Summary:

- Palantir’s strong government contracts and expanding commercial sector presence support its long-term growth potential.

- The company’s unique data analytics platform offers a competitive edge, driving customer retention and new client acquisition.

- Continued innovation and scalability position Palantir as a compelling investment opportunity in the tech sector.

- Probably one of the stickiest business models out there right now.

hapabapa

The Palantir Investment Thesis

In March of this year, I wrote an article about Palantir Technologies Inc (NYSE:PLTR) and how the market was expecting a lot of growth from Palantir, but that they could exceed those expectations. And the ‘buy rating’ at that time has proven to be correct, as the stock has risen more than 50 percent since then.

And then as now, I hear the same arguments from the bears. They say that Palantir is trading at a P/E ratio that is way too high, that insiders are selling shares en masse, and so on and so forth. The same arguments over and over again, which is why they missed the rally. But these people forget to analyze Palantir’s competitive position, which will be the deciding factor for long-term investors.

And this is where Palantir is building on what is already a significant competitive advantage. Granted, the share price may be too high for traders with a time horizon of a few weeks, but for the long-term investor, the current share price continues to offer upside potential.

So let me explain why I think Palantir will be one of the biggest winners over the next decade.

The Microsoft And Palantir Partnership

I think most of you have heard that Microsoft Corporation (MSFT) and Palantir have teamed up to offer their expertise to the U.S. defense and intelligence communities. And I think that the experience that Palantir has in dealing with highly sensitive data is the key reason for this partnership.

Because I would imagine that in the future, the relationships that Palantir has built with governments will mean that the big players will have to work with them to get those contracts. It seems like Palantir is being trusted to handle and analyze data that other companies don’t seem to enjoy yet.

In my opinion, this trust alone is a huge competitive advantage because trust and security are very difficult things to build. They have to be earned. And when you combine that trust with Palantir’s expertise in handling the data and the actions that are taken based on the data, you have an incredibly powerful company.

What Is Palantir’s Advantage, Or Why Are They So Damn Good?

In addition to giving organizations the peace of mind that their data is safe with Palantir, Palantir’s big advantage is that it works with customers’ existing systems. Palantir calls it the Unified Namespace, which means they take data from many different sources, such as MESs, ERPs, real-time data from sensors, or databases, and connect and integrate them.

In this way, Palantir leverages data that clients already had, but didn’t use or didn’t know how to use. As a result, Palantir is highly effective at extracting the right data from highly complex systems, from multiple sources, and then aggregating, analyzing, and, ideally, generating automation.

This gives customers an overview of the entire workflow in the company and allows them to see what is happening in real time.

In addition, Palantir has so-called forward deployed engineers who focus on just one client at a time and do everything they can to get the systems up and running on day one to the client’s complete satisfaction. Because Palantir wants its customers to experience and feel value from day one.

How Palantir Improves LLM Outcomes

Most of you have probably tested some LLM’s, and maybe you have encountered the problems with them. Sometimes the LLMs hallucinate and give wrong answers. This is because the LLM is trained on a specific data set, and when it tries to give an output, it looks for the most likely answer, which is not always the right answer.

And this is where Palantir excels, helping companies solve unique problems by providing the most appropriate data in a controlled environment. Palantir has access to data that the other LLMs do not, and Palantir also wants to use a “chain of thought” to show how the LLMs arrive at their results.

Because if you know how and why an output is created, you can better evaluate it and minimize potential sources of error. One of Palantir’s strengths is making its work as transparent and simple as possible for its clients. It starts with point-and-click input that allows users to operate the systems without programming experience. And it ends with the ability to fix problems at the source with a single click because all systems are synchronized.

Palantir Leverages AI

Earlier this week, Palantir announced that they are in beta with their custom-made LM-powered AI agents. Because once the customer gives the AIP Assist agent access to the custom content, they can use AIP Assist to work with it.

Again, Palantir is constantly striving to add value to its customers, and again, these agents can be operated without any programming knowledge on the part of the user.

And in general, the focus is on the Artificial Intelligence Platform, usually referred to as Palantir AIP. But to understand the competitive advantage, we need to take a step back and focus on Foundry, which is an operating system that combines strategy and operations.

Because what a lot of people don’t know is that you can also build on top of Foundry, which makes the ecosystem bigger. Airbus SE (OTCPK:EADSF), for example, built its Skywise data platform on top of Foundry. And as more companies deploy their applications on Foundry, Palantir’s network grows stronger and larger.

