Summary:

- Nvidia Corporation is potentially in a bubble due to inflated AI expectations, risking significant stock price declines when growth rates slow.

- Despite high valuation multiples, Nvidia’s extraordinary recent growth rates in revenue and free cash flow could justify its current stock price.

- The decisive question is whether Nvidia can sustain growth rates to match high expectations and avoid a Dotcom-like collapse.

- I might have underestimated Nvidia’s growth potential, but I still see significant downside risk and consider the stock very expensive.

Sundry Photography

I recently listened to a podcast episode in which Stanley Druckenmiller argued that the AI boom was not so difficult to spot. And although he admitted it was luck on his end that he invested in Nvidia Corporation (NASDAQ:NVDA) a few weeks before ChatGPT started the AI hype in late 2022, he obviously saw Nvidia taking off at a point where I was rather bearish.

In the following article, I will take two different perspectives. On the one hand, I will argue once again why Nvidia might be caught in a bubble and is still facing rather high downside risk at this point. This is an argument I already made in previous articles, in which I rated Nvidia as a sell.

On the other hand, I will also question myself and the arguments I made in past articles. And as there are signs that Nvidia might actually grow into its valuation, we are also trying to take the opposite perspective.

Bearish Side

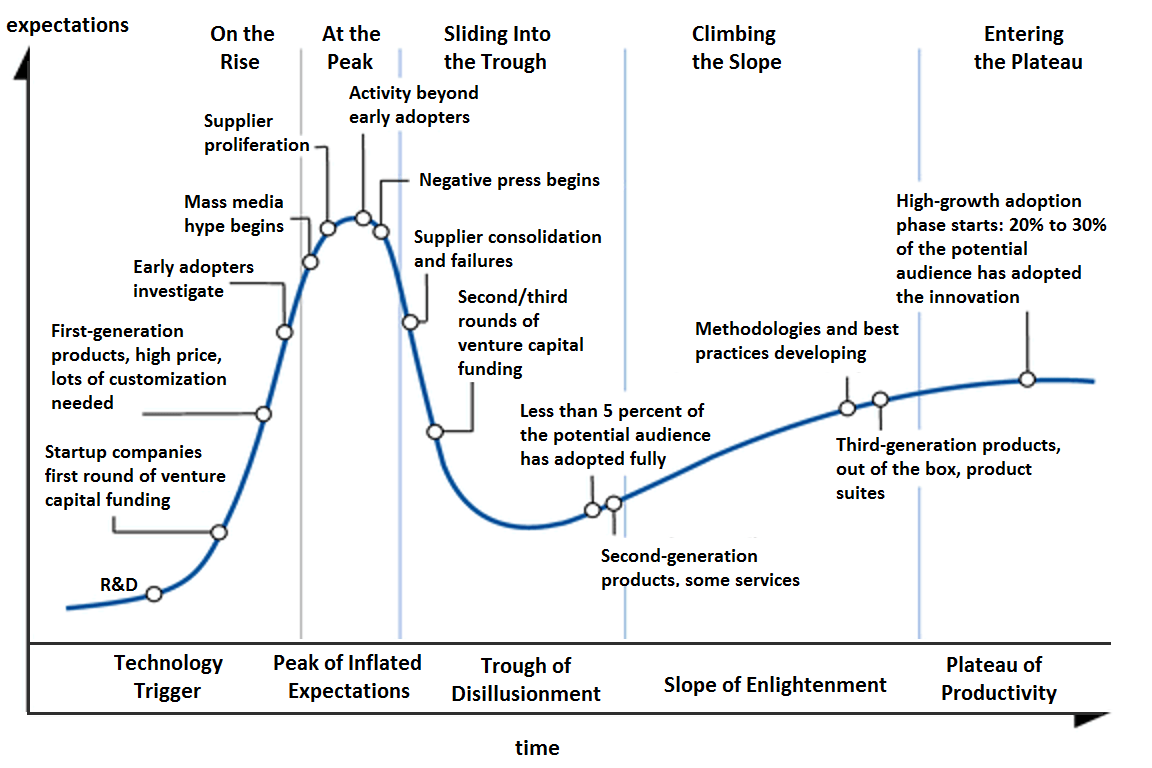

