Ahead of its upcoming Q2 FY2025 report, Nvidia Corporation stock is experiencing significant volatility. While a double beat is likely, the sustainability of Nvidia’s rapid growth and high margins remains uncertain.

Despite Nvidia’s strong business performance and leadership in the burgeoning AI chips market, I maintain a “Neutral/Hold” rating due to valuation concerns and a troublesome technical setup.

In this note, we shall preview Nvidia’s Q2 FY2025 report and take stock of Nvidia’s long-term risk/reward.

BING-JHEN HONG

Introduction

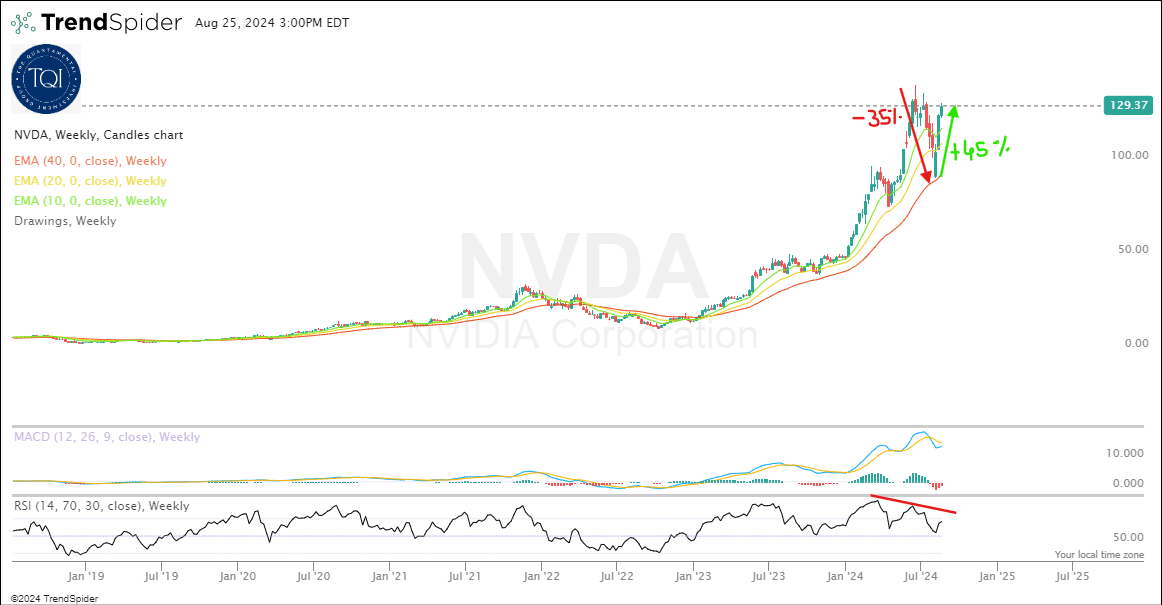

After striking a blow-off top in mid-June, Nvidia Corporation (NASDAQ:NVDA) stock has experienced significant volatility – with NVDA tumbling by nearly 35% from ~$140 to ~$90 per share from mid-July to early August. However, with the unwind of the yen carry trade taking a pause and earnings excitement taking hold, Nvidia’s stock has rebounded by +45% to ~$130 per share, heading into the semiconductor giant’s Q2 FY2025 report on Wednesday, 28th August 2024.

NVDA Weekly Stock Chart 08/23/2024 (TrendSpider)

If you have been following my work on Nvidia, you know that I have been “Neutral” on this semiconductor giant for several quarters now – despite acknowledging Nvidia as one of the most obvious “picks and shovels” plays for the era of GenAI. Here’s an excerpt that explains my stance:

Since its breakout Q2 FY2024 results, NVDA stock has gone up in parabolic fashion, and I have missed this astronomical run [coming close to getting on board at ~$45]; however, at $100 per share, I see little to no margin of safety here because NVDA stock seems overvalued despite the use of generous assumptions for long-term margins and sales growth in our model.

Now, in the case of Nvidia, I have been a broken record for a while, but I have to say this again –

Nvidia Corporation is a great company with market-leading products and arguably the best CEO in the semiconductor industry. However, the price we’re being asked to pay for Nvidia is too steep, in my opinion. In a zero-interest rate world, investors can afford to be valuation agnostic; however, we are no longer operating in such an environment, with the FED still pulling liquidity out of financial markets and a bank credit tightening cycle in effect after multiple bank failures.

Despite running the risk of missing out on further gains in NVDA stock, I choose to remain on the sidelines here. FYI, I have been wrong about NVDA stock in the past, and I could be wrong again. While Nvidia is performing exceptionally right now, the current price tag leaves little to no margin of safety for a long-term investor.

While GenAI demand still appears to be insatiable, the quantum of revenue beat is getting smaller, and Q2 top-line guidance was in line with buy-side expectations. Furthermore, Nvidia’s management guiding for a margin contraction for the back half of FY2025 is ample reason for investors to take a pause.

Nvidia is clearly winning big in the era of Gen AI; however, this initial-stage demand growth jump could yet be temporary in nature. Yes, Nvidia is trading at just ~35-40x forward P/E, but margins could be peaking here (at least for the short term). With all of its major customers building AI chips in-house (potential risk to revenues and margins), I see a genuine lack of a margin of safety here.

In my view, Nvidia Corporation remains the most obvious “picks and shovels” play in the AI gold rush; however, a lot of future success is already baked into Nvidia’s current stock price, and the long-term risk/reward doesn’t justify allocation of fresh capital right now. Due to unfavorable risk/reward and sheer lack of a margin of safety, I am going to stick to the sidelines on Nvidia Corporation stock.

Key Takeaway: I continue to rate Nvidia Corporation stock “Neutral/Hold” at $100 per share.

Author’s Coverage History for Nvidia (Seeking Alpha)

In today’s note, we shall preview NVDA’s upcoming report and re-evaluate the stock using TQI’s Quantamental Analysis process to see if it’s a buy/sell/hold at current levels.

What Is The Earnings Forecast For NVDA?

