Summary:

- Pfizer cuts financial guidance for 2024 due to slumping Covid drug demand and inability of the Seagen contribution to offset losses.

- The biopharma forecasts an EPS jump back to ~$2.15 in 2024, but the Covid business continues to impact financials.

- PFE stock gets intriguing at this valuation once Pfizer management is able to show stability in the business without further Covid drug sales hits.

Finnbarr Webster/Getty Images News

In another disappointing move, Pfizer Inc. (NYSE:PFE) cut financial guidance for the period ahead. The biopharma continues to struggle with slumping Covid drug demand, while the Seagen (SGEN) contribution can’t offset the big losses. My investment thesis remains Neutral on the stock, as the company works to reset the business while the stock has fallen dramatically.

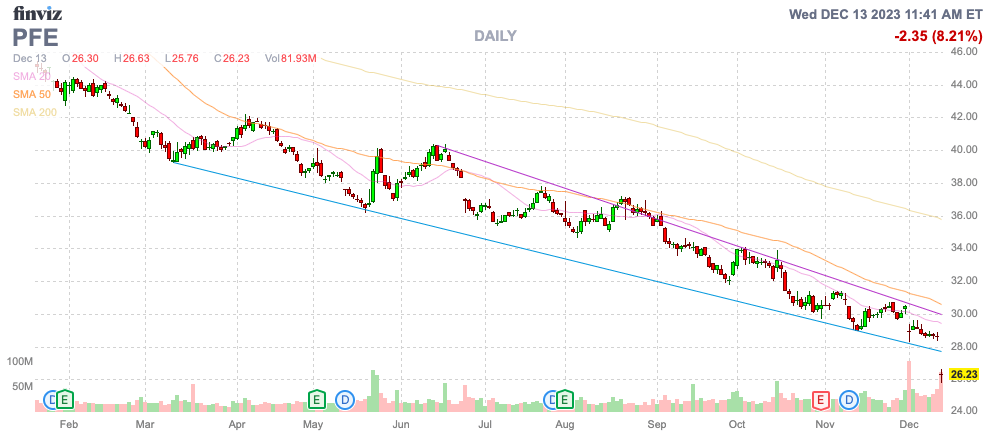

Source: Finviz

Another Big Guidance Cut From Pfizer

Only back in October, Pfizer slashed estimates for 2023 after the biopharma amended a supply agreement with the U.S. government for Paxlovid and cut forecasts for Covid vaccines. The new financial target cuts resets the expectations for 2024, as Covid demand continues to slump.

