Summary:

- PepsiCo’s Q2 financial results beat top and bottom-line estimates, leading to an upgraded FY23 outlook with higher expected revenue and EPS.

- PepsiCo continues to see resilient demand for its products, which allows it to increase prices. Still, the company did see a slight drop in volumes in Q2.

- The company’s strong brand portfolio and focus on zero-sugar options and new product launches are expected to drive sustained growth.

- Management’s long-term targets of achieving 5-6% revenue growth and high-single-digit EPS growth are conservative.

Justin Merriman

Investment thesis

I maintain my buy rating on PepsiCo (NASDAQ:PEP) stock and update my revenue and EPS estimates following the company’s Q2 financial results, which beat both the top and bottom-line estimates from Wall Street analysts. As a result of this beat, PepsiCo has upgraded its FY23 outlook as it expects revenue and EPS to come in higher than previously anticipated.

PepsiCo is definitely not one of the most exciting companies out there. It generates little headlines and usually only receives investor attention once a quarter as it releases another strong earnings report. And yet, despite the lack of excitement, this company has proven to be one of the most stable and impressive investments over the last several decades. The company’s stability and wide economic moat make it a true Sleep Well At Night stock for investors and a solid compounder, which is why PepsiCo is one of my top stock picks.

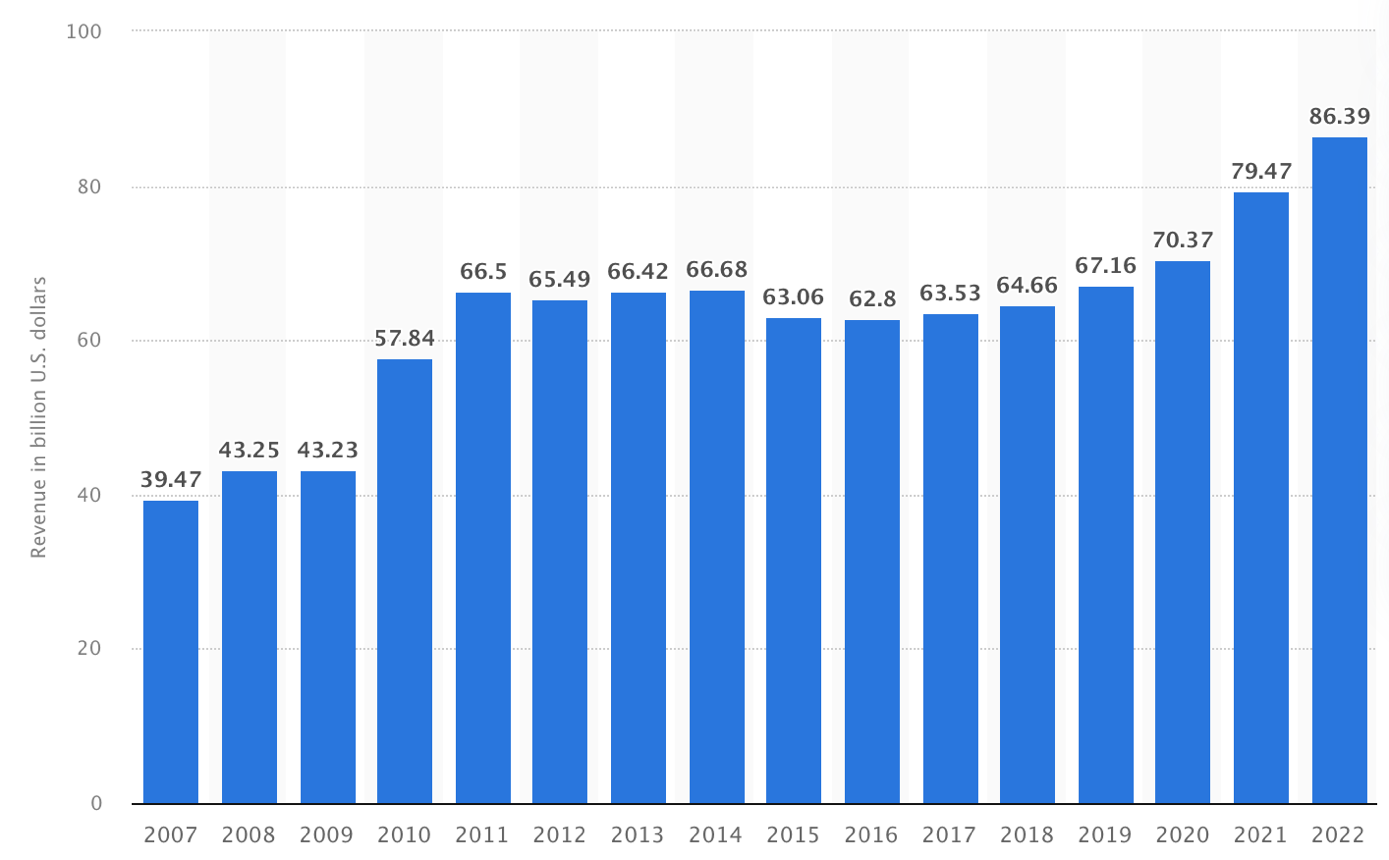

Its unmatched portfolio of beverage and food brands that includes multi-billion-dollar brands like Pepsi, Mountain Dew, Gatorade, Lay’s, Doritos, and Cheetos gives it incredible worldwide resiliency as, in the food and beverage industry, a moat is all about brand recognition and economies of scale. Even when consumer spending power falls, PepsiCo’s volumes generally hold up very well as its preferred brands are incredibly popular worldwide. This has earned the company the #1 position in the global convenient foods industry and the #2 in beverages, allowing it to optimally benefit from industry growth. As a result, the company was able to grow revenue at a CAGR of 5.31% from 2007 through 2022. On top of this, through acquisitions, divestitures, and margin improvements, EPS has grown at an even faster rate.

PepsiCo revenue (Statista)