In its Q1 FY2025 CFO commentary, Nvidia’s leadership guided for Q2 FY2025 revenues to be in the range of $27.44-$28.56B, implying +107% y/y and +7.5% q/q growth at the midpoint of the guidance range [i.e., $28B]. With triple-digit y/y sales growth, the AI party at Nvidia looks far from over heading into its Q2 report.

Nvidia Investor Relations

However, the quantum of top-line beats has narrowed significantly in recent quarters, and the projected gross margin contraction in the back half of FY2025 raises concerns about the sustainability of Nvidia’s rapid growth and ultra-high margins.

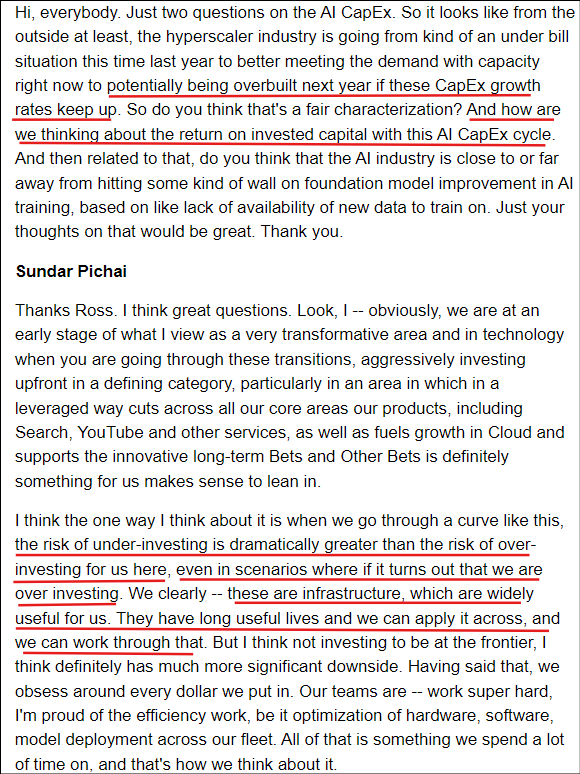

With cloud hyperscalers building their own in-house AI chips and partnering with other players [like Advanced Micro (AMD)], I am not sure whether the worries around Nvidia’s demand sustainability will ever go away. Earnings call commentary on AI CAPEX spending plans from the hyperscaler honchos – Microsoft’s (MSFT) Satya Nadella, Alphabet’s (GOOG, GOOG) Sundar Pichai, and Amazon’s (AMZN) Andy Jassy – suggested robust near-term demand for Nvidia’s AI GPUs despite a lack of clarity over ROI.

For example, Alphabet spent $13B on AI CAPEX in Q2 and plans to spend $12B+ per quarter for the foreseeable future. However, when asked about ROI on this aggressive spending cycle, CEO Sundar Pichai discussed their ability to work through an infrastructure overbuild, if GenAI fails to deliver on its promise:

Alphabet Q2 2024 Earnings Call Transcript

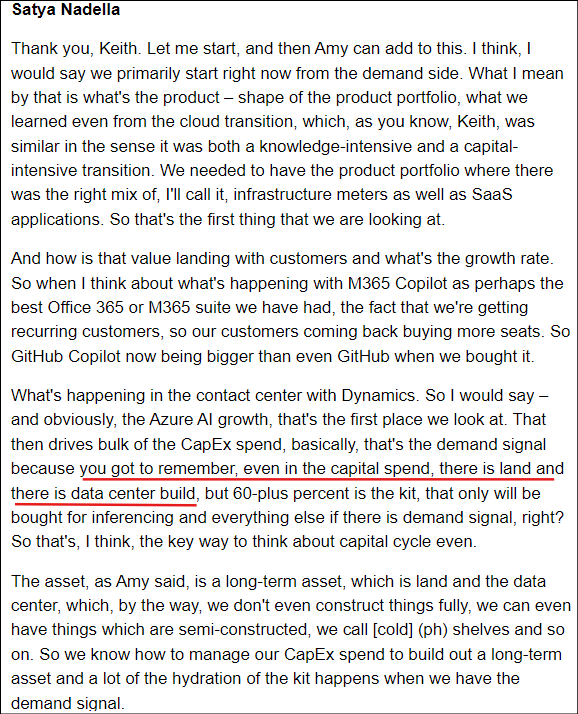

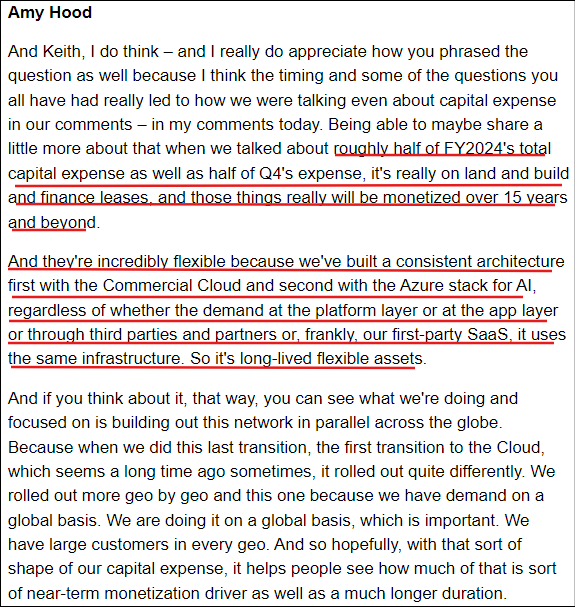

Nadella and Jassy provided similarly vague answers on the ROI of their respective AI CAPEX, alluding to the useful life and alternative use of this AI hardware in cloud computing. They also referred to this CAPEX spend as a long-term asset due to a large portion going into land, buildings, and financial leases that will be amortized over 15+ years.

Microsoft Q4 FY2024 Earnings Transcript

Microsoft Q4 FY2024 Earnings Transcript

By committing to increased spending on AI infrastructure for the near term, I believe the hyperscaler honchos have boosted some animal spirits, driving the parabolic run-up in Nvidia’s stock. However, the vague answers over ROI on their AI spend and “hedging” by the cloud hyperscaler trifecta keep the risk of a growth cliff for Nvidia firmly on the table.

