Summary:

- Novavax’s financial position improved significantly with a $570 million cash infusion from Sanofi, boosting its balance sheet and cash reserves to $1.1 billion.

- Despite Jefferies’ bullish $31 price target, Novavax faces challenges with limited market share and uncertain future revenues from royalties and new drug sales.

- The Sanofi partnership is beneficial, but Novavax’s future sales are expected to decline, impacting stock valuation.

Richard Drury/DigitalVision via Getty Images

Novavax, Inc. (NASDAQ:NVAX) is in a far better financial position following the partnership deal with Sanofi (SNY). The biotech has a vastly improved balance sheet, but a lot of questions exist on how the company will boost the stock going forward. My investment thesis remains Neutral on the stock with a $2 billion market cap, though the stock soared due to analysts with a very bullish view on Novavax.

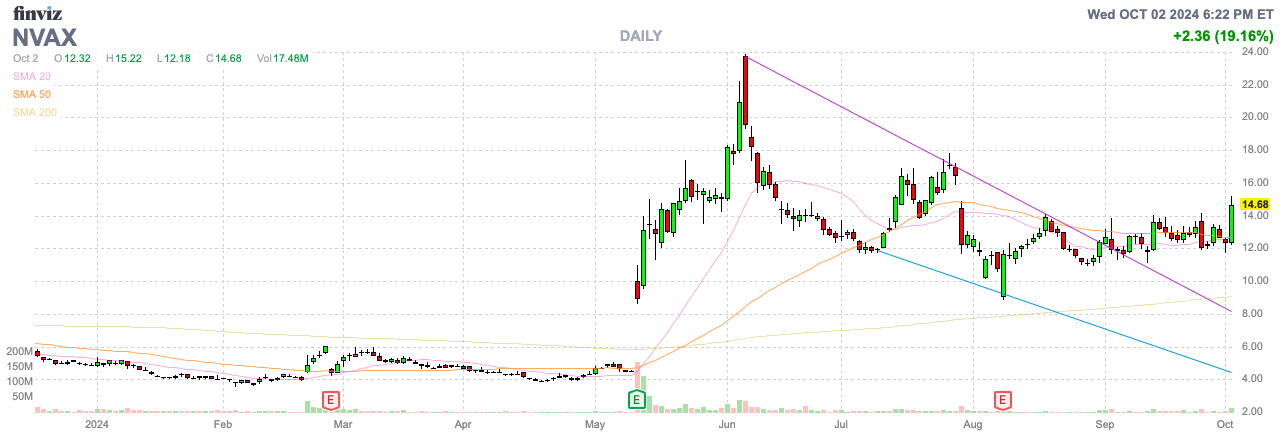

Source: Finviz

New Chapter

Novavax entered a new chapter in Q2, with the company receiving $570 million in cash from Sanofi as part of the partnership. Novavax now has a cash balance of $1.1 billion, with $500 million in upfront payments and the other $70 million via equity investment in stock.

Jefferies issued a bullish note on the stock based on meeting with management. The research firm has a $31 price target for ~100% upside from here, but the prospects of only meeting ’24/’25 seasonal sales aren’t so promising.

At the recent Baird conference, management outlined the product sales guidance for the fall season at only $225 million as follows:

Then product sales guidance, $275 million to $375 million. So you got a midpoint at $325 million.

In that $325 million midpoint, you got a $100 million that we already sold this year under our advanced purchase agreements. The remainder, $225 million in sales for the fall season, the vast majority of which, U.S. market.

Now the question is what revenues are possible for Novavax via new drugs and how much royalties the company can claim from Sanofi on top of the $700 million in additional development, regulatory and launch milestone payments. Sanofi would have to be far more successful selling the Covid vaccine in the ’25/’26 season in order for Novavax to record material royalty revenues.