In addition to its incredible global brand strength and financial stability, management also still sees plenty of growth opportunities out there to boost future growth, despite its already massive size. Besides the industry’s overall growth, one of PepsiCo’s most important growth drivers is the shift in consumer preferences. PepsiCo endeavors to tailor its product lineup to align with consumer preferences, exemplified by its emphasis on zero-sugar options in its beverage portfolio. This strategy involves introducing novel products within established brands that better cater to current preferences. Additionally, PepsiCo launches entirely new product brands that revolve around these emerging trends, leading to remarkable expansion for these niche brands. A notable example of this success can be observed with SodaStream, which offers a sustainable and healthier alternative to traditional bottled sodas. Alongside SodaStream, other rapidly growing product categories such as meals, energy drinks, and zero-sugar products are anticipated to drive sustained growth for PepsiCo in the long run.

Other growth opportunities for PepsiCo lie in the shift to digital and the integration of new technologies. PepsiCo aims or already uses, the latest high-tech innovations like AI or IoT to improve business operations.

By leveraging these growth opportunities, management believes it can consistently deliver 4% to 6% organic revenue growth and high single-digit operating EPS. I think investors should expect this business to grow revenues by closer to 5-6%, with bottom-line growth of close to 10% as management targets 20 to 30 basis point margin expansion every year.

In addition to this, the company’s impressive margins and financial health allow it to meaningfully reward its shareholders, resulting in PepsiCo becoming a rare dividend king after increasing its dividends for 51 consecutive years. PepsiCo remains focused on rewarding its shareholders and considering the expected growth, I believe that investors should expect the dividend to keep growing at around 7% a year, further boosting my enthusiasm for PepsiCo.

In the remainder of this article, I will take you through the latest developments and its Q2 results and update my estimates and view on the company accordingly. (This article builds on my initial article on the company last March)

PepsiCo remains one of the best-performing consumer staple companies after its Q2 results.

PepsiCo reported Q2 revenue of $22.32 billion, up 10.4% YoY and beating analyst estimates by $590 million. Organically, revenue was up by 13% YoY as its brand strength drove a strong performance in both the beverage and convenient food portfolio with these growing 11% and 15% YoY, respectively. Growth was still largely driven by price increases as overall volume growth for both convenient foods and beverages came in negative, although only slightly, with a 3% drop for convenient foods and a 1% drop in beverage volume.

