Summary:

- In our opinion, Palantir is extremely overvalued at the current price.

- Our valuation model shows that the downside could be nearly 50%.

- We believe that Palantir is a STRONG SELL right now.

nhill

After we released our update on Palantir (NYSE:PLTR) last month, the company published its earnings report for Q2 in which it reported a major boost in sales and increased the guidance. This has led to the growth of Palantir’s stock, which is now over 10% up since our update was released in July. While our bearish thesis hasn’t played out yet, we continue to believe that the company’s stock trades at irrational levels and represents a significant downside.

The Good, The Bad, and the Ugly

Our recent bearish idea hasn’t materialized yet since Palantir’s share price has grown by over 10% thanks to the positive earnings report which showed that the company’s revenues in Q2 increased by 27.2% Y/Y to $678.13 million, above the expectations by $25.71 million. The increased guidance by the management has also reignited investors’ confidence.

However, we still believe that the company’s growth will slow down, which could prompt the share price to depreciate. If we look closely at the earnings presentation, we will see that while Palantir’s US commercial revenue increased by 55% Y/Y, it increased only by 6% Q/Q. At the same time, while the US commercial count was up 83% Y/Y, it was up only 13% Q/Q.

The big annual increase could be attributed to the fact that Palantir’s flagship product AIP was launched only in April of 2023, so the Q2’23 numbers that served as a base for comparison for the current year were not that impressive in the first place. That’s why the company was able to deliver solid Y/Y growth in Q2’24. We believe that a growth rate won’t be as impressive going forward since the main cohort of clients has already started to use AIP in recent quarters, and we would make the case that the Q/Q numbers support our point of view.

In addition, we believe that no matter how useful AIP is for enterprises, with a market cap of over $70 billion Palantir can’t realistically be worth more than half of the entire generative AI market, which is expected to be worth $128 billion this year.

The Stock Price Continues To Make No Sense

When we published our update on Palantir last month, we also added our valuation model, the goal of which was to figure out what is the real value of the company. That model revealed that Palantir’s intrinsic value is only $13.55 per share. Since Palantir reported good numbers for Q2 last week and prompted the management to increase the guidance for the fiscal year, we decided to make some changes to our model as well to better reflect the company’s opportunities and risks.

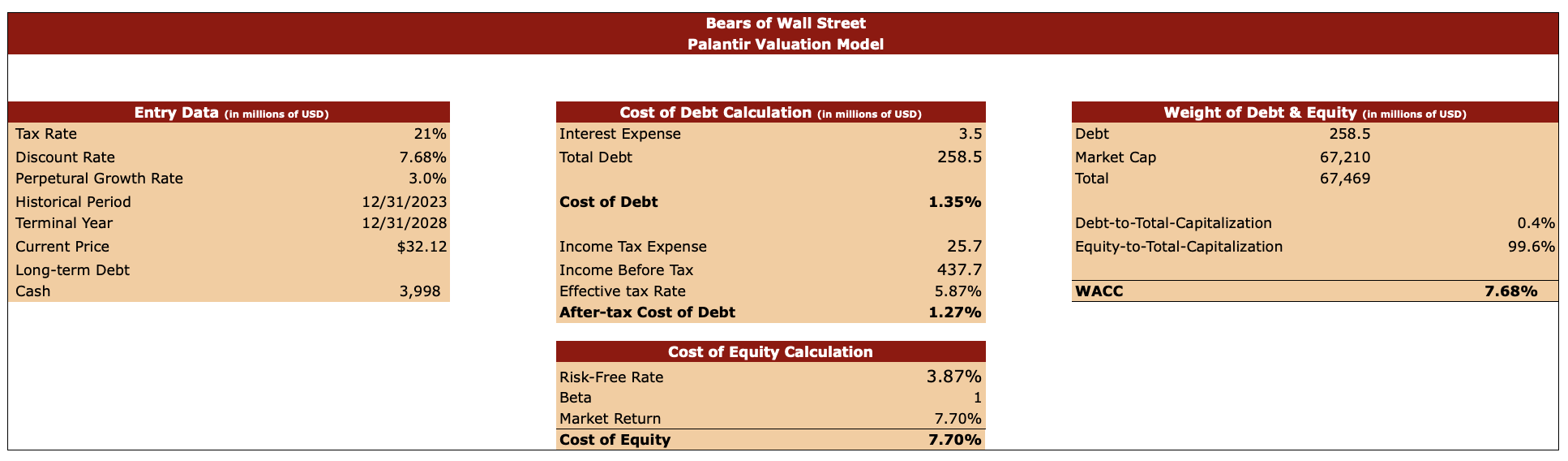

On the left side of the table below, some of the data has been changed, while some has remained the same as before. The tax rate and the perpetual growth rate are the same as they were in our previous valuation model. The share price at the moment of the valuation is $32.12 per share, and the cash reserves data now includes the data from Q2. The forecasted period remained the same as before as well.

