Inflection investing is challenging and often involves making unpopular decisions that others may not understand.

Recommending a stock can be unpopular because it involves seeing potential others can’t.

Alex Karp selling 10% of his stake raises concerns for me; when the captain jumps ship, it often signals rough waters ahead.

At 54x forward free cash flow, Palantir is no longer undervalued, and my strategy demands I rotate capital into more favorable opportunities.

mikkelwilliam

Investment Thesis

Palantir (NYSE:PLTR) is today a crowd favorite. It has amassed an amazing army of devoted investors.

And yet, its captain has just unloaded about 10% of his holding. Does this inspire belief in the company? Or does it further nuance to what was already a highly contentious stock?

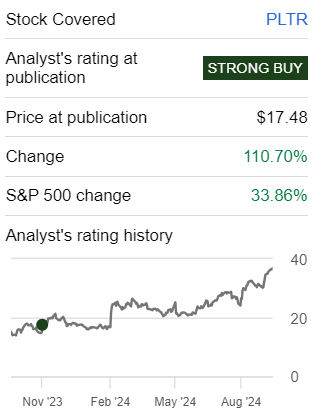

Having previously been a strong proponent of PLTR, I explain why Deep Value Returns recently sold out of PLTR, as I believed that paying more than 50x next year’s free cash flow didn’t make enough sense to me.

Rapid Recap

I recommended Palantir to subscribers of Deep Value Returns at $10 per share.

Author’s work on PLTR

I also subsequently posted this on SA, in November 2023:

For detractors of the stock, they’ll be quick to remark that stock-based compensation, or SBC, continues to be excessive. However, I don’t believe investors at this point mind. Why?

Not only is this element already priced in, but the fact that Palantir is already GAAP profitable largely does away with this bearish concern.

Altogether, I continue to declare that I believe this is a good time to buy Palantir, as the stock continues to demonstrate clear end-customer diversification as well as meaningful growth opportunities.

Author’s work on PLTR

Allow me to explain, Inflection investing is a lonely road. You are always making unpopular decisions.

You are unpopular when you recommend the stock because you see what others can’t. You are unpopular when you sell the stock because you can’t see what others do.

The return is made in the middle because hero investors end up as zero investors.

The moment I recommended PLTR, it fell from $10 to $7 per share. Naturally, my timing sucked. It was such an unpopular recommendation!

In time the stock moved higher and higher, but its path was so volatile, that it ensured that nearly nobody would have held on to PLTR. Indeed, I recognize that the majority of investors only invest with stop losses, and since PLTR was so volatile, I do not believe that anyone managed to make even 50% of what I made here.

But this makes sense, investing is difficult. Here’s the thing, inflection investing succeeds best when I’m making unpopular decisions.

Latest Development; Captain Starts To Sail Off

SA reports there’s a 10 million block sale by an unnamed person. Meanwhile, from my understanding, I can only see 9 million shares being sold from Alex Karp and a substantially smaller figure from Lauren Friedman.

Not quite sure where that 1 million shares came from that SA reports, but I don’t believe that matters all that much at this point, for our discussion.

Meanwhile, in the interest of balance, I want to remark something that many investors will have forgotten.

