Summary:

- PepsiCo reported Q3 results that beat expectations.

- The management team paired the beat with a favorable revision to full-year earnings guidance.

- Though volume trends continue to disappoint, robust strength in PEP’s international business is providing a valuable offset.

- I maintain a bullish view on PEP following current results and its recent weakness over the last six months.

Spauln

PepsiCo (NASDAQ:PEP) just reported Q3 results that beat expectations. In prior coverage on the stock, I have maintained a bullish view due in part to continuing strength in their Frito-Lay division and its growing revenue parity with PEP’s namesake unit.

Just prior to their Q2 release, I also noted that shares were at greater risk of a pullback due to the current run-up in the shares. At the time, PEP was trading near their 52-week high in the mid-$190/share range. Since that update, the stock has pulled back by about 12%, considerably worse than the S&P’s 1% loss over the same period.

Despite the recent weakness, I maintain the view that the stock has a pathway to $200/share. At current trading levels, there is a steep hill to get there. And though shares may not reach that target in the near-medium term, recent results reaffirm my overall bullish view on the stock.

PEP Q3 Results

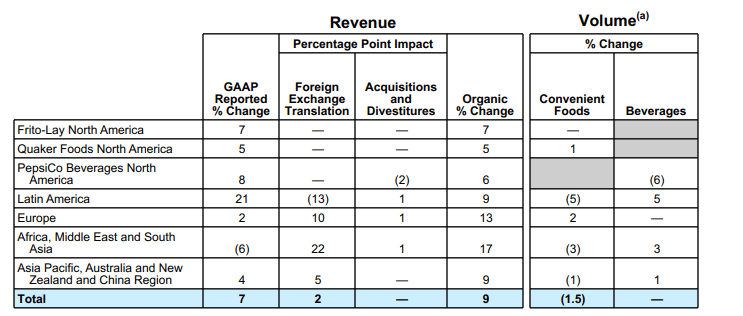

Total reported net revenues grew 6.7% YOY, in-line with estimates. On an organic basis, adjusting for foreign currency effects, revenues were up 8.8%, well above the consensus expectation of an increase of 8.3%.

Effective net pricing again drove revenues, as overall unit volume decreased 1.5%, led entirely by convenient foods. Here, PEP realized a mid-single-digit decline in Lay’s and a high-single-digit decline in their offering of dips. Offsetting the declines here to a degree was mid-single-digit growth in their Doritos and Cheetos brands.

PEP Q3 Earnings Release – Summary Of Revenue/Volume Performance

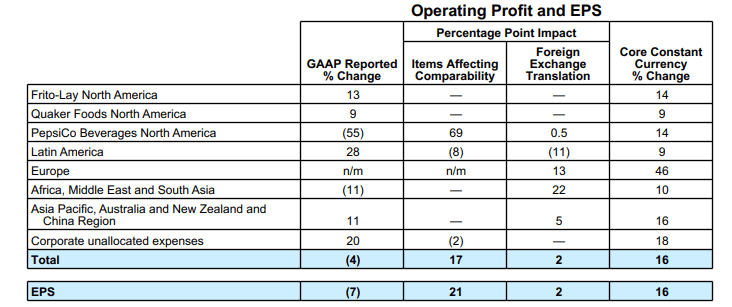

At the bottom line, PEP reported total core EPS of $2.25/share, reflecting a beat of $0.10/share, and representing a 16% YOY increase. Driving the earnings beat was continued strength in margins from cost savings and pricing actions. Core gross margins were up 105 basis points (“bps”), while core operating margins were up 80bps.

PEP Q3 Earnings Release – Summary Of Operating Profit/EPS Performance

Among their individual divisions, PEP reported growth in all major reportable units. Frito-Lay North America (“FLNA”) grew 7% and gained additional market share in the macro and savory snack categories. Though positive, the results marked an end to the double-digit growth streak in this segment. In Q2, revenues in the unit were up 14%, marking the seventh consecutive quarter of double-digit growth.

The pullback in FLNA was offset by stronger performance in their Quaker unit, which grew 5% compared to 2% last quarter. PEP’s international segment also continued to exhibit robustness, as indicated by its 12% organic growth during Q3. This marked the tenth consecutive quarter of double-digit organic revenue growth.

Market Reaction To PEP Quarterly Results

In the pre-market trading hours immediately following the release, shares of PEP were up about 1%. This compares favorably to the broader S&P (SPY), which vacillated around the flatline.

The modest gains post-release is somewhat of a reprieve from the weakness seen in the shares over the last six months. The stock is down about 12% in this timeframe.

Seeking Alpha – PEP Share Price Performance Over Last Six Months

The decline is notable considering PEP had also hit its 52-week high during this same period. The weakness could have been attributable to investor anxiety regarding PEP’s volume performance, which continues to reflect negatively on their otherwise positive revenue figures. Additionally, a persistently inflationary environment is leading some analysts to express their concerns regarding potential customer trade down to private label brands.

Outlook For PEP Stock Following Q3 Results

PEP’s weaker volume performance still hasn’t negatively impacted their overall operating performance. Looking ahead, PEP continues to see strength in their global beverage and convenient foods businesses. The optimism enabled the management team to reiterate guidance for full-year organic revenue growth. Consistent with Q2, organic revenues are seen growing 10%.

And further headway in their cost management initiatives provided the team the confidence to raise their expectations for EPS growth. Full-year 2023 EPS is now seen growing 13%, up from 12% previously and ahead of consensus analyst expectations.

Is PEP Stock A Buy, Sell, Or Hold?

PEP has exhibited expectation-beating organic revenue strength throughout FY23. One aspect of this outperformance is their continuing strength in their Frito-Lay division, as well their robust growth internationally. In my view, I expect the strength in each to continue, but perhaps more so internationally, which currently is on its tenth consecutive quarter of double-digit revenue growth.

The streak of double-digit growth in PEP’s Frito-Lay division, on the other hand, ended in Q3. And I am expecting the unit to remain in upper-single-digit territory moving forward. Furthermore, I expect PEP’s Doritos and Cheetos brands to continue outperforming their Lay’s trademark, which is an offering more likely at risk of consumer trade-down to private label brands.

Looking at the management team’s forecast for full-year revenue growth, I believe the 10% organic revenue growth target is attainable, though I expect investors to become increasingly impatient with the company’s volume performance. While pricing actions thus far have fully negated the weakness, I believe PEP will face a more difficult comparable environment in FY24 without a turnaround in their unit sales.

Consensus estimates peg shares fairly valued at about $190/share. In past coverage, I viewed $200/share as more likely. Recent results reaffirmed my bullish view on the stock. But the moderation seen in PEP’s Frito-Lay unit combined with the continuing weakness in unit sales warrant a reassessment of PEP’s value in the near-medium term.

At a 25x multiple of expected forward earnings, shares would be valued at just under $190/share, in-line with consensus estimates. Continued market-share gains in their core business and growing strength internationally could support this multiple in the near-medium term.

For investors looking to build a position in a quality beverage company with staying power, I believe the dip in PEP over the last six months presents an attractive opportunity for new or further initiation.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.