But Palantir also has its own plans to serve industries with its new product, called Warp Speed. They want Warp Speed to become the modern manufacturing operating system in America. And after that, they want to conquer other industries.

Are Insiders Really Selling That Much Stock?

Yes, the insiders are selling a lot of stocks, but they have been doing so for years. For example, Alexander Karp’s first sales were in November 2020, when he sold 2.5 million and 1.2 million shares. This means that the insiders are selling all the time, and not just because the prices have gone up. Therefore, I do not believe that the selling alone indicates that the insiders think the stock is overvalued.

In addition, the insiders receive generous stock options, as can be read on the SEC website, some of which can be exercised at significantly lower prices. And just because CEOs or insiders sell does not mean that they know what the future holds, I mean, if Bill Gates had never sold a share of Microsoft, he would have been the first trillionaire. And I think most people who held on to their Microsoft shares when Bill Gates sold his have made a pretty good return on them.

What Is The Market Pricing In?

Author

Although the share price has risen sharply since my article, the market is currently pricing in a lower EPS growth rate than it did then. In March, EPS growth was priced in at 40%, now it is down to 35% p.a. as EPS has grown faster than the stock.

And of course, 35% growth still sounds incredibly high, but you have to remember that EPS has only been positive for a short time. So the growth will be faster than for an established company that has had positive EPS for a long time. And on December 23, EPS was $0.1, and now it is $0.18 TTM, which is almost double. And I expect it to be over $0.30 for the full year ’24.

Seeking Alpha

And even the analysts are expecting strong growth, although I still think the FY25 estimate is too low. But even these have been revised up, in March they were $0.33 for FY24 and $0.39 for FY25. Plus, I think for FY25, Palantir will probably crack $0.5 EPS.

And I could see Palantir hitting $1 EPS in 2026. That would mean that Palantir trades at about 35x 2026 EPS. That makes the multiple look a lot more attractive to me.

Historical Company Comparison

Seeking Alpha

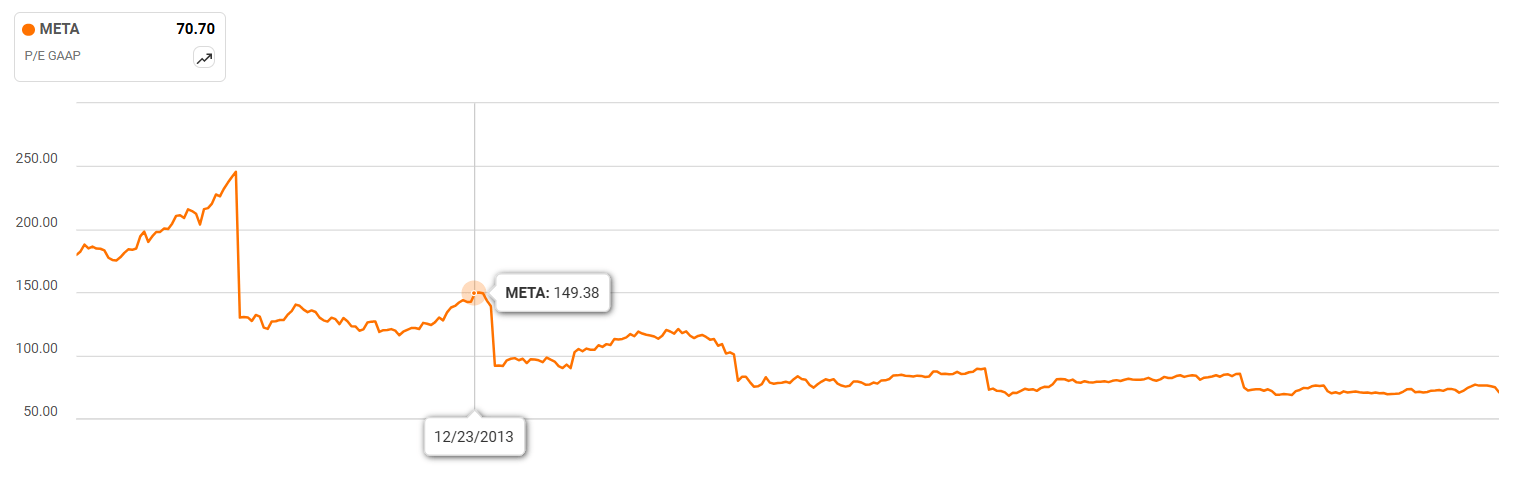

For comparison, here is the historical chart of Meta Platforms Inc. (Meta is currently my largest position). Meta’s (META) P/E was also above 200 at times in the years 2013 to 2015, and it was still a rewarding investment for anyone who bought at that time.