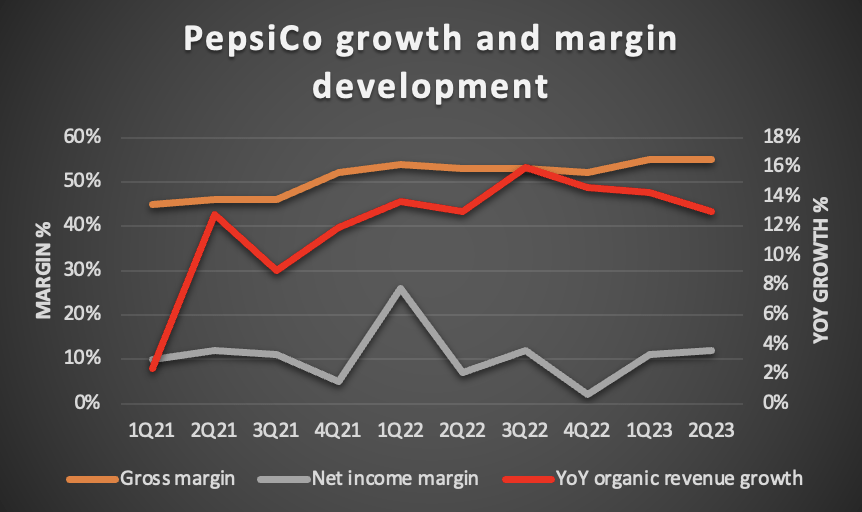

In relation to this, moving forward, reporting these growth rates will become much more challenging for PepsiCo as food inflation is moderating. Over the last two years, a large part of the growth (visible in the graph below) was driven by price increases which followed the increase in input and operational costs. Yet, with food inflation now easing off to 5.7% YoY and only 0.1% sequentially, this growth driver will most likely disappear slowly over the remainder of 2023, bringing growth back to more normalized levels of around mid-single digits. Of course, the massive food inflation we have seen over recent years and meaningful price increases across PepsiCo’s brands has also had a negative effect on volume growth, further boosted by decreasing consumer purchasing power.

Author

Looking at the Q2 performance by segment, North America saw solid organic overall growth of 11% YoY. The performance in Frito-Lay North America remains strong (+14% YoY) with a seventh consecutive quarter of double-digit growth. The segment’s solid collection of products gives it the ability to drive continued top-line momentum and further market share gains in savory and salty.

Beverages also performed well in the North American region as this one delivered 10% organic revenue growth. In particular, Energy drinks performed well, partly driven by advancements in zero-sugar offerings and the increasing popularity of this type of drink.

According to data collected by Nielsen, growth in energy drink sales is accelerating with the data showing growth of 12.5% YoY in the March to May period, while May alone recorded growth of 13.1%. And while pricing was the largest contributor to this growth, volumes are clearly holding up better than many other food and beverage categories, also outpacing soda sales and alcoholic beverage sales. As PepsiCo currently holds a market share of approximately 5% in the energy drinks market, it is a meaningful beneficiary of this resilience. However, the company is far behind industry leaders Monster (MNST) and Red Bull with a 37% and 35% market share, respectively. With an expected CAGR of 8.3% through 2030, the outlook for the energy drinks industry is very solid, making it an important market for PepsiCo.

Also, the focus from PepsiCo on zero-sugar beverages, in general, is a crucial one as this is expected to remain a significant growth driver of the beverage industry. Future Market Insights even projects the zero-sugar beverages market to grow at a very strong 14.7% CAGR through 2033 as growth accelerates from the 12.5% CAGR recorded over the last four years.

PepsiCo’s continued efforts in zero-sugar and energy drinks are positioning it well for continued beverage growth. Just this last quarter the company released and refreshed several zero-sugar and energy drink products, opened the newest Gatorade Sports Science Institute Research & Development lab, and obtained licenses to distribute Hard Mtn Dew. As a result of these efforts, it remains optimistic about profitably growing this operating segment.

The performance in the Quaker Foods North America segment was somewhat weaker as this recorded a limited increase of 2% YoY and core operating profit declined, driven by double-digit growth in advertising and marketing spend. Meanwhile, the business does continue to take market share across the board, solidifying its revenue potential.

Moving to the performance of the international business segment, this saw organic growth of 15%, primarily driven by an impressive performance across most international regions as Europe recorded organic growth of 19%, 13% growth in Latin America, and 18% in Africa, Middle East and South Asia. In general, growth in emerging markets remains essential for PepsiCo. According to management, it continues to drive the impressive international performance as the company is rapidly gaining market share in these regions. However, it should be noted that foreign exchange rates had quite an impact on these regions, resulting in an overall 2.5 percentage point negative FX impact on overall net revenue.

Moving to the bottom line, PepsiCo saw margin improvements across the board despite another double-digit advertising and marketing expenses increase. The focus of management on continued investments in advertising and marketing is crucial in maintaining the strong moat of its brand portfolio. Therefore this YoY increase is a huge positive. And even despite these continued investments, PepsiCo managed to expand the core gross margin by 130 basis points YoY, while the operating margin expanded by 45 basis points.

