Summary:

- Netflix’s shares rose 13.7% in after-hours trading after the company reported strong financial results for Q3 2023.

- The company saw robust growth in membership, with 247.15 million global paid members, and increased revenue per user per month.

- The successful launch of the live action adaptation of the manga series One Piece contributed to Netflix’s success and garnered over 62 million views globally.

- The company finally looks appealing based on all of this data and more.

Wachiwit

After the market closed on October 18th, shares of pure-play streaming giant Netflix (NASDAQ:NFLX) skyrocketed, rising around 13.7% in after-hours trading. This move came about after the company reported financial results covering the third quarter of the company’s 2023 fiscal year. In addition to matching estimates when it came to revenue, the company comfortably exceeded the earnings per share that analysts had forecasted. Of the other data reported by the company was incredibly bullish as well. Add on top of this some price increases for some of its offerings, and there is a lot to be bullish about.

Those who follow my work closely will probably know that this kind of statement from me is quite significant. I have written about the streaming giant multiple times in the past. And in almost every case, I have rated the company a ‘hold’ to reflect my view that it’s not a horrible prospect, but that it’s also far from a great one. My attitude is changing, however, based on recent financial performance. And although there are many parts at play here, central to this shift in thinking is perhaps the most famous pirate story ever written.

Netflix found the One Piece

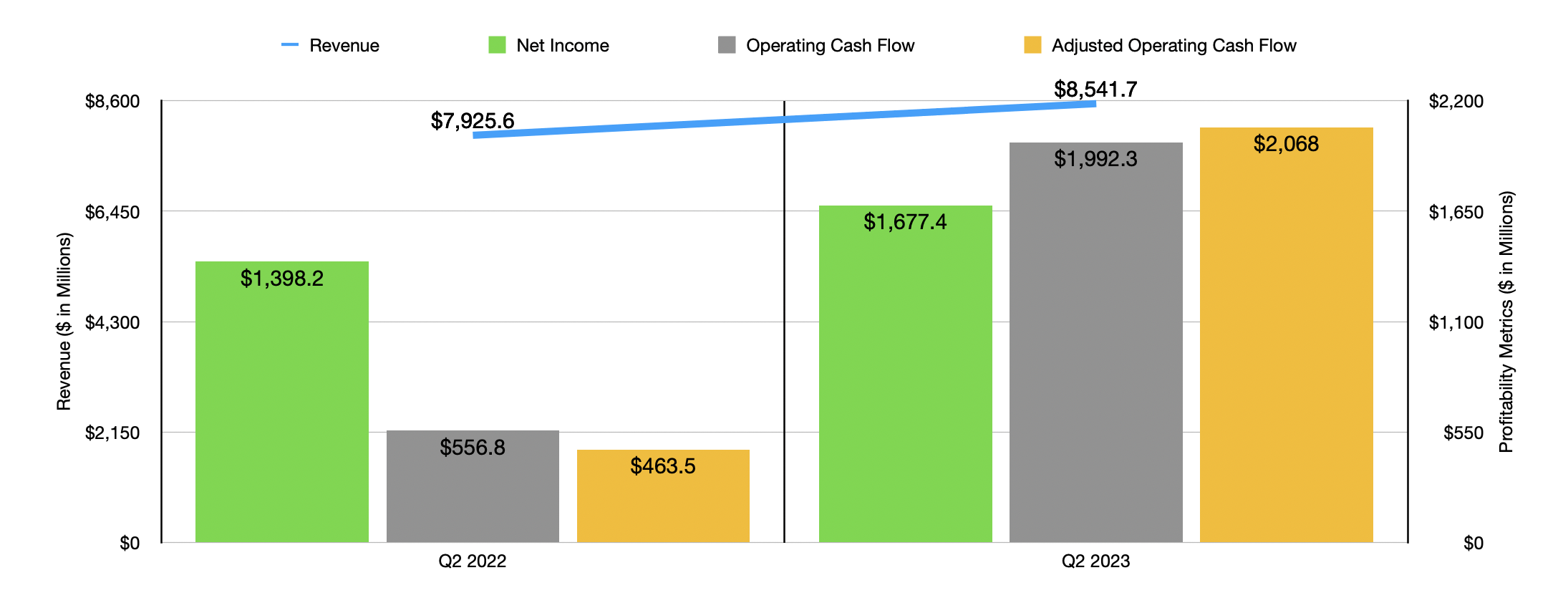

