Summary:

- Chip inventories are mounting up for Nvidia Corporation as sales for PCs continue to slow.

- Nvidia has a p/e ratio of 120x, which would need to fall 88% to be at 15x p/e.

- Nvidia is worth as much as Taiwan Semiconductor and Advanced Micro Devices combined, while TSM and AMD’s net income are ~8x greater than Nvidia’s net income.

- There is increased competition from Google, Apple, Intel, and Europe.

- Sell recommendation for Nvidia Corporation with an estimated price target of $115 per share.

Justin Sullivan

Thesis

In my eyes, Nvidia Corporation (NASDAQ:NVDA) has several risks that would make me sell or deter me from buying the stock. First off, inventories have been mounting up across the board for all semiconductor companies, with Nvidia’s inventories nearly increasing 5x since 2020. Additionally, significant sales exposure to a possible China and Taiwan conflict could further decrease demand for Nvidia’s products. Furthermore, insiders have sold over $62 million in share value over the last 4 months. Additionally, looking to competitors, one can see that Nvidia’s valuation is bloated, with Nvidia being worth as much as Taiwan Semiconductor Manufacturing Company Limited (TSM) and Advanced Micro Devices, Inc. (AMD) combined, while TSM and AMD’s net income is 7x greater than Nvidia’s.

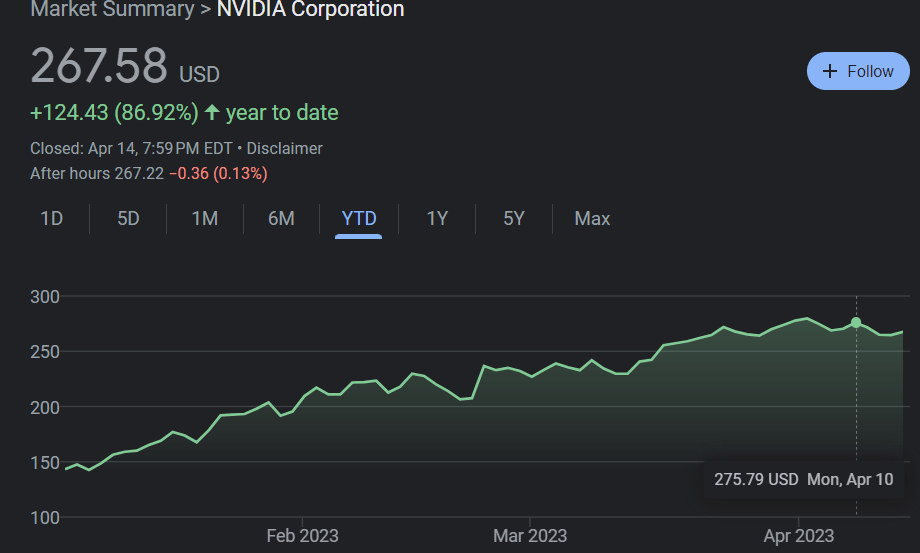

According to my model, I am seeing a price target for Nvidia Corporation of $115/share, compared to the market value of $272/share.

Chip Inventories Mounting Up + China/Taiwan Exposure

Nvidia has seen inventories increasing quite sharply year-over-year, as seen below.

CapitalIQ

Historically speaking, Nvidia’s inventory levels have been rising for the last 4 years. As a company’s inventory levels continue to rise, cash flow is delayed and companies typically sell products at reduced prices, which further reduces forecasted revenues. According to an article from Nikkei, Taiwan Semiconductor Manufacturing Company expects it will take until the first half of 2023 for inventories to begin to return to normal. I think this may be an aggressive projection, considering demand for PC’s fell during Q1 2023.

