Bubble implosions are predictable in their magnitude but not in their timing.

NextEra Energy has a tailwind of high base rate growth and a headwind of higher interest rates.

We tell you how the two fit into our valuation model and how we would play it.

We also give our outlook for 9.6% yielding corporate units.

RyanJLane/E+ via Getty Images

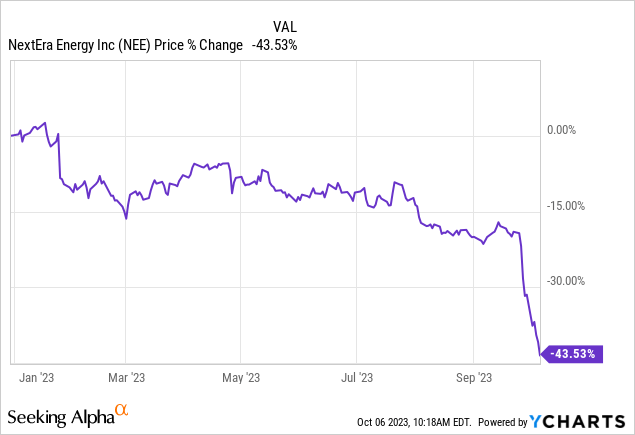

It always seems easy with 20/15 hindsight. The ZIRP (zero interest rate policy) bubble was designed to suck in the most number of investors and leave the battlefield filled with casualties as it ended. NextEra Energy Inc. (NYSE:NEE) was no different. The adjustment period was swift and the reckoning remorseless.

We have covered NextEra Energy Partners LP. (NEP) previously and saw how NEE is likely to take this into its fold eventually. Today we examine NEE and see whether the damage has been done to allow for a good entry.

The Business

NextEra Energy’s primary business is the regulated utility unit, FPL, in Florida. The complementary assets are the rapidly expanding renewable energy business. The regulated side has generally seen lenient oversight and high allowed returns on equity. It also has a some of the lowest rates for customers allowing NextEra legroom to increase its fees without blowback. The renewable expansion has been one of the most aggressive we have seen amongst utilities. While all utilities have moved to expand renewables, NextEra was the earliest and the most ambitious. It backed wind energy early on and likely had the first mover advantage when the best sites were available and construction costs were low. Its recent expansion has focused on solar and utility level energy storage. These multi-year plans have given it some of the fastest growth rates and there are no immediate plans to dial things down. The company plans to invest about $60 billion over the next few years and aims to grow their base rate at almost double-digit clips.

Valuation

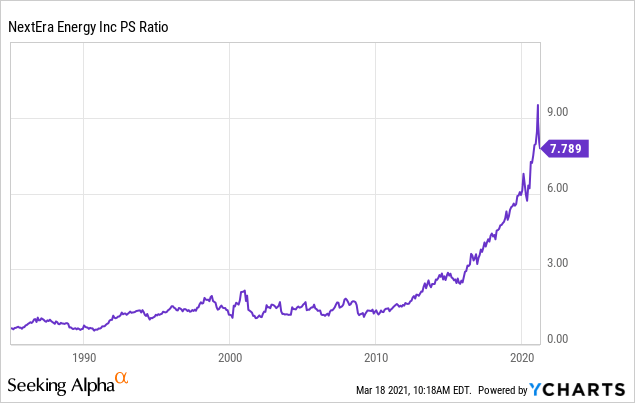

Sometimes you look at a chart and wonder what exactly the rest of the market is thinking. With NEE the multiples were so silly that we did not even bother to comment beyond a passing mention in our article on (QCLN).

NextEra Energy Inc. (NEE) has a similar bubble valuation and at 7.8X sales, destined to give negative returns as far as the eye can see (and beyond).

We used a rather obscure valuation metric there. Pretty much no-one uses price to sales for utilities. But we did it simply because it almost hit the magical 10X revenues number. That number is something that the former CEO of Sun Microsystems poked fun at, even in the context of extremely fast growing technology companies.