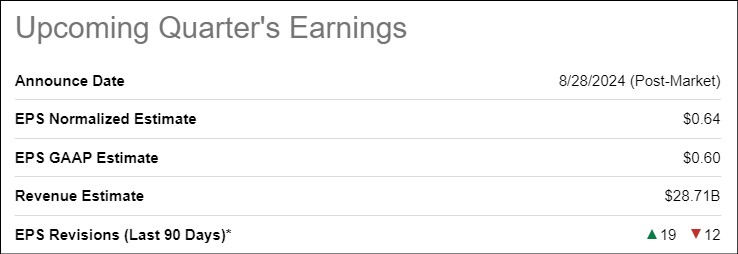

Now, that said, for Q2, Nvidia is projected to beat management’s guidance, with consensus street estimates for revenue sitting at $28.71B:

Nvidia Q2 FY2025 Estimates (Seeking Alpha)

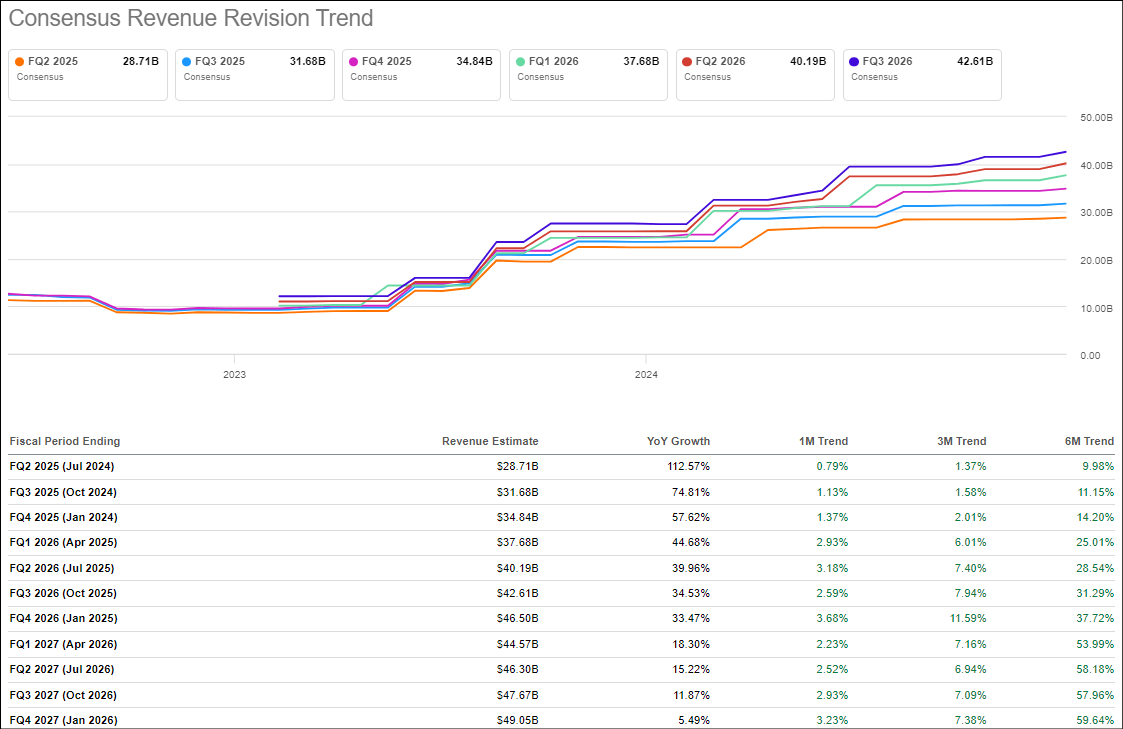

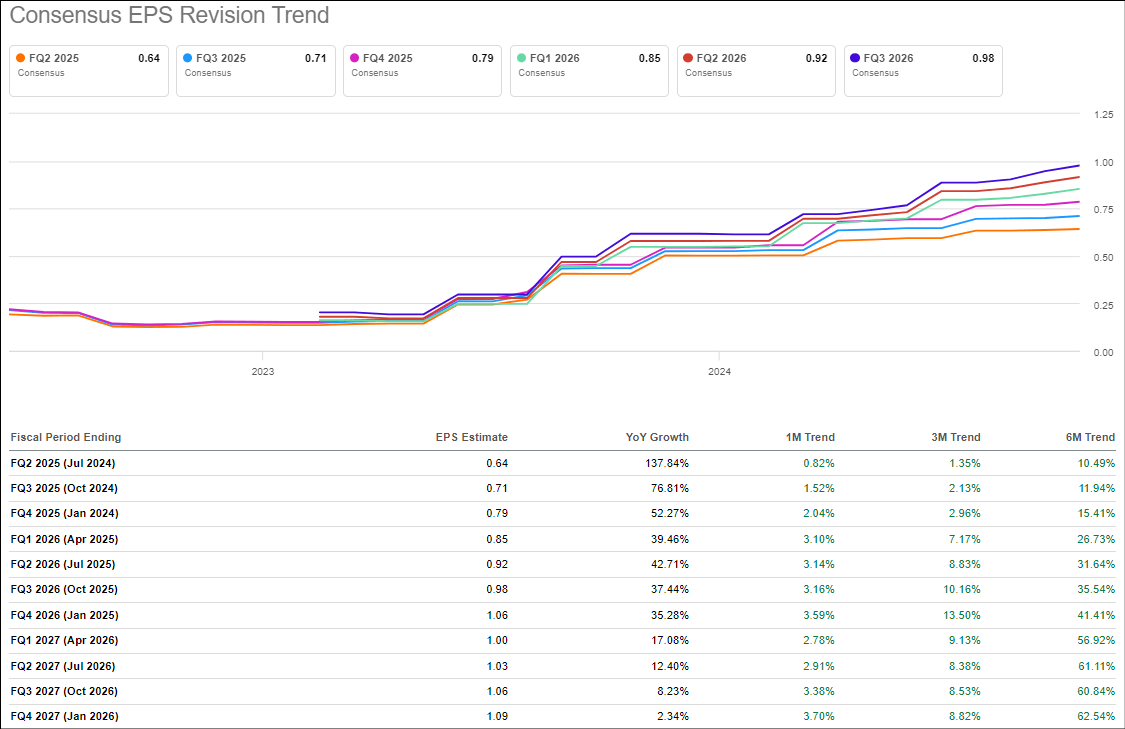

Furthermore, ahead of Nvidia’s Q2 FY2025 print, both revenue and earnings revision trends have been trending positive [i.e., analysts have been lifting their projections] with 13 “Revenue Up Revisions” and 19 “EPS Up Revisions”:

Nvidia Revision Trends (Seeking Alpha)

Nvidia Revenue Revision Trends (Seeking Alpha)

Nvidia EPS Revision Trends (Seeking Alpha)

How Was Nvidia’s Previous Earning Report?