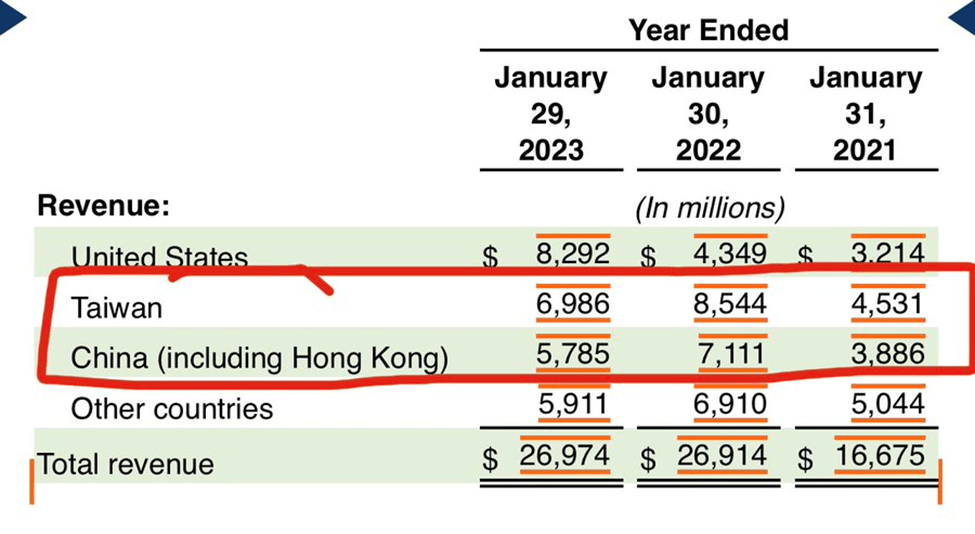

Additionally, Nvidia maintains a significant exposure to China and Taiwan. China has been performing large scale aerial and sea exercises around Taiwan in what seems to be an intimidation tactic. This has caused high tensions and speculations about possible conflict between China and Taiwan. Conflict between the two nations can lead to decreased demand for each country, with Nvidia having significant sales exposure to both China and Taiwan, as seen below.

10-K

Bloated Valuation

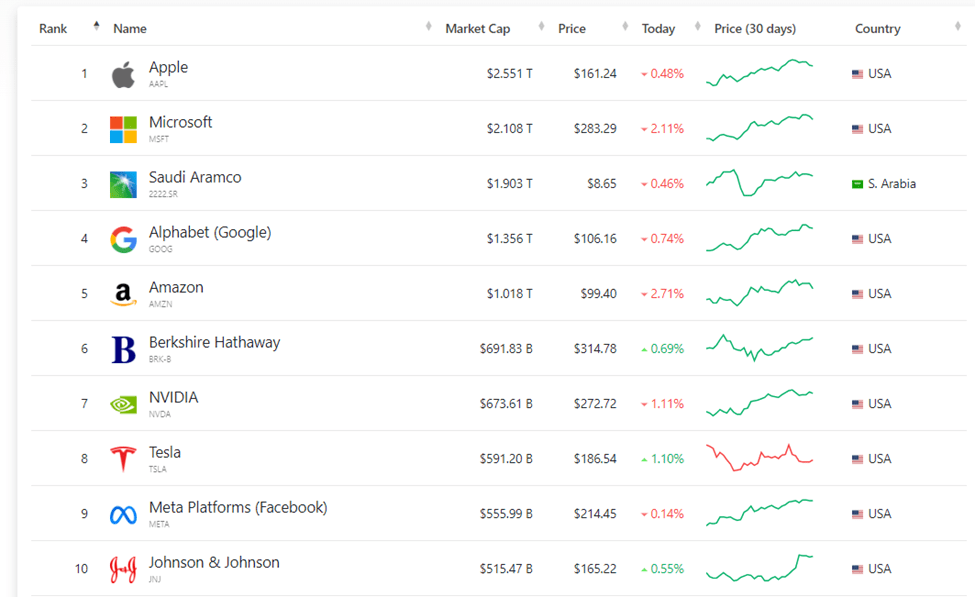

When sorting companies by their market cap, we get the following list as presented below:

companies market cap

What is particularly interesting to me is that Nvidia is the 7th largest company in the world. This puts Nvidia ahead of Tesla, Inc. (TSLA), Johnson & Johnson (JNJ), Meta Platforms, Inc. (META), and on par with Berkshire Hathaway Inc. (BRK.A), which is quite shocking. Furthermore, Nvidia has a p/e ratio of 156x and would need to fall 96% to be at 15x p/e.

CapitalIQ

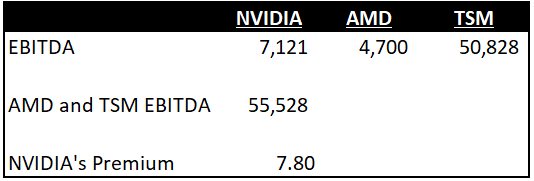

Looking to competitors in Nvidia’s industry, such as AMD and TSM, provide valuable insight as to an appropriate relative valuation. Nvidia is worth as much as TSM and AMD combined, with TSM and AMD EBITDA being ~8x Nvidia.