At 10 times revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends. That assumes I can get that by my shareholders. That assumes I have zero cost of goods sold, which is very hard for a computer company. That assumes zero expenses, which is really hard with 39,000 employees. That assumes I pay no taxes, which is very hard. And that assumes you pay no taxes on your dividends, which is kind of illegal. And that assumes with zero R&D for the next 10 years, I can maintain the current revenue run rate. Now, having done that, would any of you like to buy my stock at $64? Do you realize how ridiculous those basic assumptions are? You don’t need any transparency. You don’t need any footnotes. What were you thinking?

Source: Medium

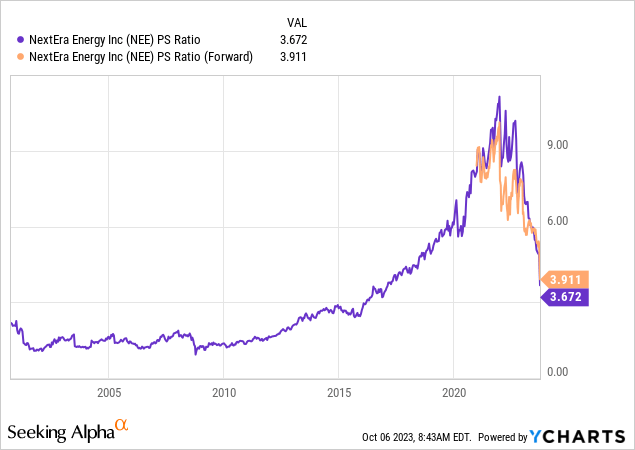

So when NEE had briefly crossed 9.0X sales (and eventually crossed 10X mark as well) because it was investing in renewables, you knew right then this was going to have an epic ending. Today that multiple has contracted back down, though still well above its historic range.

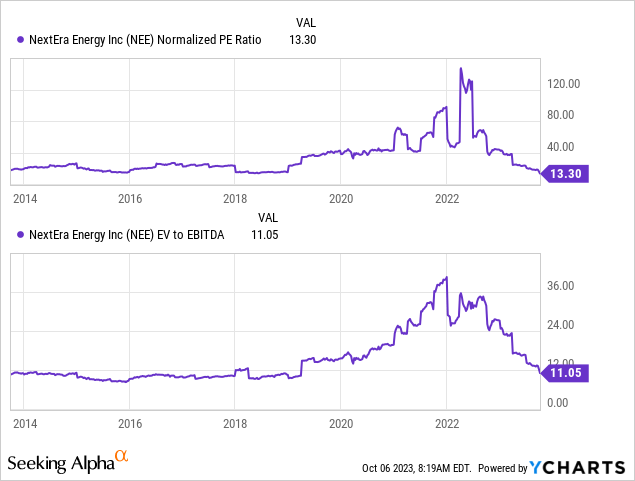

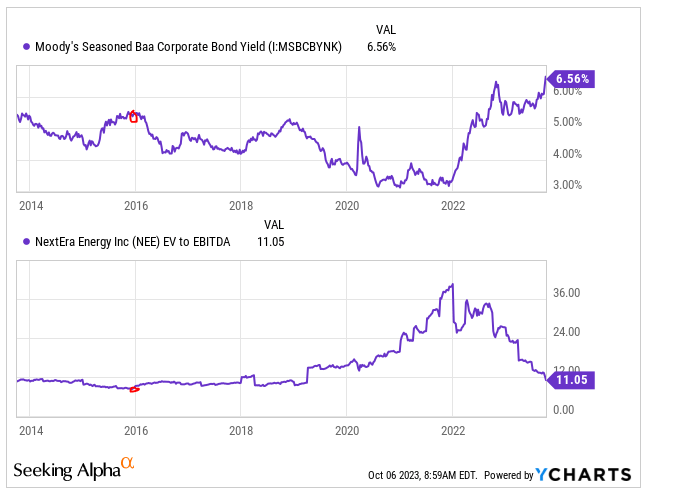

The two metrics might be considered cheap of the ZIRP era but are nowhere near cheap for 5.5% short term interest rates. You are also now getting 6.56% yields on 10 year investment grade corporate bonds. We will note that with a 5.25% interest rate on BAA bonds in 2016, NextEra traded as low as 9.7X EV to EBITDA.

