Summary:

- Pfizer’s stock underperforms the S&P 500, facing patent expirations and competition, yet offers a 6.3% forward dividend yield.

- Despite a positive Q3 earnings surprise, profitability remains weaker than pre-pandemic levels, and valuation analysis shows the stock is fairly valued.

- Pfizer’s oncology market share is modest, and its financials are weaker compared to leading competitors.

- High R&D spending and strong operating cash flow support potential new products and sustainable high dividend yield, but I maintain a ‘Hold’ recommendation.

JHVEPhoto/iStock Editorial via Getty Images

Introduction

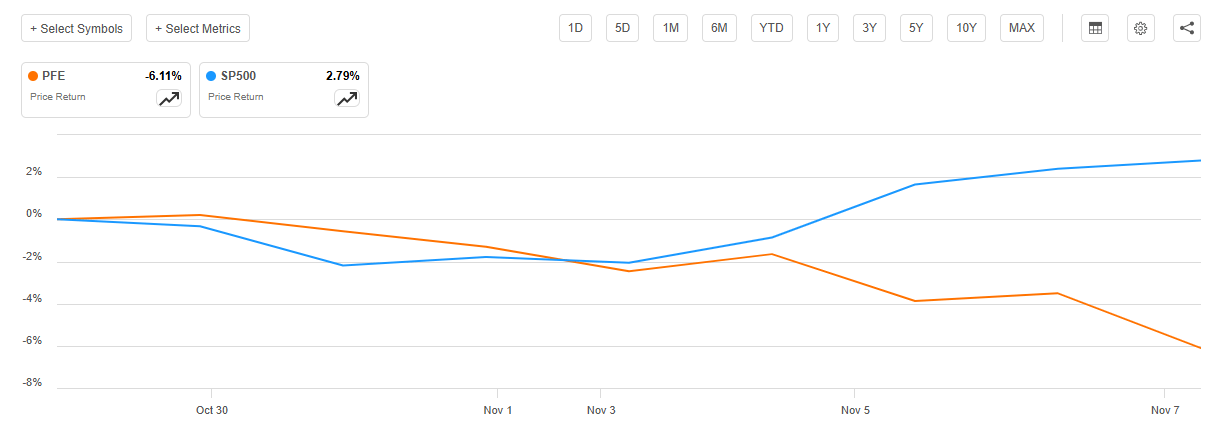

Pfizer (NYSE:PFE) continues performing weak compared to the S&P 500 index with a negative total return since my previous neutral call was published. The stock now offers a 6.3% forward dividend yield, which might attract some investors. Nevertheless, I remain cautious with my ‘Hold’ recommendation because Pfizer faces several fundamental issues that includes patent expirations for its several important products, increasing competition risks for its dominance in pneumococcal vaccines and several challenges in achieving its targets to expand its market share in oncology drugs. The recent Q3 earnings release delivered solid positive surprise, but profitability is still notably weaker compared to pre-pandemic levels. Furthermore, the valuation analysis indicates that there is no upside potential as the stock is approximately fairly valued.

Fundamental analysis

Despite its significant pharmaceutical market footprint, Pfizer continues underperforming compared to the S&P 500 index. The stock has lost around 27% of its value while the benchmark U.S. equity market index has almost doubled. One of the primary risks facing Pfizer is the expiration of patents for several key products. Products that are expected to lose their exclusivity in 2025-2027 include Eliquis, Prevnar, Ibrance, Xeljanz, Xtandi, and Inlyta. During Q3 2024 these six products’ sales accounted for one third of the company’s total revenue.

Compiled by the author based on the latest 10-Q

Thus, the loss of exclusivity for these six products poses a significant threat to one third of Pfizer’s sales and this is a large portion. Competition from generics typically leads to substantial price erosion and market share loss.

Pfizer has a solid historical record of developing and rolling out new compelling products, but the industry is becoming more and more competitive. For example, Pfizer’s Prevnar product is one of the leaders in the pneumococcal vaccine business that generated more than 10% of the company’s revenue in Q3. Prevnar is a dominant force in the industry as the product generated $6.4 billion in FY2023 sales while the industry size is estimated at $8.8 billion. However there are indications that Pfizer might lose its competitive edge in this niche over the next few years as Prevnar’s patent expires in 2026 and there is a competitive pressure from Vaxcyte (PCVX) that has advanced significantly in developing its pneumococcal vaccine.

Despite these two big fundamental issues, there are good developments as well. The company’s Q3 earnings release delivered dual positive surprise. Pfizer’s actual Q3 results were notably stronger compared to consensus expectations. The management also raised FY2024 revenue guidance to a range of $61.0 to $64.0 billion and raises adjusted diluted EPS guidance to a range of $2.75 to $2.95. Strong performance and guidance upgrades did not impress investors, though. The share price decreased by more than 6% after October 29.

SA

Another reason why investors are still bearish about PFE might be its slow profitability recovery. Despite Pfizer’s TTM revenue currently significantly higher compared to pre-pandemic levels, the TTM EBITDA is still notably below 2018-2019 levels.

Another reason of the market’s doubts about Pfizer might be explained by the management’s focus on oncology, which was reiterated during the Q3 earnings call. According to Statista, Pfizer is not even among the top five players in the oncology drug industry. Therefore, competing with more experienced players with larger footprints might be an extremely challenging task for Pfizer.

