Summary:

- Netflix’s ad-supported plans and international growth are under-appreciated, likely driving revenue and profitability beyond expectations, with Q3 2024 earnings on October 17th.

- Netflix’s global reach and competitive pricing, combined with AI-driven content recommendations, position it for sustained growth and higher EPS in 2024 and 2025.

- Despite market saturation in the U.S., price increases and ad-supported plans may optimize profit margins, with risks from competition and content costs.

- Netflix shares are poised to reach new highs, potentially hitting $750 by year-end 2024 and over $800 in 2025, based on strong growth metrics.

bymuratdeniz

Netflix (NASDAQ:NFLX) is making new highs and its shares look ready to continue their ascension up the chart. Netflix’s position as the leader of the pack in streaming television remains underappreciated. Further, its global reach is underappreciated as a capacity to maintain better than expected growth in viewership and revenue streams that are likely to increase Netflix’s profitability. Moreover, Netflix’s addition of ad supported plans is likely to surpass expectations as the platform proves itself as an above-average deliverer of advertising.

Netflix is scheduled to deliver its Q3 2024 earnings on October 17th. The company has guided for revenue growth of about 15% for 2024, as well as Q3 revenue guidance of $9.7 billion. Netflix appears likely to have total revenue of $38-$39 billion for full year 2024 and free cash flow of around $6 billion. Last quarter, free cash flow came in at about $1.2 billion, which was below guidance and that miss was due to higher than forecast spending on new content and platform improvements.

I believe those expenditures are likely to drive increased revenue and profitability in coming quarters. Such results may be evident as soon as the reporting of Q3 earnings results, and especially if Netflix shows improving revenue from the continued successful launching of ad supported subscription plans. Further, Netflix has shown a capacity to increase the pricing of its ad-free subscriptions, while current pricing remains highly competitive.

Last quarter, Netflix added over eight million net subscribers, increasing its total number of subs to about 277.7 million. Monthly average revenue per user or subscriber (“ARPU”) remained highly differentiated by geographic region with the U.S. and Canada remaining highest at $17.17, followed by EMEA at $10.80, LATAM at $8.28, and APAC excluding China at $7.17. Netflix’s total revenue of $9.6 billion was up about 17 percent year over year, while its operating margin was 28.1 percent. I expect Netflix to have total 2024 earnings per share of about $19.25 and for 2025 EPS to be above $22.50. A key concern to Netflix reaching this target could be a strengthening dollar that would lower the contribution to international growth.

A major advantage of Netflix versus most of its peer competitors are that it lacks legacy film and television assets that continue to decline in value. Without such declining business segments, Netflix can maintain a singular focus on its streaming product. Moreover, Netflix appears to have already obtained a sufficient subscriber base to permit the company to develop content while maintaining profitability, where many competitors still lack a substantial enough base to support profitability.

It appears increasingly likely that Netflix’s ad-supported subscription plans will remain popular and profitable. A continuing driver of ad supported plans is likely to be Netflix’s continued measures to eliminate password sharing. Netflix is also expanding into live-streaming of sporting events, among other forms of live entertainment, where sports could improve engagement and provide a platform for higher cost advertising. At the same time, Netflix has refrained from competing for costly league sports programming that has been a cornerstone for many of its competitors. Rather, Netflix has increased its focus on developing exclusive content.

Netflix is also likely to be identified as a company that is benefitting from its use of artificial intelligence. Netflix is already known for its use of proprietary technology to push recommendations to its subscribers, as well as to determine new content initiatives. Netflix has a proven capacity at personalizing a tailored list of suggestions that both pushes new and existing content. Netflix’s ability to generate demand for older content could improve through AI optimization that might facilitate greater tailoring to the individual viewer.