Y-Charts

Is it unreasonable to assume a similar valuation with corporate bond yields more than 130 basis points higher? Absolutely not. In fact, if bubbles should teach you one thing, it is that we see undervaluation levels at the bottom. We are nowhere in the postal code of that.

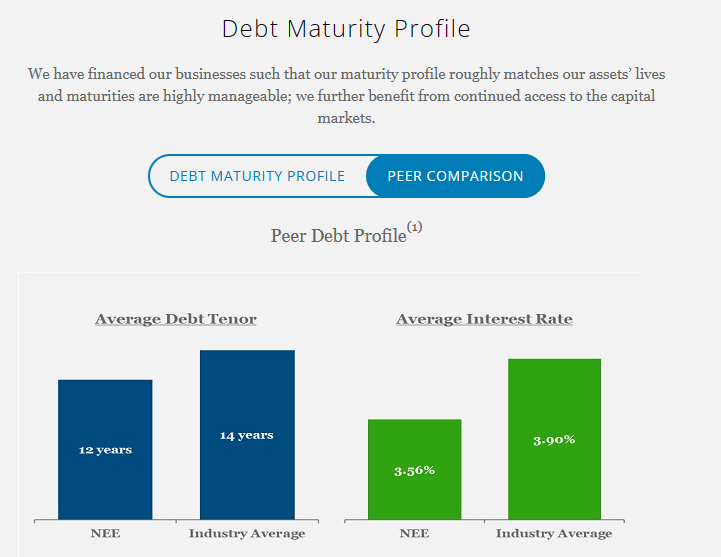

The debt maturity profile of NEE is also an interesting case study. The 12 year average debt tenor and the interest rates locked in are about average.

NEE Presentation

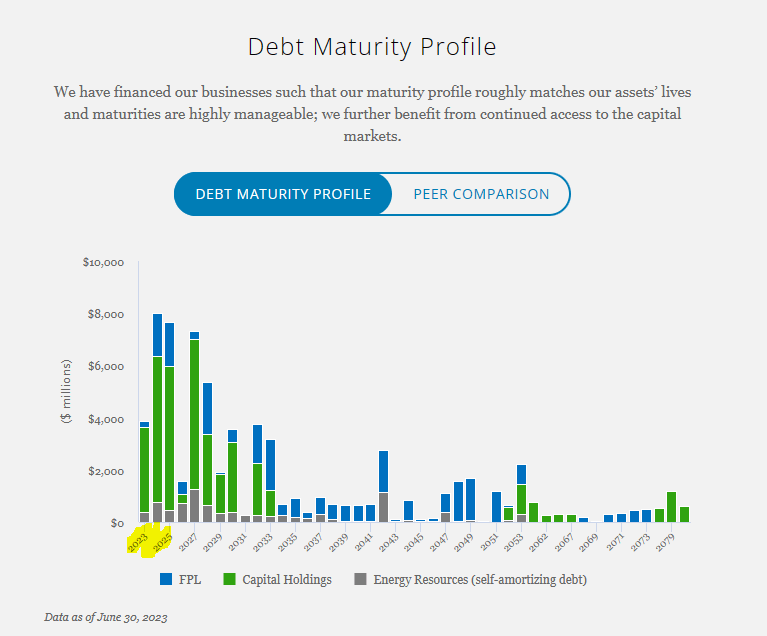

But NextEra has a very heavy debt roll in the next 3 years.

NEE Presentation

NEE has some massive hedges in place on the interest rate front, though the combination of these rolls and new debt issuance will far exceed the $20 billion in hedges over the next 5 years. If you assume the weighted average interest rate creeps up to 5% over the next 5-7 years you create a headwind to earnings growth.

