Summary:

- Despite positive fundamental developments such as a $38 million deal win and qualifications to do work with more sensitive government data, there are no consensus EPS estimate upgrades.

- Palantir will be joining the Nasdaq 100 index. But I think the trade opportunity for this has already played out since PLTR initially switched from a NYSE to Nasdaq listing.

- PLTR’s recent price appreciation is led more by multiple expansion than earnings growth expectations, which have remained flat.

- Relative technicals are at a key resistance level albeit without any slowdown of bullish momentum.

- Overall, I believe PLTR stock’s expectations are finally getting priced in. Missing out on a positive revenue guidance surprise in the next quarter is a key risk to my ‘Neutral/Hold’ view.

Joe Raedle

Performance Assessment

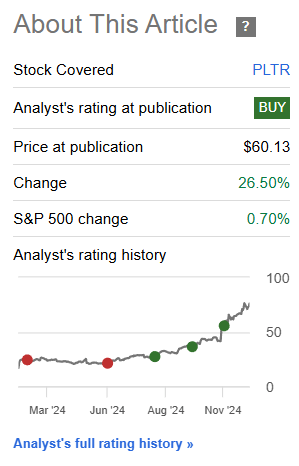

After a small period of bearishness, I turned into a Palantir (NASDAQ:PLTR) bull earlier in August this year. Since my last update on the stock, Palantir has continued its impressive run, handily outperforming the S&P 500 (SPY) (SPX) (IVV) (VOO):

Performance since Author’s Last Article on Palantir (Seeking Alpha, Author’s Last Article on Palantir)

Thesis

Recent developments have led me to believe the expectations in PLTR stock are finally getting priced in to a more full extent:

- Despite positive fundamental developments, there are no EPS estimate upgrades

- The Nasdaq inclusion trade has already played out

- Recent price appreciation is led more by multiple expansion than earnings growth

- Relative technicals are at a key resistance level but without any slowdown of bullish momentum

- Revenue guidance beats are a key upside risk

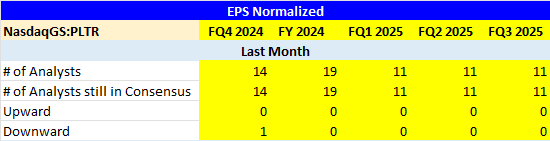

Despite positive fundamental developments, there are no EPS estimate upgrades

Over the past few weeks, Palantir has seen some positive developments. For example, it recently signed a deal worth $38.3 million of 1-year revenues with the US Special Operations Command. PLTR stock popped up 7% following the news. The momentum with Government business continued as Palantir was granted the FedRAMP High Baseline Authorization, which:

embodies the highest level of security within the FedRAMP program, meticulously designed to address the unique needs of highly sensitive and classified government data stored in cloud environments

This is significant as it proves that Palantir has won the trust and reliability to get deeper into the sensitive IT ecosystems of governments to deliver value; naturally a highly exclusive opportunity.

However, despite these instances of progress, the normalized EPS estimates for the next 4 quarters have hardly moved over the last month:

Normalized EPS Revisions by Wall St Analysts (Capital IQ, Author’s Analysis)

This indicates to me that the positive fundamentals are starting to get fully priced in.