One of the major bearish arguments made in a previous article about Nvidia is the bubble in which Nvidia and AI are in right now. Generative AI is one of the hot topics right now and almost everybody is bullish, which is pushing several stocks to extreme levels. But when looking at the typical hype cycle (see a more detailed version below), we know that the peak of inflated expectations is followed by a steep decline and the trough of disillusionment.

Wikipedia

And in my opinion, we are at the peak of inflated expectations with activity beyond early adopters, as AI is not just used by a few people anymore. Currently, everybody is bullish and is expecting high growth rates and wide AI adoption. The problem here is that people (including investors) tend to extrapolate current growth rates into the future – this is not only the case when businesses are growing at an extremely high pace, but also when businesses are declining. We almost always assume the current situation will continue for a long time – but at the peak of inflated expectations, these are just too optimistic. The widespread adoption is coming – and it will come for AI – but the process usually takes longer than people expect. Meanwhile, growth rates are lower than expected and hyped companies with a stock price reflecting very high expected growth rates suddenly collapse.

Author’s work

I have already written about the hype cycle in great detail in articles about Bitcoin (BTC-USD) (in early 2019) and Beyond Meat (BYND) (in early 2020). I explained the typical signs for a bubble and how it plays out – and in my opinion, we also see the typical signs for AI (and Nvidia). In my article Beyond Meat: Beyond The Bubble, I wrote:

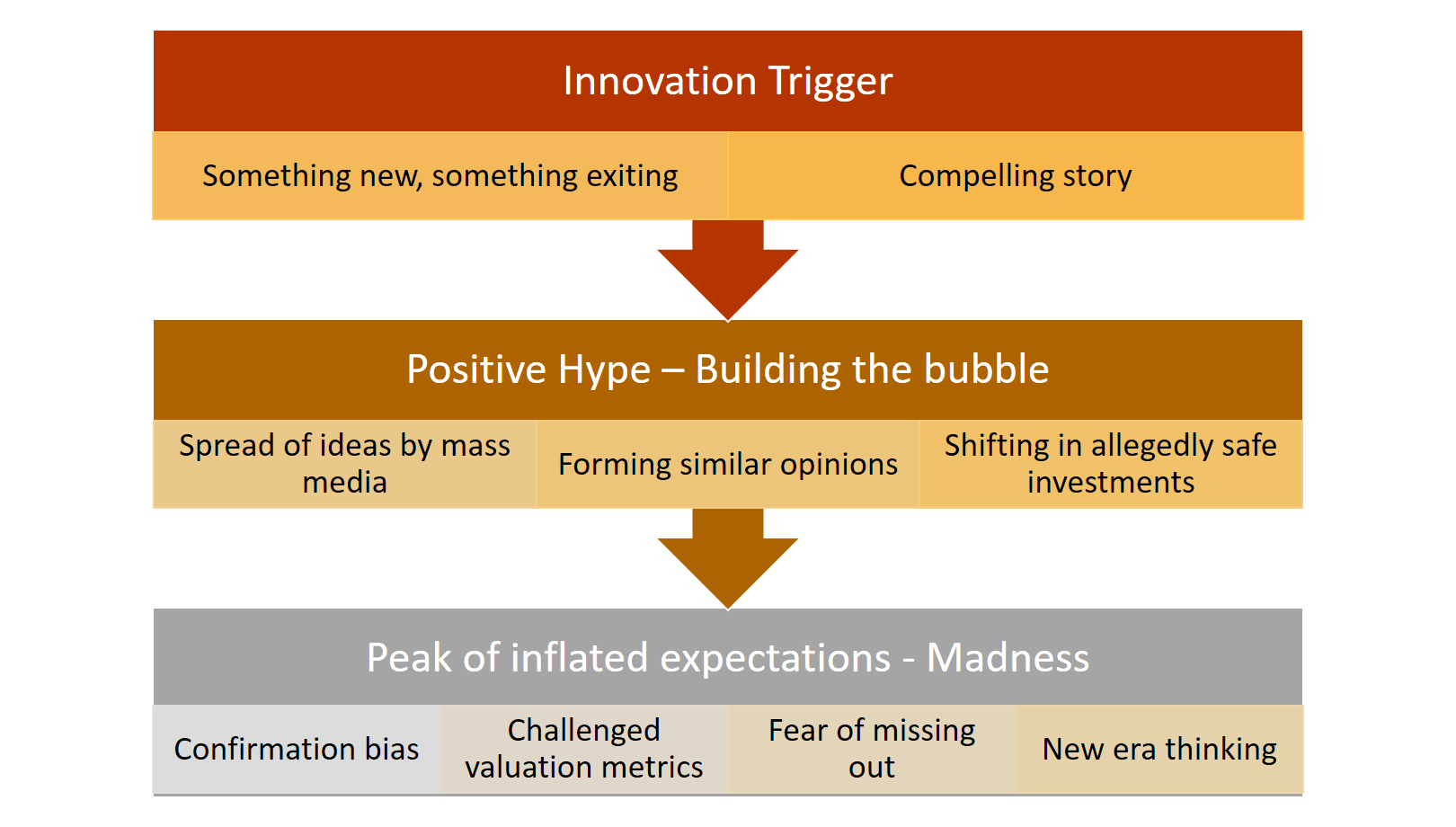

In a first step, we need an innovation trigger. People are always drawn towards new innovations, new technologies, or inventions as they are fascinating to us. Additionally, we need a compelling story created around that invention or innovation, how it can alter people’s lives sustainably or could solve a great problem mankind has been having for decades (people imagining that is enough).

AI is a perfect example. It is a great innovation, and it is built on technology. The fact, that it is fascinating and scaring people at the same time is also great for a potential bubble and hype, and it is difficult to understand for most people what is actually happening.

But an innovation trigger is not enough to create a hype. People have to form a similar (bullish) opinion about the asset or asset class – otherwise, a bubble is not possible. If only a few people assume that the asset should be worth much more and others have the opinion it should be worth less, there won’t be a bubble. In his famous book “Irrational Exuberance,” Robert J. Shiller wrote the following:

Significant market events generally occur only if there is similar thinking among large groups of people, and the news media are essential vehicles for the spread of ideas. (Shiller, p. 71).

Hence, it is important that the story must be picked up in the mass media. If the invention or new technology is not exciting or news-worthy and provides the opportunity for great stories, it probably won’t lead to a hype.