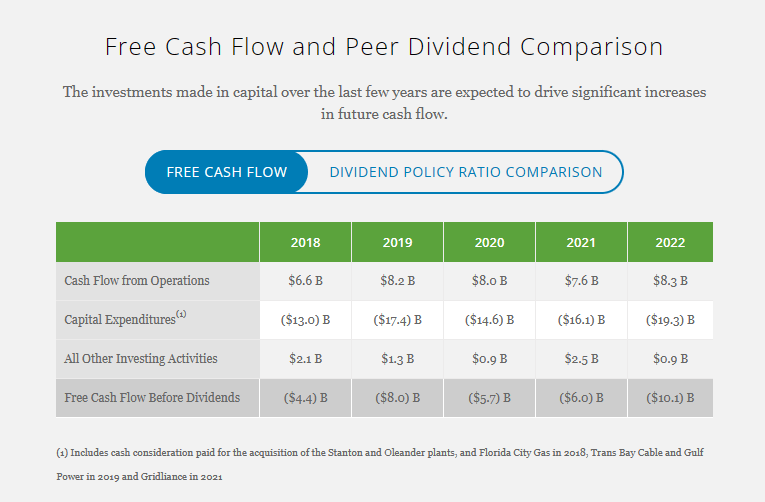

Investors must also note that historically, NEE has not even come close to funding its capex and dividends from operating cash flow.

NEE Presentation

Yes, yes. We get that it is going to recoup those costs and nothing breaks the utility model. But don’t assume this is a risk-free model. If the allowed return on equity is lowered and we have seen this on many utilities, NEE may suddenly find itself up a creek without a paddle.

Verdict

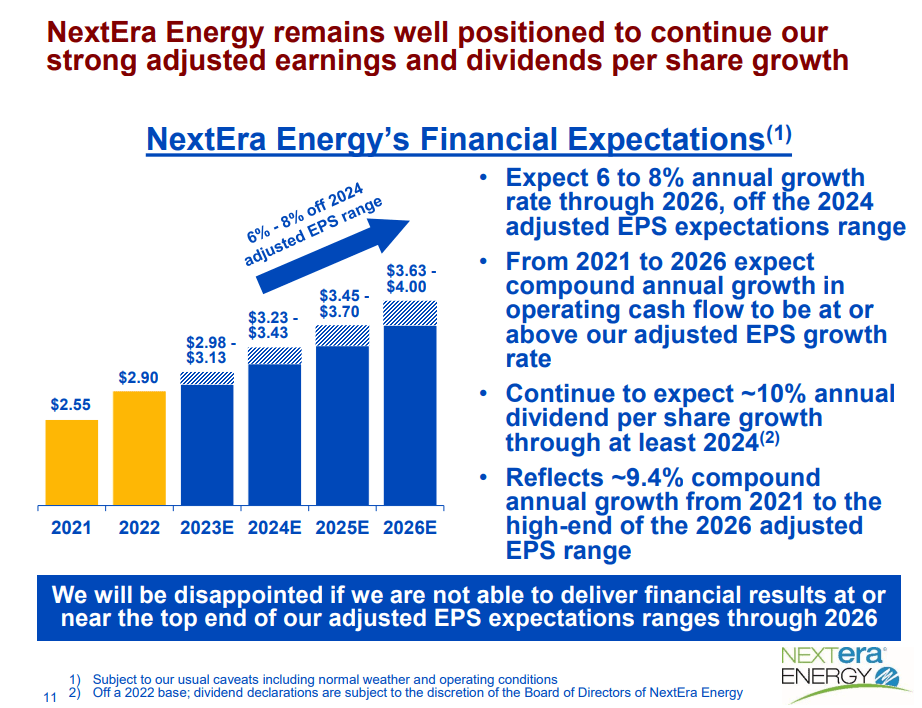

It is easy to get seduced by slides like this. 8% growth rates as far as the eye can see.

NEE Presentation

NEE added they would be disappointed if they did not hit the high end of their adjusted EPS range. They are very likely to be disappointed. But even if they are not, the company is trading at 12X the high end of their earnings estimates for 2026. There is nothing stopping the company for trading at that number. Which means you make just the dividend yield over the next 3.5 years.