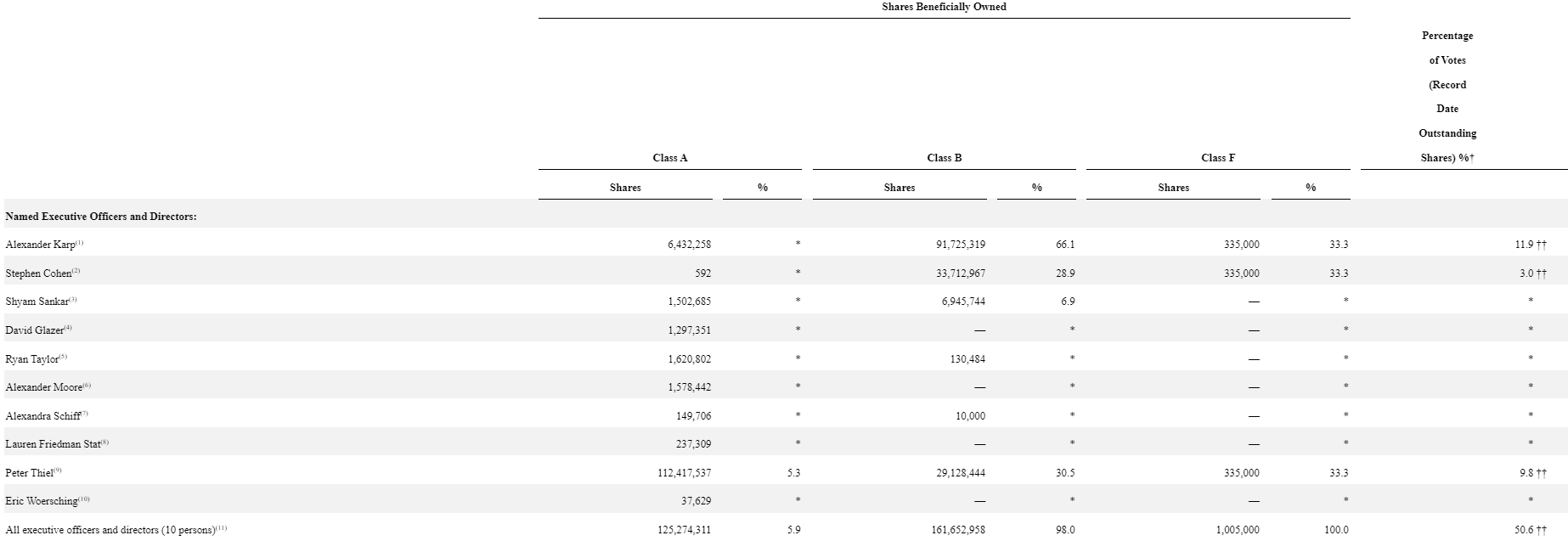

If you zoom in on the table below, you’ll see that Alex Karp has somewhere around 90 million shares. Hence, this sale is for around 10% of his holding.

SEC filing; proxy statement

Consequently, I wouldn’t be too quick to read into the headlines that everything has changed from management’s perspective, despite a couple of insiders selling out of PLTR.

Nevertheless, I wish to explain why I sold my ownership of PLTR.

Why I Sold Palantir

Palantir’s Q2 2024 did not increase its free cash flow guidance beyond the midpoint of $900 million. However, given that its topline is now expected to increase so significantly compared with its earlier guidance, I now believe it makes more sense to embrace Palantir’s high end of its free cash flow guidance. Hence, we should expect approximately $1 billion of free cash flow from Palantir in 2024.

Moreover, as we look out to 2025, given Palantir’s increased scale, together with its strong growth rates, I believe that Palantir’s free cash flow could reach $1.5 billion in 2025.

This means that Palantir is being priced at approximately 54x next year’s free cash flow. This doesn’t strike me as all that expensive, for what it offers. Indeed, I could quite easily make the argument that there’s still more upside potential here.

But at the same time, I don’t want to be complacent. I know that the market is brutal. And it’s very important to stick with my inflection investing strategy. As such, you can never rest on your laurels. You have to always be moving capital around, keeping only names that are extremely undervalued in the portfolio.

For those interested, I deployed my capital into Peloton (PTON). And you may contend that PTON has nothing in common with the almighty PLTR. Did I simply misspell PLTR? Jesting aside, I believe that Palantir’s risk-reward isn’t all that compelling right now.

Yes, it’s not completely shocking to pay 54x forward free cash flow for Palantir. I continue to believe that its prospects are very interesting over the long term. But as an Inflection investor, I must always be thinking about investing as a game of odds. Of risk versus reward. Am I being sufficiently compensated for the potential reward? And I don’t believe I am.

The Bottom Line

As an inflection investor, my strategy revolves around making difficult, often contrarian, decisions at key moments of change in a company’s narrative.

I make moves when others are either overly enthusiastic or too pessimistic, always seeking value where it is hidden.

Palantir has been an exciting journey, but the fact that its CEO, Alex Karp, sold 10% of his stake should raise questions from its shareholders.

While some might view this sale as insignificant, it signals to me that even the captain may not be fully confident in the ship’s future course. Combined with the high valuation and the uncertainties ahead, this diminishes the investment’s appeal.

In investing, it’s important to know when to hold ’em and when to fold ’em – and right now, the odds for Palantir just aren’t stacked in my favor. In short, I’d rather be ahead of the curve than left behind on a sinking ship!

Analyst’s Disclosure:I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Strong Investment Potential

My Marketplace highlights a portfolio of undervalued investment opportunities – stocks with rapid growth potential, driven by top quality management, while these stocks are cheaply valued.

I follow countless companies and select for you the most attractive investments. I do all the work of picking the most attractive stocks.

Investing Made EASY

As an experienced professional, I highlight the best stocks to grow your savings: stocks that deliver strong gains.

Deep Value Returns’ Marketplace continues to rapidly grow.