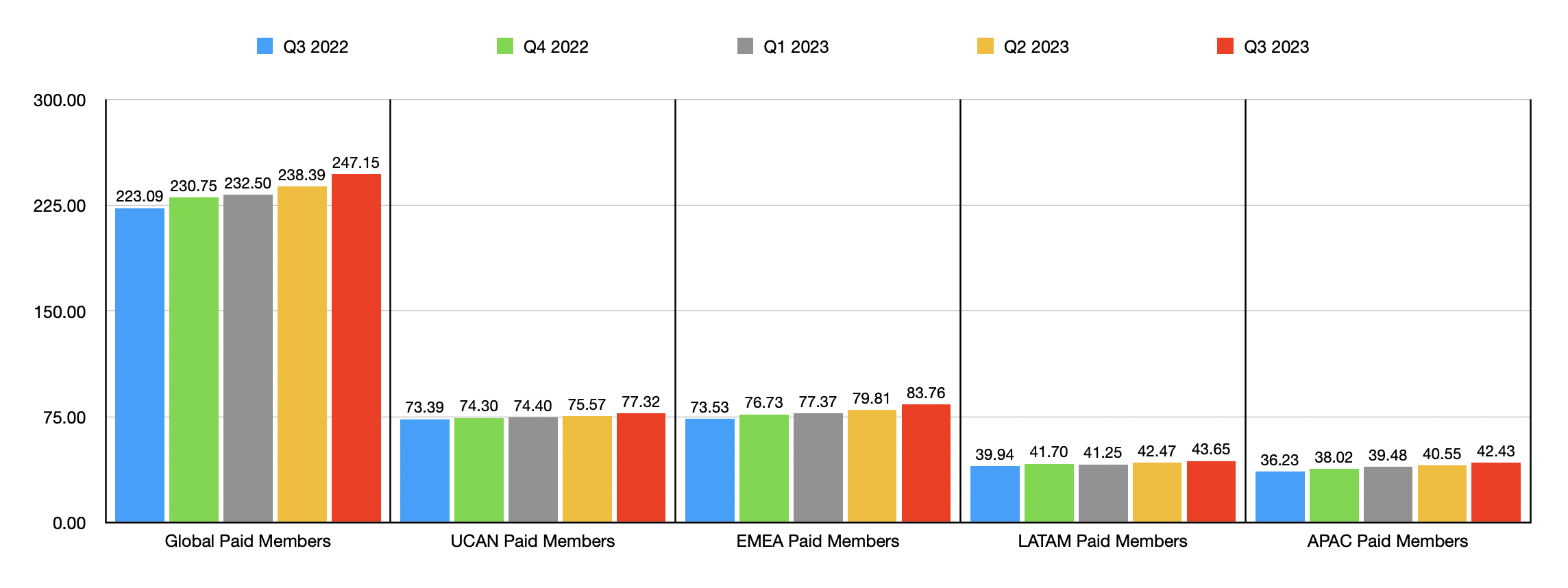

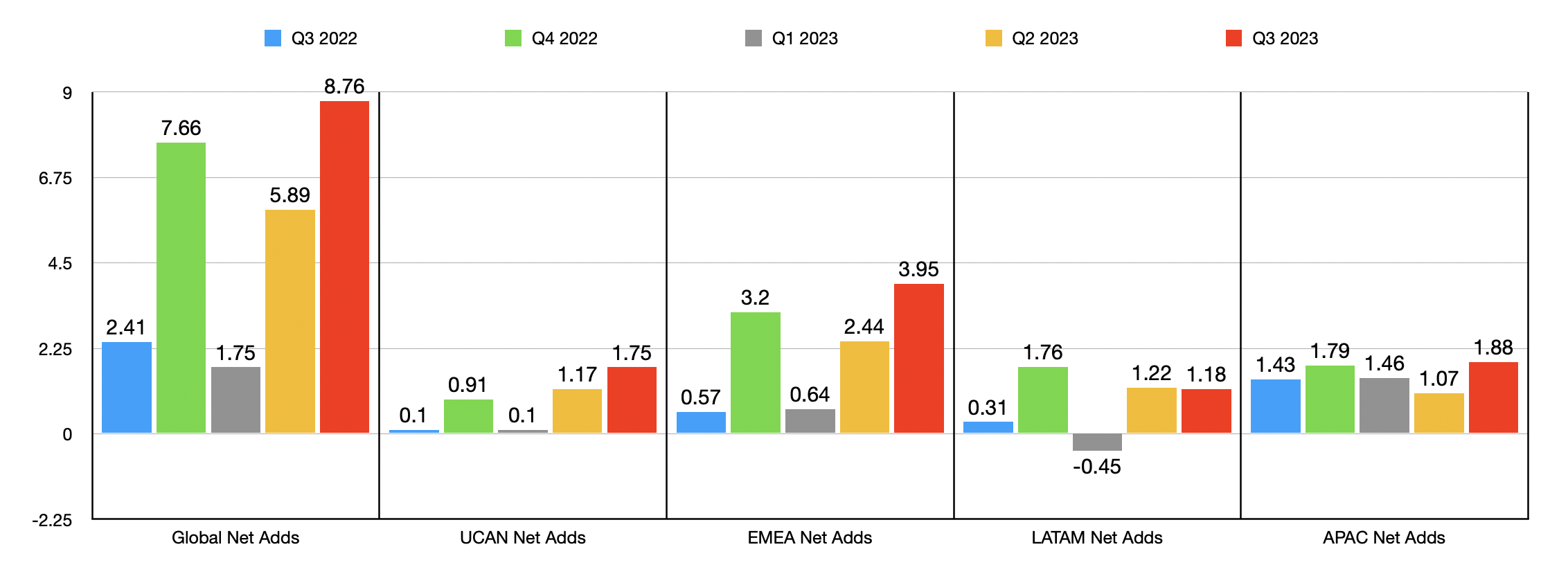

After the market closed on October 18th, the management team at Netflix announced financial results covering the third quarter of the company’s 2023 fiscal year. Revenue for the quarter came in strong, hitting $8.54 billion. In addition to matching what analysts forecasted for the quarter, this amount of revenue translated to a 7.8% increase over the $7.93 billion the company reported the same time last year. This increase in sales was attributable to robust growth in membership on the company’s platform. At the end of the quarter, the firm boasted 247.15 million global paid members. This is 8.76 million higher than the 238.39 million reported only one quarter earlier and it is up 10.8%, or 24.06 million, compared to the 223.09 million reported the same time last year.

