Summary:

- Netflix’s transition from a premium growth stock is acknowledged, but the focus shifts to its robust free cash flow generation potential.

- At a forward free cash flow valuation of 23x, Netflix appears attractively priced, leveraging its dominant position as a streaming provider.

- Recent strategic moves, including the WWE partnership and a heightened emphasis on advertising, contribute to positive near-term prospects.

Mario Tama

Investment Thesis

Netflix’s (NASDAQ:NFLX) guidance for Q1 2024 provided investors with ample positive news. However, even as Netflix strives to describe that it has a “lot more room to grow”, the fact of the matter is that this is no longer a premium growth stock. But that’s not where the bull case is found.

The bull case for Netflix is that it’s already meaningfully free cash flow producing, and there is even more room to become a free cash flow machine.

Without any heroics, I estimate that Netflix is priced at 23x forward free cash flow. For what many consider to be the ultimate streaming provider, paying this valuation strikes me as a bargain.

Why Netflix? Why Now?

Netflix’s near-term prospects appear promising as the streaming giant continues to strategically expand its content portfolio and global reach. The recent partnership with WWE, including the acquisition of WWE Raw rights, signals Netflix’s commitment to diversifying its offerings with live sports entertainment. The addition of such content aligns with Netflix’s aim to enhance its live event programming and cater to a multigenerational fan base.

Furthermore, the company’s focus on improving its advertising business and the successful implementation of paid-sharing features position it well for sustained growth.

With a robust slate of content, a growing subscriber base, and an expanding presence in diverse markets, Netflix seems poised for positive momentum in the coming quarters.

However, Netflix faces near-term challenges too. The intensifying competition in the streaming industry poses a threat, with new entrants continually vying for market share. Indeed, Netflix always alludes to its competitors not necessarily being other streaming providers but rather other distractions, such as gaming and social media.

Furthermore, the maturation of the streaming landscape has led to heightened content acquisition costs and increased competition for exclusive rights. Moreover, as the average revenue per member (“ARM”) benefits from paid sharing begin to diminish in 2024, sustaining subscriber and revenue growth becomes crucial.

Additionally, while the WWE partnership enhances the sports entertainment segment, sports rights are anything but cheap. How much can Netflix truly pay to increase its sporting slate while balancing its determination to be a free cash flow printing machine?

Given this update, let’s now discuss Netflix’s financials.

