Summary:

- We’re upgrading Netflix, Inc. to a hold.

- Consistent with our negative thesis, Netflix management confirmed the longer growth runway for its ad tier and softer margins at the investor conference this week.

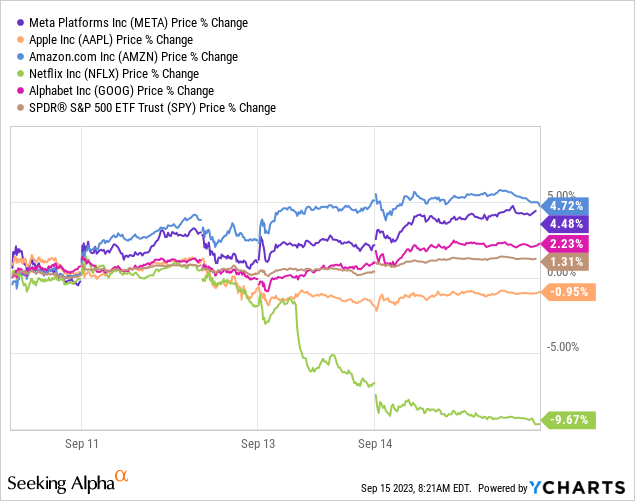

- The stock has traded down over 10% this week alone, underperforming the S&P 500 by 11%.

- While we still don’t see any major growth catalysts in 2H23, we believe the stock has now priced in most of our negative investment thesis.

- We are now less negative on the stock but would still recommend investors to remain on the sidelines.

simpson33

We’re upgrading Netflix, Inc. (NASDAQ:NFLX) to a hold. We were previously sell-rated on the stock, as we believed the market was too optimistic about the sharing crackdown and ad tier driving revenue growth in the near-term. We now think the stock has priced in our negative thesis; Netflix is down 10% this week alone, underperforming the S&P 500 by 11% and underperforming the FAANG Group. We’re constructive on password-sharing sign-ups and the ad tier, but we don’t think either will boost revenue growth in the near-term due to their longer growth runway and current macro uncertainty. Management finally confirmed our expectation in this week’s Bank of America Securities Media, Communications and Entertainment Conference; CFO Spencer Neumann noted that “we’re still in the crawl of the crawl, walk, run.” We’re less negative now that the headwinds are priced into the stock, but we see no catalyst driving growth in the back end of the year. We recommend investors remain on the sidelines.

The following graph outlines Netflix’s stock performance against the FAANG Group and S&P 500.

YCharts

In the crawl of the crawl, walk, run

The word “healthy” was thrown around a lot on the call, with Neumann noting that the company sees a “healthy” mix from the ad tier and paid sharing. The catch, however, is that management expects both to be mid-to-long-term growth catalysts instead of revenue boosters in the near-term. Netflix has been struggling to reaccelerate revenue growth in FY23; the company missed revenue estimates for the past two quarters and guides for $8.52B in revenue for 3Q23, lower than the consensus of $8.68B. Given the slower revenue growth, management also guides for softer margins for FY23. Operating margins peaked at 21%, and now the company is working in the 18% to 20% range.

Here’s a breakdown of paid-sharing and the ad tier:

Paid Sharing –

Netflix had +100M users borrowing accounts rather than paying and prepared to roll out the crackdown on sharing to 80% of its revenue base. We’re constructive on Neumann reporting a muted cancelation reaction, as it means there’s a better retention base for existing users. Still, we continue to believe the paid sharing won’t be able to generate material revenue growth in the current macro environment; as management phrased the situation, “It’s not super sexy.”