Author – SEC EDGAR Data

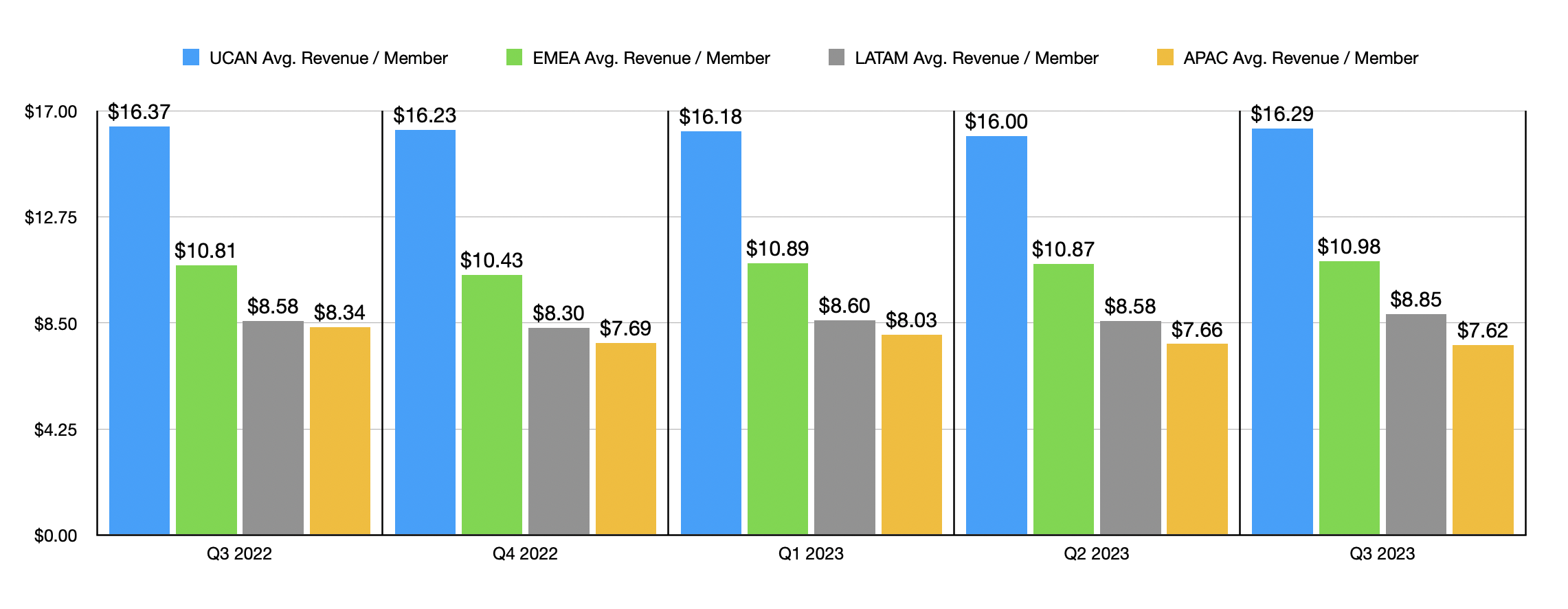

The company saw growth across the board. In the US and Canada region, the company added 1.75 million new members in the course of a single quarter. This took the total user base up to 77.32 million for the region. Average revenue per user per month also increased, climbing from $16 to $16.29. Although that may not sound like much, when applied over the span of a single three-month window, and using the most recent number of users provided, this translates to an extra $67.3 million in revenue per quarter. Growth was strong elsewhere also. In the EMEA (Europe, Middle East, and Africa) markets, subscribers hit 83.76 million. That’s up 3.95 million from the same time one year earlier. Average revenue per user per month also managed to grow from $10.87 in the second quarter to $10.98 in the third quarter. The company reported a 1.18 million member increase across the LATAM (Latin America) region, taking the user count up to 43.65 million. This was accompanied by a rise in average revenue per member per month from $8.58 to $8.85. And finally, in the APAC (Asia/Pacific) region, the company added 1.88 million paying members, taking the total number to $42.43. This was the only area in which pricing weakened sequentially, dropping from $7.66 to $7.62.

Author – SEC EDGAR Data

At the end of the day, content is what drives users to a platform like Netflix. And it was during the third quarter that the company had some really major wins under its belt. Most notable was the widely acclaimed launch of its live action adaptation of the manga and anime series One Piece. For those who don’t know, the series is about a pirate named Monkey D. Luffy and his crew as they search for a legendary treasure called the One Piece. Even though this may come across as some obscure story to many here in the western world, the series is actually the second best selling comic book series in history, with over 516.5 million volumes sold since its launch in 1997. That has allowed it to eclipse Batman and places at second only to Superman at somewhere around 600 million copies. One Piece is known as being in its final saga, but it likely will still take a few years for that to conclude. It took Superman around 15,000 issues to get where it is today. By comparison, One Piece only recently came out with its 1,095th chapter and its 106th volume. So it certainly will surpass Superman at some point. In addition to that, the anime is currently on episode 1,079.

Author – SEC EDGAR Data

Personally, I have been reading the manga religiously since late in the Amazon Lily arc. But to many, the live action adaptation was their first introduction to that world. And while there was significant concern from the anime and manga community about the potential success of such an adaptation, justifiably so because of the poor history of adaptations due to budget issues and what has been perceived as a massive amount of disrespect levelled at source material, the end result for the first season of One Piece was fantastic. According to Netflix, the series has already seen over 62 million views globally. It was the first ever English title that the company had that debuted in the number one spot in Japan. And it stood at the number one spot on the company’s Top Ten list for three weeks in a row. Of course, this didn’t come easy. The series had an estimated budget of $18 million per episode. But neither that nor the seven years that it took to take it from an idea to an 8-episode show prevented its success, nor the subsequent news that it has been renewed for a second season.

Author – SEC EDGAR Data

Of course, One Piece wasn’t the only piece of content that drove excitement to the Netflix brand. The company had other successful series during the quarter, such as season three of The Witcher, season two of Top Boy, season four of Sex Education, and Love at First Sight. The company also had major local language victories, including ones in Germany, Brazil, India, and France. Some of the greatest success that it has had come from not original content, but instead from licensed content. Suits, for instance, continues to perform well, resulting in over 1 billion view hours on the platform globally during the 12 weeks beginning in late June. This is in spite of the fact that the show came to an end back in 2019.