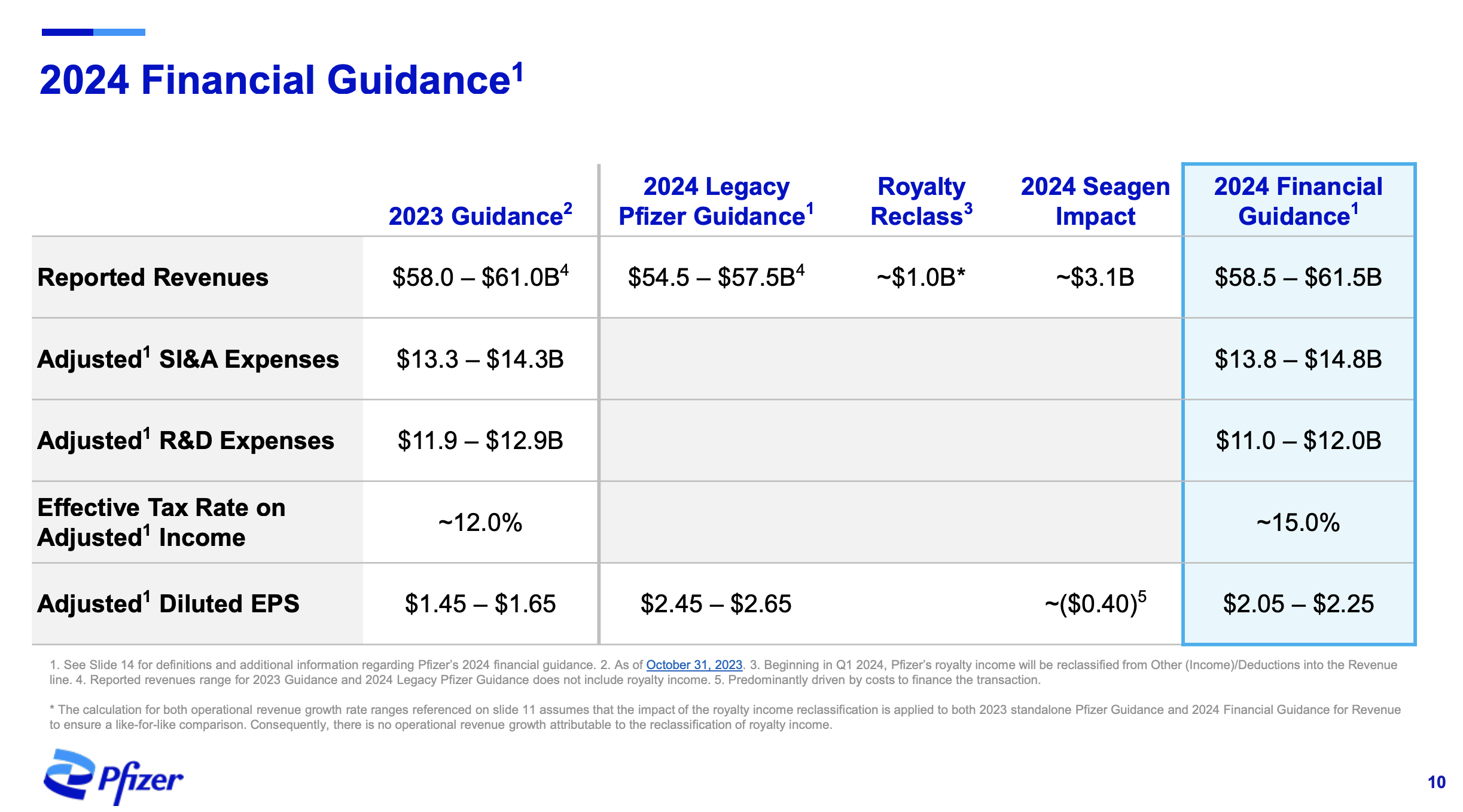

Pfizer is now guiding to revenues generally flat with 2023 numbers despite adding the Seagen business and shifting $1.0 in royalty payments to the revenue line. The Seagen deal is expected to close on December 14, with the cancer business adding ~$3.1 billion to sales in 2024.

Source: Pfizer 2024 presentation

Naturally, for the revenues to be flat next year despite adding in the Seagen business, Pfizer is cutting the legacy business guidance. The 2024 guidance as the legacy revenues slumping a similar amount to between $54.5 to $57.5 billion, down from $58.0 to $61.0 billion for 2023.

Due to up to $4.0 billion in cost cuts by the end of 2024, Pfizer is forecasting an EPS jumps to ~$2.55 next year, up from an estimate of $1.55 in 2023. The Seagen business will slash $0.40 from the estimates, leading the biopharma to a $2.15 EPS target for 2024.

The good news is that Pfizer again strips out a larger portion of the Covid revenues from the estimates for 2024. Though, the numbers due still forecast ~$8 billion for Comirnaty ($5B) and Paxlovid ($3B).

Back in October, Pfizer had guided to full-year 2023 Covid revenues of only $12.5 billion, down from an original estimate of $21.5 billion. The majority of the revenues were targeted towards the 2H, so these revenues were the expected run rate going forward, but Covid vaccine demand continues to slump.