Very good companies are unfortunately often very expensive, but they grow into their valuation because a long-time horizon is the friend of investors who think long term and buy quality companies.

Seeking Alpha

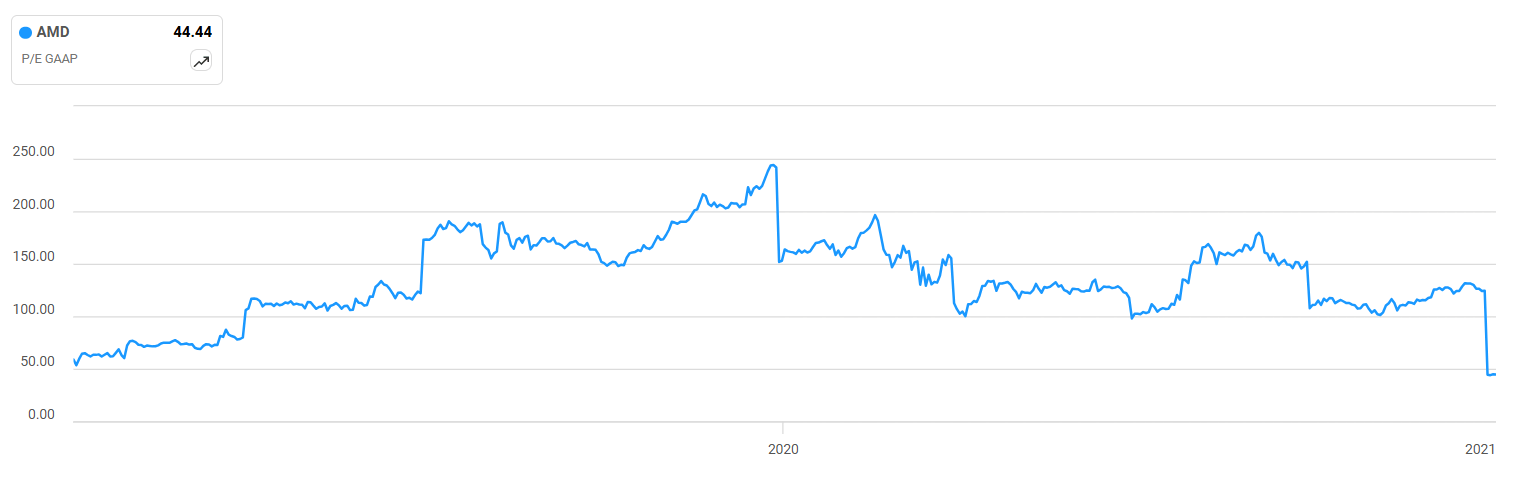

And as a second example, we have Advanced Micro Devices Inc. (AMD), another position I own, which also had a multiple of over 200 in 2019 and 2020. These companies, like Meta or AMD, were all undervalued because of their competitive position and advantages, even though they seemed too expensive to many at first glance.

And I see Palantir in the same league as them from a business perspective, which is why I think the current valuation is still undervalued for long-term investors.

Conclusion

So all in all, I think there could be pullbacks in the short term, but long term, and long term to me means 5 years+, Palantir is going to be a powerhouse. I think Palantir is going to be one of those investments that 10 years from now everyone will say it was a no-brainer and why not everyone invested in it. But as we can see now, and as we’ve seen with Amazon (AMZN) or Google (GOOGL), a lot of people can’t see the forest for the trees and recognize that this company is going to be one of the cornerstones of AI in 10 years.

Here are the reasons I am so positive about Palantir:

- Strong barriers to entry through security clearances and model development.

- The business is incredibly sticky because once Palantir is set up and customers see the value, the switching costs are huge.

- The employees are among the best in the world regarding AI, and the management team has years of proven experience.

- The business model of providing an operating system on which further applications can be built leads to enormous network effects.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of META, AMD, PLTR either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.