Netflix

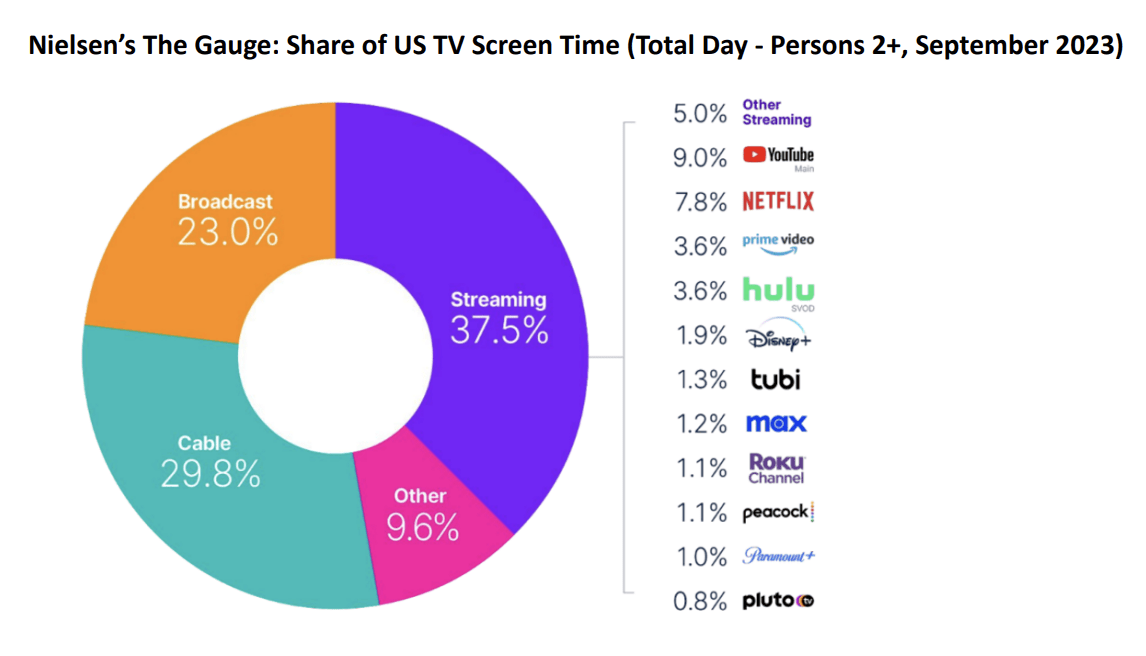

Management did provide some other interesting data. For instance, during the month of September of this year, in the U.S. market, streaming was the primary means of video screen time for individuals. It accounted for 37.5% of all such screen time. 7.8% of all screen time, or approximately 20.8% of all streaming time, involved the Netflix platform. That placed it second only to YouTube at 9%. This is up from 7.6% reported the same time last year, so the company is growing its market share. Though I have to say that I continue to be proud of The Walt Disney Company (DIS) because its Disney+ and Hulu platforms are, combined, keeping pace with the market share growth that Netflix is achieving.

