Summary:

- Palantir Technologies Inc.’s parabolic rise is unsustainable, with negative divergences in momentum indicators suggesting the uptrend may be nearing its end.

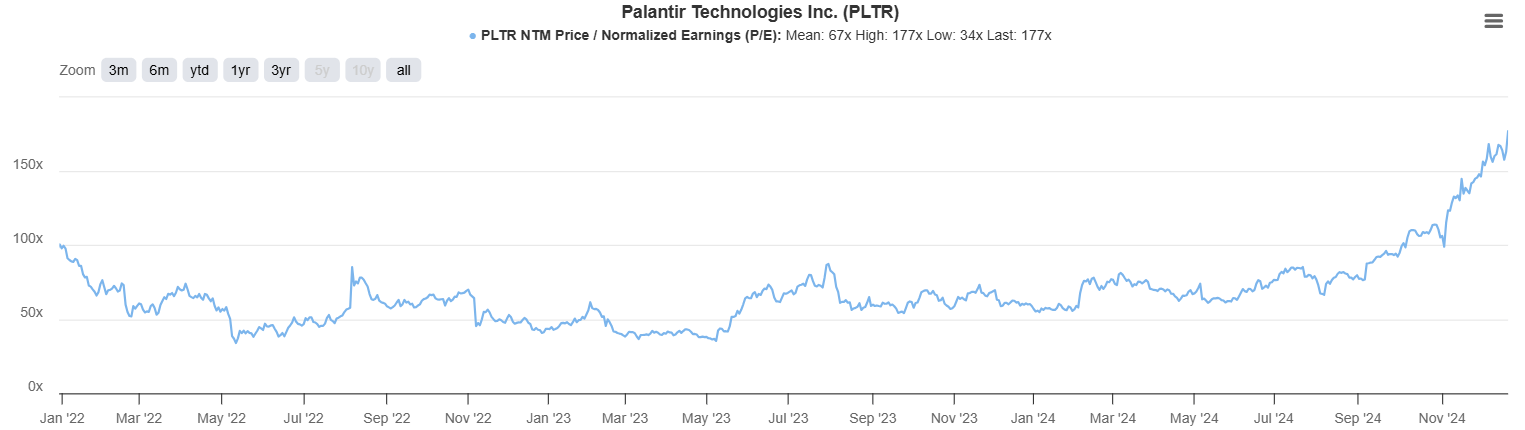

- Palantir’s valuation is extremely high at 170X forward earnings, with decelerating EPS growth not justifying the current price.

- Fundamental risks include shareholder dilution, reliance on interest income, and high operating expenses, which could hinder future earnings growth.

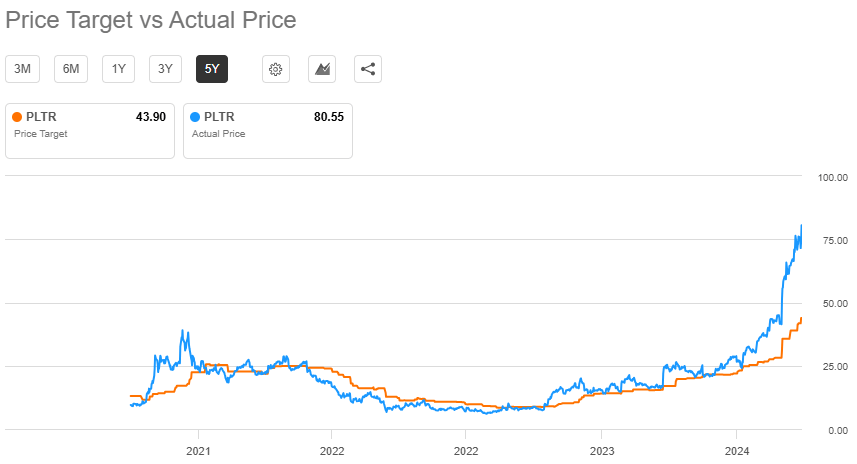

- Analysts’ average price target is 46% lower than the current price, indicating potential significant downside for PLTR.