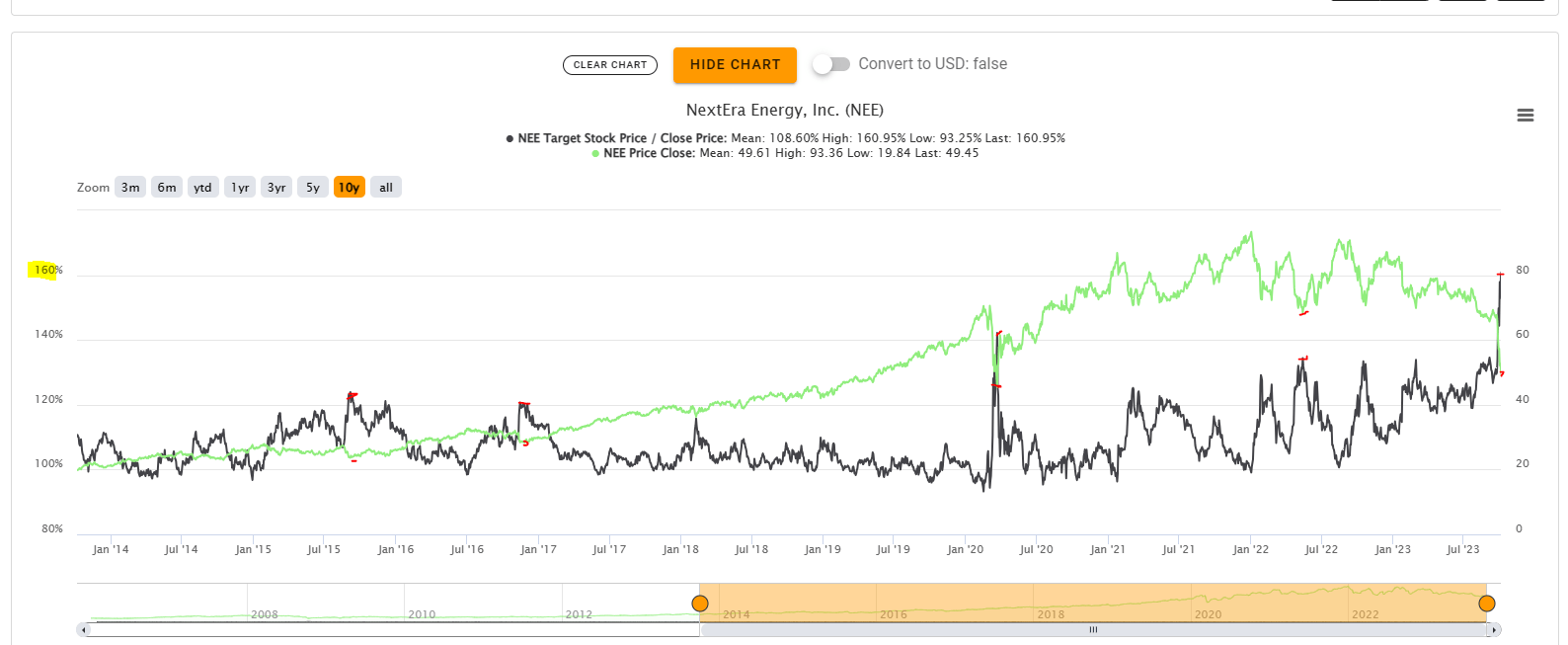

One metric is favorable here and that is the analyst price target divided by the current price. This is a sentiment metric more or less but shows how quickly things have gone to the doghouse. We will note that this percentage (currently over 160%, on left hand scale) has historically topped out (stock bottomed out) at lower numbers.

TIKR

Even during the COVID-19 crash this metric did not get this high. We think this should caution the bears from joining this late into the party on the higher interest rate theme. A reversal could be just as violent. For our part, we are staying out as we have enough duration sensitive assets here. If we had to play it we would use the deep-in-the money covered call approach.

