Summary:

- PayPal is putting profitability back into the driver’s seat of its growth story under the leadership of its new CEO Alex Chriss.

- The stock’s resilience despite PayPal’s slashed guidance for 2023, the Venmo-Amazon breakup, as well as recent market volatility in response to mixed market data on the labour market underscores confidence.

- Looking ahead, PayPal remains well-positioned to benefit from a V-shaped recovery.

- Near-term value-accretive factors include easing lapping dynamics on revenue, a resilient holiday shopping season, and stabilizing take-rate on inflationary tailwinds in TPV, which complements ongoing margin expansion efforts through improved operating leverage.

Justin Sullivan

PayPal’s (NASDAQ:PYPL) latest earnings call was led by its newly installed President and CEO Alex Chriss, succeeding Dan Schulman following his retirement announced earlier this year. As discussed in our previous coverage, PayPal’s new CEO is expected to drive greater clarity into the company’s forward outlook. And investors were already able to get a small glimpse of this in PayPal’s third quarter earnings release, with Chriss embedding “profitable growth” as the core driving principle ahead for the payments processing company. Under Chriss’ leadership, PayPal has also named Jamie Miller as its new permanent CFO, which represents progress in putting an end to its 13-month running streak of temporary placeholders within the company’s senior management team.

Despite the company’s slashed full-year guidance for its adjusted operating margin, citing the extended persistence of existing revenue headwinds, the stock has climbed close to 20% since its Q3 earnings release. PayPal’s recent valuation gains have stayed resilient despite Amazon’s (AMZN) breakup with Venmo earlier this month, which risks thwarting the company’s trajectory on better monetizing the peer-to-peer payment platform. The market’s response continues to reflect investor focus and optimism on PayPal’s anticipated return to a sustained trajectory of profitable growth, which retracts previous missteps on spreading itself too thin through acquisition-related overexpansion in recent years. Management’s commitment to margin expansion is also expected to better compensate for structural buyers’ regression following the post-pandemic boom in e-commerce, as well as transitory cyclical headwinds stemming from ongoing macroeconomic uncertainties.

Looking ahead, PayPal’s anticipated delivery of a clear business roadmap with profitable growth at its core in the coming months under Chriss’ leadership, alongside consistent positive progress in improving operating leverage as management has committed to will be key drivers to the stock. We believe PayPal remains well-positioned to benefit from a V-shaped recovery in the near-term, similar to what has recently been observed at growth peers, such as Meta Platforms (META) and Salesforce (CRM), that have rediverted focus to operating efficiency and margin expansion to compensate for normalizing growth.

PayPal’s New Playbook: Profit Comes First

Restoring profit margin expansion has been a key lifeline for growth stocks that have been punished for their topline underperformance this year – whether that has been due to company-specific challenges or the broader economic downturn. And we expect a similar set-up for PayPal, which harbours a similar trajectory of value creation within the foreseeable future, as it focuses on further scaling opportunities within its core checkout and back-end payments processing services, and redeploys resources from rightsizing its operations into acquiring incremental demand from its target end-users.

While management has yet to provide a detailed roadmap on its key focus areas for the upcoming year, and the extent of which it plans to improve operating leverage going forward, PayPal’s guidance for the current quarter implies its transaction margin compression observed in recent quarters has bottomed. Specifically, PayPal’s non-GAAP operating margin of 22.2% in Q3 represents a drop of 18 bps from the prior year due to the combination of persistent revenue headwinds, spanning outsized contractual compensation revenue from merchants last year and the impact of persistent currency volatility on FX-related fee revenue. Although management expects a similar portfolio of headwinds in the current quarter, ensuing transaction margin dollars are now expected to show sequential improvement from Q3.

Fading Transitory Revenue Headwinds

This puts PayPal’s upcoming inflection to sustained profitable growth on the right foot, and will likely be complemented by a reduced impact from lapping a tough prior year revenue comp. Specifically, management has cited the outsized contractual compensation received from merchants last year, which PayPal does not have the benefit of in the current year, as a key culprit to the challenging set-up for transaction margin dollars.

Recall that PayPal charges a contractual compensation penalty from merchants that have violated rules on the contractual partnership, including for the engagement in fraudulent transactions and/or participating in the sales of counterfeit items. Contractual compensation received from merchants are recorded into transaction revenue, and has a direct impact on the transaction margin. The company recorded $190 million in contractual compensation from merchants in 2022, which is more than double the amount observed in 2021.

