Summary:

- NVDA revenue decreased by 21%, significantly impacted by its gaming market platform which saw a year on year decrease in revenues of 46%.

- The company is experiencing a massive inventory glut with inventory levels doubling in just 12 months.

- Management returned value to shareholders to the tune of $1.2 billion during quarter through share repurchases and dividends.

- Despite exceeding analysts’ expectations and the current AI enthusiasm, financial performance continues its slowdown and should not be taken lightly.

Justin Sullivan

Business Overview and Investment Thesis

Nvidia Corporation (NASDAQ:NVDA) is an important player in the semiconductor industry, operating as a fabless chip designer. The company designs a range of products, including graphics processing units also called GPUs, central processing units (CPUs), data processing units (DPUs), and network interface controllers (NICs). NVDA is truly known for its GPUs which one could argue are the backbone of the company’s business. With this range of products, NVDA serves markets including gaming, data centers, professional visualization, autonomous vehicles, and OEMs.

During my previous article, I explained how NVDA is a well-established player in the semiconductor industry. The company’s robust financials combined with its strong position in key markets such as the Data Center and Gaming markets give it substantial room for growth. Nonetheless, uncertainty in its gaming market platform, export controls, and the volatility the stock faces are risks which are too big to ignore.

Despite exceeding analysts’ expectations and the current AI enthusiasm, the financial results during the fourth quarter left the company with the same or even with greater uncertainty. The gaming market platform revenue has slumped and recorded about half of the revenues reported during the same period last year. Further to this, the Data Center revenues are holding up the company‘s top line, however with a slowdown in the cloud computing market, this market platform could see revenue growth decelerate. These uncertainties continue to lead me to rate this stock as a hold. Let‘s look at how the company performed during the fourth quarter.

Nvidia 4Q-23 Results

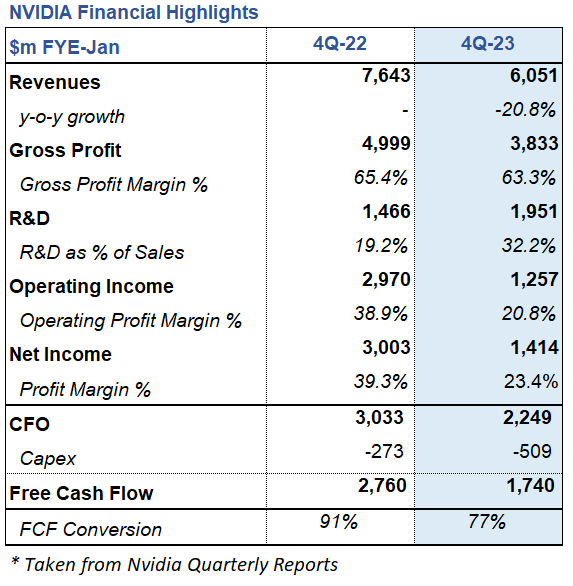

Nvidia Quarterly Financial Highlights (Company‘s 10-Q)

During the fourth quarter of FYE 2023 NVDA recorded a decline in revenue of 21% to $6.1 billion. Revenue decline was driven by the gaming market platform which saw a decrease of 46% to $1.8 billion compared to $3.4 billion during the previous year. This decrease was driven by disruptions in China gaming demand and overall lower sales. It should be mentioned that quarter on quarter gaming revenues increase by 16% due to the company‘s new GPUs (GeForce RTX). Additionally, the market platforms Professional Visualization and OEM & Others also saw a decrease in revenues of 65% and 56%, respectively. As we can see these are major decreases in revenues. The overall revenue decline was partially offset by the company‘s Data Center and Automotive platforms which saw increases of 11% and 135%, respectively.

Financial performance was further slumped by an increase in operating expenses of 23% year on year, with R&D expenses increasing to $2 billion and accounting for 32% revenues. These increases depressed operating income by 40% to $1.8 billion compared to $3 billion during the same period last year. As a result, NVDA reported a net income of $1.4 billion with a profit margin which almost halved to 23.4%.

Despite seeing a slowdown in revenues and a bottom line significantly depressed, NVDA was able to post a free cash flow of $1.7 billion for the period. The free cash flow was used to return value to shareholders to the tune of $1.3 billion through share purchases amounting to $1.2 billion and dividends of $98 million. The rest of the cash was used to bolster the company‘s balance sheet increasing cash and cash equivalents to $3.4 billion.

