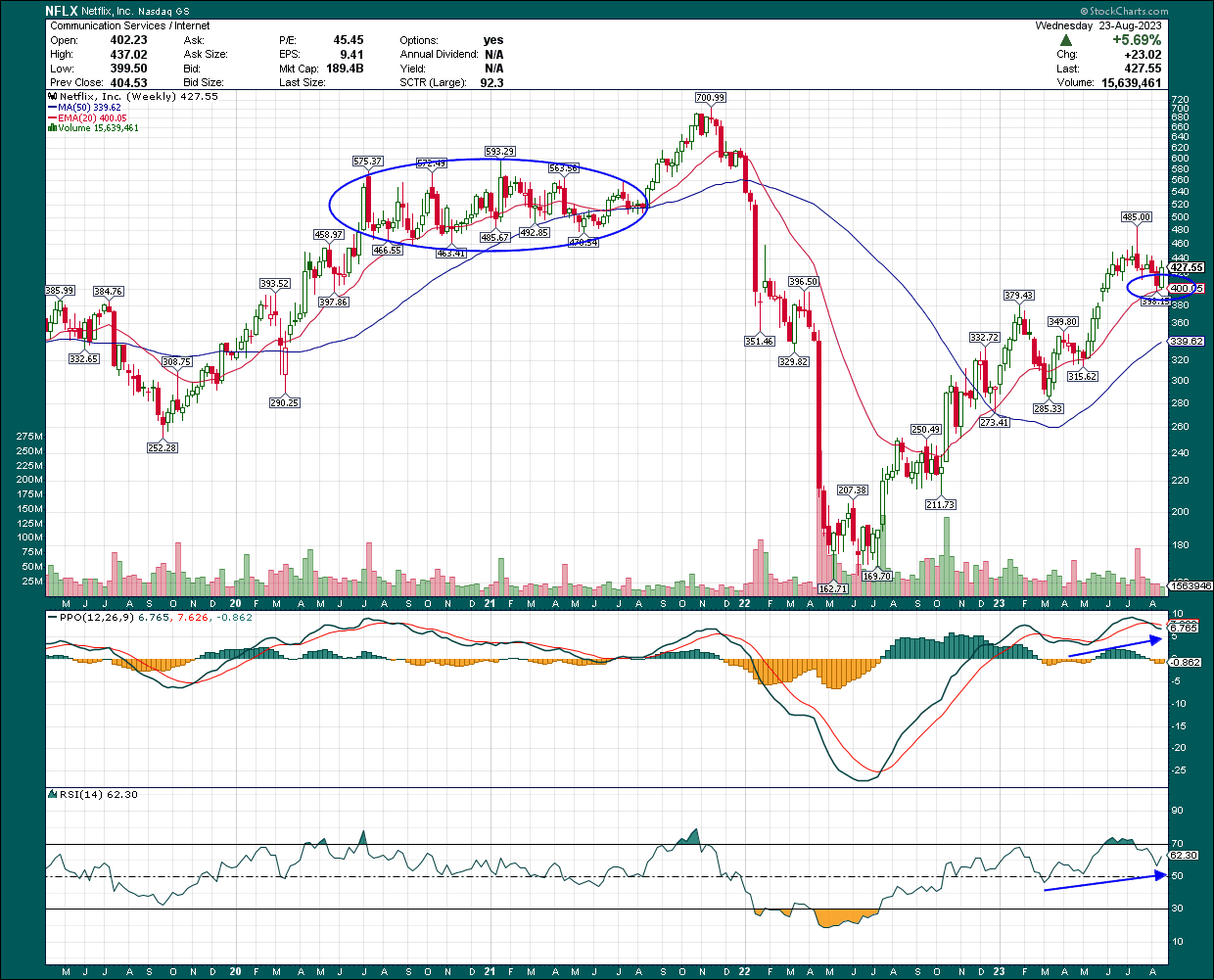

Let’s now turn our attention to the longer-term weekly chart, which shows a very successful 20-week exponential moving average test.

StockCharts

I’ve circled that test, which occurred last week, and the stock has bounced very strongly off of it. The weekly PPO is flying and making new highs, while the 14-week RSI is moving up again. The weekly chart, to me, looks better than the daily chart, which makes the long case easier to make.

There isn’t significant resistance on the weekly chart until the consolidation that took place in 2020/2021 between roughly $470 and $570. A huge amount of trading took place in that consolidation, and it should prove to be at least a stopping point later on. But we’ve got at least fifty bucks of upside potential before that becomes an issue.

