In recent years, Nvidia has transformed from a simple GPU manufacturer into a leading AI powerhouse, driving significant growth and returns for investors.

As the company has gotten more expensive, some may be looking to reposition into NVDY, the ‘covered call’ version of NVDA.

While the logic makes sense, we think NVDY is a poorly constructed wrapper you should avoid.

While it may be a while before NVDA’s business ‘catches up’ with the stock, holding this long-term winner appears to be optimal.

Consequently, we rate NVDA a ‘Hold’ and NVDY a ‘Sell’.

Monty Rakusen

In case you’ve been living under a rock, Nvidia (NASDAQ:NVDA) has been on quite the run over the last few years.

What once was a simple GPU manufacturer has blossomed into a fully-fledged AI juggernaut, focused on designing and supplying the compute base of tomorrow. As Nvidia has released leading AI chips, infrastructure, and software, the company’s financials have exploded, which has led to a significant increase in the stock price.

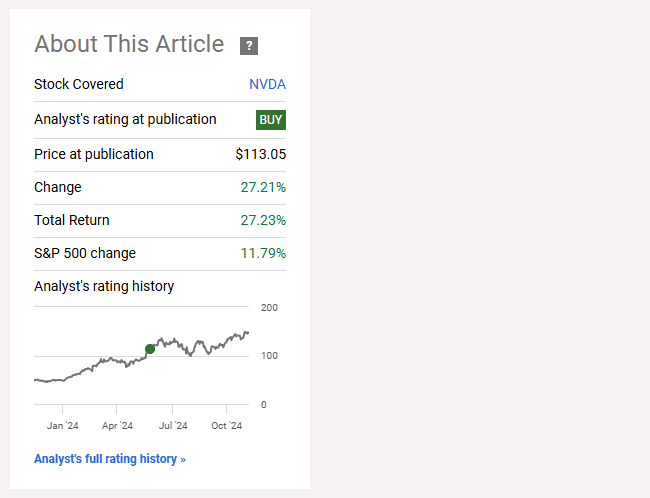

In May, we argued that – while expensive – NVDA shares were still a ‘Buy‘, based on the company’s strong margins, addressable market, and growth projections. Since then, the stock has outpaced the S&P 500 handily, much to the celebration of investors:

Seeking Alpha

At the same time, YieldMax, a new ETF issuer, has recently burst onto the scene by offering ‘covered call’ ETFs focused on a number of popular stocks.

One of their top funds, NYSEARCA:NVDY, the YieldMax NVDA Option Income Strategy ETF, focuses on selling calls on NVDA exposure, thus maximizing yield for investors.

However, as time has gone on and NVDA has gotten more and more expensive, a question has emerged: Is NVDY the better option?

In the event that NVDA’s best days are behind it, it seems possible to imagine that NVDY may outperform the underlying stock going forward, especially if shares begin to trade sideways or trade down for an extended period.

Today, we wanted to explore NVDA’s prospects, re-examine NVDY, and come up with an answer to the following question: Which is the better buy for the foreseeable future – NVDA, or NVDY?

Let’s dive in and find out.

NVDA’s Earnings

As always, let’s start with the financials.

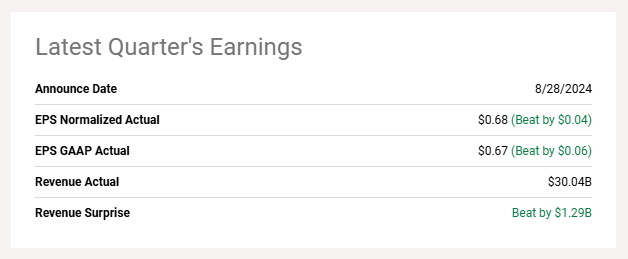

Since we last wrote about the stock, NVDA has reported earnings once, with the next report scheduled for next week.

In short, the report in September showcased just how far NVDA has come in a year. In Q2, the company reported a beat on the top line, a beat on the bottom line, and YoY sales growth of over 120%, which is absolutely incredible:

Seeking Alpha

The company was also able to maintain gross and net margins at the 75% and 55% level, respectively, which is a huge accomplishment. These margins go to show just how big NVDA’s current lead is, in what has historically been a competitive market.

Keep in mind that these stats also come as the company begins to lap 2023numbers, which came in after NVDA began to see explosive revenue growth in the AI segment. This lapping of expanded comps shows how the business continues to grow, and how big the opportunity really is.

