Summary:

- Palantir is a polarizing stock, with value investors deeming it overpriced and many growth investors believing its growth potential isn’t fully priced in.

- I recognize the possibility of me underestimating Palantir’s future earnings potential, but I believe too much growth is priced into Palantir stock for easy gains, making it very risky.

- Stock-based compensation continues to be a drag when assessing the company’s financial metrics and valuation.

- The recent gains from the S&P 500 inclusion highlight the hype around the stock.

Michael Vi

Palantir (NYSE:PLTR) is an extremely divisive stock, with plenty of value investors saying it’s overpriced and some growth investors saying that not enough growth is priced in. I’m taking the first side. I think this data analytics and software stock has gotten a bit ahead of itself for now and that there’s some hype involved, especially with the recent S&P 500 inclusion. Plus, I’m not a fan of the company’s high SBC (stock-based compensation) and its “adjusted” financial metrics, which add back SBC to make the numbers look better.

Nonetheless, Palantir has proven that it’s a great company with a competitive advantage, and I will talk about some of its positive metrics below. But it’s the high valuation that makes me have to give the stock a Hold rating.

S&P 500 Inclusion Reaction Proves That PLTR Stock Carries Lots Of Hype

Yesterday (September 9), news came out that Palantir will join the S&P 500. Of course, this is good news for the stock, as an inclusion in the index will force index funds to buy it, and it will increase the stock’s liquidity as well.

Here’s where the hype can be somewhat quantified, though. Palantir wasn’t the only stock that received that news this week. Dell Technologies (DELL) and Erie Indemnity (ERIE) are also set to join the S&P 500. However, DELL and ERIE finished 3.8% higher and 0.6% lower, respectively, after the announcement, while PLTR stock gained over 14%. And it’s not as if this was some sort of huge short squeeze. Palantir only had 3% of its float sold short, as of August 15. So, in my opinion, this just shows the difference in hype level between the stocks.

What Makes Palantir So Special?

Palantir is a data analytics and software firm that helps organizations customers interpret/use massive amounts of data. Its services are highly customizable, meaning that they can meet very specific customer needs, which creates loyal customers and product stickiness, and, in turn, a high gross profit margin and solid growth. After all, if a company creates a highly customized, advanced solution for you and you end up incorporating it into your company, it would be a pain to then abandon the solution for a new one, and this would come with high switching costs.

Here’s a quick example. BP p.l.c. (BP) uses a digital twin of its oil production operations to monitor and optimize its operations. Notably, BP has been a customer since 2014, and just yesterday, it “entered a five-year strategic collaboration to introduce new artificial intelligence capabilities with Palantir’s AIP software.”

Loyal customers are a sign of a good product, and you can quantify that based on Palantir’s net dollar retention rate of 114% for Q2.

In the company’s Q2 earnings call, Palantir’s CFO, Dave Glazer, stated the following:

“Net dollar retention was 114%, an increase of 300 basis points from last quarter. The increase was driven both by expansions at existing customers and new customers acquired in Q2 of last year. As net dollar retention does not include revenue from new customers that were acquired in the past 12 months, it does not yet fully capture the acceleration in velocity in our US commercial business over the past year.”

This means that Palantir’s existing customers are not only remaining as clients but are also spending 14% more year-over-year. And the 114% figure excludes revenue from new customers, so it’s entirely driven by existing clients increasing their spending.