As this balance normalized through 2023, the company has already faced a combined revenue headwind of more than $150 million (~$75 million disclosed in Q2 and Q3) through September 30 compared to the same period last year. This effectively underscores a lesser impact stemming from lapping strong PY contractual compensation payments moving forward, which corroborates a sequential improvement to transaction margin dollars in Q4 as management has guided, and supports an easier PY comp set-up heading into 2024.

Holiday Shopping Tailwind

Meanwhile, PayPal continues to face an elevated exposure to ongoing macroeconomic uncertainties given its inherent sensitivity to the discretionary spending environment. However, the consumer has, time and again, prevailed with resilience. Online sales observed through the latest Black Friday/Cyber Monday (“BFCM”) holiday shopping season grew 7.4% y/y. This contributed to market expectations for an overall 4.8% growth in online sales during the final two months of the year, outpacing 2022’s performance, despite remaining “well below the annual average rate of 13% growth before the pandemic” to support a cooling economy.

At PayPal, specifically, the company processed approximately 400 million transactions over the annual post-Thanksgiving shopping weekend alone. Cyber Monday, which primarily benefits online storefronts, drew in 87 million transactions for PayPal, representing total payment volume of $5.8 billion. To put into better perspective, this represents a quarterly TPV run-rate of more than $533 billion, which represents sequential growth of 38% from Q3’s TPV of $387.7 billion. While PayPal is not expected to achieve this kind of TPV for the current quarter, robust transactions processed on Cyber Monday corroborates another strong holiday quarter for the company despite the shaky consumer backdrop, and lessens concerns that ongoing macroeconomic uncertainties could disrupt its full year outlook.

While the consumer shows risks, it is rapidly losing steam heading into the new year, as pandemic-era savings are expected to run out by the end of 2023, with consumer-level debt and related delinquency rates on the rise amid a high borrowing cost environment, PayPal is mitigating its exposure by capturing opportunities elsewhere. We expect PayPal’s Buy Now Pay Later offering to have been a key beneficiary of the latest BFCM shopping season, while also driving adjacent revenue through branded checkout. Payment data showed a rise BNPL checkouts during the latest BFCM shopping frenzy to more than $7 billion, with the figure expected to rise 17% y/y to a total of $17 billion by the end of the holiday season.

In order to hedge for rising default risks, PayPal has been active in externalizing its BNPL loans portfolio. This includes its arrangement to offload up to €40 billion of its European BNPL receivables to KKR under an exclusive multi-year agreement with the firm. The arrangement is expected to generate up to $1.8 billion in proceeds initially, of which $1 billion will be allocated towards its $5 billion capital returns program pledged for full year 2023. The company has already realized $1.4 billion of the planned initial proceeds to date, with the “next tranche of [its] back book sale of credit receivables” likely to have closed in November. This underscores the potential for PayPal to have a similar strategy in the works for the U.S., which would be significant in limiting its net credit exposure and reduce the stock’s sensitivity to macro-driven multiple compression risks.

Creating Value Where It Matters

And over the longer-term, Chriss has also pinpointed priority for greater monetization of PayPal’s SMB-heavy merchant base by driving a unique value proposition through its portfolio of branded checkout solutions, while also scaling Braintree deployments at its large enterprise customers.

SMBs: This includes scaling the recently launched features within PayPal’s complete payments solution to make it easier for SMBs to sell globally. Currently, PayPal’s complete payments solution allows SMBs to process purchases using PayPal, Venmo and BNPL. And this slate has recently expanded to include Apple Pay (AAPL), as well as the previously discussed “Passkey” feature that enables a low-friction, password-less check-out experience for customers.

Continued expansion of PayPal’s complete payments solution is expected to reinforce its margin expansion trajectory through scale by better facilitating SMB merchants’ prioritization over customer acquisition and conversion. More than half of online shoppers have cited the absence of their preferred payment method as a typical reason for abandoning their shopping carts at check-out, underscoring the importance for SMBs to include a comprehensive slate of payment options in order to drive conversion.