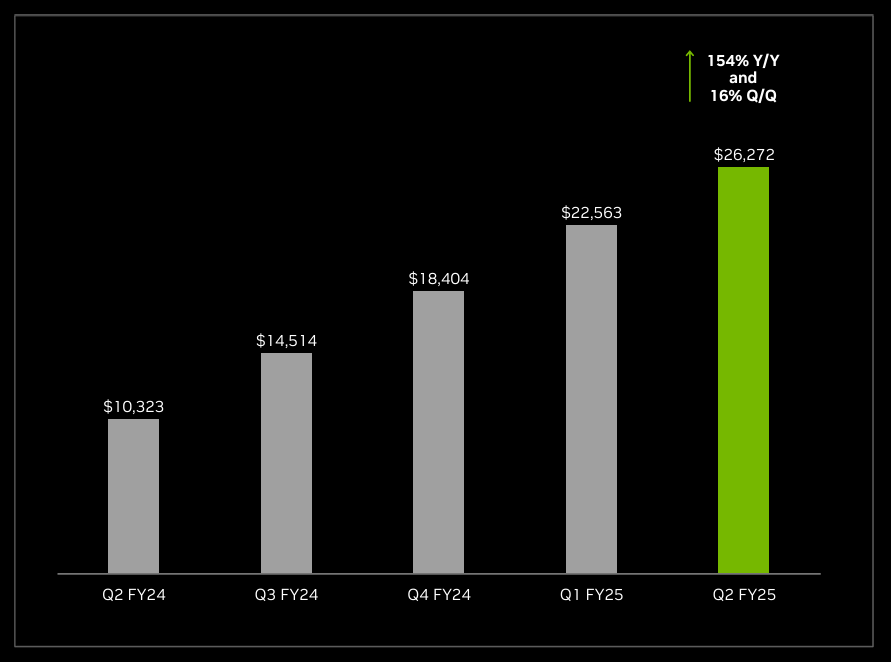

On the business side, a lot of this outperformance has been driven by NVDA’s H200, InfiniBand and Ethernet solutions for AI compute and networking. As this hardware has begun/continued to sell like hotcakes (the H200 launched in Q2), Data Center revenues have continued to charge up and to the right:

IR

At the same time, the company’s highly anticipated Blackwell release should hit shelves in Q4 and continue into next year, which should lead to significant further growth in revenue. For Q4 alone, management is expecting to ship billions of dollars in sales of the new architecture:

Blackwell is widely sampling, and production ramp is scheduled to begin in Q4 and continue into F2026; expect to ship several $B in Blackwell revenue in Q4.

This comes after a reported delay for Blackwell due to a design issue, which has been 100% remedied by the company as of mid-October.

Blackwell is particularly important for Nvidia given how drastically it impacts compute performance on an overall basis, as we’ve argued before:

More broadly, Blackwell, NVDA’s new AI compute architecture, is making a huge splash due to the platform’s ability to run trillion-parameter AI models at a fraction of the cost and energy consumption – up to 25x less…

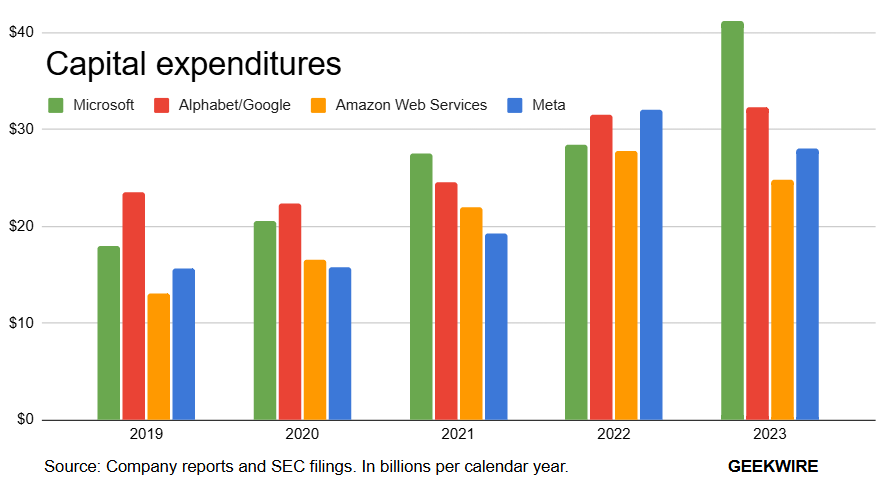

This should drive serious, long tail demand for NVDA’s data center compute and networking products, as Capex amongst the largest players has only grown over time, and we expect that AI will send these numbers even higher:

Geekwire

For CSP’s and other big AI customers, this performance boost is absolutely crucial.