Authors Calculation

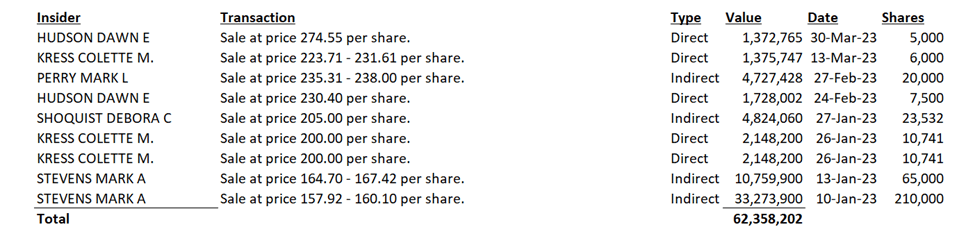

Additionally, insiders have been strongly selling Nvidia stock to start off the year. As of 2023, 6 different insiders sold their shares in Nvidia, totaling $62.3 million.

Author Calculations

An increase in shares sold by insiders makes me believe that they think the top is in for the stock. Usually I consider insider selling to be a warning sign and a sign to dig deeper into the stock.

Increased Competition

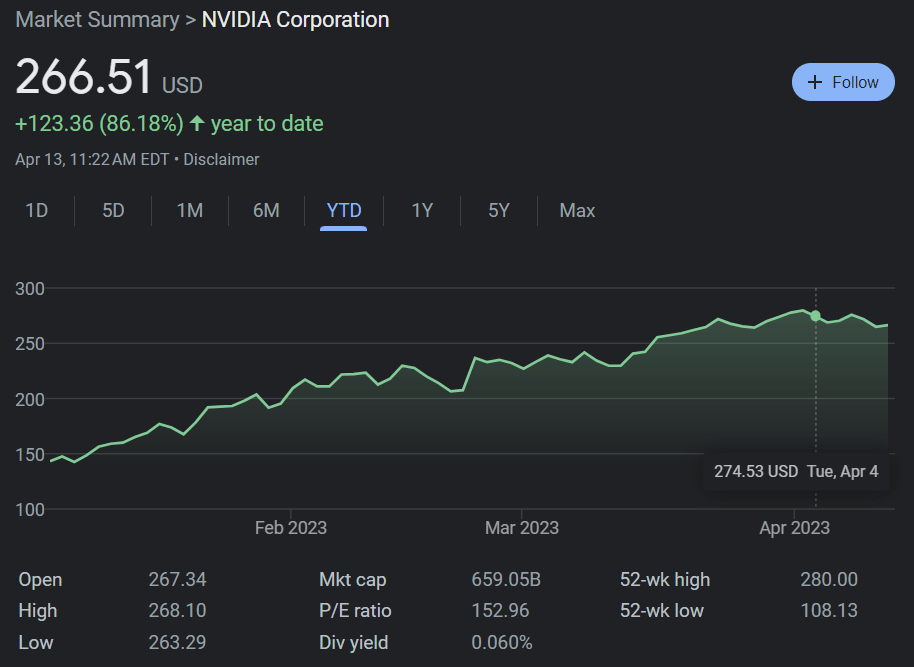

Nvidia has been touted as the dominant supplier in the semiconductor industry. Due to this, Nvidia has enjoyed nearly a ~90% year-to-date gain in its stock price as a result of the AI boom.

Google Finance

The AI boom could prove to be a double-edged sword for Nvidia. As AI continues to become more and more relevant, competitors do not want to keep paying top dollar for Nvidia’s products. My theory is that as AI continues to boom, many of these companies will start to make their own chips to save on costs, and competitors will increase their output to compete with Nvidia.

According to a Seeking Alpha Article, companies such as Intel Corporation (INTC) and TSM are scheduled to begin operations of new U.S. chip plants in 2024, while Micron Technology, Inc. (MU) and others have also announced large-scale investment plans. The article also goes on to mention that:

“Google (GOOG) (GOOGL) said the fourth-generation Tensor Processing Units, or TPUs, that train its artificial intelligence models are faster and more power-efficient than Nvidia’s A100 chips.”