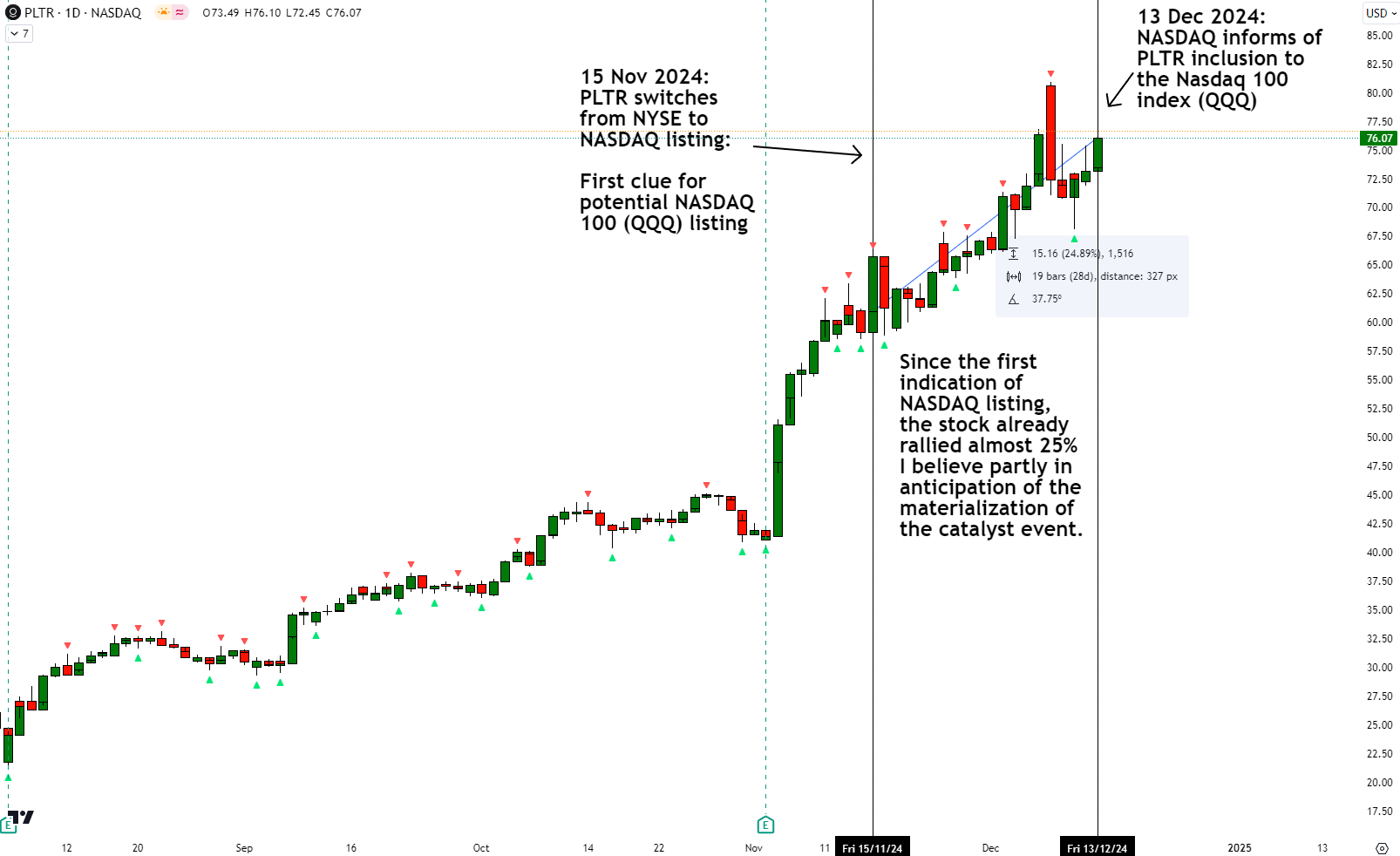

The Nasdaq inclusion trade has already played out

On 14 Nov 2024, Palantir announced that it was switching its stock exchange listing from NYSE to the Nasdaq in the hopes of meeting the criteria to make it into the coveted Nasdaq 100 (QQQ) index. Following this, I believe the market saw a Nasdaq inclusion trade theme on Palantir, fueling an almost 25% rally until 13 Dec 2024, when Nasdaq (NDAQ) announced that PLTR would be included in its flagship index:

PLTR Rally After First Sign of Potential Nasdaq Inclusion (TradingView, Author’s Analysis)

I think it is too late to bet on the Nasdaq inclusion catalyst now, since that has already materialized or been confirmed. Typically, the opportunity for alpha exists in the anticipation of a catalyst playing out; which I suspect is the case here during 15 Nov 2024 to 13 Dec 2024.