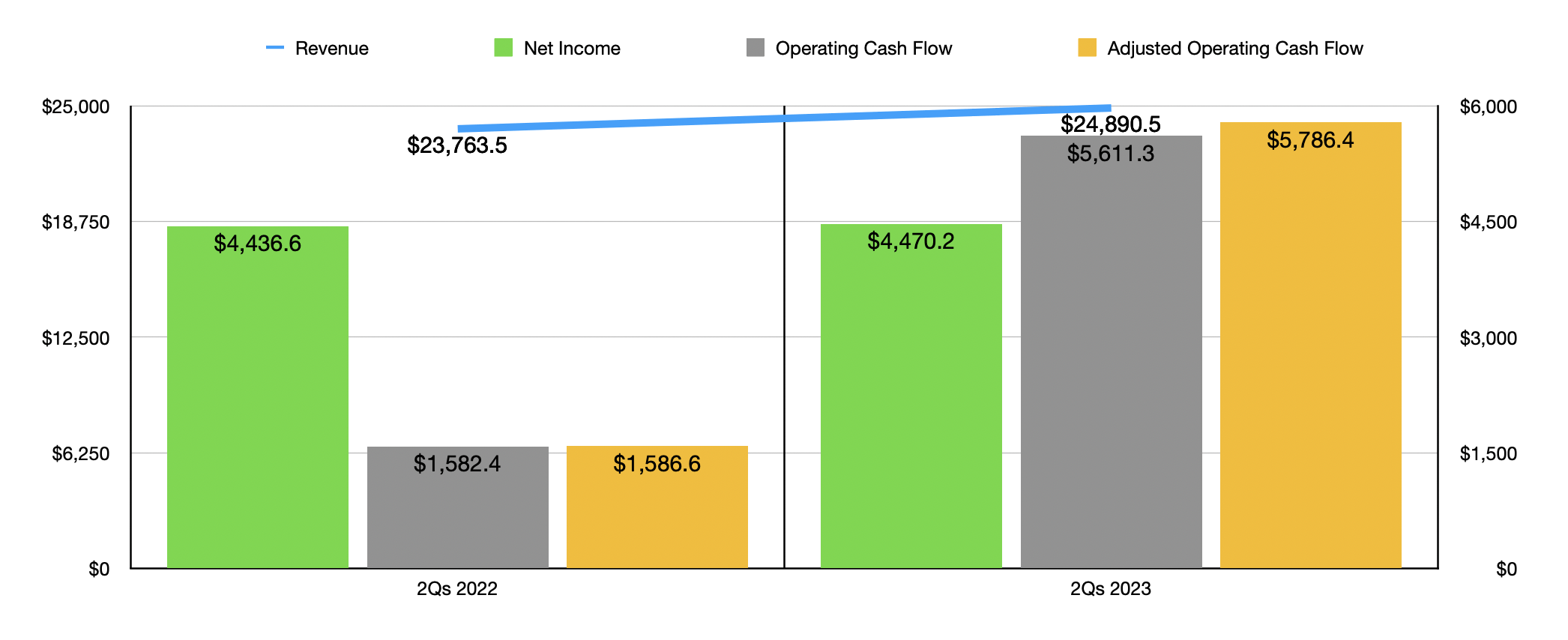

On the bottom line, Netflix is doing quite well also. Earnings per share came in at $3.73. This represents a nice increase over the $3.10 per share that the company reported the same time last year. It’s also $0.23 per share above what analysts were anticipating. This means that the company went from generating net profits of just under $1.40 billion in the third quarter of 2022 to $1.68 billion the same time this year. Operating cash flow also improved, shooting up from $556.8 million to $1.99 billion. Even if we adjust for changes in working capital, we would get an increase from $463.5 million to $2.07 billion. As you can see in the chart below, the robust performance generated in the third quarter of this year was instrumental in pushing up performance for the year as a whole so far.

Author – SEC EDGAR Data

Management is so bullish about the situation that the company decided to buy back $2.5 billion worth of stock during the most recent quarter. That’s approximately 6 million shares. This means that only $1 billion incapacity remained under the company’s existing share buyback program. So in response to that, the firm increased its plan by another $10 billion. Guidance was also pushed higher for this year. Management is now forecasting free cash flow of $6.5 billion. That compares favorably to the $5 billion previously forecasted. However, about $1 billion of that change is because of reduced cash content spend resulting from the WGA and SAG-AFTRA strikes. The former of these has now concluded, but the latter is still proving to be a problem. That could cause further revisions for the company. But for now, they are still forecasting $13 billion in content spending this year, which would be down from the $14 billion previously forecasted. Next year, however, they looked to hike that spending up to $17 billion. For those who are worried about cash flow, it’s important to note that management said that they still expect ‘very substantial positive free cash flow’ in 2024.

Some of this optimism certainly centers around some of the pricing changes that the company has implemented. For instance, the ad supported programs the company previously launched seemed to be doing quite well. Management claimed that adoption of the ads plan continues to grow, with total plan membership up almost 70% in the third quarter compared to the second quarter. In fact, 30% of sign-ups in the countries in which it has such a plan now fall under that category. Across the US, UK, and France, the company has also decided to increase pricing for the Basic plan from $9.99 per month to $11.99 per month. This is an old plan that individuals were grandfathered into that is only available for those who have kept that plan since the company retired it. Meanwhile, the Premium plan will be increased from $19.99 per month to $22.99 per month. If you check on the company’s US website, you will notice that these changes have already taken effect.

Takeaway

Based on all the data provided, I can only say that Netflix is doing a really solid job. It might be the fanboy in me, but I do believe that a good portion of the success recently stemmed from the successful adaptation of One Piece. At the very least, it has proven to be a massive win for the business and, in turn, its shareholders. There obviously were other pieces to the pie as well and, when combined, it’s clear that the enterprise is in far better shape than it has been in the past. Given these developments, I have decided to increase my rating on the stock from a ‘hold’ to a ‘buy’.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of DIS either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Crude Value Insights is an exclusive community of investors who have a taste for oil and natural gas firms. Our main interest is on cash flow and the value and growth prospects that generate the strongest potential for investors. You get access to a 50+ stock model account, in-depth cash flow analyses of E&P firms, and a Live Chat where members can share their knowledge and experiences with one another. Sign up now and your first two weeks are free!