In order to drive better cost efficiencies for SMBs, another key consideration for the cohort of price-sensitive merchants, PayPal will also be offering “market-leading rates on processing fees for card payments, alternative payment methods and other digital wallets (e.g. Apple Pay), at just 2.59% + 49 cents”. This compares to 3.49% + a 49-cent fixed fee PayPal currently charges on its own branded payment options (e.g. PayPal Checkout; Venmo; PayPal BNPL; crypto), and an industry average of up to 3.5% charged on credit card transactions by traditional payments processing avenues. With more than 80% of commerce remaining offline today, and “trillions of offline retail dollars moving online over the much longer-term”, PayPal’s continued ramp-up of its complete payments solutions for SMBs is expected to improve its market share gains within the fastest-growing multi-channel storefront segment.

Large Enterprises: Braintree continues to be a key focus area for PayPal, with the payments processing solution now commanding a 10% share of large enterprise e-commerce transactions worldwide. Braintree also remains the key growth driver at PayPal, compensating for the slight deceleration observed in branded checkout volumes. The growth trend underscores PayPal’s ability in capturing opportunities from the less recession-prone large enterprise cohort through Braintree, which has been key for mitigating its exposure to competitive and broader macroeconomic challenges facing branded check-out.

However, Braintree remains a less profitable arm of PayPal’s core businesses, with the segment’s higher volume mix in recent quarters having an adverse impact on transaction expenses and, inadvertently, transaction margin dollars. This is largely in line with expectations that large enterprises have historically had stronger pricing power, thus impacting Braintree’s pace of margin expansion with scale.

Looking ahead, we expect management’s reiterated commitment to profitable growth and improving operating leverage to be key in unlocking incremental value from Braintree’s resilient demand environment. This includes the continued ramp of Braintree deployments for large enterprises at scale, as well as potential price increases on the horizon to better match the product’s value proposition to large enterprise merchants, and facilitate ongoing margin expansion efforts.

We have a beachhead now with Braintree, which I’m really excited about. And I think we’ve earned the right now to expand margin and make sure that we’re really pricing to value and ensuring that we’re delivering what we need to across the board.

PayPal’s expanded Braintree penetration into SMB opportunities could also represent a value accretive undertaking in the near-term. Recall from earlier this year when management had contemplated the extension of Braintree to the SMB market. This was estimated to expand its TAM by about $750 billion. While Braintree remains largely an enterprise-focused offering, we see similar end-to-end payments processing capabilities now being offered in the recently introduced PayPal complete payments solution catered to SMBs. We expect the SMB-driven Braintree opportunity to drive higher margins with scaled deployments over the longer-term, as the cohort typically has less pricing power relative to the large enterprises, and complement the company’s broader efforts in driving profitable revenue growth.

And PayPal’s ability to utilize insights on consumers’ buying behaviours, interests and spending habits through payments data acquired through Braintree is also expected to drive adjacent value for the company’s broader operations and further aid its margin expansion efforts. Paired with the accelerating implementation of AI capabilities, PayPal is well-positioned to create greater value for both merchants and consumers by improving the user experience, enabling cost efficiencies and driving conversion, while also bolstering its own demand environment critical to achieving better operating leverage through scale

Consumers: Meanwhile, on the consumer front, management’s focus on improving integration across the consumer PayPal wallet features with the broader check-out experience will be key to improving market share retention and transaction volumes going forward. This will likely reinforce scalability of related deployments and improve margin accretive monetization across PayPal’s wallet share of consumers.

The relevant integration initiatives are evident through PayPal’s expanded features in the PayPal complete payments offering discussed in the earlier section, which will improve consumers’ check-out experience by catering to a wider range of payment options. This is further expanded into the post-checkout experience through an integrated rewards system, spanning cashback on purchases made with the PayPal Mastercard and PayPal Rewards.

And PayPal’s further integration of data acquired across its core Braintree and branded checkout offerings is expected to drive incremental value-add features to consumers’ shopping experience, including an AI-powered “shopping recommendation engine to provide more relevant rewards and savings back to customers”. This is expected to improve PayPal’s appeal to online shoppers worldwide and drive incremental transaction volumes, especially as their sensitivity to price changes increase amid tightening financial conditions. Specifically, more than 60% of consumers are on the hunt for discounts heading into the holiday shopping season, as they look to “spend the least amount of money possible”, underscoring the value that PayPal’s integrated check-out experience has to offer.