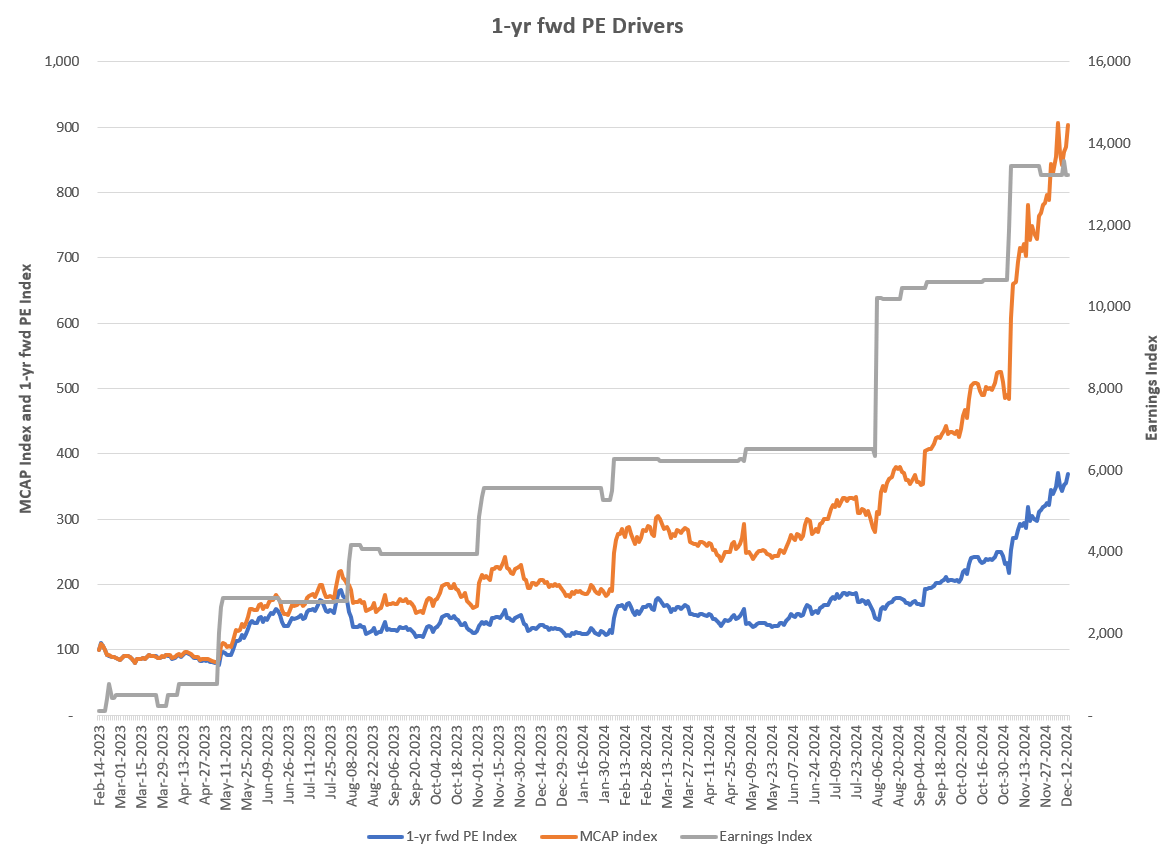

Recent price appreciation is led more by multiple expansion than earnings growth

Palantir’s market capitalization and share price appreciation (orange line) seems to be fueled primarily by an expansion in the 1-yr fwd PE multiple (steep rise in blue line) since the earnings growth index (grey line) has remained flat so far:

1-yr fwd PE Drivers (Capital IQ, Author’s Analysis)

This makes me believe the market sentiment on PLTR is chasing hype more than EPS growth, which, I believe, is more likely to be unsustainable.