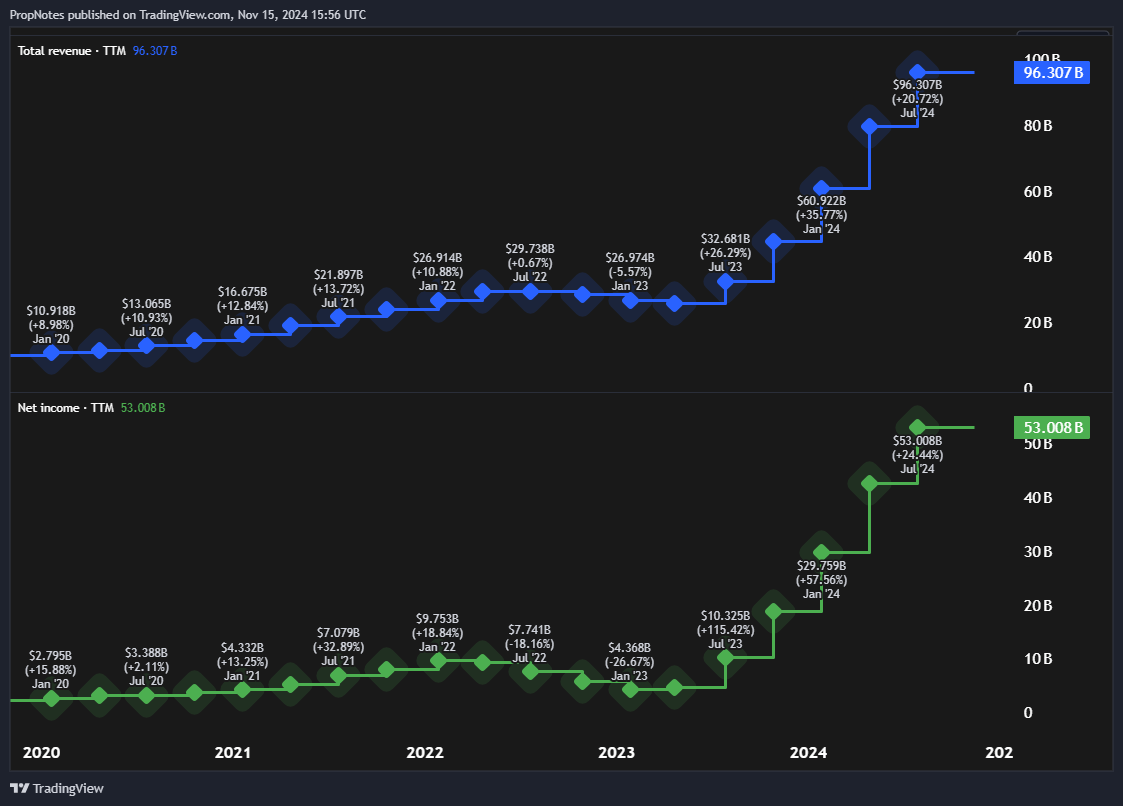

As the company currently sits, the business is producing TTM $96 billion in sales, and TTM $53 billion in net income:

TradingView

Looking ahead, if you include the company’s ongoing top and bottom-line growth, we see revenues continuing to surge towards a $40 billion per quarter run rate.