Fundamental and Valuation Considerations

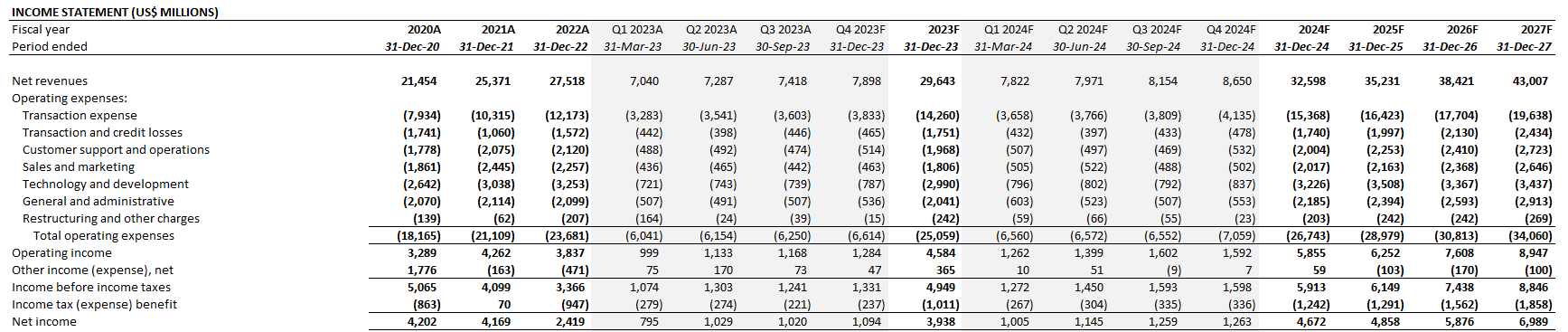

Adjusting our previous forecast for PayPal’s actual Q3 performance, revised guidance, and forward prospects based on the foregoing analysis on management’s commitment to profitable growth, we expect the company to finish the fiscal year with revenue growth of 8% y/y to $29.6 billion. This would imply transaction revenue growth of about 6% y/y to $26.7 billion for full year 2023, based on more than $1.5 billion in total payment volume, which is in line with expectations for another resilient holiday quarter ahead.

Author

Meanwhile, we expect a transaction margin of 45.6% in Q4 (or $3.6 billion in transaction margin dollars), which would represent a slight sequential improvement and continued y/y contraction due to ongoing revenue mix and lapping dynamics. Taken together, we expect full year 2023 transaction margin of about 46%. As ongoing contraction in transaction margin is likely to have bottomed in Q3, we expect the metric to complement management’s commitment to improving operating leverage through scale going forward, which represents a strong set-up for further income and cash flow growth over the longer-term.

Author

PayPal_-_Forecasted_Financial_Information.pdf

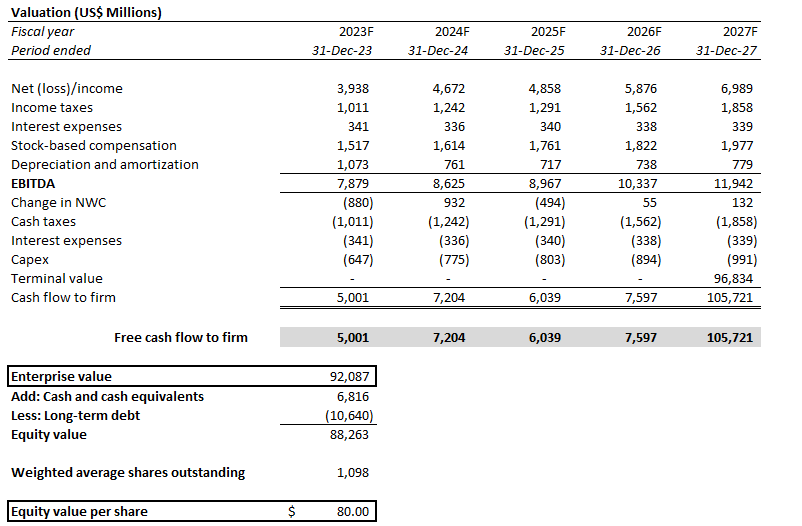

Taken together with continued divestments of non-core businesses at PayPal and other initiatives taken to right-size the business for better focus on its core business opportunities, the company is also well-positioned for improved growth of cash flows underpinning its valuation prospects. We are setting a base case price target for the stock at $80.