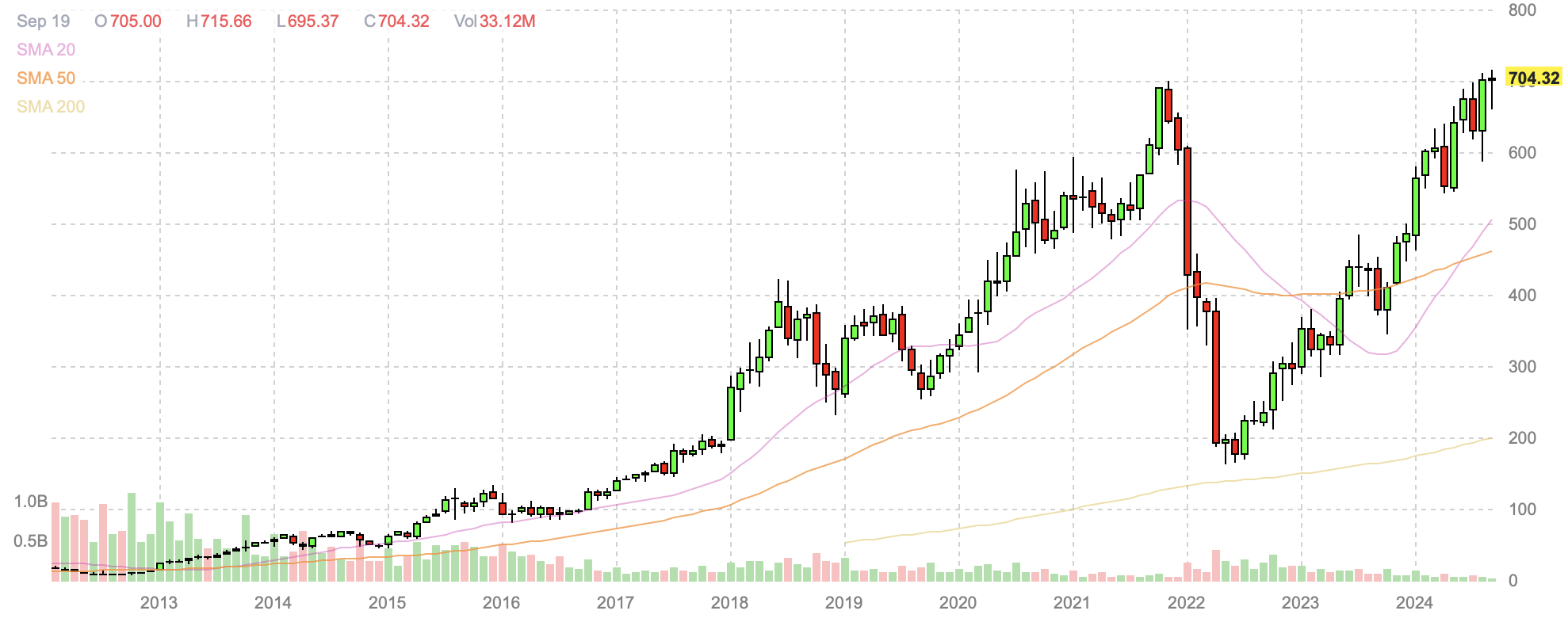

Netflix shares peaked in late 2021 at prices comparable to current levels, only to subsequently decline by about 70 percent. Since then, shares have slowly and somewhat steadily climbed back.

NFLX monthly candlestick chart (Finviz.com)