Market Platforms Results

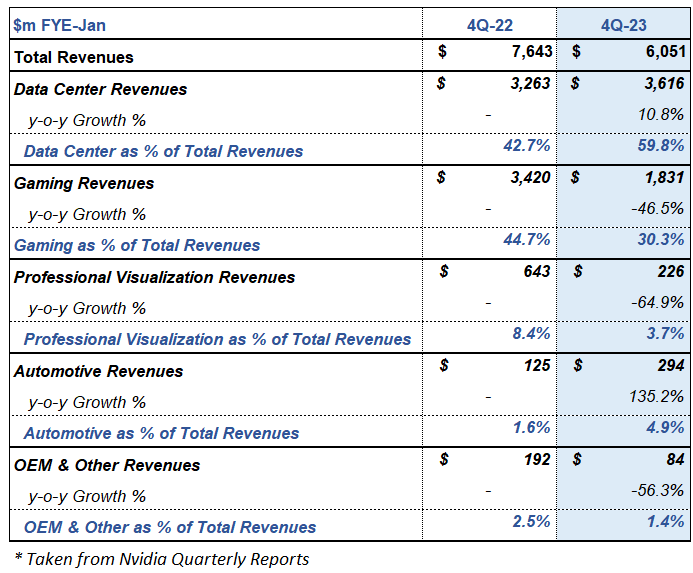

Nvidia Market Platforms Highlights (Company‘s 10-Q)

From the table above we can see that the Data Center platform is clearly holding up revenues for NVDA. Data Center revenue saw an increase of 11% compared to the same period last year driven by U.S. cloud service providers. However, the company did report a slowdown in China, which is also reflected in the slowdown in cloud revenues from the top cloud computing providers in the country. Automotive revenues saw an impressive triple digit increase in revenues led by growth in sales of self-driving solutions and computing solutions for electric vehicle makers. Due to the growing trend in self driving solutions and electric vehicles, we could see this market platform continue to increase revenues during the next quarters. Despite these increases in revenues, three market platforms saw significant declines in revenues during the quarter. Gaming has already been discussed, in regards to Professional Visualization and OEM & Other, these market platforms also saw declines to the tune of 65% and 56%, respectively. Professional Visualization decrease was mainly impacted by lower sales while OEM and Other was impacted by Cryptocurrency Mining Processors, which reflects the impact of certain market trends, specifically the crash of the cryptocurrency market during the previous quarters.

Key Takeaways

Gaming slowdown continues: The Gaming platform has slowdown significantly during the previous quarters and as of the latest quarter report it accounts for 30% of total revenues. This is a stark difference compared to one year ago when it accounted for almost half of NVDA revenues. The announced partnership with Microsoft and Activision Blizzard could enhance revenues however the gaming market as a whole will need to see a rebound before NVDA is able to achieve its previous results.

Data Center revenue growth could see deceleration: Data Center continues to be the stronghold of NVDA overall revenues. However, it is no secret that the cloud computing market has seen a slowdown during the latest quarter, with the main cloud computing providers seeing growth rate declines all across. Please refer to my article on the leading cloud computing providers for more information about this topic. Furthermore, Chinese cloud computing providers have reported flat or slight increases in revenues. As such, these cloud computing providers could try to decrease costs which could impact the revenues for NVDA. I will follow this closely during the next quarter results of NVDA as well as the numerous cloud computing providers.

Inventory Problems: Similar to many semiconductor companies, NVDA has seen an inventory glut during the year. For reference at the end of FYE 2022 NVDA had inventory levels of $2.6 billion, fast forward 12 months and the inventory levels are now at $5.2 billion. Now the question is, will NVDA be able to offload this inventory at full price or will it need to offer heavy discounts to go back to more efficient inventory levels? I am weighting my answer towards heavy discounts.

Bottom Line

As mentioned at the start of the article despite exceeding analysts’ expectations and the current AI enthusiasm, the financial results during the fourth quarter left the company with the same or even greater uncertainties. Revenue has slumped in three of its five market platforms, inventory levels have doubled within 12 months and the cloud computing market could see a slowdown in the coming months. All these uncertainties continue to lead me to rate this stock as a hold. It is true that the potential for growth is significant however with the stock priced at a P/E multiple above 50 times, I would recommend investors to wait for a more attractive entry point or until uncertainties have diminished.

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.