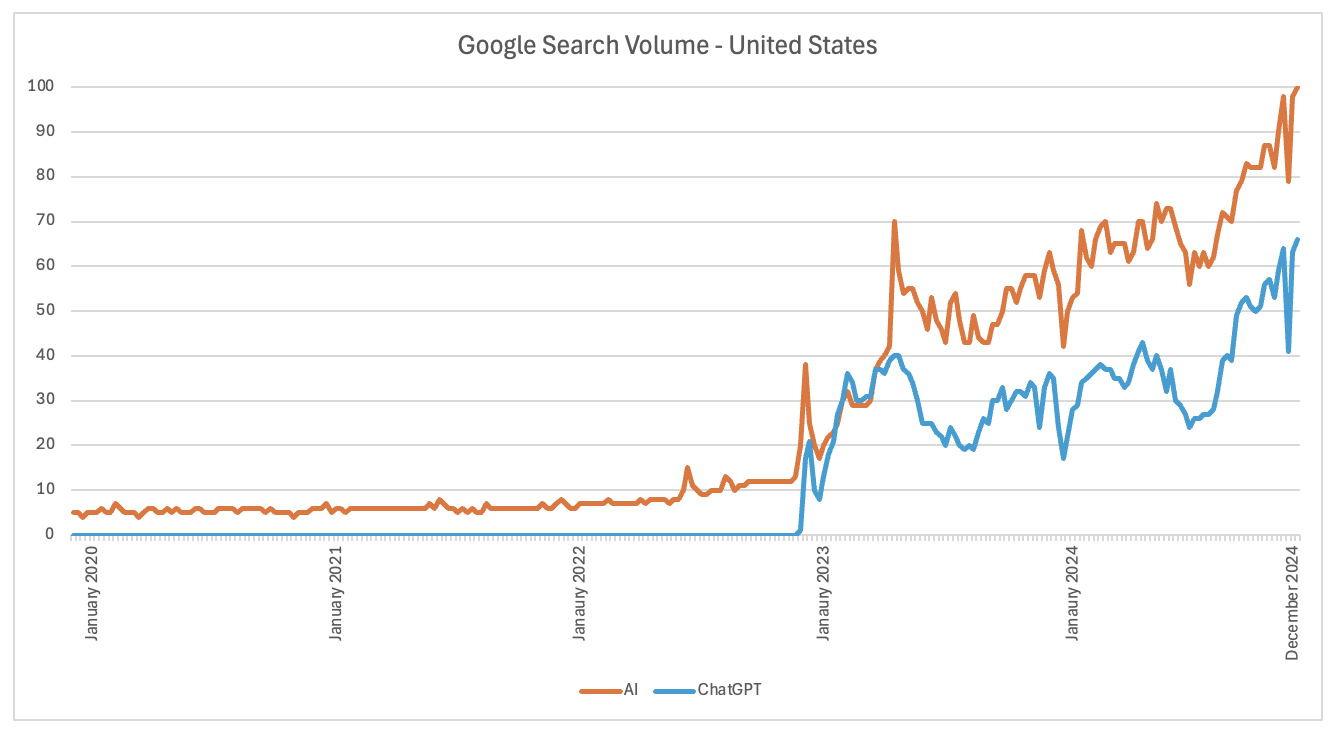

Author’s work based on Google Trends

And the topic has been picked up by the mass media, which can be shown for example by Google search volume (see chart above). We clearly see interest picking up and going higher and higher starting in November 2022 when ChatGPT was released.

I could go on and talk about confirmation bias, the fear of missing out, and the typical challenge of valuation metrics we always see in such bubbles. But I think we can say with some level of confidence that AI – and most companies operating in the industry or companies that are associated with AI – is in a bubble. We have to expect the bubble to pop at some point, with the typical pattern following the bubble peak. In the case of stock prices, we are usually talking about declines of 80-90% and massive losses.

Bullish Side

The bearish perspective about AI being in a typical hype and close to the peak of inflated expectations is one side. Now we can try to take the opposite perspective.

