Summary:

- With lower revenue and greater losses, PENN Entertainment’s first quarter earnings were a disappointment for investors.

- However, during the quarter, I believe the company made some positive steps for better management of ESPN Bet.

- As the stock valuation in terms of the P/S multiple is hovering around the historical bottom, I believe the stock price would show better performance in the coming months.

SolStock

Thesis

PENN Entertainment, Inc. (NASDAQ:PENN) recently announced its Q1 earnings, which once again disappointed investors, causing the stock to drop more than -17% during the day and finishing roughly -9% lower. In my opinion, investors in the current stock market put more value on companies that generate immediate profits, rather than those that incur high costs through investments without any plans for profits. This appears to be the case for PENN, with lower revenue and higher costs due to ESPN Bet. However, despite the disappointing earnings for the first quarter, it still has some potential. With historically low valuation in terms of Price-to-Sales multiples, it is worth it for investors to be patient, as the Interactive segment could potentially trigger momentum for an increase in the stock price.

Overview of the First Quarter Earnings: Bad Results, but with Good News

Review of the First Quarter Earnings

The company’s earnings report

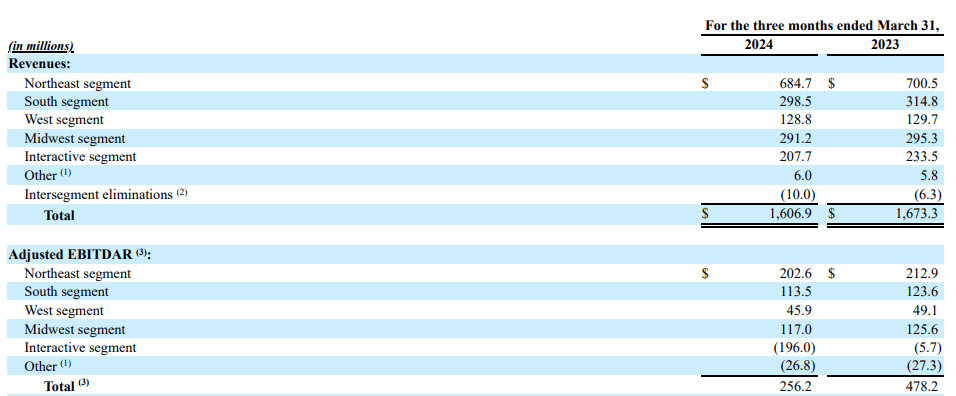

Overall, compared to the first quarter of 2023, the revenue for the first quarter of 2024 decreased by 4%, and the gross margin dropped sharply from 41.8% to 29.6%. The cost of goods sold for the first quarter of 2024 was $1,130.7 million, whereas it was $973.8 million in the first quarter of 2023. According to the company’s earnings report, the difference, roughly $157 million, came from gaming expenses incurred due to ESPN Bet, which is about $150 million. With these numbers, I believe ESPN Bet continues to be a loophole that increases costs for the company.

To dive more deeply into each segment, the retail business recorded $1.4 billion, which decreased by roughly 3% from the first quarter of 2023. I believe this drop was understandable due to the negative impact of bad weather in January, and it is expected to gradually recover. On the margin side, the adjusted EBITDAR margin dropped from roughly 35.5% to 34.1% in this quarter due to increased costs such as labor. The Interactive Segment recorded $207.7 million, with $196 million losses of EBITDAR. When compared to the first quarter of 2023, the revenue dropped by 11% with substantial costs.

Revised Guidance

The company updated its guidance for 2024. The company now expects the Retail segment to earn revenue between $5.61~$5.76 billion, with $1.88~$2.00 billion of EBITDAR. Compared to the previous guidance, the revenue is likely to increase slightly with a lower margin. For the Interactive segment, now the company expects to generate revenue between $1.02~$1.07 billion. This is a huge drop from the previous guidance, when the company anticipated revenue between $1.28~$1.42 billion. In contrast, the company is expecting it would incur more losses ranging from -$475~–$525. Overall, I believe the guidance was negative and may have put pressure on the stock price.

Qualitative point

Despite the disappointing first quarter earnings report, in my perspective, there are some positive steps the company made during the quarter.

Firstly, a Disney CTO, Aaron LaBerge, who directed Disney technology initiatives such as Disney Plus, was appointed as the CTO of PENN Entertainment. One of the crucial factors necessary for the company to retain sports bettors was to improve the user experience of the ESPN Bet application. By focusing more on overall improvements of the ESPN Bet application and making an effort to increase parlays like competitors, I think the management understands what the problem is and heading in the right direction.