Revenue Growth Rates to Improve, Slightly

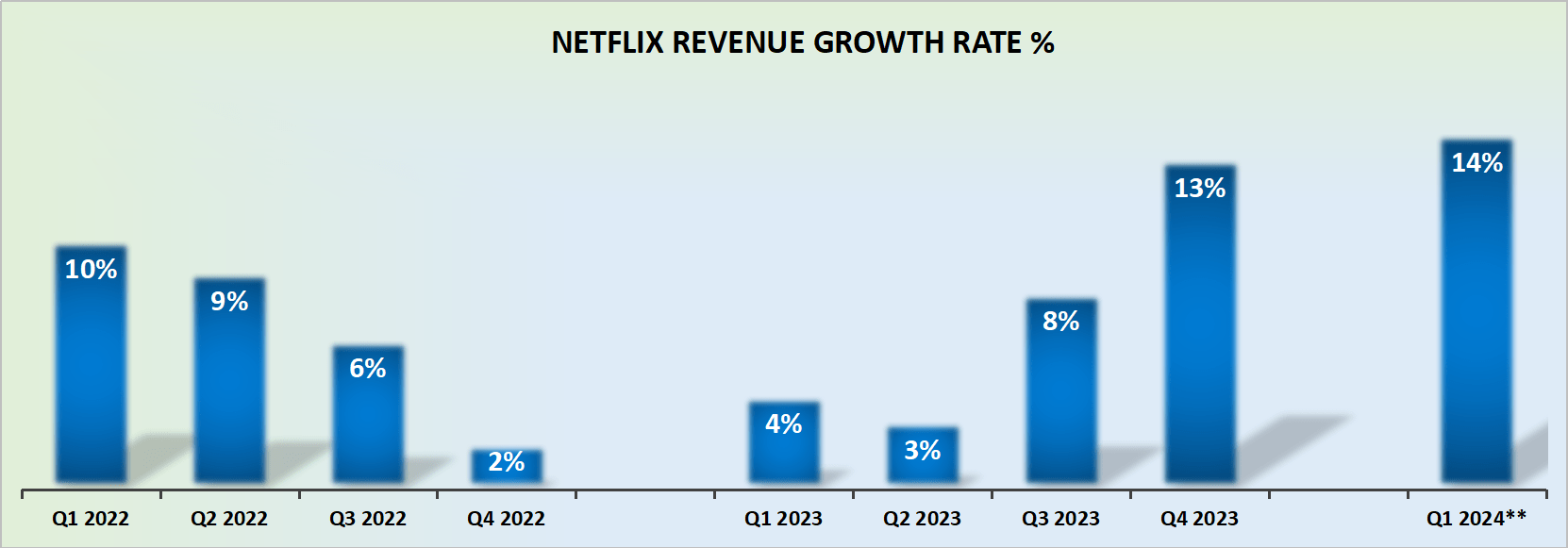

NFLX revenue growth rates

Netflix’s growth for Q1 2024 points to mid-double-digit growth rates. Put another way, the days when Netflix could be expected to deliver premium growth, meaning durable growth of +20% is now in the rearview mirror.

But of course, the fact that it can still be counted on for mid-teens isn’t something to be sneered at either.

That being said, we have to keep in mind that Q1 is up against a relatively easy comparable quarter. As Netflix progresses towards comparing against H2 of last year, it will be a tougher hurdle, that may ultimately see its revenue growth rates struggling to deliver 10% CAGR.

Furthermore, note below that Netflix’s revenue beats have in the past several quarters been moderate, with less than 2% revenue beats in the best case, and a slight miss the other half the time.

SA Premium

Therefore, I believe we can surmise that what we see here, is all there is. However, that’s not where the bull case is found for Netflix. That we discuss next.

NFLX Stock Valuation — 23x Forward Free Cash Flow

Netflix has now demonstrated that it can generate ample free cash flow. More specifically, Netflix yielded nearly $7 billion of free cash flow in 2023. Consequently, when Netflix guides for its free cash flow to dip lower in 2024 to around $6 billion, investors are not perturbed, given that this management team has proven itself time and time again to be terrific capital allocators.

This means that, even though the free cash flow in 2024 will be less than 2023, there’s ample reason to expect this upcoming use of cash to deliver stronger free cash flows in the next few years.

NFLX Q4 2023

And to reassure investors that this is the case, consider the continued progression in profit margin expansion expected for Q1 2024, at slightly more than 26%.

Given that Netflix’s operating margins are expected to expand by a whopping +500 basis points in 12 months, this leads one to believe that in the long-run, Netflix could perhaps end up delivering 30% operating margins! This is for a business that not long ago had all kinds of questions as to whether it could in actuality actually deliver any significant free cash flows.

Therefore, I believe that if we presume that in 2025 Netflix will deliver approximately $43 billion with 23% free cash flow margins, this leaves Netflix priced at 23x forward free cash flow. A figure that I believe many reasonable investors will recognize as being very attractive.

The Bottom Line

In wrapping up my assessment, Netflix’s investment thesis paints a nuanced picture. While the acknowledgment of a transition from a premium growth stock is evident, the real appeal lies in the company’s robust free cash flow generation potential and the opportunity to fortify this aspect further.

I believe that there’s going to be more value investors chasing this stock going forward, since paying 23x forward free cash flow for Netflix seems attractively priced, particularly considering its commanding position as a streaming provider.

The recent strategic moves, like the WWE partnership and emphasis on advertising, contribute to what I see as positive near-term prospects.

Despite grappling with challenges such as intense streaming competition and the changing streaming landscape, Netflix’s proven ability to navigate these obstacles, coupled with its adept capital allocation, bolsters my confidence in this stock.

The anticipation of sustained growth, supported by improving profit margins, positions Netflix as an enticing investment choice.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Strong Investment Potential

My Marketplace highlights a portfolio of undervalued investment opportunities – stocks with rapid growth potential, driven by top quality management, while these stocks are cheaply valued.

I follow countless companies and select for you the most attractive investments. I do all the work of picking the most attractive and profitable businesses.

Investing Made EASY

As an experienced professional, I highlight the best stocks to grow your savings: stocks that deliver strong gains.

- Honest and reliable service.

- Hand-holding service provided.

- Very simply explained stock picks. Helping you get the most out of investing.

- Balanced arguments.