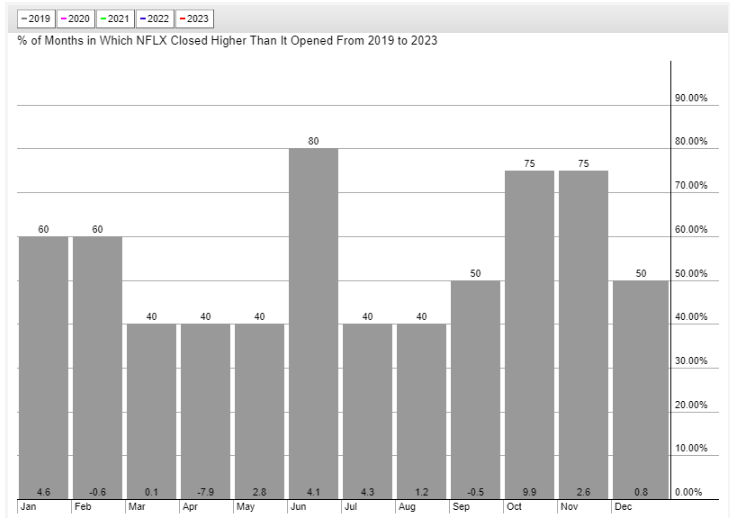

One final technical factor is that seasonality strongly favors Netflix in the last three months of the year.

StockCharts

August is relatively weak, as is September. However, October and November are outstanding, and I think this year will be no different.

To sum up the technical outlook, we have an improving daily chart, a very bullish weekly chart, and strong seasonality trends all working in the favor of the bulls. I can’t help but be bullish here given the risk/reward potential.

Let’s now take a look at some fundamental factors to see if we can support the bull case there.

All about margin growth

Netflix, like many tech companies, saw slowing revenue growth last year and even posted some slight Q/Q declines. However, those days appear to have gone, and the company’s top line is back to moving in the right direction.

Catalysts include subscriber growth, including its ad tier, and cracking down on password sharing. Subscriber additions are robust once more, with 2.6 million added in July on top of 3.5 million in June. These kinds of gains aren’t likely to sustain given the current effort to build the subscriber base, but it is resetting the base number of subscribers higher. That’s critical for long-term margins, as Netflix needs higher revenue to boost margins.

Netflix continues to be a leader in customer engagement, which is important given how crowded the streaming entertainment space is these days.

Netflix shareholder letter

Streaming continues to grow in terms of market share, and Netflix is right at the top with YouTube in share of streaming hours. The company has been heavily investing in both purchased and original content for years in preparation for this, and those investments are paying off. Higher subs mean more investment cash flow for content, which means higher subs, and so on. Netflix has figured out how to win in streaming and that’s a big plus for the bull case.