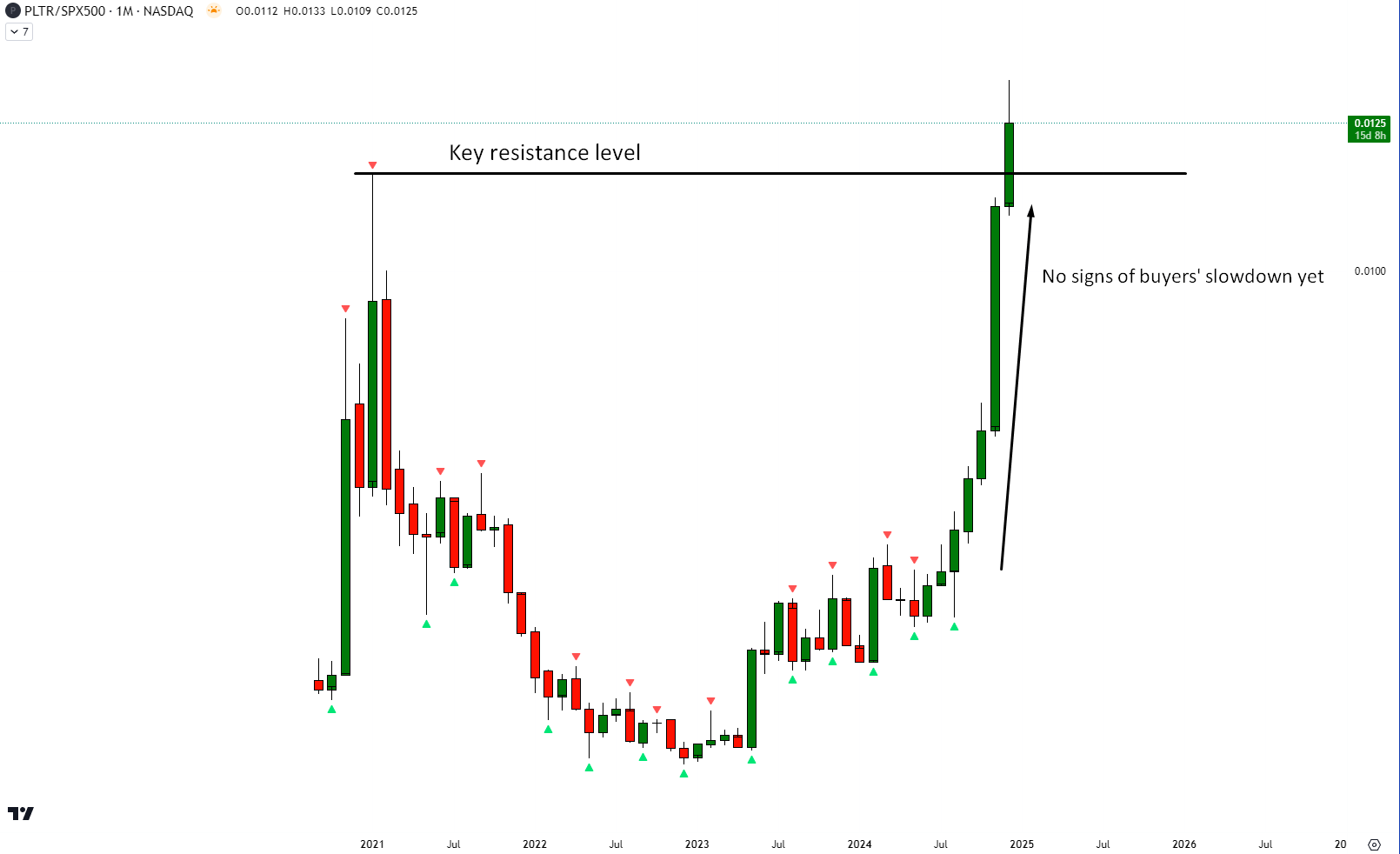

Relative technicals are at a key resistance level but without any slowdown of bullish momentum

If this is your first time reading a Hunting Alpha article using Technical Analysis, you may want to read this post, which explains how and why I read the charts the way I do. All my charts reflect total shareholder return as they are adjusted for dividends/distributions.

Relative Read of PLTR vs SPX500

PLTR vs SPX500 Technical Analysis (TradingView, Author’s Analysis)

Relative to the S&P 500, PLTR is at a key resistance level. However, there are no signs of slowdown by the buyers just yet. Still, I believe continuing fresh buys at this critical juncture is more risky.