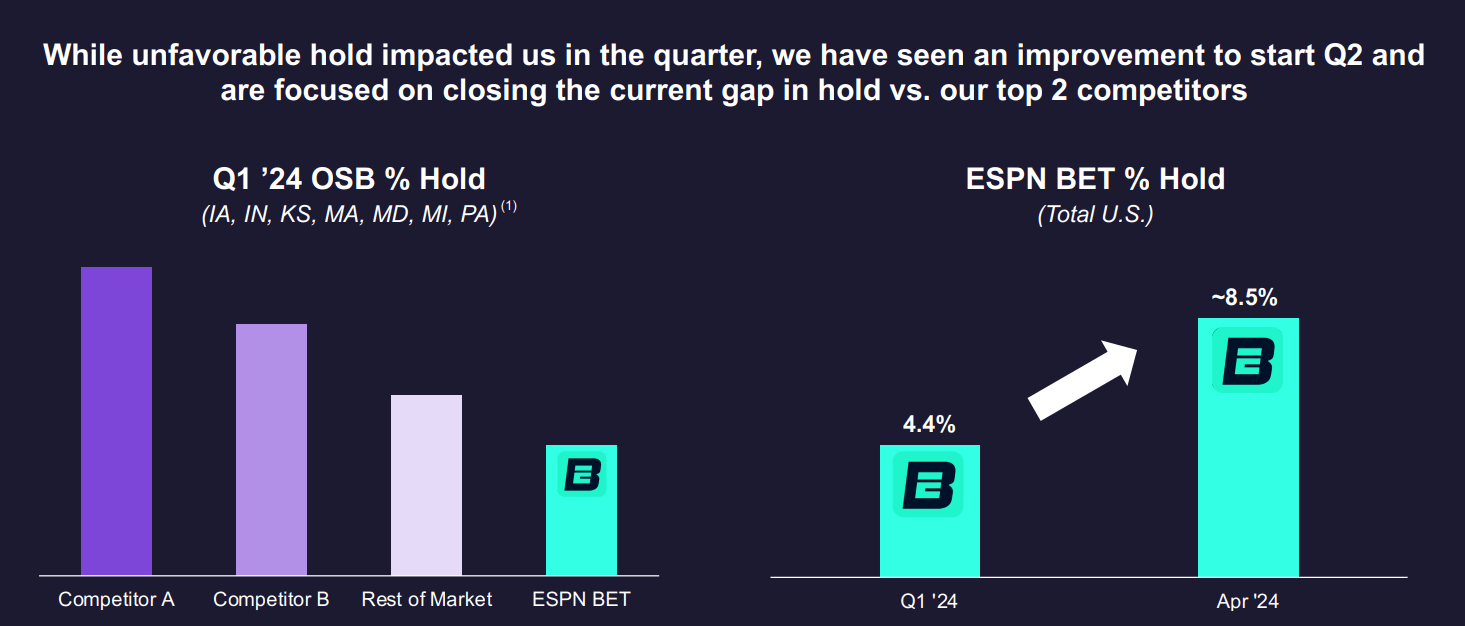

Secondly, ESPN Bet’s performance has improved in terms of hold rate, despite a decrease in market share. To summarize the performance of ESPN Bet in the first quarter of 2024, the sportsbook achieved higher hold rates with lower promotions, but experienced a decrease in the market share despite the differences among states. These states are the examples.

On Maryland, from January to March, the market share of ESPN Bet was 6.8%, 5.2%, 6.1% respectively whereas the hold rates moved from 4.4%, 7.9%, 1.5% respectively.

On Iowa, from January to March, the market share of ESPN Bet was 7.0%, 5.3%, 4.3% respectively, whereas the hold rates moved from 0.4%, 4.8%, 7.4% respectively.

On Massachusetts from January to March, the market share of ESPN Bet was 7.1%, 5.8%, 5.4% respectively, whereas the hold rates moved from 4.5%, 7.3%, 7.5% respectively.

Penn Entertainment Earnings Presentation

For April, the company reported that the overall hold rate has improved from 4.4% in the first quarter to 8.5%. In my opinion, even though the market share and hold rates of ESPN Bet are still far from sufficient, they are moving in the right direction.

- I calculated market share by dividing the company’s handle by total handles.

- I calculated hold rates by dividing the company’s revenue by handle.

- Even though I checked several times, I recommend investors verify the numbers individually.

Valuation

Similar to my previous article, I would continue to use P/S multiple to find out whether PENN is undervalued or not. To get a better understanding of why I’m using P/S multiple and walk through the company’s stock price history, I recommend investors read my previous article.

Seeking Alpha

In my previous article, I argued that the historical bottom of the company’s valuation in terms of P/S multiple is around 0.3. When the first quarter earnings report was released, the stock price dropped sharply, but rebounded after it reached $13.5. With the revised revenue guidance, the P/S multiple at the stock price of $13.5 is roughly 0.306, which, I believe, is the short-term bottom. At the current market cap of $2.4 billion, the P/S multiple hovers around 0.36. As I believe that the negative factors such as huge losses regarding ESPN Bet are partially reflected in the stock market, the current market valuation is not expensive.

Risk

- Possibility for disappointing earnings

The revised guidance related to ESPN Bet, which was presented on the first quarter conference call, is based on April hold rates and current market share trends. However, roughly 8% hold rates recorded in April are somewhat high when compared to historical trends. I recommend investors track ESPN Bet’s monthly handles and hold rates from each state’s official homepage to check whether the company can meet its guidance.

- Decreasing discretionary spending

I believe the basic scenario for investing in the company is that the retail segment works as a cash cow to sustain investments for ESPN Bet. However, consumers would likely decrease spending on casinos if high interest rates and inflation lead to lower disposable income.

- Focus on Growth Stocks

My investment approach in PENN is not based on the growth-oriented style, but focuses on deep value. If money flows again to growth stocks such as A.I.-related companies, I think the company may not attract interest from the stock market, requiring investors to be patient for a longer period of time.

Conclusion

Even though the first quarter earnings fell short of expectations, considering that ESPN Bet is slowly heading in the right direction and the current valuation of PENN is near its historical bottom, I will maintain a Buy recommendation for this stock.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of PENN either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.