Along with Google, Intel has also increased it capacity. The article further states:

“Intel has worked to increase its manufacturing presence on the continent and compete in the foundry space, announcing plans to build a fab in Germany and discussing plans for another plant with Italy and other European countries.”

I believe the new AI wave is going to push companies to start their own AI chip making, pushing Nvidia out.

DCF

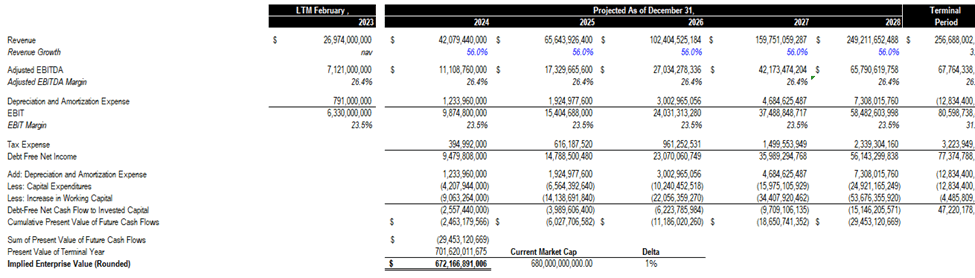

Utilizing a discounted cash flow (“DCF”) approach can provide insight into how much money an investor should reasonably pay for a company by discounting future cash flows to present value. Currently, Nvidia has a market cap of $680 billion, implying a 56% growth rate over the next 5 years. An annual growth rate of 56%, consecutively, over the next 5 years seems aggressive considering the risks outlined above.

CapitalIQ

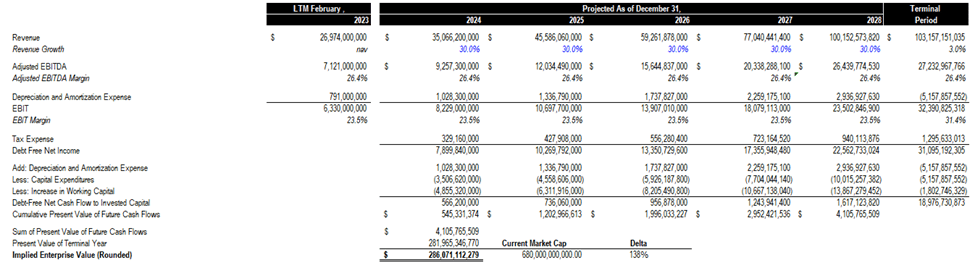

Using a 30% growth rate year-over-year still seems aggressive to me, considering the risks outline above. However, I decided to use an annual growth rate of 30% to stay conservative in my approach, while using a discount rate of 8% with 26% EBITDA margins. These assumptions ultimately resulted in a market cap of ~$290 billion. Nvidia is currently trading at $272/share, compared to my projected price of $115/share based on my DCF analysis.

Author Calculations

Risks

There are several risks surrounding Nvidia that could change my stock recommendation from a sell to a hold or buy.

One of the largest hurdles I anticipate my investment thesis faces is Nvidia’s platform “Cuda.” Nvidia’s GPU’s have much higher compatibility and in general are better integrated into tools like TensorFlow and PyTorch. AMD’s graphic cards, for example, can use Cuda. In order to use your AMD graphic card, you have to use an open source library called OpenCL. OpenCL has a much lower compatibility and does not integrate well with other tools. The OpenCL, in my eyes, is inferior to Cuda until the OpenCL source library expands as uses migrate away from Cuda.

Additionally, competitors may not make the impact they say they will have and Nvidia could continue to be the leading brand. If brands like Intel and Google’s products fail to integrate their way into the community, Nvidia could continue to be the most used graphics card and most used platform.

Lastly, Nvidia has seen nearly a 90% increase in its stock price when looking at a year-to-date chart.

Google Finance

Nvidia has gained a considerable amount of momentum and has been trending upwards over the last 4 months.

Conclusions

Overall, Nvidia Corporation has several risks that would deter me from buying their stock. Nvidia has significantly increased its inventory levels over the last 4 years, has seen decreased sales, and has sales exposure to China and Taiwan. Furthermore, Nvidia’s valuation is bloated, whether looking to their competitors or at their financials through an implied discounted cash flow analysis. According to my model, I am seeing a Nvidia Corporation price target of $115/share, compared to the market value of $272/share.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.