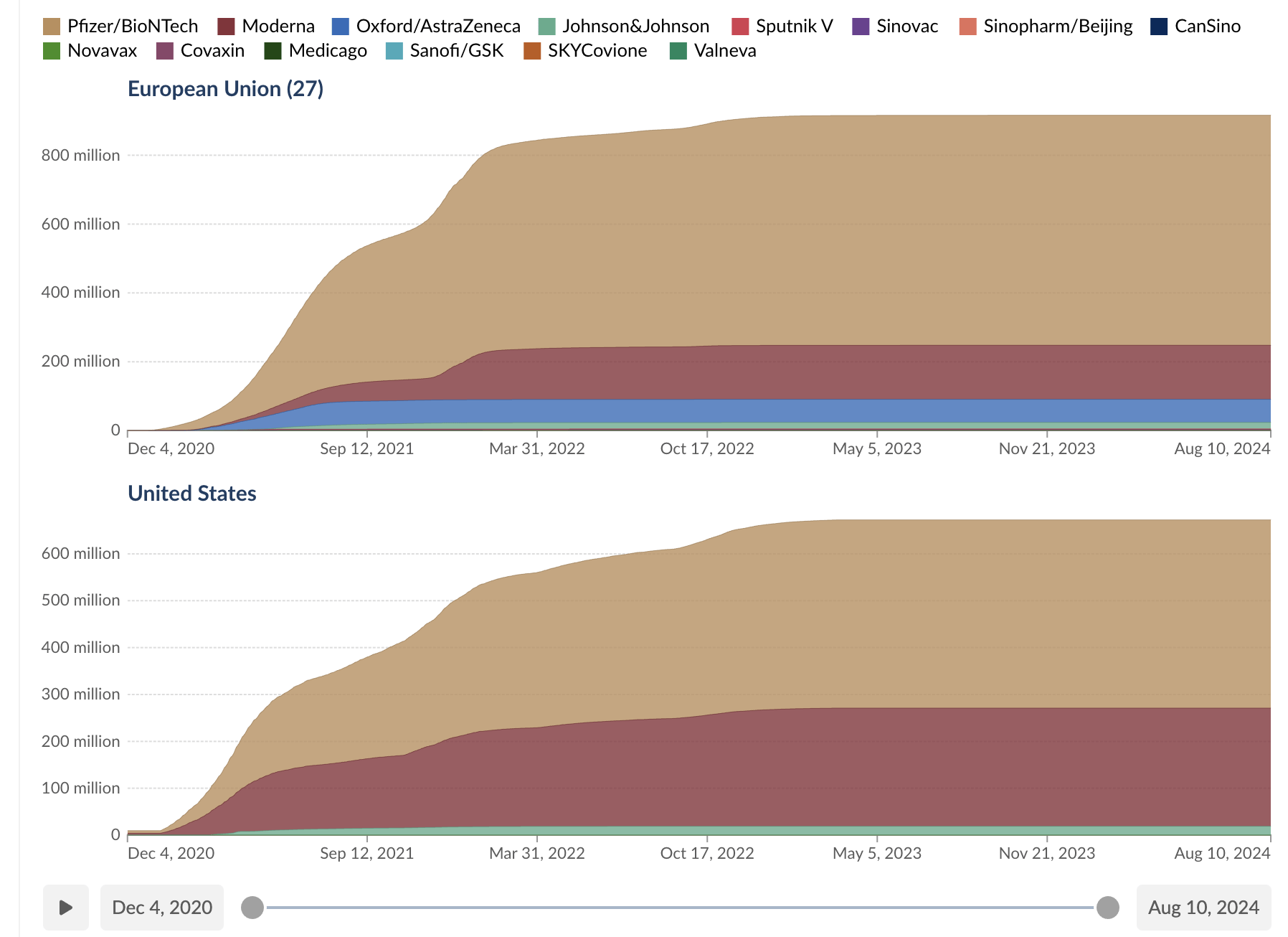

The company has very limited market share on vaccines sold in the EU and the U.S. These charts hardly show Novavax in the picture with Pfizer (PFE) and Moderna (MRNA) selling millions upon millions in vaccines.

Source: Our World In Data

The big question is, how many Covid vaccines can be sold? Novavax lists a bunch of retail locations for the ’24/’25 vaccine season, but the company turns to Sanofi to market the vaccines starting in 2025.

The Covid-19-Influenza (CIC) combination vaccine is promising. Novavax targets the start of the Phase 3 trial in Q4 with top-line results targeted for Q2’25.

One has to question how successful the small biotech can market such a vaccine against the big biopharmas, even with a partner. The biggest hope is probably for Sanofi to get their CIC drug approved to successfully market against anything from Pfizer and Moderna.

Hard To Value

While the Sanofi deal was a huge positive for Novavax, the small biotech will likely now transition to a period of declining sales. The stock market doesn’t usually reward stocks with declining sales.

Between APAs and governments forcing Covid vaccines in the past, Novavax reported far higher sales. The company even just reported Q2 GAAP revenues of $415 million, due mostly to the upfront payment from Sanofi.

The current analyst forecasts are for limited sales next year, despite Novavax still reporting revenue from the upfront payment and the potential additional milestone payments of up to $350 million. Sanofi will start selling the Covid vaccine on January 1, so going forward sales are likely minimal, based on collecting only royalties.

The consensus analyst estimates are very wide for the next few years. While only two analysts have numbers for 2027, the revenue estimate at $377 million is actually below the 2025 targets.

Source: Seeking Alpha

As mentioned above, the current 2024 revenue estimates only include ~$225 million in product sales for the current vaccine season. The other $500 million comes from $100 million in APAs and another $400+ million for the upfront payment from Sanofi recorded as revenue in 2024.

Again, the Sanofi deal is incredible, but the stock will be valued based on the revenues generated based on the royalties going forward. Especially considering Novavax plans to find another partner for the CIC vaccine, assuming regulatory approvals following good Phase 3 results.

Novavax will spend upwards of $450 million on operating expenses in 2025, followed by $350 million in 2026. The company will undoubtedly burn cash at these run rates, outside of any additional milestone payments from Sanofi.

Shareholders have long faced the pain of heavy spending, leading to share dilution to raise additional capital. The new structure likely limits the risks, but the royalty structure also cuts the upside potential from vaccine sales.

Takeaway

The key investor takeaway is that Jefferies is very bullish on the stock, but Novavax needs sustainable royalty revenues for the stock to hold on to higher prices.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

The information contained herein is for informational purposes only. Nothing in this article should be taken as a solicitation to purchase or sell securities. Before buying or selling any stock, you should do your own research and reach your own conclusion or consult a financial advisor. Investing includes risks, including loss of principal.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

If you’d like to learn more about how to best position yourself in undervalued stocks mispriced by the market to start Q4, consider joining Out Fox The Street.

The service offers a model portfolio, daily updates, trade alerts and real-time chat. Sign up now for a risk-free 2-week trial to started finding the best stocks with potential to double and triple in the next few years.