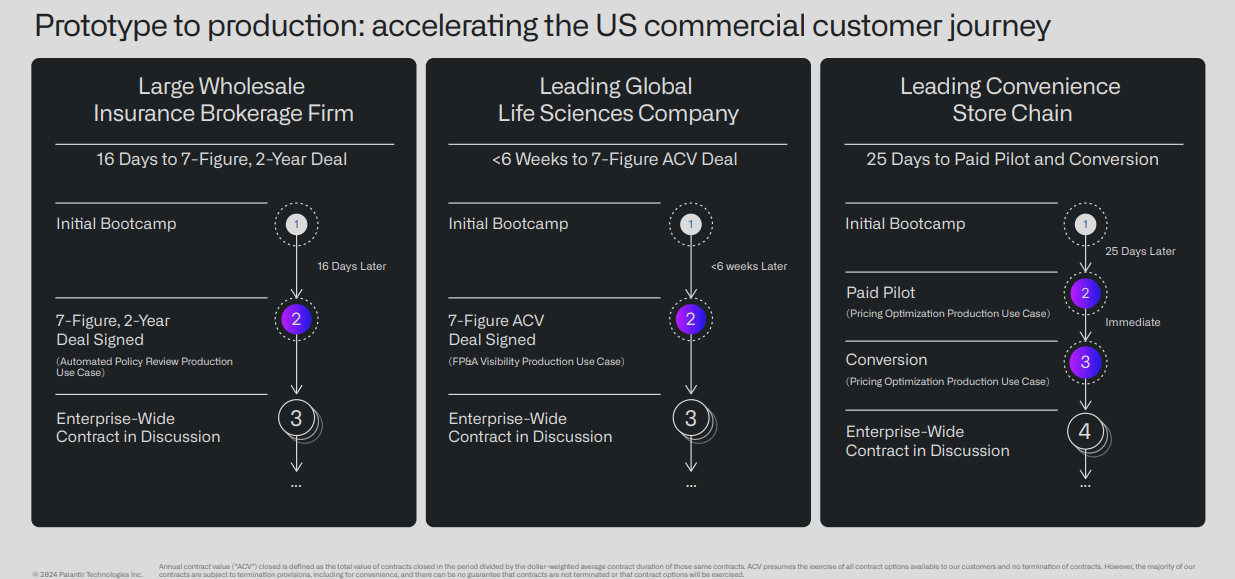

The Customer Acquisition Strategy Is Working Very Well

Palantir offers AIP, which stands for Artificial Intelligence Platform. This is Palantir’s AI-driven software platform that allows organizations to use advanced large language models (LLMs) and other AI tools for real-time data analysis and decision-making. From the videos I’ve seen, it seems like a super customized ChatGPT (along with the other AI tools) on steroids that’s integrated with your business.

For AIP, it offers free AIP Bootcamps. These Bootcamps are hands-on training sessions that quickly help clients understand and implement AIP.

Once customers see the value in these free bootcamps, they sign deals with Palantir. You can see some examples below.

Palantir Customer Acquisition Examples (Palantir’s Investor Presentation)

Growth Is Strong As A Result

Due to the high importance and quality of its product, Palantir has seen exceptional growth in the past few years, with a 3-year revenue CAGR of 23.1%. Further, revenue growth is expected to come in at 24% for Fiscal 2024 and 20.7% for Fiscal 2025. Notably, its GAAP net income grew from $28.1 million in Q2 2023 to $134.1 million in Q2 2024.

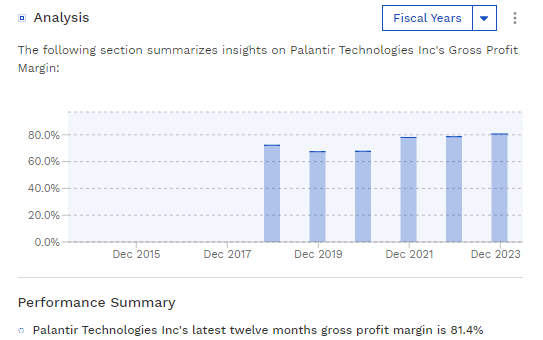

Rising Gross Profit Margin Indicates A Competitive Advantage

Aside from qualitative factors, the company’s rising gross profit margin suggests that it has a competitive advantage, as it means that competitors aren’t eroding its profitability. Palantir’s gross margin went from 72.2% in Fiscal 2018 to 81.4% for the past 12 months.