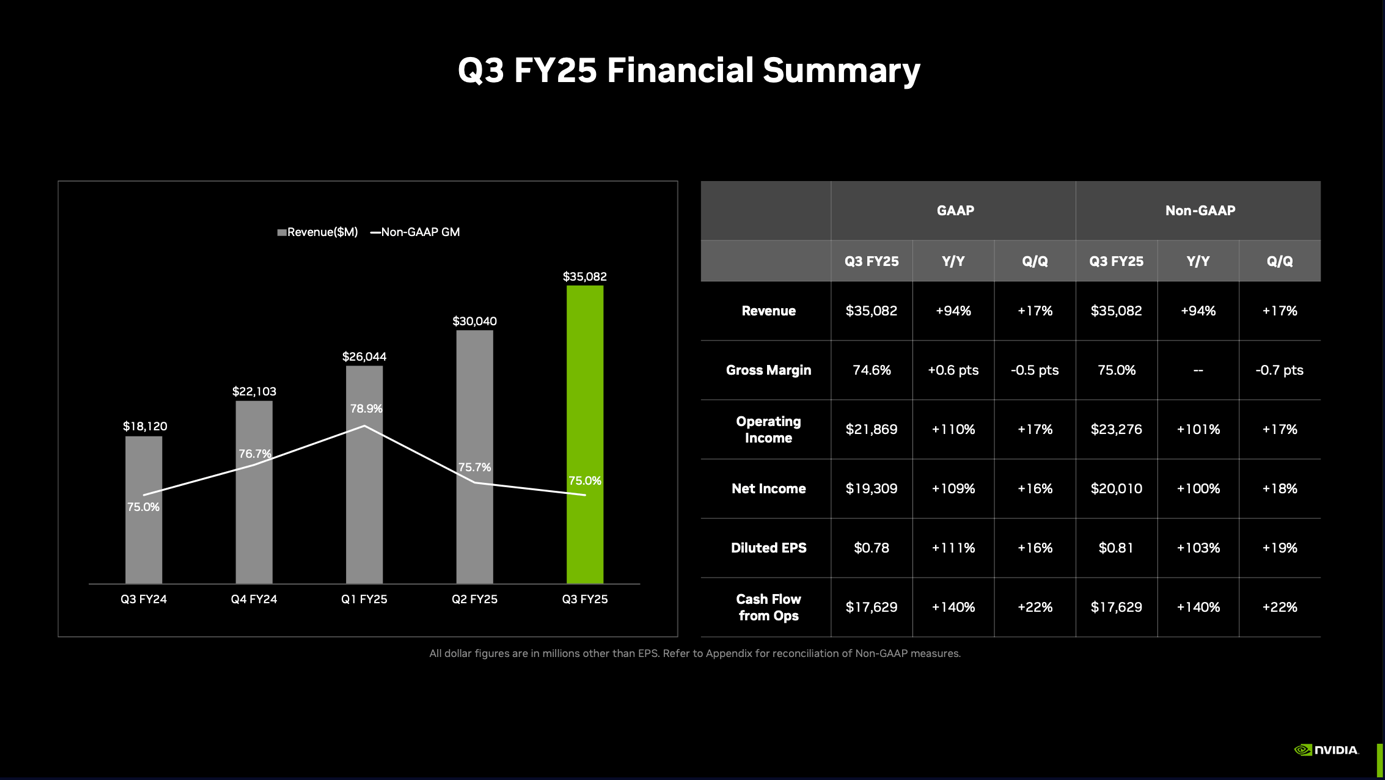

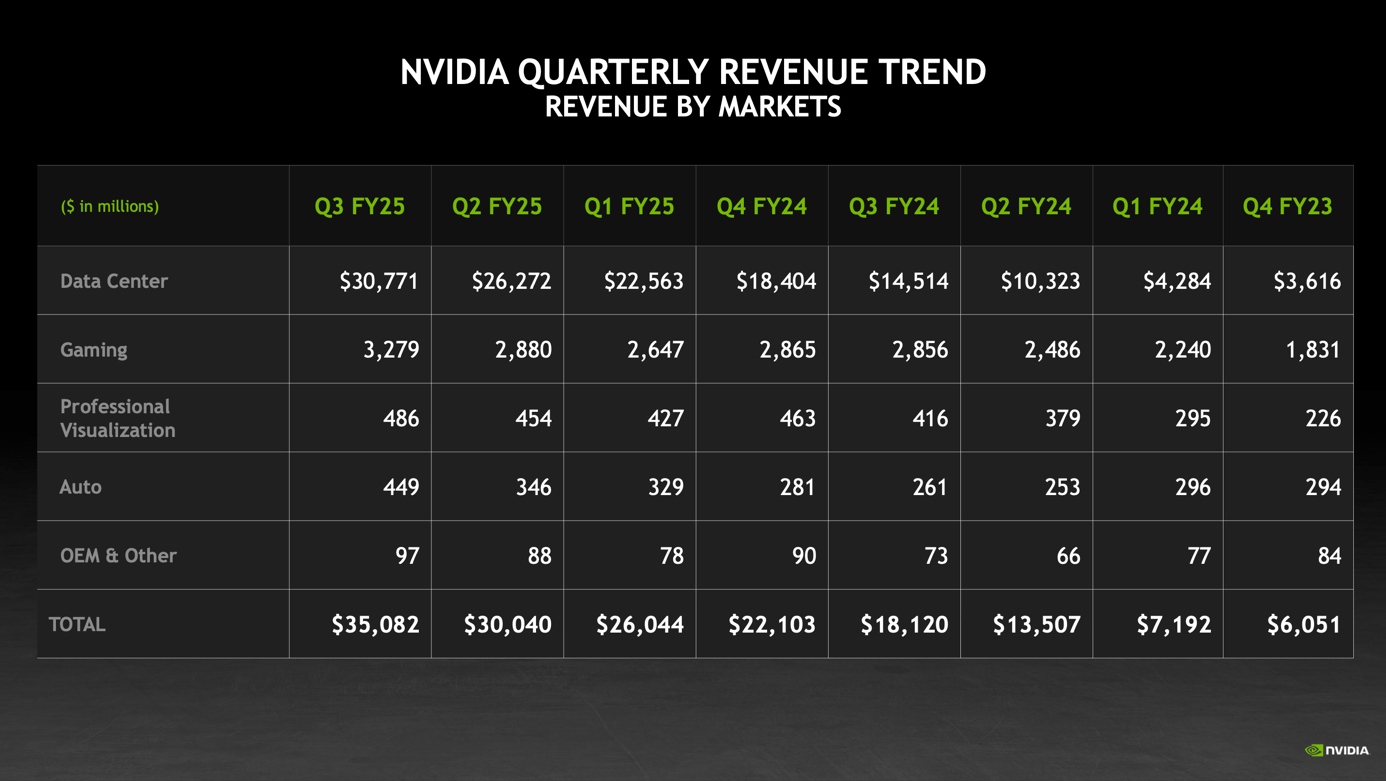

When looking at the last quarterly results, Nvidia is continuing to grow at a high pace. Revenue increased from $18,120 million in Q3/24 to $35,082 million in Q3/25 – resulting in 93.6% year-over-year growth. And while revenue did not grow in triple digits anymore (after five quarters of growth rates above 100%), operating income still increased 110% year-over-year from $10,417 million in the same quarter last year to $21,869 million in this quarter. Finally, diluted net income per share increased from $0.37 in Q3/24 to $0.78 in Q3/25 – a bottom-line growth rate of 110.8% year-over-year.

NVIDIA Investor Presentation

Free cash flow – one of the most important metrics – increased 138.4% year-over-year from $7,042 million in Q3/24 to $16,787 million in Q3/25. And similar to previous quarters, the growth rates of Nvidia were driven especially by one single market platform – Data Center. Revenue increased from $14,514 million in the same quarter last year to $30,771 million in this quarter – resulting in 112% year-over-year growth. The second major segment for Nvidia is Gaming, which generated $3,279 million and increased revenue by 14.8% year-over-year. These two segments are responsible for 97% of total revenue and to be honest, the other three segments are not really worth mentioning as they play only a subordinate role for Nvidia.

NVIDIA Investor Presentation

When looking at the other three segments, Professional Visualization increased revenue 16.8% YoY to $486 million in Q3/25 and Automotive increased revenue 72.0% YoY to $449 million. Automotive might be one of the market platforms continuing to grow at a high pace, but compared to Data Center with almost 70 times more revenue, it doesn’t really matter. Finally, OEM and Other generated $97 million in revenue in Q3/25.