Michael Vi

The rally that was kicked off in early November with the election results has faded for some sectors, but not for the AI trade. Advanced technology poster child Palantir Technologies Inc. (NASDAQ:PLTR) reaches unprecedented heights as we head into year-end, and I see it as so overvalued, it’s my top short idea heading into 2025.

Strength begetting strength

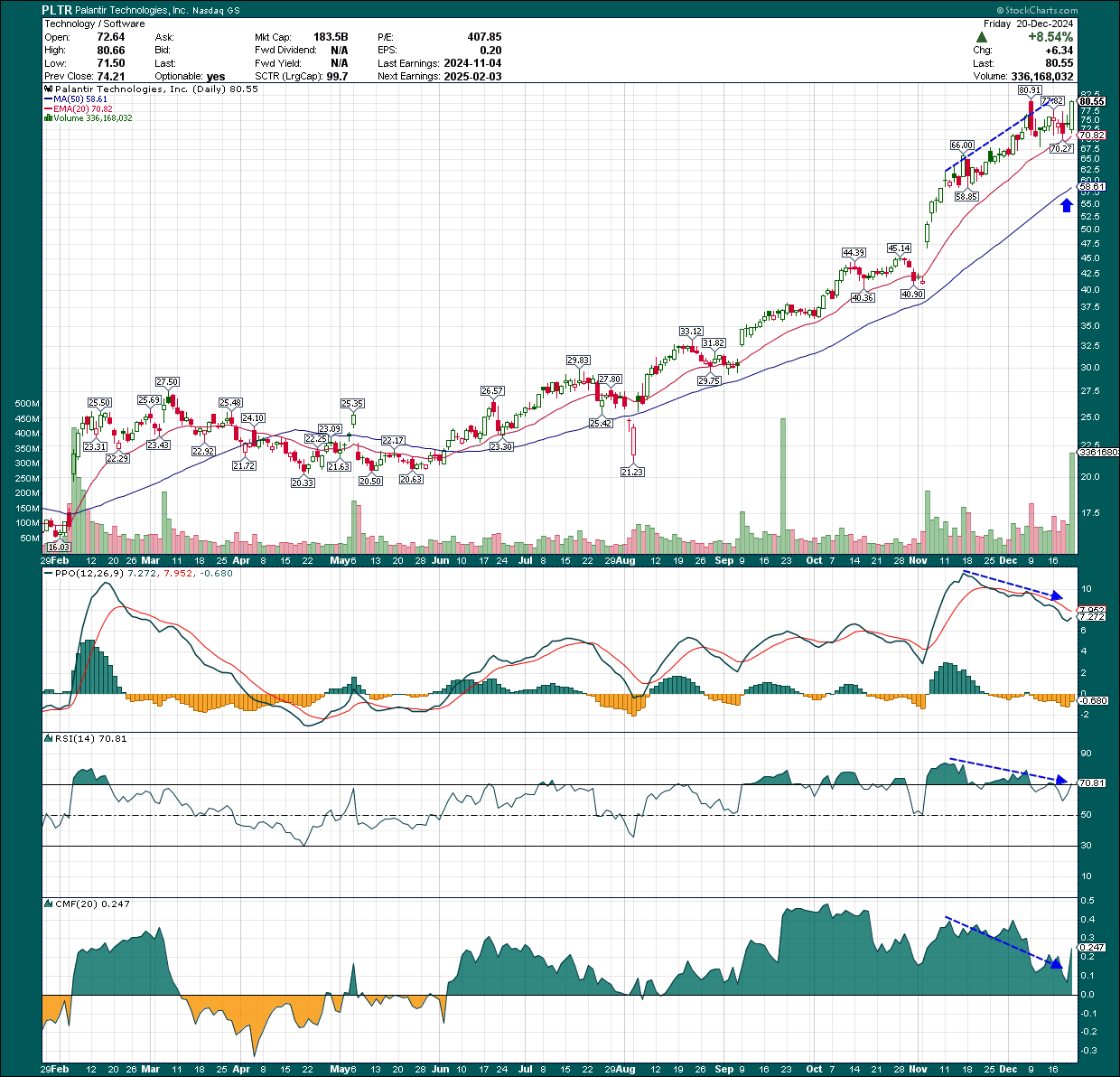

The daily chart is a thing of beauty, making higher highs constantly and no new lows in sight. The stock has doubled since early November, which, for reference, was only seven weeks ago. That kind of parabolic move is unsustainable, which adds to my bearishness. But it’s certainly not the only reason; more on that in a bit.

StockCharts

Palantir is in a classic uptrend until it isn’t, and that’s going to be evidenced by the failure of the 20-day EMA at first. That hasn’t happened, so shorting Palantir today remains extremely risky.

As with any short idea, I’m not suggesting anyone take that sort of action, as shorting carries unlimited risk. I’m simply suggesting that if you’re inclined to such things, this could be a candidate. There are other ways that are less risky, such as buying puts with defined potential losses. The method is up to each individual investor, and my focus here is on the idea rather than the specifics of the execution. Just know that shorting is tremendously risk, irrespective of the stock, and I’m not recommending anybody do that.

So why don’t I like a chart in a strong uptrend? It’s more that I think the time of this uptrend is coming near its end. The three momentum indicators – the PPO, RSI, and Chaikin Money Flow – all show glaring negative divergences. That is, price is at a new high while none of the momentum indicators are anywhere close to such moves. That can often mean bullish momentum is waning, or the relative absence of new buyers. The same thing occurs at the end of downtrends in reverse, where sellers stop showing up in the same numbers. It doesn’t guarantee us anything, but it does make it much more likely that the uptrend is reaching the end of its current move.