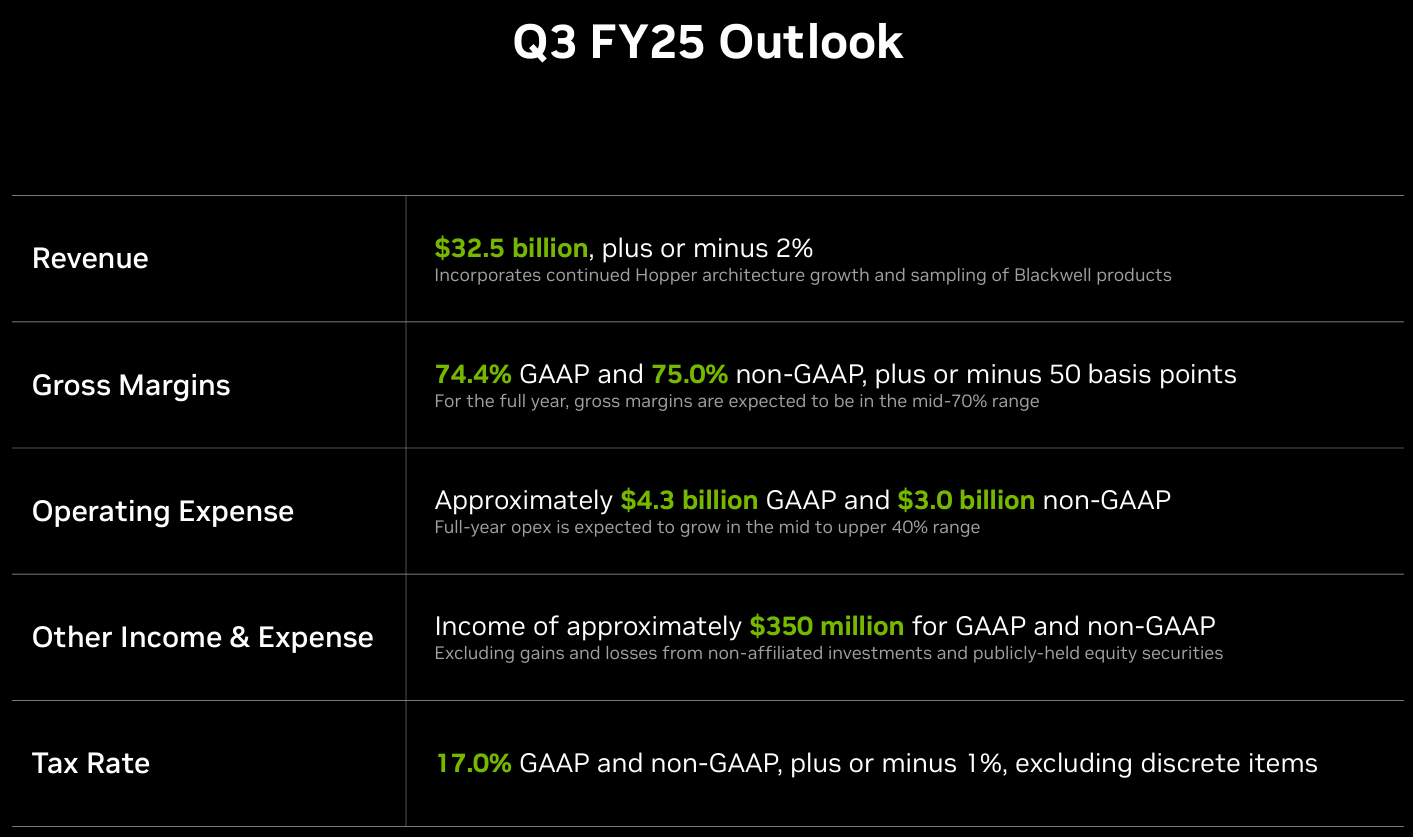

For Q3, management has projected $32.5 billion in revenue, ~74% gross margins, and $4.7 billion in expenses:

IR

This could lead to EPS in the ~$0.75 range, which would be an all-time record for the company.

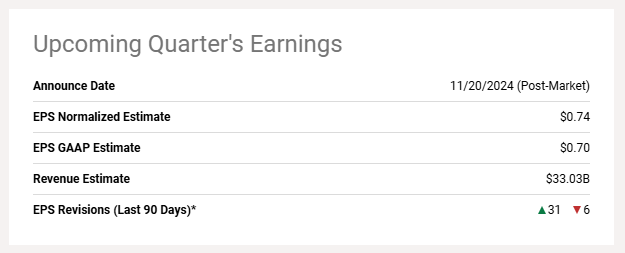

Similarly, analysts are expecting a big quarter:

Seeking Alpha

Of note, here – analysts have recently been raising EPS revisions on balance, which reflects the company’s expected, continued strength in the H200, InfiniBand, and Ethernet markets, alongside the potential growth of Blackwell.

When NVDA reports next week, we’ll be watching the company’s gross margins closely, as these dictate the cost structure and profitability of the rest of the firm. Additionally, management’s commentary on the earnings call around Blackwell timing and how the flaw impacted the release schedule will be key.

That said, no matter what happens in the short run, it’s clear to us that NVDA is still in the early to middle innings of organic growth when it comes to capitalizing on this market opportunity.