Now we can argue that growth rates for Nvidia are slowing down and will continue to be lower in the coming quarters. And it seems likely that growth rates for Nvidia will continue to slow down, but we should not ignore how extraordinary the growth rates of the last few quarters were. Even if Nvidia is reporting growth rates only in the low-to-mid double digits, these are still high and impressive growth rates. We should not ignore that Nvidia is one of the major businesses in the world, ranking among the top 100 companies by revenue and sixth in generated earnings.

In the case of extremely high growth rates, it is often a good strategy to visualize the numbers that are exceeding our imagination. And Nvidia’s stock price increased 27,000% in the past ten years – an impressive performance that we would almost automatically see as unreasonable, as almost no company can grow its fundamentals at such a pace. When comparing the stock performance to the fundamental performance, we see the stock price clearly exceeding fundamental growth.

And that is one perspective – the stock price performance tripled the fundamental performance, and such a trend can’t be sustainable over the long run. But assuming that the stock price might stagnate at its level for one year (a possible scenario) and Nvidia being able to double free cash flow once again during the next twelve months (also a possible scenario), the stock is coming rather close to reasonable value again.

Another way to answer the question if Nvidia is actually overvalued or in a bubble is by looking at some valuation multiples. Without much doubt, Nvidia is trading for high valuation multiples – at the time of writing. Nvidia is trading for 60 times earnings and for 54 times free cash flow. And these are still high valuation multiples. However, if Nvidia can continue to keep growing at a very high pace for a few quarters and with the stock price remaining at a current level, this would actually come down to a reasonable valuation multiple.

The Decisive Question

When trying to combine the bullish and bearish views, it seems to come down to one question that remains unanswered. That question will determine if Nvidia will be remembered as one of the big bubbles in history or a stock that was clearly overvalued but continued to perform, and outperformed over the long run. The decisive question is if Nvidia can grow with a pace justifying the stock price and expectations already reflected in the price.

The main reason that made the Dotcom era such a gigantic bubble, with companies completely collapsing and other stocks taking one or two decades before reaching all-time highs again, was the collapse of growth rates. Companies like Cisco (CSCO) immensely profited from the infrastructure that was necessary for the Internet to become available to the masses. But once that infrastructure was in place, growth rates declined steeply.

Now the question is if companies will suddenly stop buying Nvidia’s products as well when the necessary infrastructure is in place and the major players have their infrastructure for AI applications in place. And I certainly think the high spendings we are seeing right now for the major technology companies will decline again. But while the infrastructure that was necessary for the Internet in the late 1990s didn’t have to be replaced for several years (or sometimes decades), the infrastructure necessary for AI applications probably has to be replaced at a much higher pace.

To be honest, I have had difficulties finding reliable information about AI spendings in the coming years. Will companies like Meta Platforms (META), Microsoft (MSFT), Amazon (AMZN), or Alphabet (GOOG) spend similar amounts as right now, or will capital expenditures for these major technology companies decline again? Amazon, for example, already reduced its capital expenditures, while Meta Platforms and Microsoft are still at a very high level. Will these companies continue to spend huge amounts, or have they already purchased all the GPUs needed?

In my opinion, we will see a decline in demand – at least for a few years. This will especially be the case when the economy hits a recession – another scenario I consider very likely. And if growth rates for Nvidia will slow down dramatically, the stock will follow. When the first quarter with disappointing results (disappointing meaning in this case much lower growth rates) hits the markets, the stock could decline heavily. And usually, in such a scenario, sentiment might switch from euphoria to depression and push the stock down to unjustified low stock prices. And where I have extreme difficulty making up my mind is answering the following question: Do companies start spending heavily on AI again in maybe 2028 (after a potential recession) as the GPUs already need to be replaced by much better ones or can the infrastructure stay in place longer. Will the demand be growing at a similar pace as in 2023 or 2024, or will growth rates slow down drastically?