Cost management initiatives, unlocking capacity constraints, and further advancements in the digitalization process across the organization drove these positive margin developments. The previous graph showed that PepsiCo had been consistently increasing gross margins over the last two years, and with inflation and supply chain constraints now easing, there is still plenty of room for further margin increases over the next several quarters. As mentioned before, PepsiCo believes it will be able to drive 20 to 30 basis point margin expansion a year for the foreseeable future. Following these margin improvements, core EPS increased by 12% YoY to $2.09 and beat estimates by $0.13.

Outlook & PEP stock valuation

Following the solid results in the first half of the year, PepsiCo upgraded its FY23 outlook and now expects to report 10% organic revenue growth (from a previous 8%) and 12% core constant currency EPS growth (from a previous 9%). This should bring core EPS to $7.47, up from a previous expectation of $7.27 and above the consensus of $7.32, as well as my own previous expectation of $7.30.

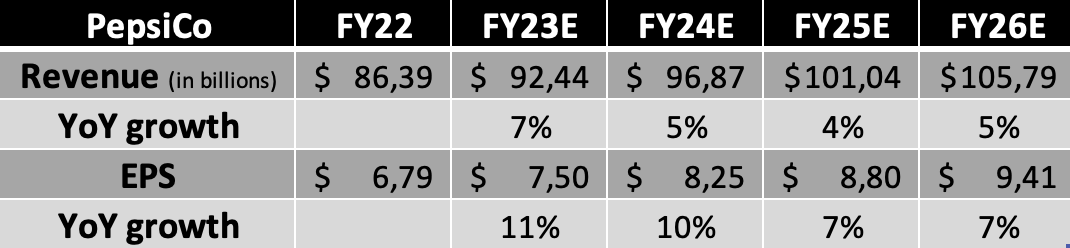

Considering this upgraded outlook from management and the company’s resilient quarterly result that has come in above my previous expectations, I have upgraded my revenue and EPS expectations until FY26. This results in the following:

Revenue and EPS estimates through 2026 (Author)

(I expect Q3 revenue of $23.46 billion and EPS of $2.16)

Shortly explaining these estimates, I now expect PepsiCo to report revenue growth of 7% for the full year. I am projecting growth to slow in the second half of the year as the company faces tough comparable quarters and easing inflation. Volumes will remain under pressure for the remainder of the year, but PepsiCo is well-positioned to outperform many of its peers and grab more market share across its product segments. Furthermore, improving margins as a result of cost-saving initiatives, easing supply chain challenges, and lowering input costs will boost EPS growth as I project this to remain in the double digits.

For the following years, I project revenue growth to normalize to mid-single-digit levels and EPS growth to remain in the high-single digits, aligning with management’s long-term expectations, as PepsiCo is poised for continued margin improvements. Also, continued share buybacks will be a tailwind for EPS growth. Overall, PepsiCo will remain an outperformer in the consumer staples sector.

Yet, the company’s excellent ability to drive surprisingly strong growth has also made it quite expensive. Shares currently trade at a forward P/E of 25x, somewhat above its 5-year average of 24.5x and far above the sector average of around 19x. Of course, investors should realize that a dividend king with a stable growth outlook does demand a premium. Yet, getting the right entry price is crucial to support strong long-term returns. Also, Coca-Cola (KO), a great alternative to PepsiCo, is currently trading below its 5-year average valuation.

So, whereas this company deserves to be trading at a premium, the current share price is very demanding from a long-term perspective. Personally, I believe shares are trading at around fair value today as I believe a 24x P/E is appropriate for this high-quality compounder. Based on this and my FY24 EPS estimate, I calculate a target price of $198, leaving an upside of only 5%. (Please note, this target price is solely based on its forward P/E and is only for indicative purposes.)

For comparison, Wall Street analysts currently maintain an average price target of $200 combined with a buy rating.

Conclusion

The overall performance from PepsiCo this quarter was very positive. Apart from the obvious strong financial performance, the company also continues its operational excellence by making several important strategic decisions like increasing exposure to zero sugar and energy drinks in beverages and increasing market share in convenient foods, which will solidify its long-term growth potential and global strength.

Yet, the strong performance has given the shares a slight boost in recent days, resulting in a very demanding valuation that sits above its 5-year average. Therefore, shares are a hold at a current price of $188. Today, I recommend to hold the shares as the long-term potential is still impressive, favorably positioning investors for solid returns. If shares dropped below $180, these would become a more attractive buy based on a better margin of safety.

I rate PepsiCo shares a hold.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of PEP either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.