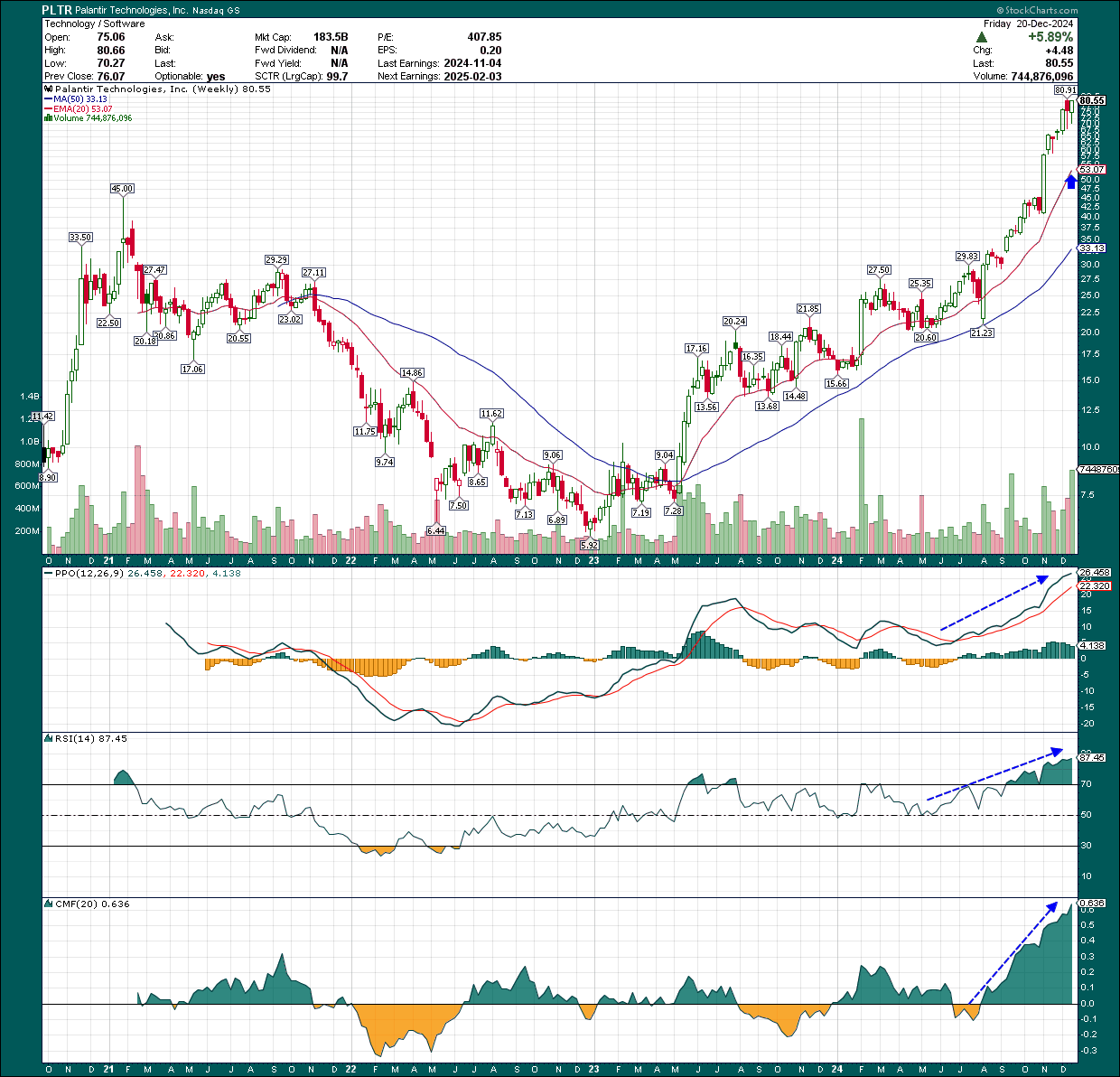

The weekly chart, to be fair, continues to just look extremely bullish.

StockCharts

The momentum indicators are showing absolutely no signs of a potential top. All continue to just go higher with price, and the only caution is the extremely overbought nature of them. That alone is no reason to take action, so this chart is not supportive of the short case. That’s a risk to my thesis, in that the longer-term outlook is quite bullish until proven otherwise.

On the daily chart, I’ve marked the 50-day SMA as a potential downside target, at least to begin with. Generally, when we get a negative divergence like we have today, a 50-day SMA test is the result. That moving average is currently just under $60, but rising quickly. It’s not that far down from current price, depending upon how long it takes to get there. On the weekly chart, I’ve marked 20-day EMA support, currently $53 but also rising rapidly.

I do not expect any selloff to just go through these levels at first. So, if we see tests of the 50-day SMA or the 20-week EMA, we should see buying ensue. Those are initial profit targets if you do decide to bet bearishly on Palantir in some way.