Palantir’s Gross Profit Margin (Finbox)

Some Financial Metrics I Don’t Like

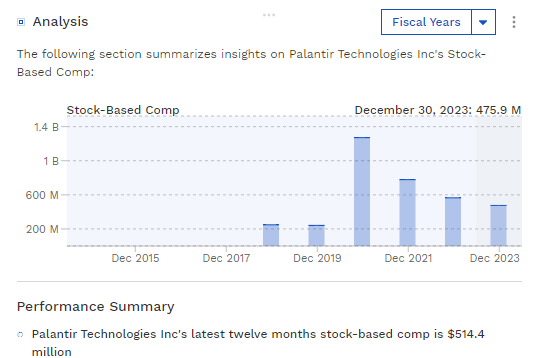

Although Palantir is solid overall, there are some things I don’t like, including its high stock-based compensation and adjusted financial metrics.

For the last 12 months, SBC comes in at $514.4 million. This is a large chunk of its $696.4 million in TTM free cash flow (and I’m not talking about its adjusted free cash flow).

Palantir’s Stock-Based Compensation (Finbox)

I, and many other value investors, view SBC as a real expense. Sure, it’s technically not a cash expense, but it dilutes shareholders, and it’s a way of paying employees. If the company didn’t use SBC, it would likely have to pay more in salaries to retain talent, which is then a cash outflow. Thus, many people treat SBC in the same way and subtract it from free cash flow to get a more conservative figure.

If you do the math, you’ll see that its FCF minus SBC comes out to $182 million. Another interesting thing to point out is that its TTM interest income on its $4 billion cash pile is $171.4 million. Therefore, most of that $182 million figure is from interest income rather than the firm’s operations.

However, it’s not all bad, as SBC as a percentage of FCF has certainly come down in the past few years (~74% for the past 12 months compared to 242% in Fiscal 2021). It looks like that trend is set to continue, especially since FCF is expected to surge to $881.27 million for the full year, per analyst estimates found on simplywall.st. So this is something that I’ll monitor going forward.

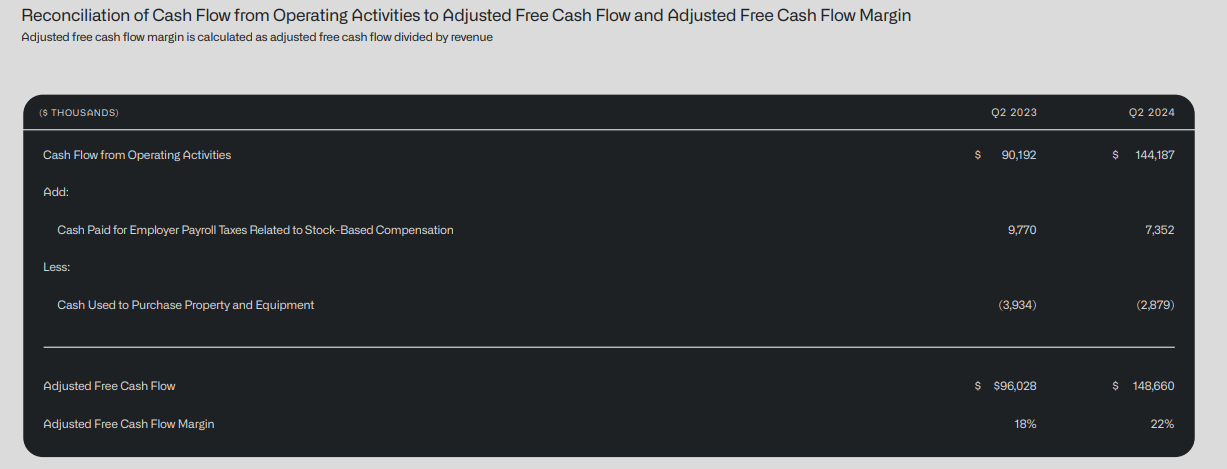

Now, back to what I don’t like. Below, you can see that Palantir reports adjusted free cash flow, which actually adds $7.35 million in “Cash Paid for Employer Payroll Taxes Related to Stock-Based Compensation” to the figure to boost it. Although it’s not a large amount, the fact that the company is adding back a recurring cash expense to its adjusted free cash flow gives me pause.