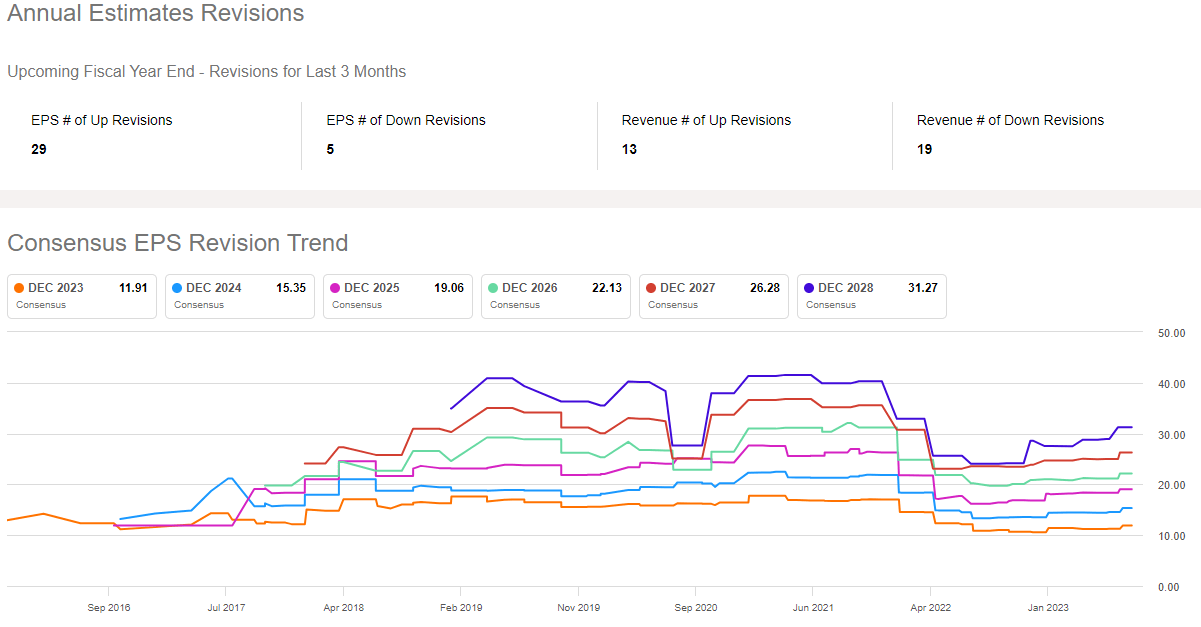

Now, estimates had gotten ahead of the company’s ability to execute during the pandemic, as many stay-at-home-friendly companies saw unrealistic expectations from investors. Netflix fit this description better than most, and its estimates for revenue and earnings were put at unsustainable levels.

Seeking Alpha

The good news is that we can see that estimates bottomed a while back, and are now moving higher. Revenue revisions are mixed, but that tends to happen at turning points in the cycle. EPS is much more bullish, with 29 of the past 34 revisions being higher. That’s due to margin expansion efforts, which we’ll look at now.

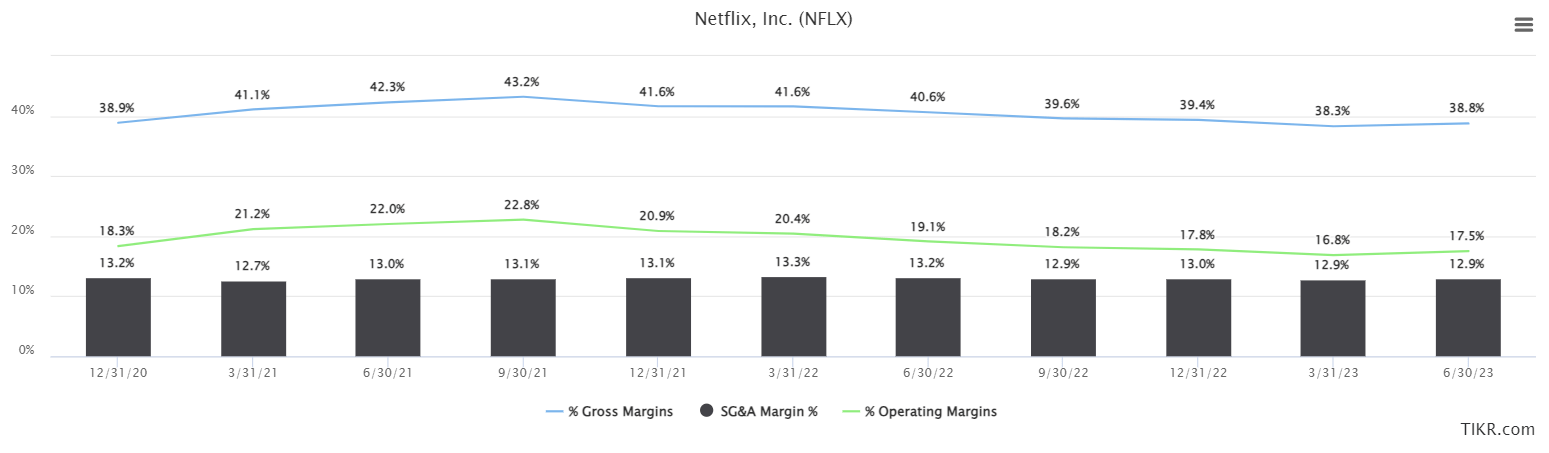

This is the trailing twelve-month data for the past few years, and we can see the company saw a boom in margins during the pandemic, only to have a reset since 2021.

TIKR

However, operating margins have leveled out, and with a focus on cost savings now at the forefront, any incremental revenue growth the company may experience will gradually boost operating margins. The double impact of spending discipline (the SG&A bars above) and revenue growth should see the green line above tick higher in the coming quarters. Revenue growth with operating leverage is a dream for investors as it means earnings grow much more quickly than revenue.