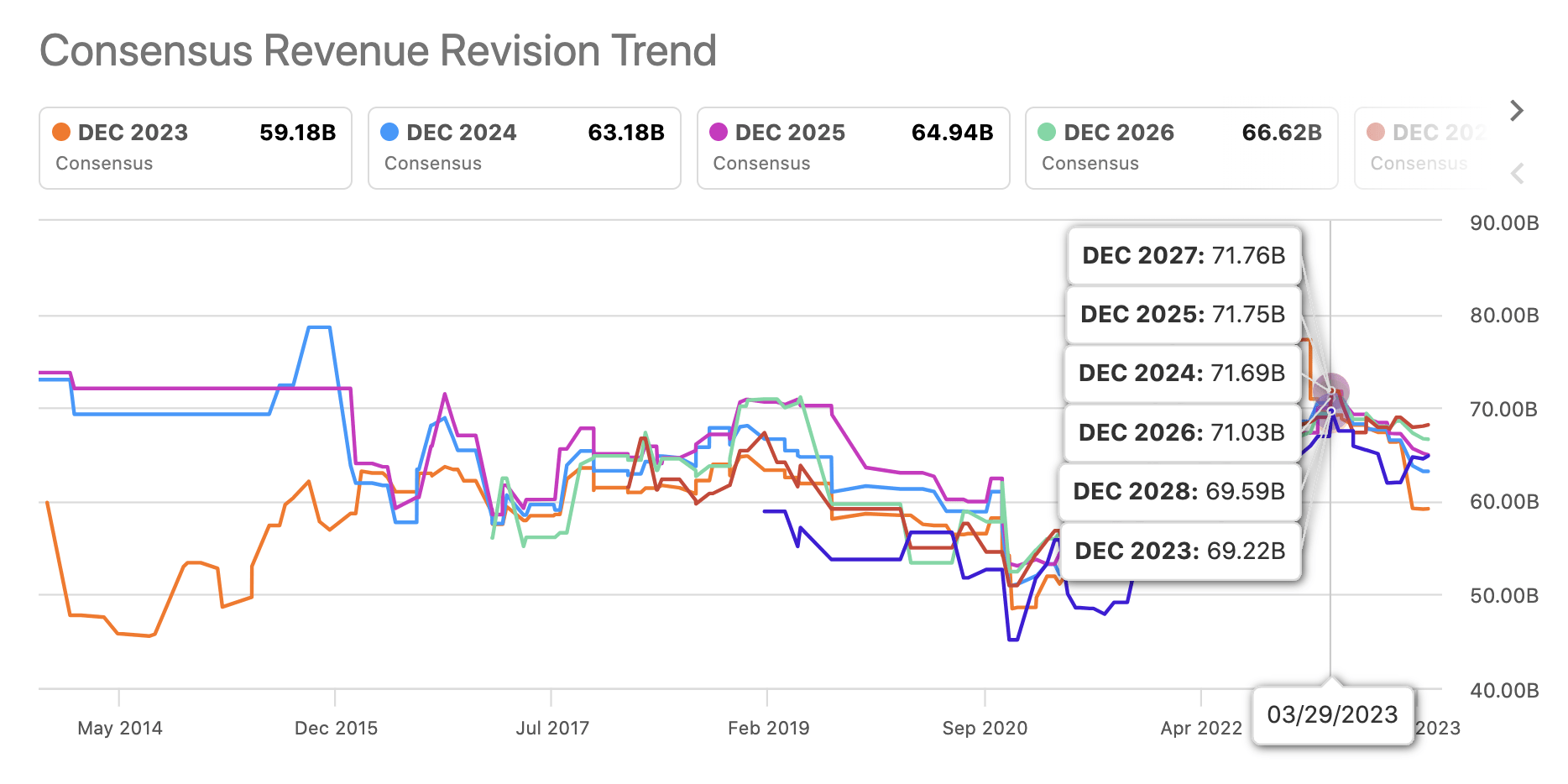

At the start of the year, Pfizer had forecast total revenues of up to $70 billion with consensus estimates generally forecasting revenues still in the $70 billion range in the years ahead. The forecast was for some general Covid sales run off offset by operational revenue growth outside of the Covid drugs in the 3% to 5% range.

Source: Seeking Alpha

In essence, Pfizer would probably be viewed in a better light without the Covid business in the way now with revenues growing somewhere from $50 billion to $60 billion over the decade. In addition, Seagen would add $3.1 billion to the prior revenue estimates.

Path Forward

Pfizer has an interesting underlying business, with the Seagen addition contributing to 8% to 10% growth without the Covid business. The company earned a $3+ EPS prior to all of the Covid boosts, so investors should look at those numbers as closer to normalization as the biopharma cuts costs and absorbs the extra Seagen costs.

When the deal was announced, Seagen was forecast to generate $2.2 billion in revenue this year and the consensus estimates predict a $2.4 billion target. Pfizer set a goal for sales of up to $10 billion by 2030.

The numbers don’t really add up with Pfizer paying $43 billion for cancer drugs. The balance sheet will suddenly have ~$65 billion in net debt just when the financial picture has significantly worsened. The biopharma will no longer have a strong Covid profit machine to help repay debt from the Seagen deal.

The annual dividend payout of ~$9 billion will absorb a lot of the cash flows in the next year, reducing the ability of Pfizer to repay debt in the short term. Investors will get a 6% dividend payout, as the company works out the troubles with the profits picture.

The stock is difficult to own here as the Covid shakeout continues. Once the drug company gets into 2024 and sets the floor in the Covid business, the stock could finally become investable.

Takeaway

The key investor takeaway is that investors were warned the Covid pain wasn’t over yet. Pfizer has dipped to new lows and the business still includes forecasts for $8 billion in revenues from the Covid drugs. Pfizer Inc. stock isn’t touchable until there is a full shakeout of the Covid business. At that point, Pfizer might get interesting, if the biopharma can continue to deliver non-Covid drug growth in the 3% to 5% range.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

The information contained herein is for informational purposes only. Nothing in this article should be taken as a solicitation to purchase or sell securities. Before buying or selling any stock, you should do your own research and reach your own conclusion or consult a financial advisor. Investing includes risks, including loss of principal.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

If you’d like to learn more about how to best position yourself in undervalued stocks mispriced by the market, consider joining Out Fox The Street.

The service offers a model portfolio, daily updates, trade alerts and real-time chat. Sign up now for a risk-free 2-week trial to started finding the best stocks with potential to double and triple in the next few years.