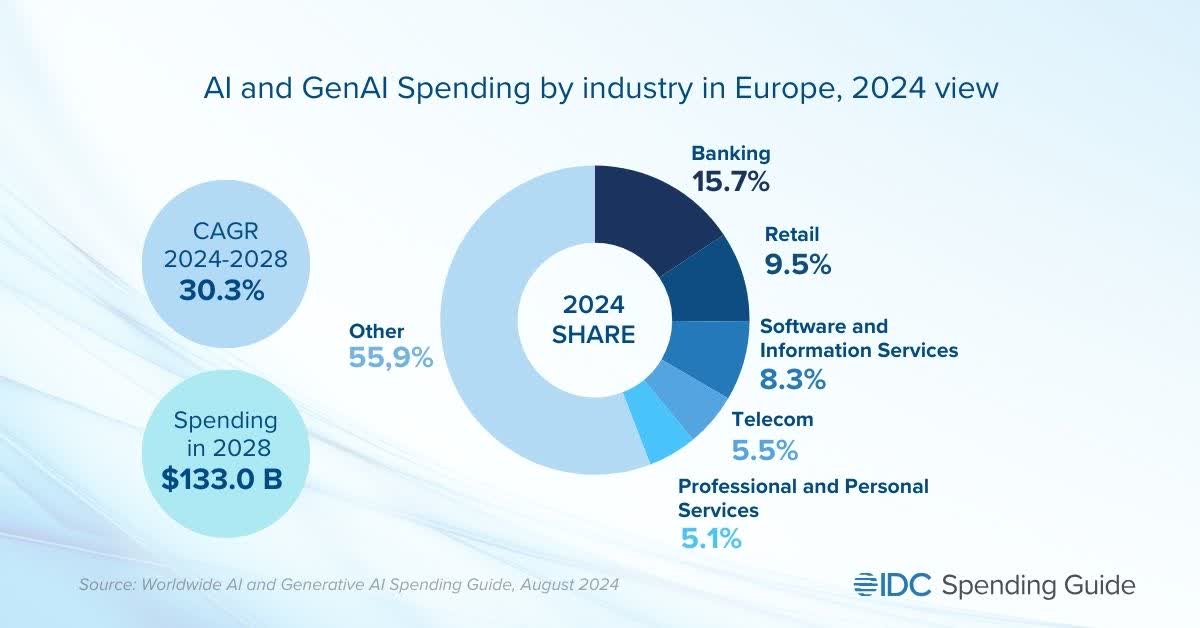

When looking at different studies, we see the expectations of high growth rates for several years to come, and Nvidia certainly might profit. IDC, for example, is expecting spendings on AI to grow with a CAGR of 30% in the years 2024 to 2028 in Europe.

IDC

And for global spendings, IDC is expecting a growth rate of 29.0% until 2028. Fortune Business Insights is expecting a CAGR of almost 40% for the years until fiscal 2032 and Grand View Research is expecting a similar high CAGR of 37.6% for the global market until fiscal 2030. But when thinking about the hype cycle and inflated expectations, we certainly have to question how realistic these studies and growth expectations are. As I have written above, forming similar bullish opinions about an asset class is a typical sign of a bubble. It might be that most investors, most analysts, and many studies are just too bullish at this point.

Conclusion

An important part of being an investor is being humble all the time and realizing when one might have made a mistake – and we all make mistakes constantly. Nobody can be right about every sector, every stock, or the economy all the time. In such a scenario, we have to adjust accordingly.

And I might have been wrong about Nvidia. The stock was and still is overvalued, but I have underestimated the growth rates the company can report now for several quarters in a row, which are to some degree justifying the high stock price. That does not mean I am now bullish about Nvidia – I still think the stock is expensive and not a good investment. But I might have been too pessimistic about the stock in the past two years and clearly underestimated the growth potential of the business. While I still see huge downside risk for the stock in the coming quarters, the fear of a lost decade might not be justified for Nvidia.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of META either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.