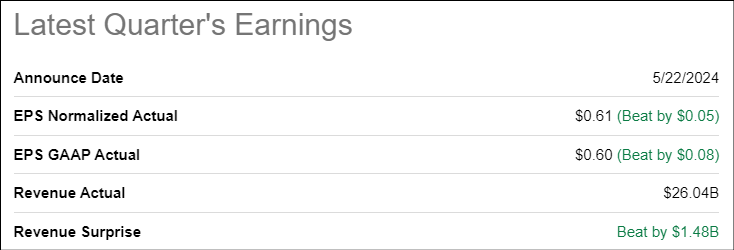

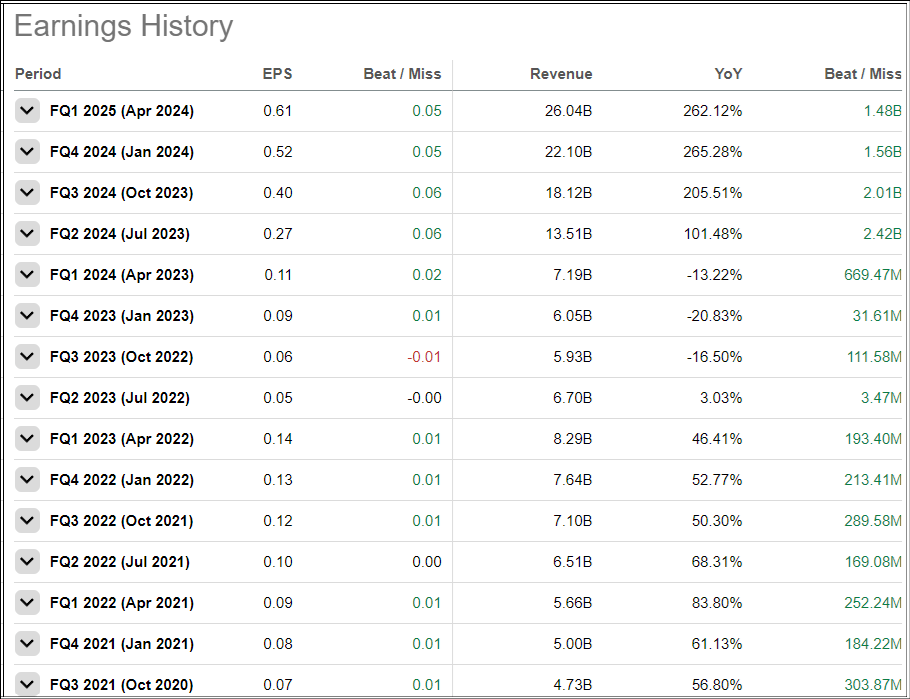

Last quarter, Nvidia eased past consensus estimates, with Q1 FY2025 revenue and normalized EPS coming in at $26.04B and $6.12, respectively.

Nvidia Q1 FY2025 Results (Seeking Alpha)

Here’s an excerpt from my Q1 earnings review note for Nvidia:

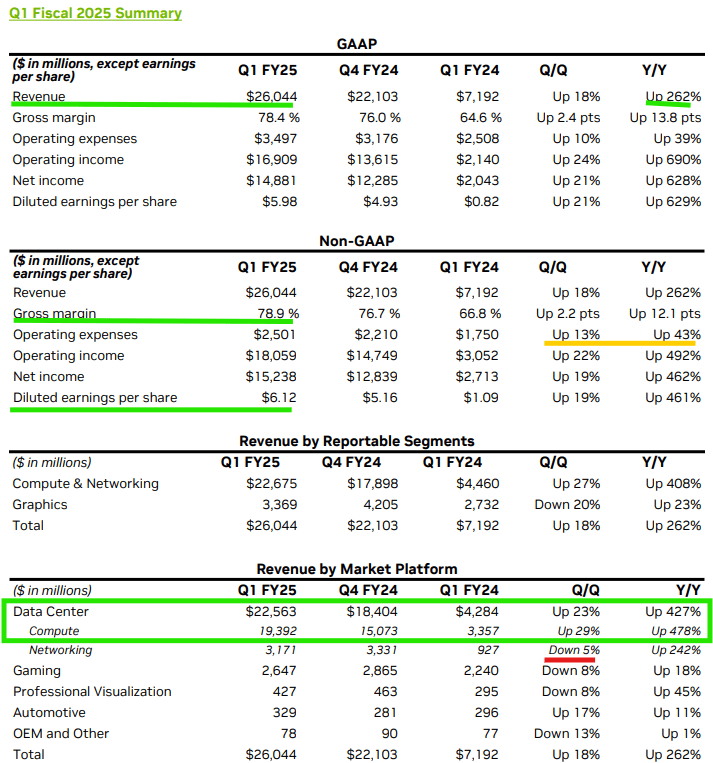

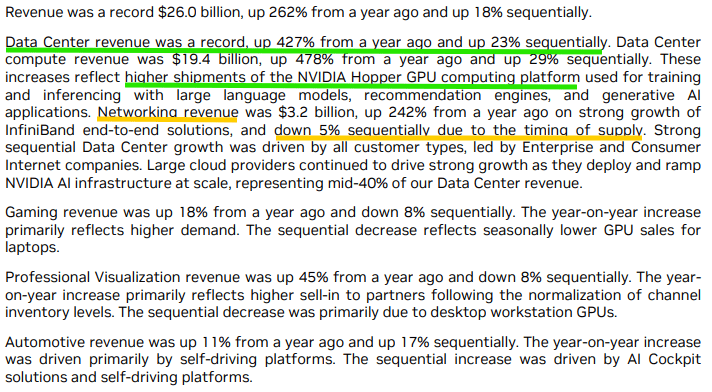

Once again, Gen-AI-induced demand for its AI GPUs drove remarkable +427% y/y growth within Nvidia’s Data Center business, which remains the primary driver of the explosive business growth Nvidia is delivering right now:

Nvidia Investor Relations

In Q1 FY2025, Nvidia’s Data Center revenue jumped to $22.56B (+427% y/y, +23% q/q) [vs. est. of ~$22B] driven by higher shipments of Nvidia’s Hopper GPU computing platform amid a gold rush for NVDA’s AI GPUs. Interestingly, Networking revenue was down -5% q/q, and this is something to keep an eye on for future quarters.