Palantir’s Adjusted FCF (Palantir’s Investor Presentation)

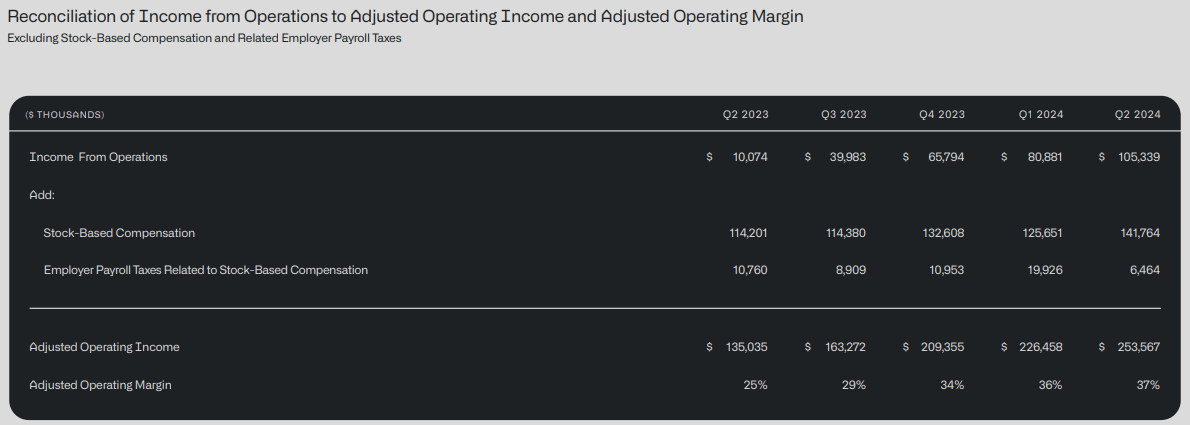

You can also see the difference in adjusted operating income for Q2 2024 ($253.57 million) compared to regular operating income ($105.34 million). The reason I bring up these metrics is because, again, SBC is a real expense, and my hope is that investors will take a closer look at Palantir’s unadjusted earnings and financial metrics before making investment decisions.

Palantir’s Adjusted Operating Income (Palantir’s Investor Presentation)

The Valuation Prices In Lots of Growth

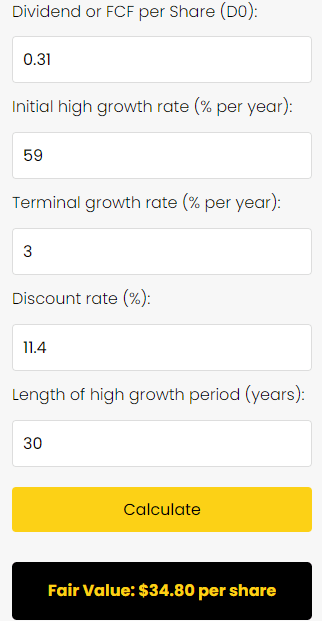

Now, let’s talk about PLTR stock’s valuation, which seems high to me. For the valuation, I’ve used an H-Model valuation calculator that I created. I actually reverse engineered the inputs to see how high of a FCF growth rate Palantir would have to experience in order to justify its current share price of around $34.80. So just to be clear, the fair value calculation from the calculator below is not my estimate of fair value.

Allow me to explain how it works (although you can find a more in-depth explanation here). The H-Model starts with FCF/share, which is $0.31, per Finbox. Then, I need a high growth rate for FCF/share. This is the growth rate that will be seen in the first year (I put 59%). I then input how long I think the high growth period will last. I put 30 years because Palantir has many years of growth ahead.