A move with no basis in reality

I see the parabolic move in Palantir as reason to be extremely cautious at a minimum. However, the fundamental case is one I simply cannot reconcile, and that’s why it’s a high-conviction short idea in my view.

Seeking Alpha

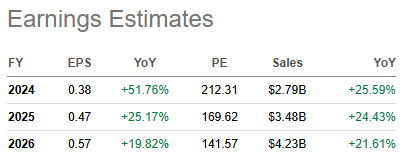

Earnings for 2025 are slated to be 47 cents per share, or an earnings yield of 0.6%. At 170X forward earnings, Palantir is difficult to describe in terms of how expensive it is. Now, if it were doubling EPS for the next few years, I could get behind such a valuation. However, it isn’t, and it’s not even close. EPS growth of 25% is good, and 20% for 2026 is strong as well. But that’s worth up to 40X or 50X earnings at a maximum, as that would be a price-to-earnings-growth ratio of ~2X. Today, Palantir’s PEG is 6.8X, and that’s simply unrealistic to expect to continue.

This is particularly true given Palantir’s growth rate for 2026 is worse than 2025. This company is not seeing accelerating earnings growth; it’s seeing quite the opposite. Why should we pay stratospheric multiples for a company with decelerating earnings growth? You can if you like; that’s not for me.