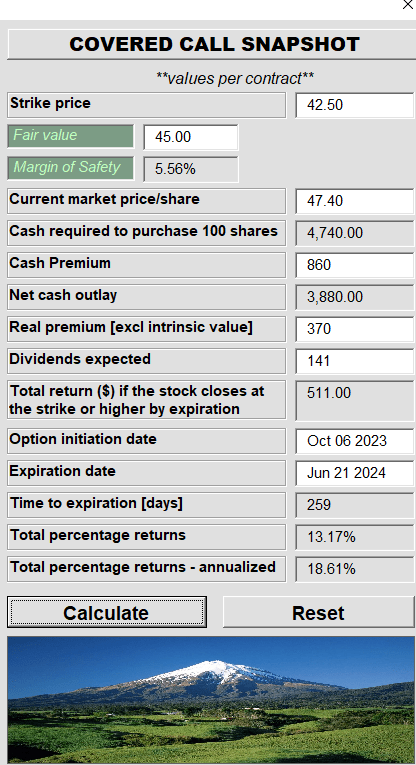

The stock is currently near $47.40 as we write this.

Interactive Brokers

The $42.50 covered calls offer enough protection for this A rated utility and create an 18.61% yield even if it drops another 10%.

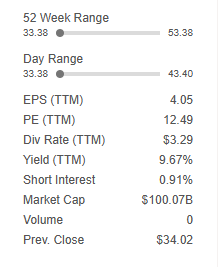

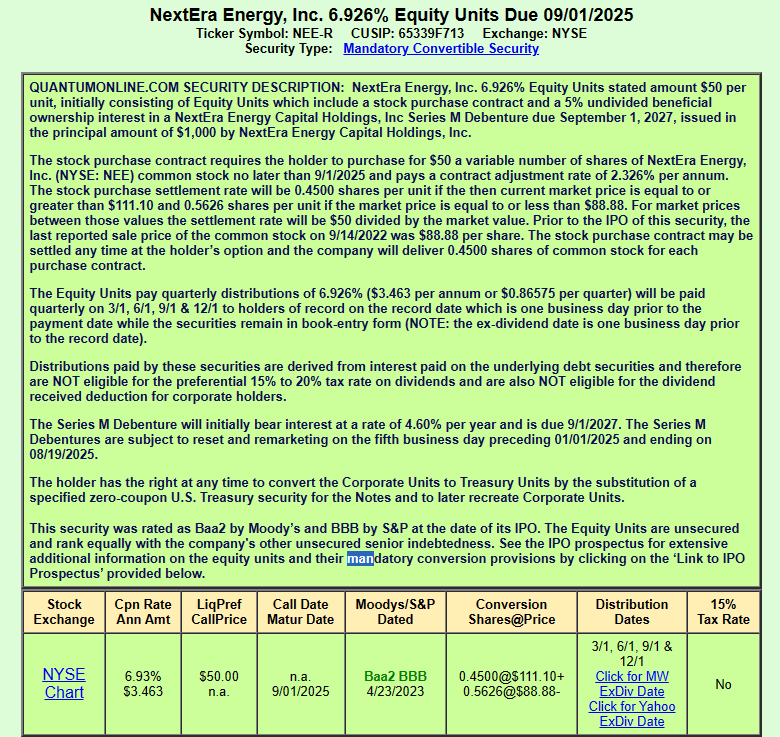

We want to briefly touch on these units which sport a massive yield.

Seeking Alpha

We have seen investors fail to understand similar units and think they are somehow superior to the common shares. We saw this in the case of Algonquin Power & Utilities Corp. (AQN) where the corresponding Algonquin Power & Utilities Corp – Units (AQNU) were hailed as an easy way to make twice the dividend yield. NEE.PR.R presents the same danger. As a mandatory convertible you are going to get about the same return profile as common shares with the difference being that you get a higher cash flow and then a capital loss on conversion.

Quantum Online

You can glance at the capital loss by converting 1 unit of NEE.PR.R into 0.5626 shares of NEE today. These can be bought if there is an arbitrage opportunity AND you like NEE at the prevailing price. But we would stick to deep in the money covered calls for a straight 18.6% yield and a big buffer.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Analyst’s Disclosure:I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Are you looking for Real Yields which reduce portfolio volatility?

Conservative Income Portfolio targets the best value stocks with the highest margins of safety. The volatility of these investments is further lowered using the best priced options. Our Enhanced Equity Income Solutions Portfolio is designed to reduce volatility while generating 7-9% yields.