Nvidia Investor Relations

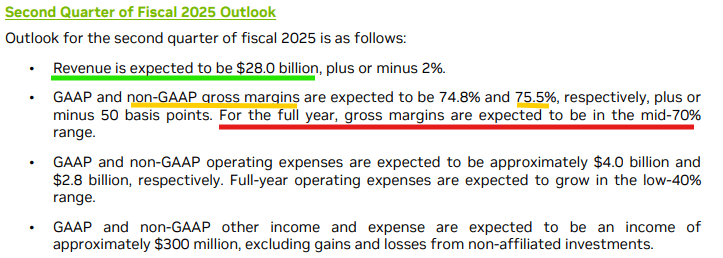

On the margin front, Nvidia’s non-GAAP gross margin expanded to 78.9%, up 220 bps over Q4 FY2024 and up 1,210 bps over Q1 FY2025. With its vast first-mover advantage in AI, Nvidia’s hardware + CUDA software ecosystem is commanding tremendous pricing power. Interestingly, the gross margin guide for Q2 calls for sequential contraction to 75.5%, with full-year gross margin guidance of mid-70% pointing to a low 70% gross margin in the back half of this year! With Blackwell GPUs, Nvidia plans to start generating SaaS revenues, but such a steep margin decline could be an indication of deteriorating pricing power. Yes, Nvidia’s management could be sandbagging, but I guess time will tell if such a margin profile is sustainable in the long run.

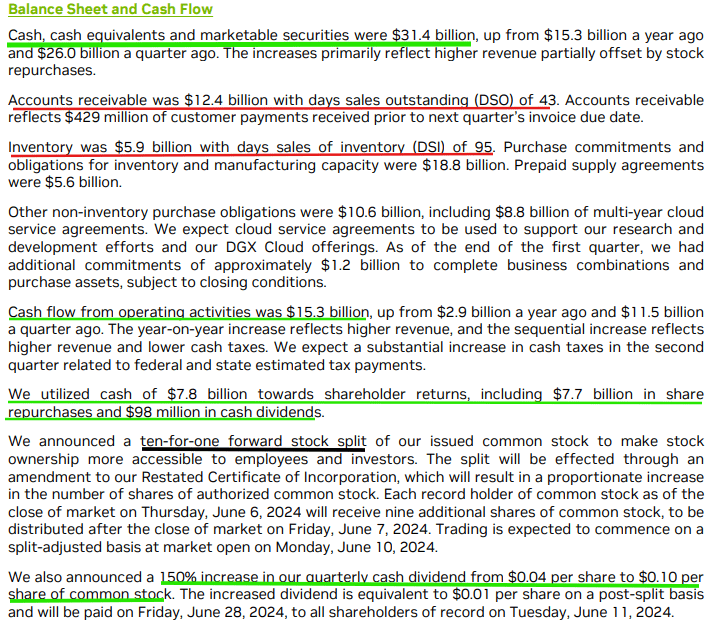

As of Q1 FY2025, the combination of explosive top-line growth and margin expansion is driving a massive AI windfall, with Nvidia’s quarterly operational cash flow jumping to +$15.3B in Q1 (up from $2.9B a year ago) [free cash flow: $14.94B]. Despite Nvidia returning $7.8B to shareholders via buybacks ($7.7B) and dividends ($98M) during Q1, the semiconductor giant’s fortress-like balance sheet keeps getting stronger, with cash and short-term investments position rising to $31.4B, up from $26B last quarter.

Given the historical cyclicality associated with semis, I still think that raising capital at a $2.4T market capitalization is a far better idea for Nvidia than returning capital to shareholders via buybacks at ~20x forward P/S.

Nvidia Investor Relations

Along with its Q1 report, Nvidia announced a 10-for-1 stock split and a 150% increase in its quarterly cash dividend. While a ten-cent dividend isn’t a game changer, the stock split could drive more volatility in NVDA shares due to greater accessibility for retail investors.

Given Nvidia’s ongoing business momentum, positive Q2 read through from its biggest customers [i.e., cloud hyperscalers], and Huang & Co’s solid track record of exceeding consensus street expectations, I believe Nvidia’s Q2 report will be better than expected.

Nvidia’s Earnings History (Seeking Alpha)

However, will a double beat on Wednesday be enough to justify the lofty investor expectations built into NVDA’s $3.1T+ market capitalization?

Concluding Thoughts: Is NVDA Stock A Buy, Sell, or Hold Ahead Of Q2 FY2025 Earnings?