Seeking Alpha

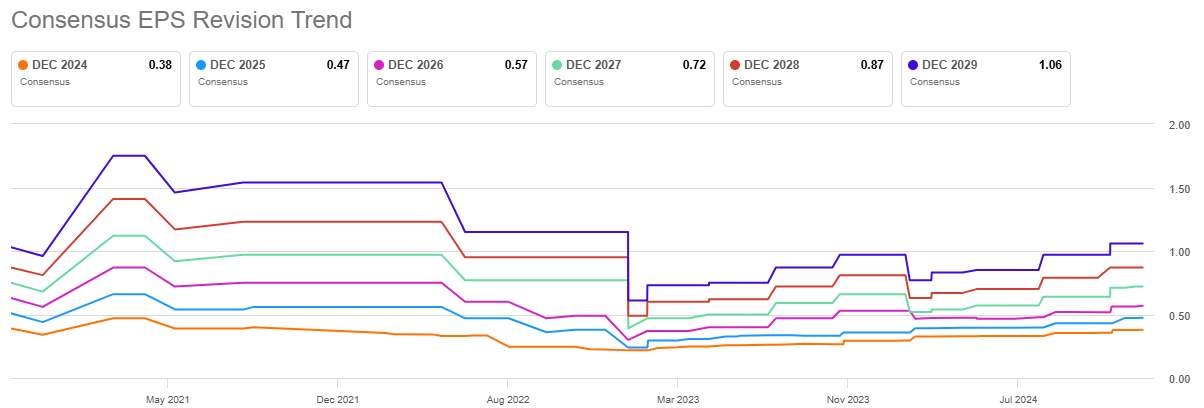

What’s worse is that while Palantir has seen recent revisions move estimates higher, they’re from trough levels. Today’s estimates are nowhere near where they were a couple of years ago. Revisions have also been small. Higher is good, but in tiny quantities, and off low levels is just not good enough for the current rally.

If we turn our attention back to the EPS estimates table, we can see that revenue is set to grow at the same rate as EPS. For 2026, it’s 22% for the top line and 20% for EPS. Now, there are three ways any company can grow EPS. First is revenue growth, second is margin expansion, and third is reducing the float. We have the top line for the next two years above, so let’s look at the other two factors.