The discount rate in our valuation model is 7.68%. The calculation of the discount rate is presented in the middle and the right side of the table below. To calculate the cost of debt, Palantir’s TTM financial data was used. When calculating the cost of equity, we used the beta of 1, which is similar to the market’s beta; the risk-free rate of 3.87%, which is the current yield of the 10-year treasury note; and the market return of 7.70%, which is the inflation-adjusted return of the S&P 500 since 1950. In the end, we got a discount rate of 7.68%, which is similar to the cost of equity simply because Palantir has a relatively clean balance sheet with little total debt. This is why the cost of equity has a greater weight when figuring out the discount rate.

Valuation Model (Bears of Wall Street)

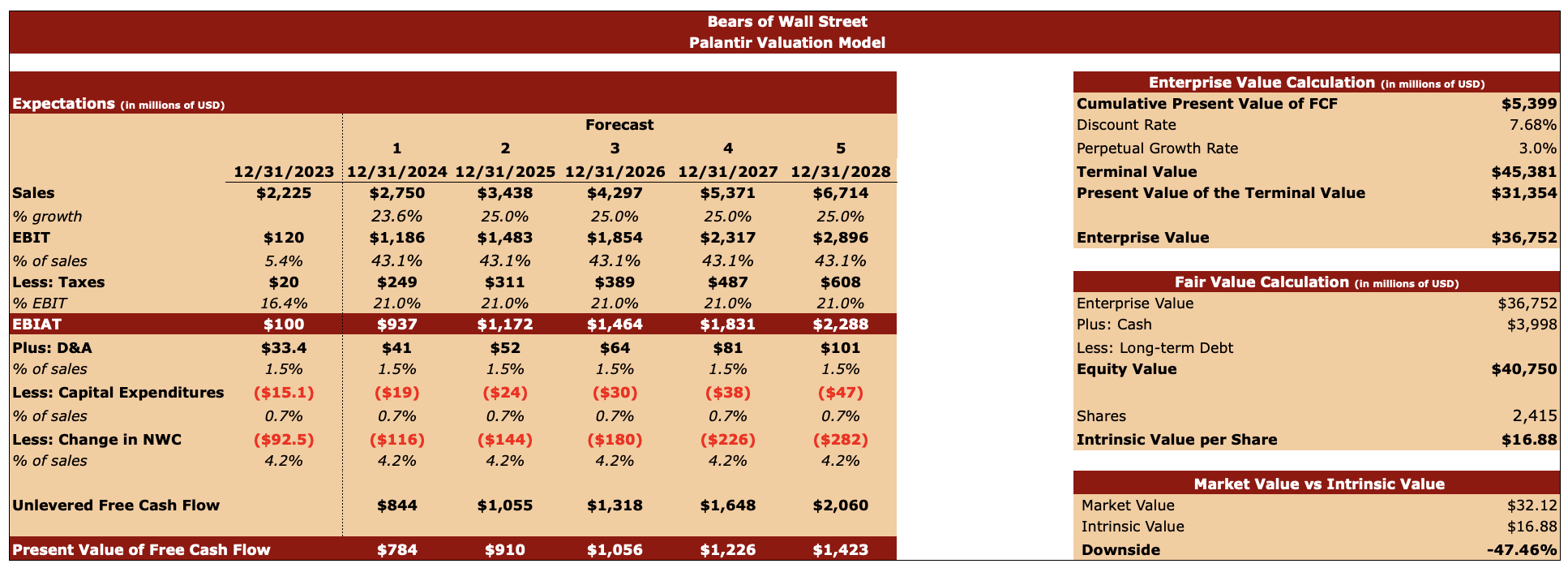

When it comes to the forecast of Palantir’s sales and earnings, we’ve changed several things. First, we have increased Palantir’s sales expectations for the fiscal year 2024 to $2.75 billion, which is on the higher end of the management’s latest guidance. We also assumed a sales growth rate of 25% in the following period, which is higher than the current expectations. It is done to simply ensure that our model covers a potential increase of guidance as it happened recently when the Q2 report came in and the analysts started to revise their estimates.

We have also aggressively increased the EBIT assumptions for the upcoming years from the 35% rate that was used in the previous model to 43.1% in the current model. The explanation for it is simple. As generative AI tools and platforms become more popular and able to improve the companies’ margins, it makes sense to assume that the earnings are going to improve as well.

If we look at Microsoft’s (MSFT) financial statement, we will see that the company has greatly improved its sales and earnings in recent quarters in large thanks to the launch of its generative AI assistant Copilot. Microsoft’s CEO Satya Nadella in the latest conference call also called Palantir one of the leaders of the Models as a Service business, which is experiencing an increase in usage of its products. This indicates that AIP’s and Copilot’s enterprise clients likely have a lot in common. That’s why after we divided Microsoft’s EBIT of $27.93 billion for the recent quarter by its revenues of $64.73 billion, we found out that Microsoft’s EBIT accounts for 43.1% of its revenues and decided to apply the same rate to Palantir as well. By doing so we could once again ensure that the model properly covers a potential increase of guidance. The forecast for other things remained the same as before.