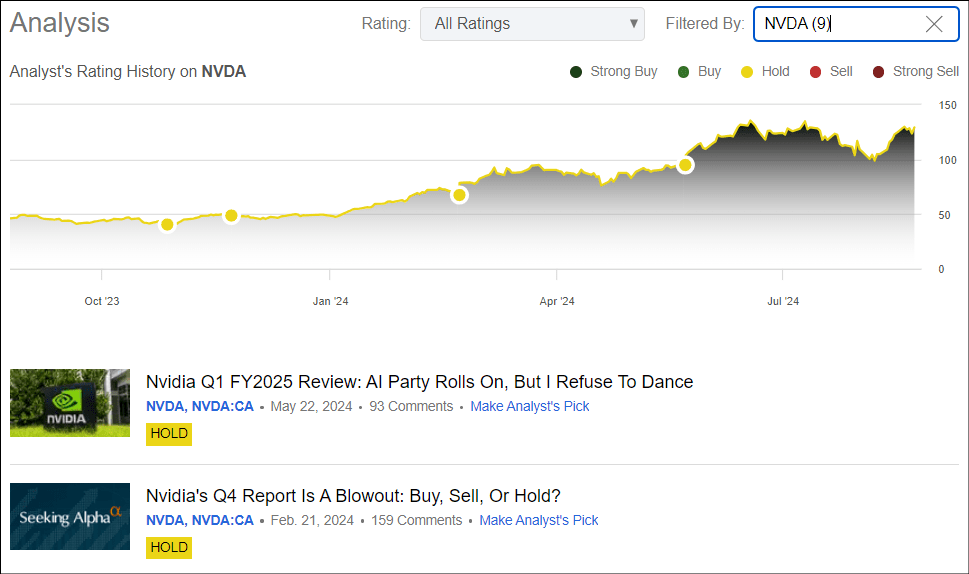

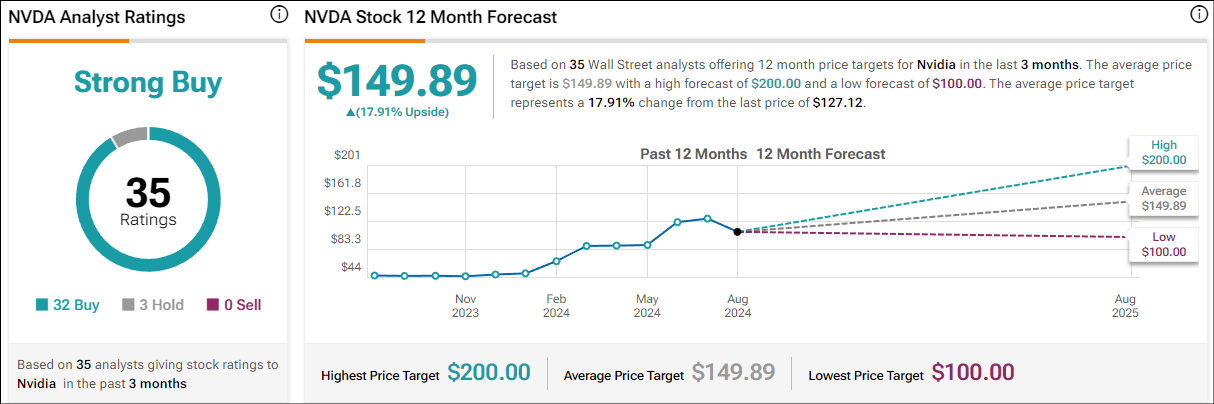

Heading into a pivotal quarterly report, Wall Street analysts remain bullish on NVDA stock, with 32 out of 35 analysts covering NVDA [nearly 92%] rating the stock as a “Buy” right now. With the remaining 3 analysts rating NVDA a “Hold,” there are no “Sell” ratings from Wall Street firms on NVDA right now.

NVDA stock forecast & price target (TipRanks)

While the 12-month price target range for NVDA stock is expansive [$100-200], the consensus estimate of ~$150 points to an upside potential of ~18% from current levels!

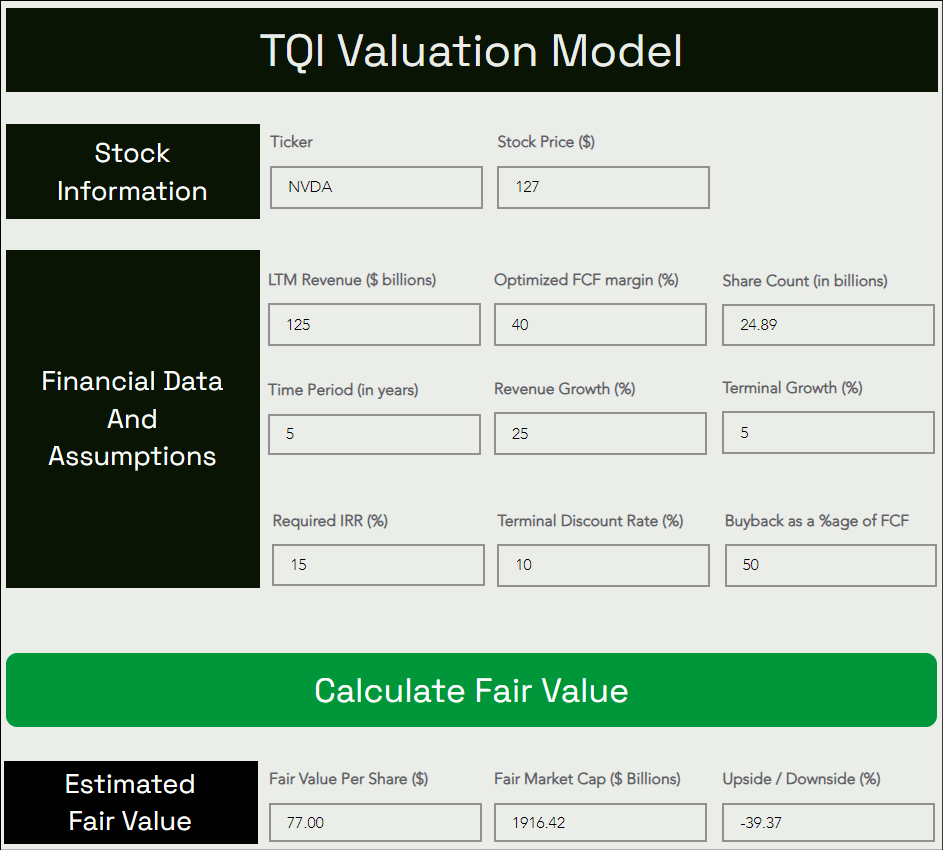

However, using generous assumptions for future growth and margins in our proprietary valuation model, we determined that NVDA stock is still overvalued at current levels. As of now, TQI’s fair value estimate for Nvidia stock stands at ~$77 per share, roughly 40% below current levels. If you would like to understand our assumptions in more detail, please check my prior report.