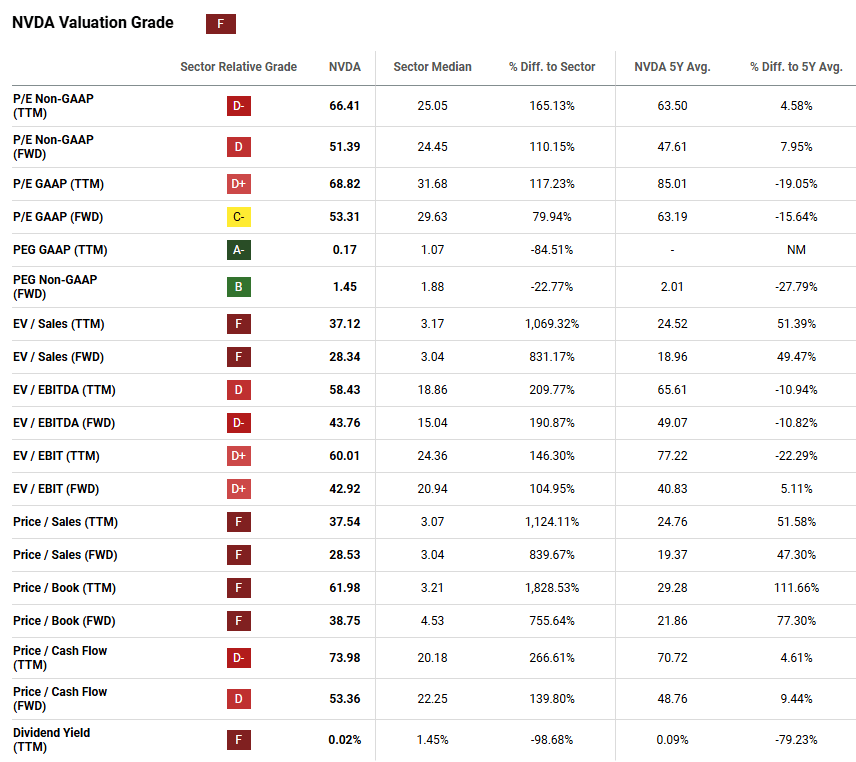

NVDA’s Valuation

At the same time, while we’re bullish on NVDA’s business, a lot of this potential growth seems to have already been baked into the stock price.

Looking at NVDA’s valuation ratios, the stock appears extended:

TradingView

On a sales basis, shares are trading at a 36x sales ratio. On that basis alone, the company appears to be one of the most expensive companies on the market.

Of course, this ratio only appears too expensive due to the company’s very high net margins, but it’s still something to think about.

On the bottom line, which is far more important in cases like this, NVDA trades at 67x TTM earnings, which is also quite expensive. Of course, this valuation is lower than it has been in two years, but those quarters had a high level of expected future earnings to account for.

When you bake in NVDA’s projected growth, the multiple becomes a bit easier to handle:

Seeking Alpha

Seeking Alpha’s quant rating system does give the stock an ‘F’, but looking at the PEG, we see that on a FWD basis NVDA has a PEG in the 1.45 range, which is relatively low for the sector. Interesting.

In our view, though, we expect NVDA’s growth rates to slow down, simply as a function of the company’s current size. Sure, the nominal increases will likely remain high, but as the market saturates and the rate slows, the denominator in the PEG above, for year two+ will likely shrink, which means that the stock once again appears expensive looking out past 2025 and into 2026 & further.

Why does any of this matter?

Well – two reasons.

First, if you’re an NVDA investor, then the stock’s current valuation, which appears somewhere between premium and super premium, becomes potentially problematic. Even if NVDA can grow the top and bottom line substantially, as we believe they will, we still could see middling stock performance as the company ‘catches up with’ the shares.

Second, Is NVDY a better choice in the event the stock trades down or sideways for a while?

NVDY’s Construction & Performance

NVDY, if you don’t know, is a covered call fund. This means that the fund builds a position in NVDA via options and then sells call options on the exposure.

This, in theory, gives investors a high level of income, with some potential upside appreciation.

If NVDA trades sideways, it stands to reason that it could be a perfect option to consider – the upside you forfeit doesn’t matter as much, and the income could produce higher total returns.

At present, many other analysts seem to think NVDY could be a good option in the exact case we’ve outlined, or as a great underlying exposure that you can use to generate high levels of yield:

Seeking Alpha

Here’s the problem, though.

As we’ve argued before, NVDY isn’t as simple as it sounds. Many investors look at NVDY and think some version of the following:

“NVDA is a ‘high quality’ underlying stock, and I’m willing to trade some of this upside for a high dividend yield”

The problem comes when you look at how NVDY is constructed.

In short, NVDY investors appear doomed to long term principal erosion as a result of the following mechanic:

The real issue with NVDY is that the fund pays out the option premiums it collects as “yield” whether [or not] selling the options was a profitable trade in the first place…

Imagine that there was a fund that bought and sold a particular stock once every month. Let’s say that the fund’s trading strategy wins about 70% of the time, and every win makes about 2%. Not bad, right!

Here’s the problem. Let’s imagine that the same fund pays out 2% of its assets, whether or not the monthly trade made any money. This is functionally what these high-yield ETFs are doing.