The model assumes a linear decline in the growth rate, which will gradually drop from 59% to a terminal growth rate of 3% by year 31. The 3% terminal growth rate reflects Palantir’s perpetual growth potential once it matures. I chose 3% because it’s a reasonable growth rate after maturity based on long-term GDP growth. Generally, I use 2.5%, but I use 3% for companies with better growth prospects.

Regarding the discount rate, I used 11.4%, which was calculated by Finbox using the CAPM model.

For the PLTR example below, FCF growth would be 59% in year 1, 57.13% in year 2, ~55.27% in year 3, 53.4% in year 4, and steadily downward in this fashion until it reaches exactly 3% in year 31. After that, the growth rate will be 3% per year in perpetuity.

In short, that’s the type of growth it would take PLTR stock to justify its current valuation, as you can see below. For me, that’s just a bit too optimistic to want to buy the stock. Let’s also not forget that the valuation uses FCF per share, and per-share metrics will be negatively affected by the high stock-based compensation.

Palantir H-Model Valuation (Author)

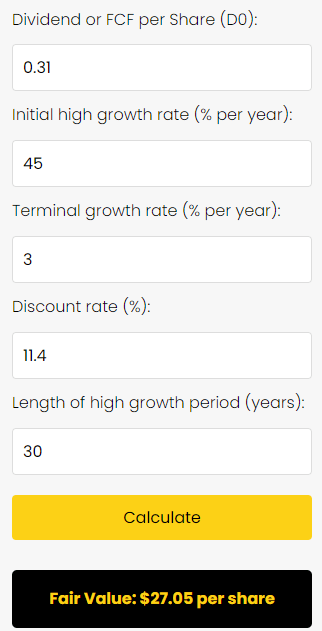

The valuation is obviously very sensitive to the growth rate. If I just change the high growth rate to 45%, which is still very high, the fair value drops to $27.05 per share. This highlights the limited margin of safety in the stock’s valuation.

Palantir H-Model Valuation (Author)

The Risk In My Thesis: I Could Be Underestimating Palantir’s Growth Potential

This week, Bank of America (BAC) analyst Ronald Epstein raised his price target on PLTR stock to $50 from a previous target of $30. The analyst made an important point.

He stated the following:

“In 1980, AT&T hired a consultancy company to estimate the market size for cell phones by 2000. The study suggested there would only be 900k users. The actual number of mobile subscriptions in 2000 was over 100 million. These early estimates also failed to anticipate the world of apps, streaming, smart devices, and ultimately, how this new product would bring forward the first public trillion-dollar company.

We view Palantir’s (PLTR) capabilities, technology and path forward facing a similar fundamental misunderstanding. The upcoming S&P 500 inclusion provides a watershed moment for institutional investors to revisit what they ‘know’ about PLTR. We reiterate our Buy rating and raise our PO to $50.”

Therefore, if Palantir is truly in a similar situation as the one mentioned from 1980 and analysts are underestimating its growth potential, then it can truly be undervalued. I’m just not willing to bet on that at the moment.

The Takeaway

Palantir is an excellent company with a great product and customer acquisition strategy. The highly specialized services it offers create a competitive advantage via high switching costs. This competitive advantage and customer loyalty can be quantified by looking at the firm’s rising gross profit margin, 114% net dollar retention rate, and consistent growth while improving profitability.

Nonetheless, as shown above, the current valuation is pricing in lots of growth. I’m not saying there’s a 0% chance that the high-growth rate will be reached, and the Bank of America analyst certainly made a good point that the market can be underestimating its growth potential. However, I just find it too risky to bet on a company with such high expectations already baked in.

Plus, I’m not a fan of the high stock-based compensation, which will negatively impact per-share growth and leaves the company with a relatively low amount of what I call “true” cash flow. Lastly, I believe that investors should consider looking at the company’s unadjusted metrics when analyzing the stock, as they paint a different picture of the company’s profitability.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.