TQI Valuation Model (Free to use at TQIG.org)

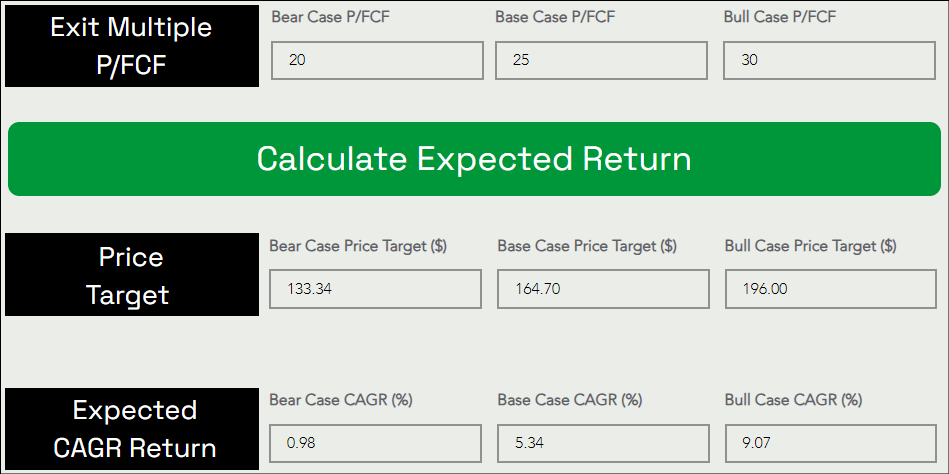

Assuming a base case P/FCF exit multiple of ~25x [ascribing a “quality” premium], we get to a 5-year price target of ~$165 per share, which implies a CAGR return of ~5.3%.

TQI Valuation Model (Free to use at TQIG.org)

With Nvidia’s base case expected CAGR falling well short of my investment hurdle rate (of 15%) and slightly lower than long-term market (S&P-500) returns (of 8%-10% per year), I do not view NVDA as an attractive investment at current levels.

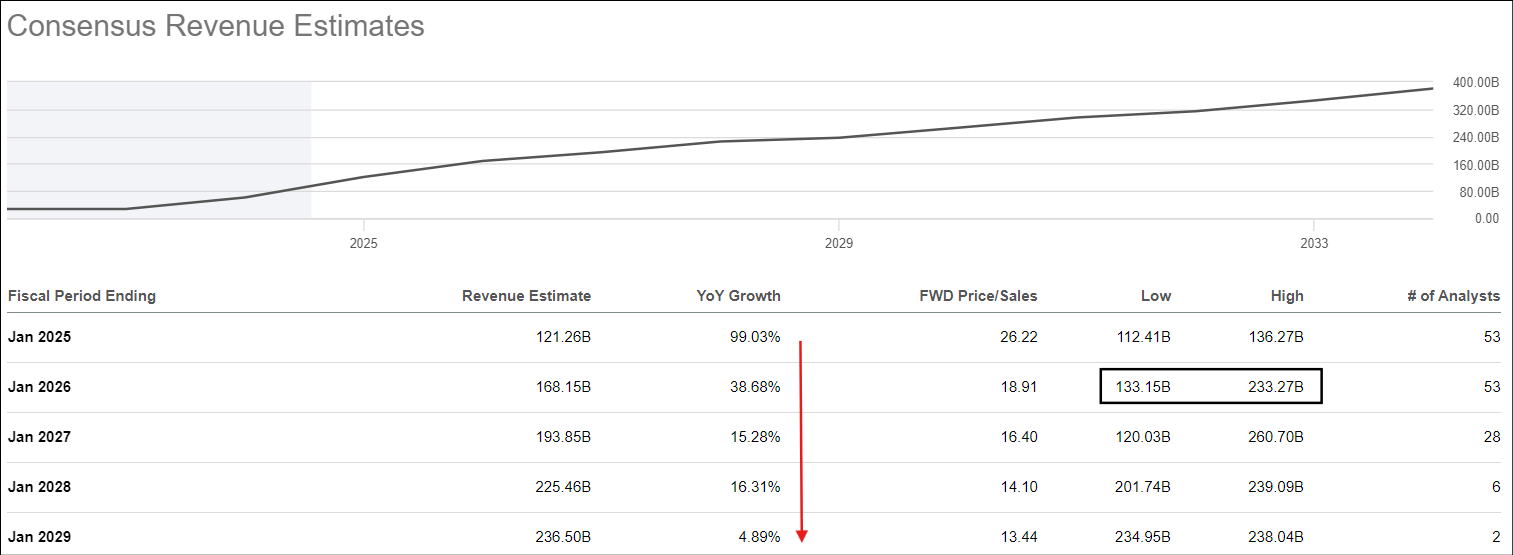

Now, some of you might consider our 5-year CAGR sales growth assumption of 25% to be overly conservative, given the range of analyst estimates for FY2026 [$133B to $233B] calls for a continuation of AI-powered hypergrowth next year as Blackwell comes to market! However, through our linear approximation, we are projecting $380B+ annual revenue in FY2029, which is well above current consensus estimates. Hence, I think underwriting even higher growth would be imprudent.

Nvidia Revenue Estimates (Seeking Alpha)