Ad tier –

The company introduced the ad tier in November of last year, understanding the lucrative opportunity in advertising as ad revenue accounts for the bulk of revenue for Paramount (PARA), Alphabet (GOOGL), and Amazon (AMZN), among others. We think Netflix’s customer base makes it well-positioned for robust ad revenue growth, but we see a longer growth runway for Netflix’s ad tier based on two factors. The first is the macro headwinds causing advertisers to tighten budgets. And the second is the lack of scale in Netflix’s ad tier. Management noted the second factor on the call this week, stating, “We have to scale the reach of our ad’s tier… advertisers want a scaled solution.” Management is now seeing spinoff subscribers favoring ad-free viewing, which is less than ideal for Netflix’s ad business, and hence, scaling the ad tier should help improve growth. We think the ad tier growth story is something we’ll see in FY24, not before.

Valuation

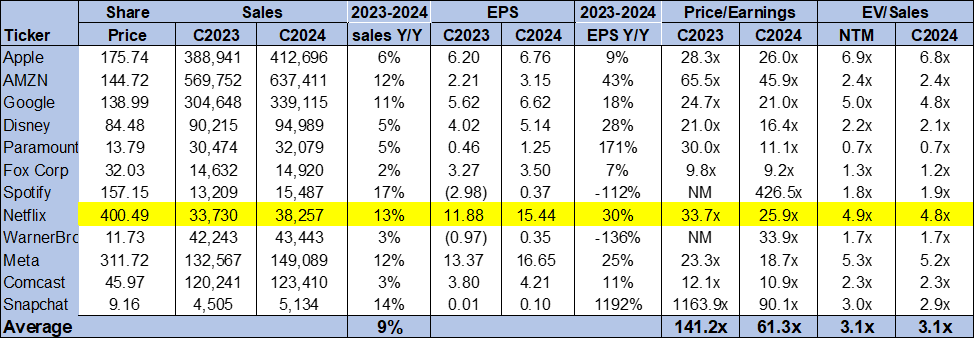

The stock is trading above the peer group average at 4.8x EV/C2024 Sales compared to the peer group average at 3.1x. On a P/E basis, the stock is trading at 25.9x C2024 EPS $15.44 versus the peer group average of 61.3x. We don’t see attractive entry points into the stock at current levels. We don’t think valuation is justified against the company’s near-term growth rate.

The following chart outlines NFLX’s valuation against the peer group.

TSP

Word on Wall Street

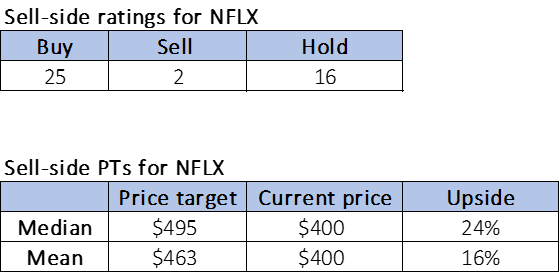

Wall Street is bullish on the stock. Of the 43 analysts covering the stock, 25 are buy-rated, 16 are hold-rated, and the remaining are sell-rated. We think the market is getting ahead of itself, expecting Netflix to reaccelerate to pandemic-level growth. While we believe the stock has recovered to healthy demand from post-pandemic lows, we don’t see any growth catalyst driving outperformance in the near-term.

The stock is currently priced at $400 per share. The median sell-side price target is $495, while the mean is $463, with an upside of 16-24%.

The following charts outline NFLX’s sell-side ratings and price targets.

TSP

What to do with the stock

We’re upgrading Netflix to a hold. The stock has priced in our negative thesis; the stock has dropped from a 52-week-high $485 to $400.49. While we think the market now expects slower revenue growth in 2H23, we still don’t see any catalyst counteracting the slowdown in the near term due to macro uncertainty. We are now less negative on the stock but would still recommend investors to remain on the sidelines.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Appreciate your interest in our tech coverage. If you want first-hand access to our analysis of software/hardware and semiconductor spaces, best ideas within the current macro backdrop, and our coveted research process, we hope you’ll take a 2 week free trial of Tech Contrarians, our Investing Group service. The first wave of subscribers gets a significant lifetime discount on annual subscriptions after the 2 week free trial so we hope to see you in our group soon.