TIKR

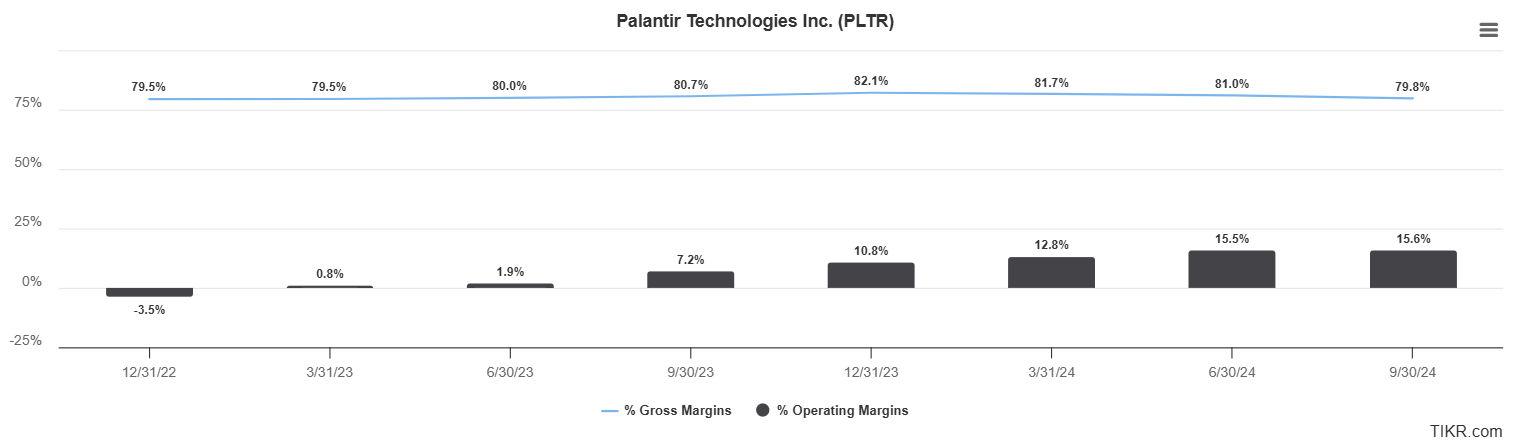

Gross margins are absolutely world-class at about 80% of revenue. That’s something just about any company in the world would envy. On the other hand, they’re not growing, so that appears to be the top. That makes operating expenses of the utmost importance, and we can see that Palantir is indeed building its operating income over time. The most recent quarter saw operating income of almost 16% of revenue, which is okay for a software stock. The idea here is that we’ll continue to see expenses leveraged down over time as revenue rises, but there’s no such evidence of that just yet.

Company website

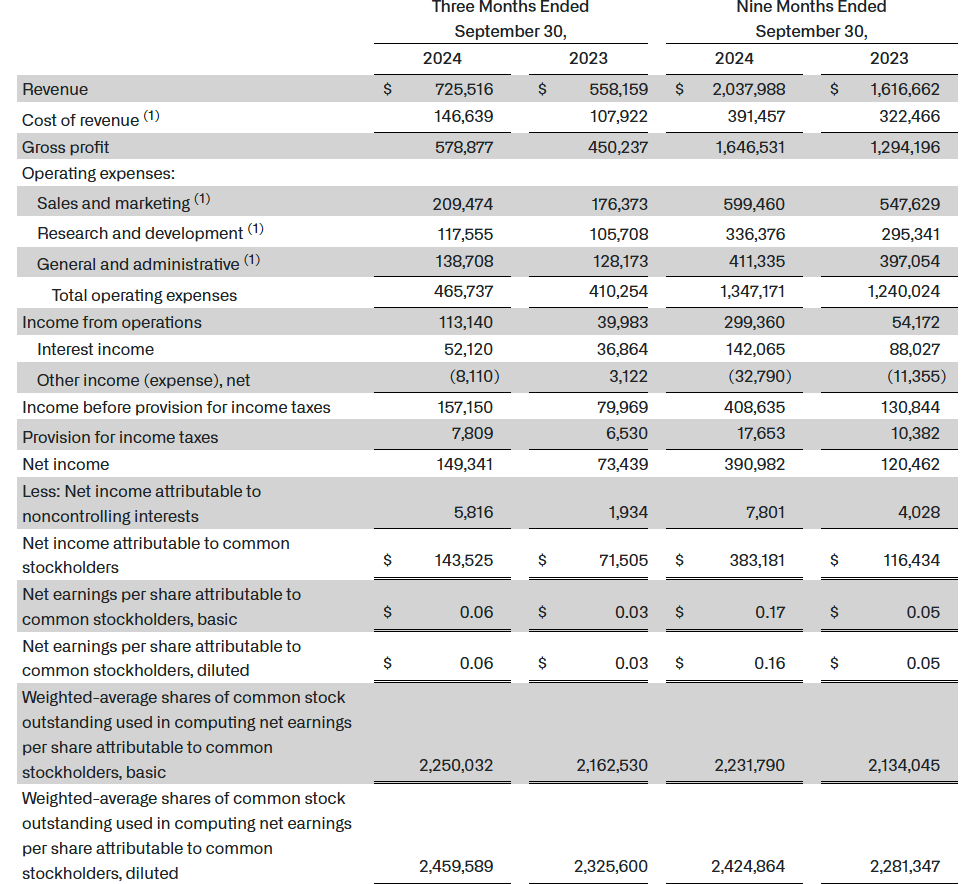

We can see that Palantir’s first three quarters of 2024 have show sales and marketing to continue to be an enormous expense, and indeed, is the single biggest line item. R&D continues to rise quickly, but that is required given that Palantir must continuously innovate or be left behind by competitors. Point being, I don’t think Palantir has any choice but to continue to spend hundreds of millions of dollars annually on sales and marketing, as well as R&D, to remain at the forefront of its industry. That doesn’t bode well for margins going forward, even accounting for forecasted revenue growth. At some point, it’s possible these line items start to shrink, but that should be many years from now, so it’s a non-factor for the moment.