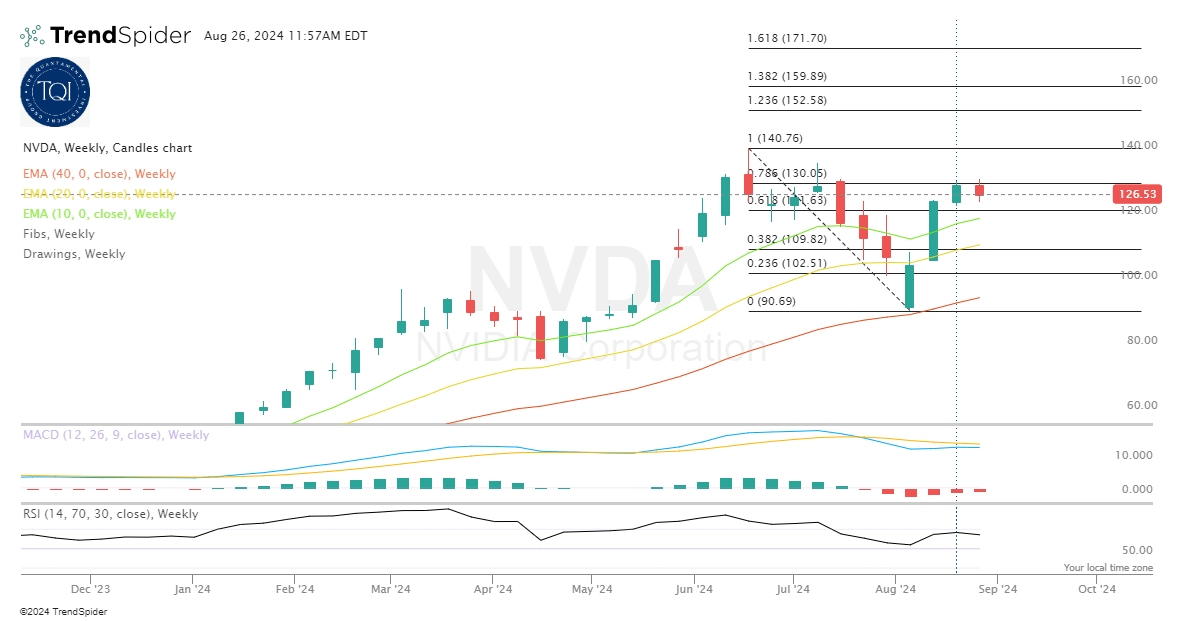

Technically, NVDA stock has regained short-term momentum ahead of earnings after re-claiming the 10-week and 20-week moving averages. However, the bounce in NVDA stock seems to be pausing at the key 78.6% Fibonacci retracement level.

If we do see NVDA making a sustained push above $130, I think the ongoing bounce can extend to $140 and then to the $152-171 range.

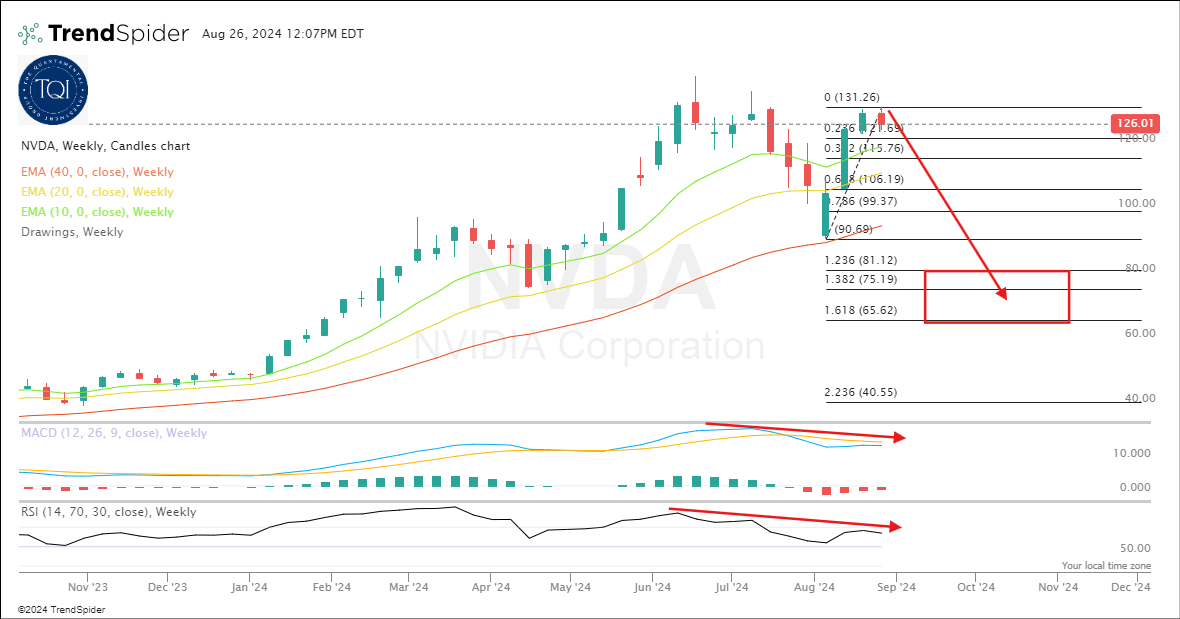

On the flip side, given the ongoing rollover in momentum indicators – Weekly RSI and MACD – selling pressure could re-appear in upcoming sessions. A strong rejection from the 78.6% Fibonacci retracement level could spark a deeper drawdown, which could send NVDA stock spiraling down to the $65-81 range marked on the chart below.

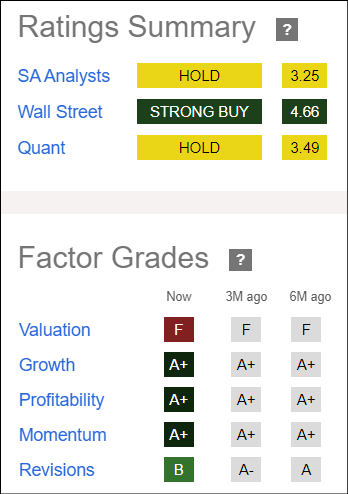

Furthermore, despite scoring an “A+” grade for “Growth”, “Profitability,” and “Momentum,” NVDA’s quant factor grades remain unsupportive for fresh buying due to its “F” grade for “Valuation” and recent deterioration in “Revisions” grade from “A to A- to B” over the past six months.

NVDA Quant Factor Grades (Seeking Alpha)

While Nvidia’s business momentum is expected to stay strong in the near term, its stock appears to be overvalued, and its technical setup looks finely balanced. Considering NVDA’s fundamental, quantitative, valuation, and technical data, I am sticking to my “Hold/Neutral” rating for Nvidia going into its Q2 FY2025 report.

Key Takeaway: I continue to rate Nvidia Corporation stock “Hold/Neutral” at ~$127 per share.

Thank you for reading, and happy investing! Please share any questions, thoughts, and/or concerns in the comments section below or DM me.

Analyst’s Disclosure:I/we have a beneficial long position in the shares of AMZN, AMD either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

We Are In An Asset Bubble, And TQI Can Help You Navigate It Profitably!

Your investing journey is unique, and so are your investment goals and risk tolerance levels. This is precisely why we designed our investing group – “The Quantamental Investor” – to help you build a robust investing operation that can fulfill (and exceed) your long-term financial goals.

At TQI, we are pursuing bold, active investing with proactive risk management to navigate this highly uncertain macroeconomic environment. Join our investing community and take control of your financial future today.