(edited for brevity and readability)

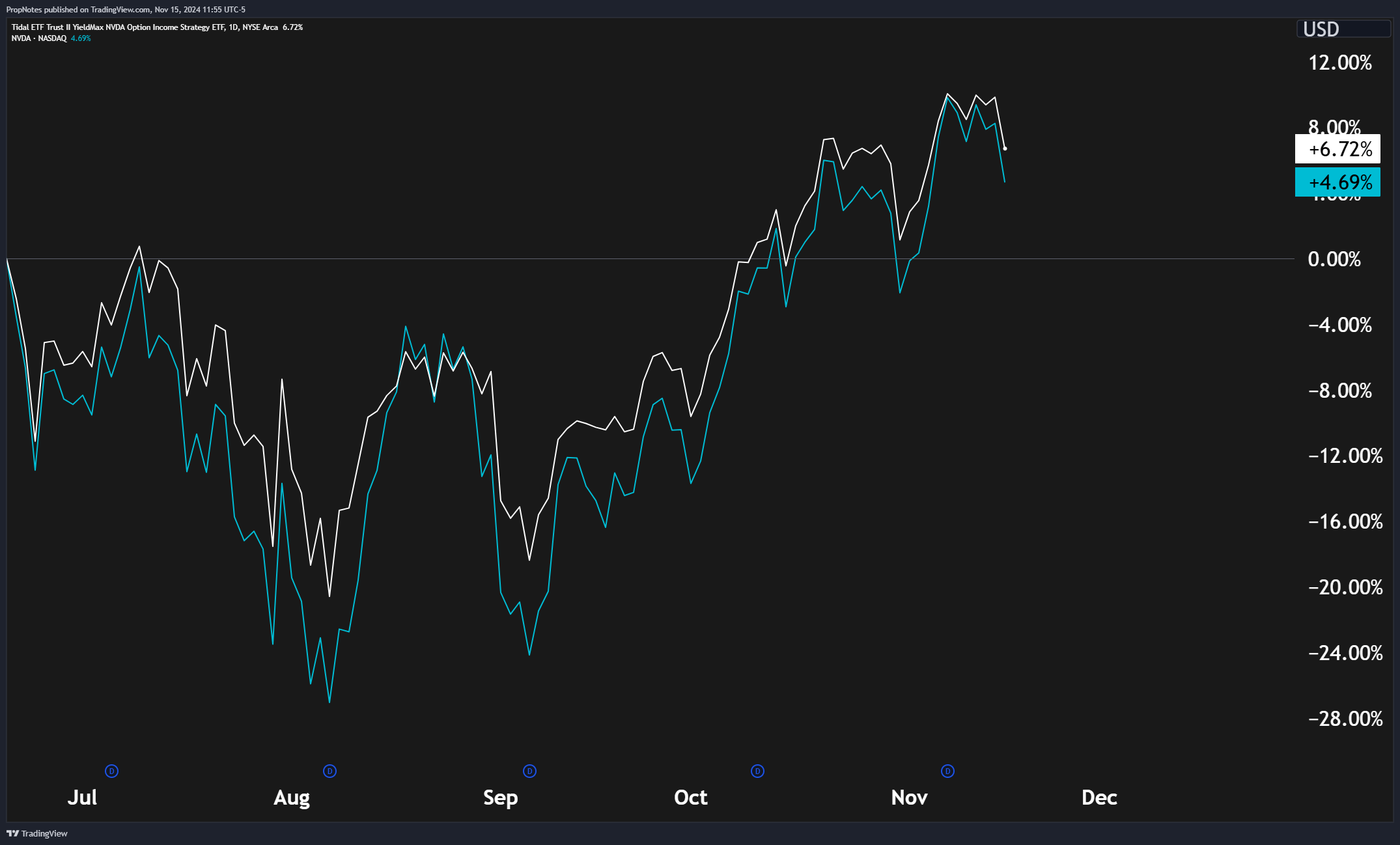

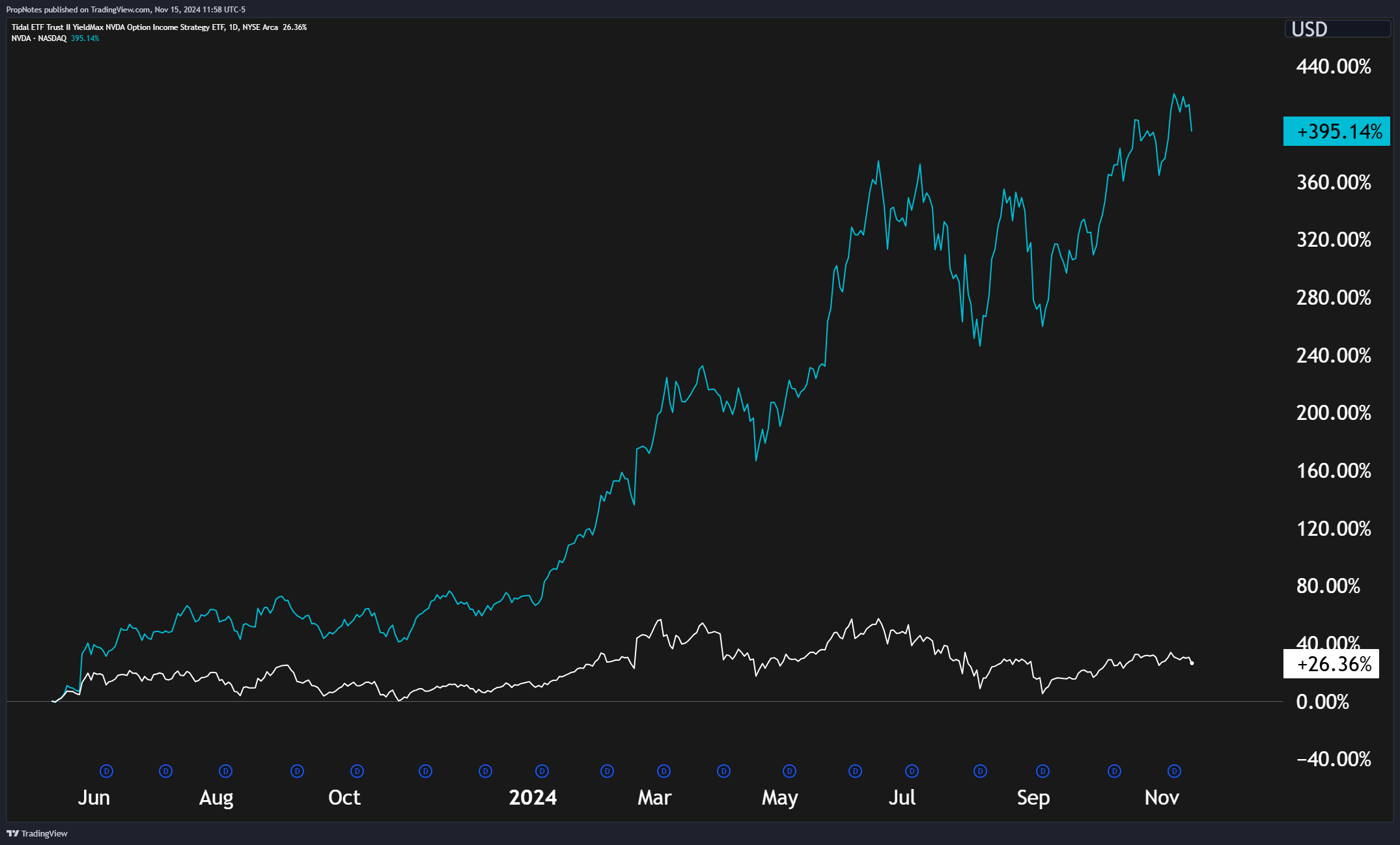

Thus, even in sideways markets, NVDY hasn’t been able to outperform NVDA materially:

TradingView

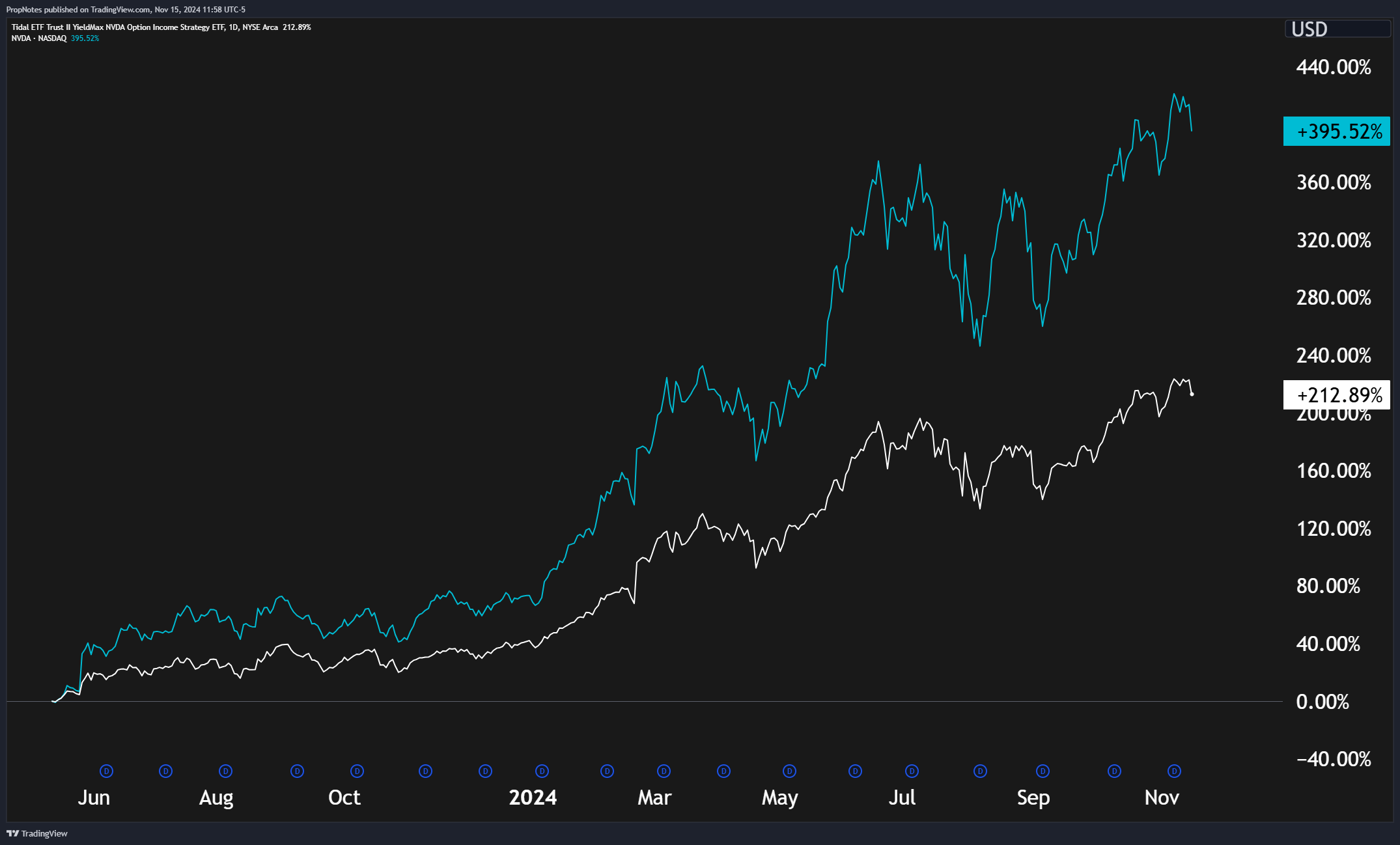

The chart above is also us cherry picking the worst possible period for NVDA vs. NVDY. Long term, the fund has been an underperformer, both with and without dividends included:

With Dividends (TradingView)

Without Dividends (TradingView)

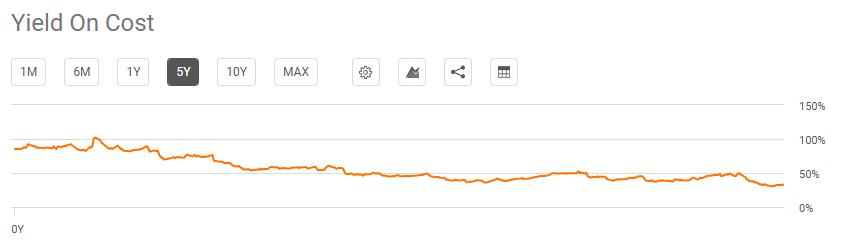

And, while NVDA’s incredible underlying performance has been able to buoy NVDY’s Yield on Cost thus far, as the stock appears primed to return to a more normal distribution of returns, we expect to see significant principal erosion and falling payouts going forward, which we’ve seen in other YieldMax ETFs like TSLY:

TSLY’s YoC (Seeking Alpha)

As a result, while NVDY might appear to be a good option for investors seeking to ‘downshift’ from NVDA, we think the fund isn’t a viable option due to the mechanisms we’ve described.

Summary

All in all, we see NVDA as a ‘Hold’ and NVDY as a ‘Sell’. As the underlying stock has gotten more expensive, we’ve become wary of the price, hence the hold rating.

At the same time, as some have looked to NVDY as a better portfolio construction ‘tool’, we see a poorly constructed wrapper that likely won’t outperform NVDA’s total return in the long run.

Thus, our ratings-

If you’re in NVDA, keep holding. If you’re not, then try to wait for a pullback. And if you’re thinking about NVDY, or already in it, then it may be time to look elsewhere.

Stay safe out there!

Analyst’s Disclosure:I/we have a beneficial long position in the shares of NVDA either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.