The other thing that is maybe under the radar is that interest income has become an increasingly important item for Palantir’s operating income. In the first three quarters of last year, interest income was $88 million. This year, it’s been $142 million. Now, depending upon how Palantir moves this excess capital around in the coming quarters, lower market interest rates may weigh on this line item. Given its size, and the fact that it grew 61% year-over-year for the first nine months, Palantir’s EPS growth rate could be at risk simply from lower market interest rates driving less growth in interest income. In other words, interest income’s growth rate is almost certain to slow, but could actually stall entirely depending upon cash usage and generation, but also just the income rates Palantir can generate. We’ll see, but this is a meaningful risk to Palantir’s earnings growth going forward in my view, and likely not one that’s widely considered.

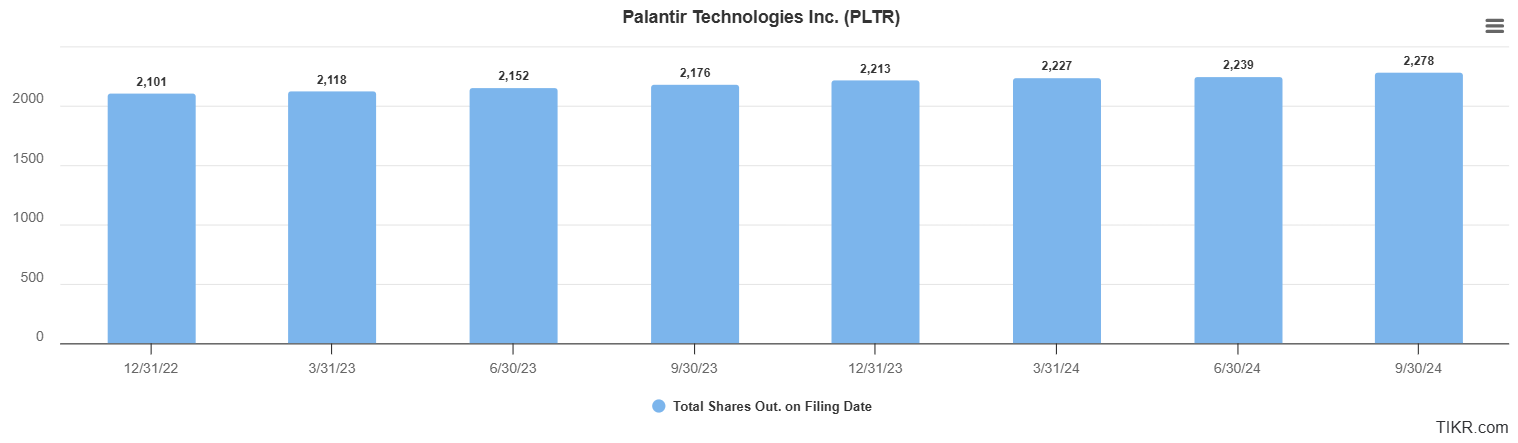

Finally, Palantir is a serial dilutor of shareholders, as we can see below.

TIKR

The company hands out stock grants as compensation as a standard way of doing business. That’s been great for those receiving the grants as shares have exploded higher, but it also means shareholders face an uphill battle with EPS as the float increases. In just the past year, the float is up 4.7%, meaning dollar earnings have to grow 4.7% just to produce the same EPS number. That’s a headwind for Palantir’s EPS until this practice changes, which is showing no signs of such at the moment.