Once found the present value of FCF under our new forecast, we can calculate the cumulative present value of FCF, apply the discount rate and the perpetual growth rate from before, and figure out Palantir’s terminal value, the present value of the terminal value, and the enterprise value, which in our case is $36.75 billion. After that, we add the cash resources to the enterprise value and don’t subtract any long-term debt because the isn’t any to calculate Palantir’s equity value, which in our case is $40.75 billion. We then divide the equity value by the number of shares at the end of Q2 and find out that Palantir’s intrinsic value is $16.88 per share. This means that the company is currently overvalued by nearly 50%.

Valuation Model (Bears of Wall Street)

While Palantir’s intrinsic value in this model increased by over 300 basis points in comparison to our latest model from July, it nevertheless helped us figure out an important thing. By applying optimistic assumptions for the sales and EBIT, we can figure out what is Palantir’s ceiling in terms of its performance and why even under the optimistic assumptions the company remains significantly overvalued. That’s why giving Palantir a STRONG SELL recommendation is the only viable option in our opinion as the current stock price continues to make no sense for us.

Major Downside to Our Bearish Thesis

One thing that seasoned investors know for a fact is that the market can stay irrational longer than they could remain solvent. The story of Palantir’s price action proves this point. Fundamentally, Palantir is extremely overvalued as it has a forward price-to-earnings ratio of nearly 100x. However, the stock could continue to trade above the technical support level of $30 per share.

In our opinion, two things can undermine Palantir’s current momentum. The first thing is the worsening of macro conditions, which could result in the overall market selloff and push Palantir’s price lower closer to its intrinsic value. The second thing is a much lower Y/Y growth of revenues and customer count, which could undermine investors’ confidence. Given a much weaker Q/Q growth, this could happen later this year or at the beginning of next year. That is why we believe that Palantir continues to be a STRONG SELL, but it can take a while before the fundamentals begin to matter again.

Our Short Strategy

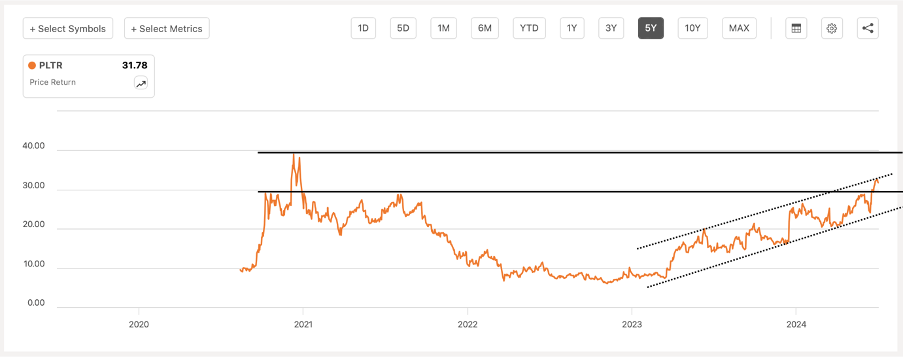

In our latest article from July, we disclosed that we are short Palantir. Back then we saw that the stock was losing its momentum and has hit an important technical resistance level. We opened that position around the time that article was published in the range between $28 and $29 per share and continue to hold it to this day. The position is shares-only, and no put options are involved.

The chart below shows that after more than a year of depreciation, Palantir’s shares began to rebound in the spring of 2023 primarily thanks to the entrance of the company into the generative AI field with the launch of AIP. However, in 2024, the performance was mixed, as the shares were unable to breach an important technical resistance level of $30 per share first at the start of the year and later earlier this summer, and were trading within a closed range.

A week after our article was published, the shares depreciated to below $23 per share but were still within the closed range that’s shown between the dotted lines on the chart below. Our thinking was that without a major catalyst, the share price could collapse below that range and depreciate closer to the company’s fair value. However, the earnings results in early August came better than expected and the guidance was improved, which pushed the shares higher to above the $30 per share level at which Palantir currently trades.

Stock Performance (Seeking Alpha)

There are several ways to go from here now. If Palantir fails to hold above $30 per share for longer and fails to go above the closed dotted range, then we have a good chance of the stock depreciating to its previous technical support levels which would be much harder to hold without another major catalyst. If the stock price goes higher, then the next major resistance level would be close to the company’s all-time high level of $39 per share.

In the first scenario, our goal would be to start taking profits at around $20 per share and possibly below, which is relatively close to the intrinsic value of the company in our model. In the second scenario, we plan to exit the position at a loss above $39 per share, wait for the establishment of new support and resistance levels, and only then reenter the short trade since we believe that the growth of Palantir’s stock can’t last forever.

Since shorting is always risky, we decided to deploy less than 5% of our portfolio capital for this trade as there’s always a possibility that the share price will remain irrational for a while.

If the stock continues to trade around $30 per share, then we will continue to hold our short position until the price goes significantly up or down. The annual percentage rate of borrowing is less than 1%, so we believe that the risks associated with shorting Palantir are worth it for us right now, as the potential reward could be significant.

Analyst’s Disclosure: I/we have a beneficial short position in the shares of PLTR either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.