Author

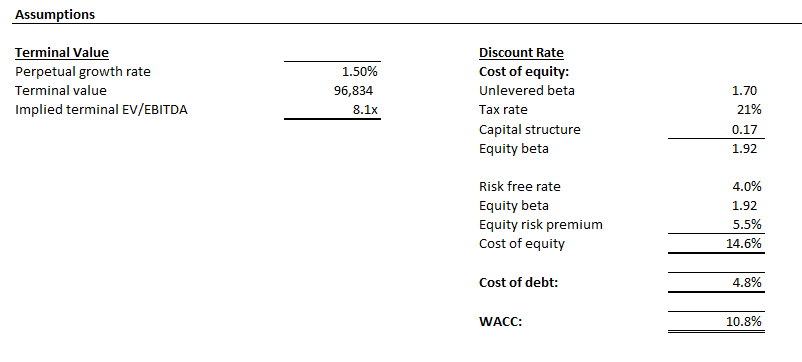

Despite our optimism for PayPal’s cash flow prospects under its profitable growth strategy, we have downwardly revised our price target for the stock given recent changes to the company’s capital structure and risk profile relative to the elevated normalized risk-free rate environment. Specifically, our price target is computed via the discounted cash flow analysis, which applies cash flow projections taken in conjunction with the fundamental forecast discussed in the earlier section. A WACC of 10.8% is applied, up from 10.5% assumed in our previous forecast, to account for the estimated increase in the normalized RFR from 3.5% to 4% under the “higher for longer” Fed policy stance. Our analysis also applies a 1.5% estimated perpetual growth rate on terminal cash flows, up from the conservative 0% applied in our previous forecast, to account for PayPal’s prospects for sustained margin accretive revenue growth under its improved business roadmap.

Author

Author

Risks to Consider

As discussed in the earlier section of our analysis, PayPal’s business model is inherently sensitive to changes in the consumer discretionary spending environment. Given the shaky macroeconomic backdrop, with growing signs of a deteriorating consumer despite resilient spending habits during the latest holiday shopping season, we remain cautious on the relevant impact on PayPal’s near-term growth prospects.

Specifically, Walmart (WMT) – both a gauge for the U.S. retail industry, as well as one of PayPal’s largest merchants – has recently warned of growing risks of consumer spending exhaustion as the double-whammy of rising borrowing costs and persistent inflation continues to hit demand. This potentially underscores headwinds to PayPal’s near-term TPV growth and ensuing challenges to its efforts in driving improved operating leverage through scale.

The recent breakout between Amazon and Venmo also represents a near-term headwind to monetizing the peer-to-peer payment platform. While reports have cited a potential lack of traction in payments with Venmo on Amazon, the falling-out effectively removes Venmo from partaking in a take-rate of as much as 3.5% (plus a fixed fee per transaction) on Amazon’s expansive reach into online shopping dollars. Although Venmo’s current contributions to PayPal’s bottom-line remain nominal, its breakup with Amazon also puts any future prospects of PayPal integration into the largest online shopping platform further out of reach.

Final Thoughts

Admittedly, PayPal’s valuation has been beaten by its inherent sensitivity to uncertainties within the consumer discretionary spending environment due to tightening financial conditions, in addition to structural headwinds stemming from the post-pandemic regression in broader e-commerce demand and heightened industry competition. Paired with the company’s unruly overexpansion in recent years, both its profitability and cash flows underpinning the stock’s valuation prospects have also taken a hit.

While PayPal is still in the early stages of a turnaround under the new leadership team, management’s acknowledgement of the underlying challenges and directly addressing investors’ calls for a returned focus on profitability is positive to the turning of a new page. Looking ahead, execution and delivery of management’s commitment to putting profitable growth at the core of PayPal’s operations going forward will be key to unlocking pent-up value in the stock. This will be particularly key to bolstering cash flows underpinning PayPal’s valuation prospects and its capital returns program, which are crucial to driving further upside potential.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Thank you for reading my analysis. If you are interested in interacting with me directly in chat, more research content and tools designed for growth investing, and joining a community of like-minded investors, please take a moment to review my Marketplace service Livy Investment Research. Our service’s key offerings include:

- A subscription to our weekly tech and market news recap

- Full access to our portfolio of research coverage and complementary editing-enabled financial models

- A compilation of growth-focused industry primers and peer comps

Feel free to check it out risk-free through the two-week free trial. I hope to see you there!