If we take all of this into account, estimates for 2025 look like this. We have 24% sales growth forecast, an assumed 4% headwind from dilution, and 25% EPS growth forecast. The net of sales growth and dilution is +20%, which then implies ~5% earnings expansion from margin growth to get to 25% total. If I’m right that interest income growth is going to have to slow down materially in 2025 with lower market rates, that means the actual business will have to produce more operating income through lower expenses. Given the discussion we had above, I don’t see that as a high likelihood. Palantir is still very much in its expansion stage, so spending less on future investments to boost near-term margins would run counter to its strategy. If that’s the case, I think EPS targets could be at risk next year. Or, at the very least, upward revisions are likely to slow or stop.

What’s it worth, then?

That’s really the key question, and as with any stock, fair value is in the eye of the beholder. For now, let’s take a look at what analysts think.

Seeking Alpha

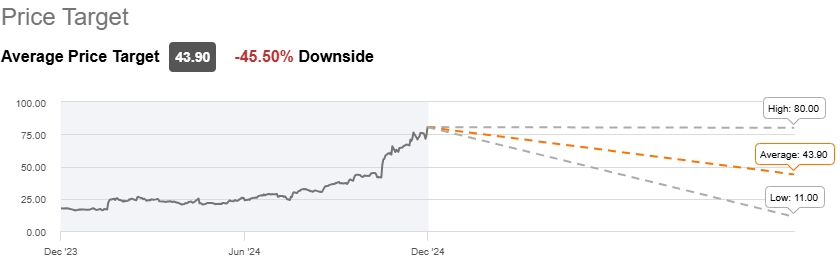

The average price target on Palantir is $44, which is 46% lower than today’s price. We know analysts don’t always get it right, and it’s possible we simply see targets rise to meet current price. However, the last time Palantir vastly overshot price targets, it didn’t end well for the bulls.

Seeking Alpha

That was back in 2020 right after Palantir went public, and the overshoot ended up with a prolonged bear market that saw the stock lose a massive amount of value in a short period. Today, the overshoot is even more egregious, so unless this time is different, I think a similar fate awaits bulls buying at the highs.

Finally, let’s take a look at the forward P/E to get a sense of the valuation picture.

TIKR

Today’s forward multiple is 177X earnings, which includes the fourth quarter of 2024, and the first three quarters of next year. By any standard, this multiple is difficult to reconcile. As I said above, on a PEG basis, even if we think current EPS growth rates will be met (which I have some doubt about), we’d be talking about a forward multiple of something like 45X at the maximum. That would see the share price back into the low-$20s, which is not on the table in terms of being reasonable right now.

So what is, then? For now, I think a test of the 20-week EMA, which is currently $53, but rising, is the first stop. That is quite reasonable, and I will be shocked if we don’t see the stock trade towards that level. Longer-term, if I’m right, and we see interest income growth stall, dilution continue, and margins not expand materially, then yes I do think something like 45X earnings is back on the table. Let us not forget that Palantir traded with such a valuation for most of 2022/2023, so it’s certainly not unprecedented.

I’m sure the bulls are laughing at me right now, but that’s fine. Markets are made up of participants on both sides, and maybe I’m wrong and this stock will just continue to go to the sky. I think the odds of that are remote, however, so Palantir is my top short idea heading into next year.

I covered the inherent risk of shorting above, so I won’t do it again here. But other risks to the short thesis include higher rates of revenue growth, as well as margin expansion that would need to come about from lower growth spending. However, I see the risk of downside as far outweighing those upside risks, so I’m sticking to my Strong Sell rating today.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, but may initiate a beneficial Short position through short-selling of the stock, or purchase of put options or similar derivatives in PLTR over the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

If you liked this idea, sign up for a no-obligation free trial of my Seeking Alpha Marketplace service, Timely Trader! I sift through various asset classes to find the best places for your capital, helping you maximize your returns. Timely Trader seeks to find winners before they become winners, and keep you out of losers. In addition, you get access to our community via chat, direct access to me, real-time price alerts, a model portfolio, and more.