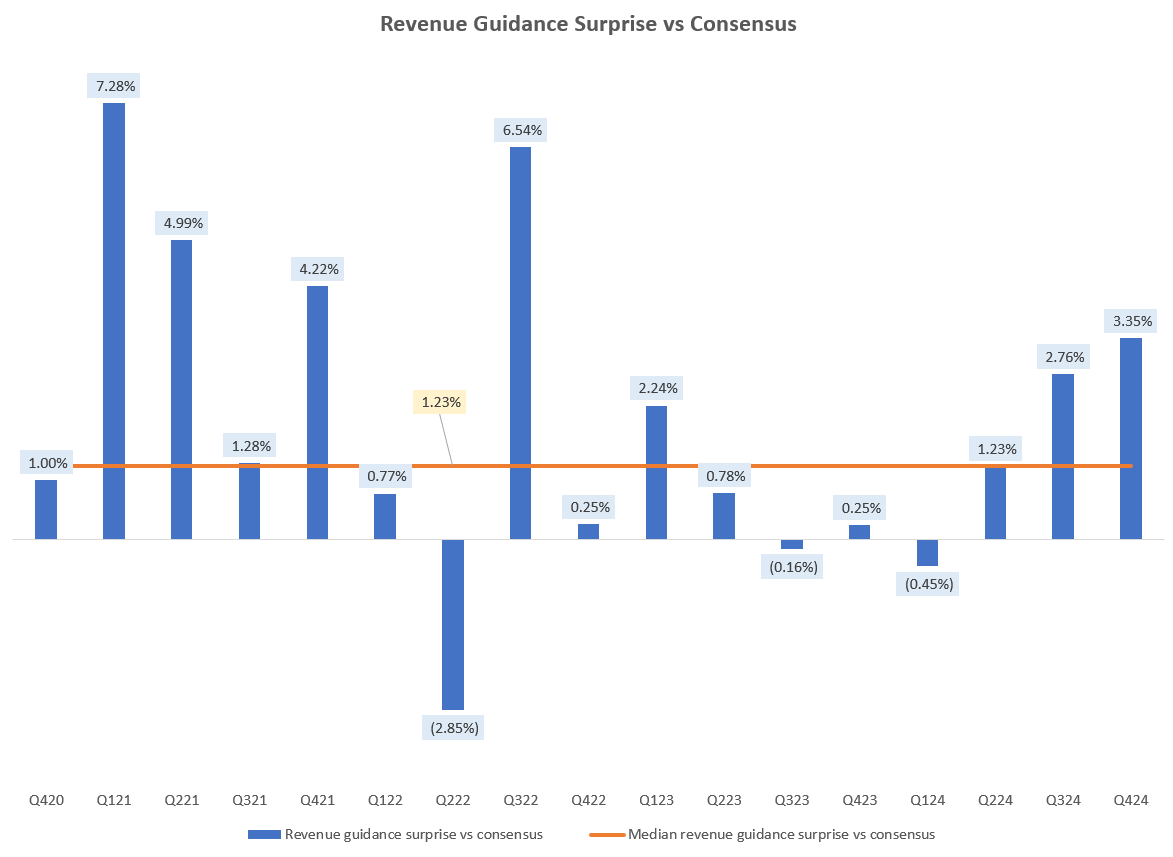

Revenue guidance beats are a key upside risk

I believe the biggest risk to my thesis that expectations are getting priced in is Palantir’s track record of positive revenue guidance beats vs consensus expectations:

Revenue Guidance Surprise vs Consensus (Capital IQ, Author’s Analysis)

Currently, PLTR’s Q1 FY25 revenue estimates stand at $796.66 million. So seeing how the Q1 FY25’s guidance pans out next quarter would be a key upside risk monitorable.

Takeaway & Positioning

My bullish views on Palantir have played out very well over the past few months. But now, I am starting to get the sense that expectations are finally starting to get fully priced into PLTR stock. This is because despite positive updates such as a massive $38 million in 1 years’ revenue deal win and progress in getting deeper into governments’ IT ecosystems, the consensus normalized EPS upgrades have barely moved an inch toward the upside over the last month. I also think the Nasdaq index inclusion catalyst has already played out, as the stock has rallied 25% since Palantir first gave investors a clue about potentially joining the Nasdaq 100 by switching its stock exchange listing from NYSE to the Nasdaq.

From a valuation drivers perspective, it is clear that the recent run-up in the stock price is driven mostly by multiple expansion, since EPS estimates have remained flat. Technically relative to the S&P 500, whilst PLTR stock is still showing strong bullish momentum, it is at a key resistance level, which increases the chances of a pause or a correction.

Hence, I am changing my stance to a ‘Neutral/Hold’. In doing so, I would have to accept the risk of a revenue guidance surprise in the next quarter, leading to a gap up reaction in the stock.

How to interpret Hunting Alpha’s ratings:

Strong Buy: Expect the company to outperform the S&P 500 on a total shareholder return basis, with higher than usual confidence. I also have a net long position in the security in my personal portfolio.

Buy: Expect the company to outperform the S&P 500 on a total shareholder return basis

Neutral/hold: Expect the company to perform in-line with the S&P 500 on a total shareholder return basis

Sell: Expect the company to underperform the S&P 500 on a total shareholder return basis

Strong Sell: Expect the company to underperform the S&P 500 on a total shareholder return basis, with higher than usual confidence

The typical time-horizon for my views is multiple quarters to more than a year. It is not set in stone. However, I will share updates on my changes in stance in a pinned comment to this article and may also publish a new article discussing the reasons for the change in view.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of VOO either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.