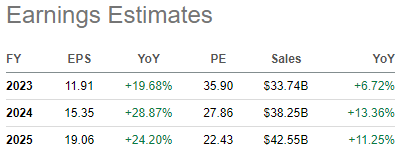

If we look at Wall Street’s estimates below, that’s exactly what’s being forecast right now.

Seeking Alpha

Sales growth is expected to accelerate in 2024/2025, and the operating leverage we just looked at is now slated to see EPS grow by ~25% or so for the next two years. And again, the more sales growth there is, the more operating leverage, the higher the EPS growth.

Slapping a ‘buy’ on Netflix

In case it wasn’t clear, I’m pretty bullish here. I think the pullback from July highs is just what Netflix needed, and risk-on sentiment appears to be back in the market in general. Netflix is seeing revenue growth turn higher at the same time as spending efficiencies hit the bottom line, which should lead to outsized EPS growth in the coming years. These, along with strong seasonality, gives us a “bullish trifecta” of factors that should drive the stock higher.

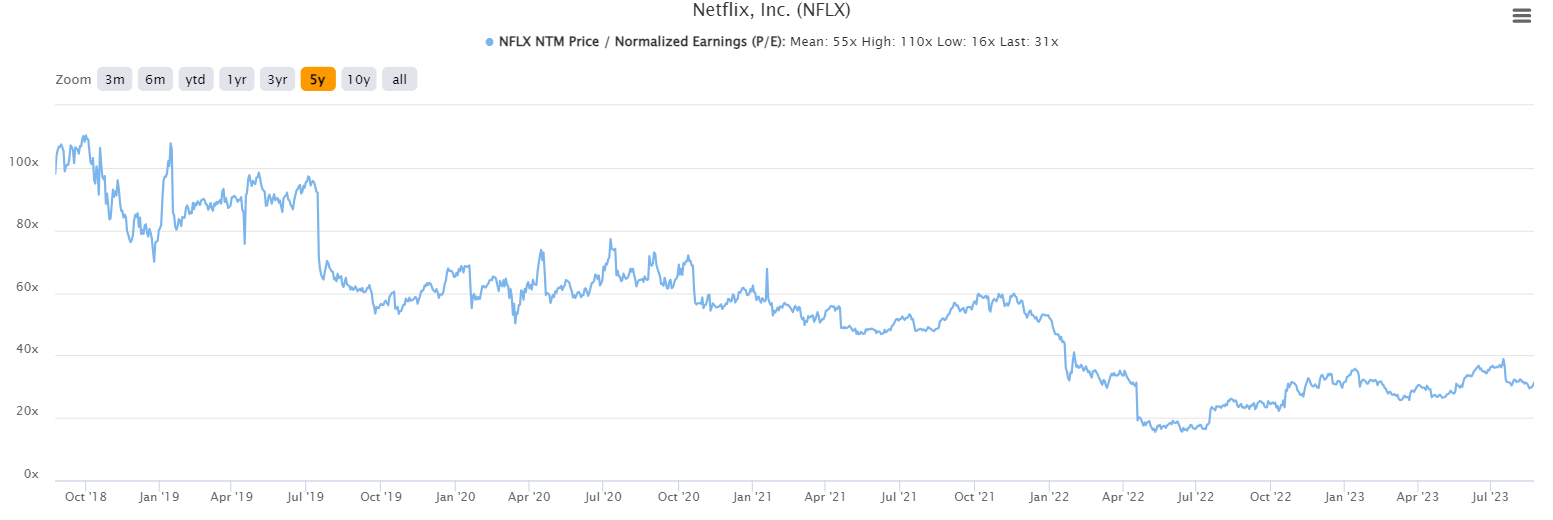

In addition to that, the valuation looks pretty good to me.

TIKR

The company’s forward P/E continues to come down, with the most recent valuation at 31X forward earnings. Keep in mind the stock has rallied hard this year, so the valuation reflects higher earnings estimates. As estimates continue to rise, Netflix will either get cheaper or ideally, the share price will continue to rise.

Either way, I see the stock as attractive here, and I’m long on the bull case that includes a breakout in the coming weeks and favorable seasonality trends heading into year-end.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of NFLX either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

If you liked this idea, sign up for a no-obligation free trial of my Seeking Alpha Marketplace service, Timely Trader! I sift through various asset classes to find the best places for your capital, helping you maximize your returns. Timely Trader seeks to find winners before they become winners, and keep you out of losers. In addition, you get access to our community via chat, direct access to me, real-time price alerts, a model portfolio, and more.