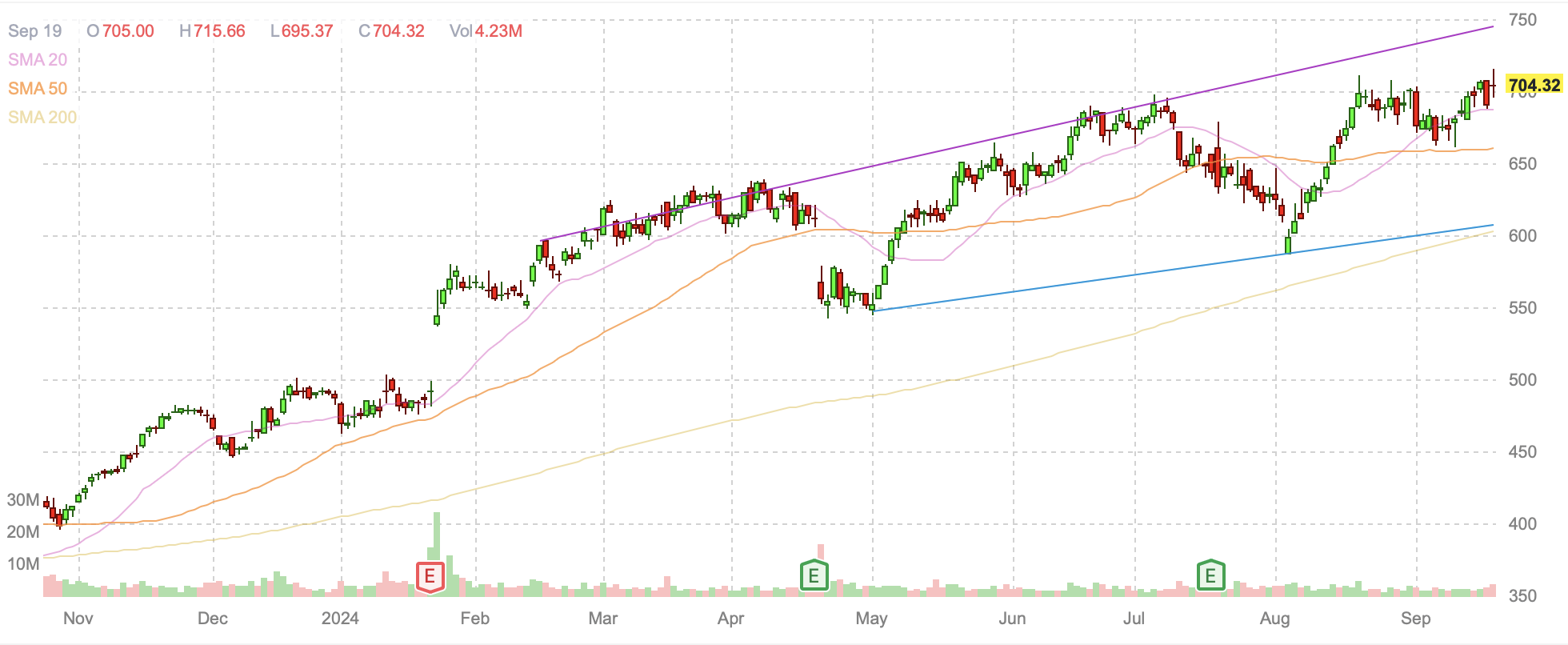

Over the last six months, Netflix has been in a wide and slightly ascending trading range. Netflix has touched both the top and bottom of this range a few times, and now, even though Netflix is roughly at its high, shares remain $40-$50 below the top of this ascending range.

NFLX daily candlestick chart (Finviz.com)

Netflix appears primed to reach the top of this range and potentially breach it and move higher when it reports earnings next month. I believe it will do so on the strength of growing its ad supported business, continued growth in its subscriber base, and greater discussion of how artificial intelligence is improving their product and processes. Most of Netflix’s subscriber growth going forward is likely to be international.

Risks

Netflix’s U.S. business has reached a level of maturity where while subscriber growth is possible, it is unlikely to substantially increase. Rather, Netflix may find existing subscribers switching from ad free to ad supported plans, which may be less profitable. This may not always be the case, as Netflix is still developing its capacity to service advertisers, and there is the potential for its ad supported plans to be the optimal choice from a profit margin perspective. In either case, given the level of saturation Netflix now has in the U.S. and Canada, price increases are likely to become a key driver of future revenue growth.

Netflix is starting to face a level of competition that it had not previously confronted, in that multiple well-funded owners of premium content are spending on their own streaming services. Further, several of these entities appear capable of accepting running their streaming service at a loss, or low margin, for at least a short while. Such will likely change if services cannot reach sufficient scale, which it appears only Disney+ has so far amongst the competition. While Netflix remains the leader of the pack, it is not clear that this position is forever insurmountable. Moreover, even if it remains the leader, its lead may be lessened by consumers opting for a mix of services where they exclude it, or subscribe on an intermittent basis.

Netflix is an expensive stock that is susceptible to significant drawdowns when the market declines, as well as when its earnings reports fail to meet expectations. Netflix now has multiple metrics that can disappoint, including subscriber growth, margins, free cash flow, and ARPU. Further, Netflix’s primary expense is spending on content. Whether they are acquiring content from others or creating it from scratch, the profitability of new content is generally a speculative endeavor. Netflix has done a good job of buying and creating content in the past, but that does not guarantee future success.

Conclusion

Netflix shares have been in a wide but ascending trading range for most of 2024, and are now trading close to their 2024 and all time highs. I believe that the growth and profitability of Netflix’s ad supported subscription plans is particularly underappreciated, and that both its growth and profitability will surprise the market when Netflix reports Q3 2024 earnings on October 17th. Netflix also appears capable of appreciating in advance of reporting earnings, and potentially testing the top of its pre-existing trading range, which would take it to the mid-$700s. As a result, I believe Netflix is likely to reach new highs in the near term and potentially go to $750 or higher before the end of 2024.

I expect Netflix to have total 2024 earnings per share of about $19.25 and for 2025 EPS to be above $22.50. If Netflix guides higher than this for 2025, it is likely that Netflix will trade above $800 in 2025. I base this on a 35 Price to earnings multiple, which is high for the market, but not for Netflix’s growth, free cash flow, and profit margins.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of NFLX either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.