Statista

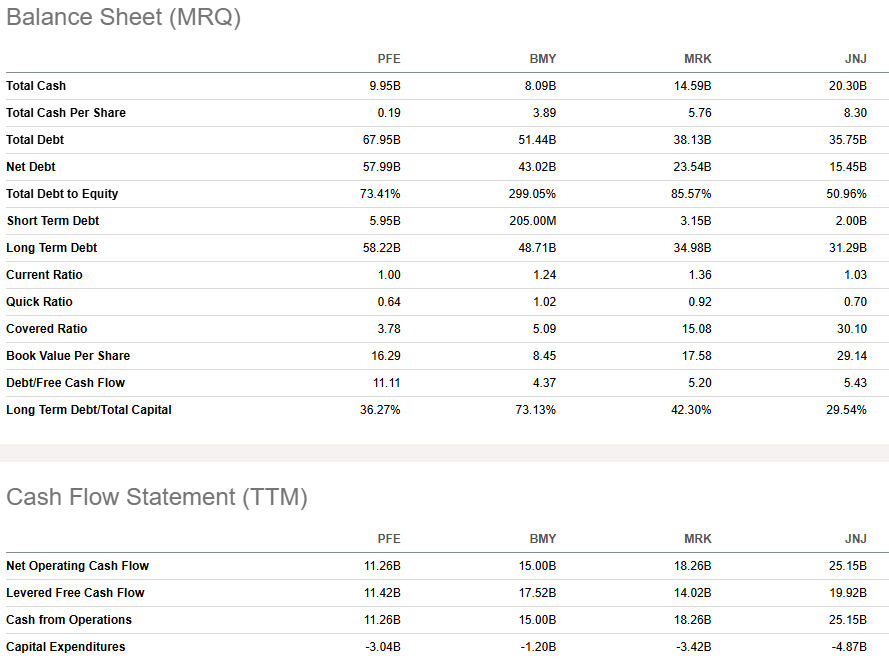

Pfizer’s relatively modest market share in oncology drugs is not the only significant challenge it faces. Compared to leading U.S.-based oncology drug companies like Bristol Myers Squibb (BMY), Merck (MRK), and Johnson & Johnson (JNJ), Pfizer is financially weaker. In addition to having the lowest trailing twelve-month levered free cash flow in absolute terms, Pfizer’s balance sheet is the weakest across almost all metrics. This positions Pfizer unfavorably against oncology drug leaders in terms of competition.

SA

In summary, despite Pfizer’s recent confident Q3 earnings beat against consensus estimates, there are some strong secular issues that will likely keep sentiment around the stock negative.

Valuation analysis

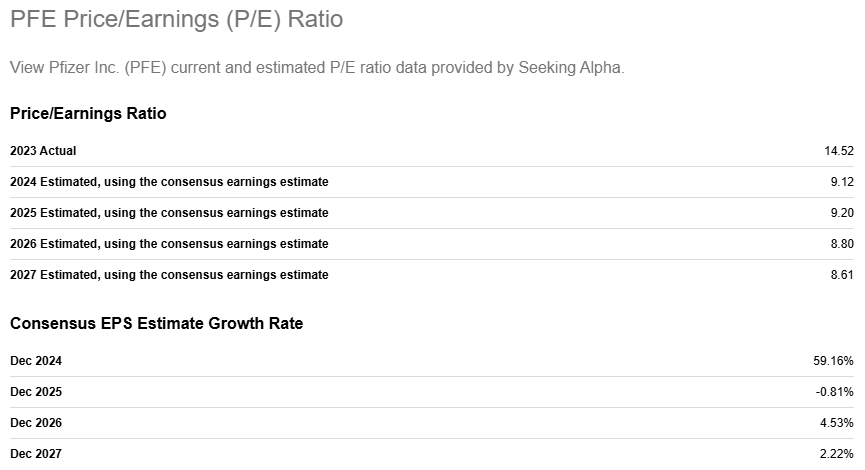

Pfizer has low forward P/E ratios for the next five years. The FY2027 forward P/E ratio is low at 8.61. On the other hand, we see that the ratio will not shrink significantly between FY2024 and FY2027, meaning that the EPS is expected to stagnate.

SA

Pfizer’s cost of equity is around 8%. According to the dividend scorecard, the forward annual payout is $1.68 and the last five years’ CAGR is 4.25%. These are the three key assumptions to simulate the DDM, which stands for the ‘dividend discount model.’

Calculated by the author

Based on these assumptions, PFE’s fair value per share is $44.8. This is 67% higher than the current market share, which is a massive discount. However, the discount can be easily explained by a few big fundamental issues that I have highlighted in my fundamental analysis.

Incorporating a 2% constant growth rate might be more reasonable given all the fundamental risks Pfizer’s investors are facing. With a more conservative dividend growth assumption, the estimated fair value is close to the market price. Therefore, it appears that PFE is somewhat fairly valued.

Calculated by the author

Mitigating factors

Pfizer might be a very attractive option for investors seeking a high dividend yield. The stock currently offers a generous 6.3% forward yield, which looks attractive even in the current tight monetary environment. As we saw in the balance sheet and cash flow peer comparison, despite being weaker positioned compared to rivals, Pfizer still has a strong operating cash flow and moderate leverage ratio, meaning that the high dividend yield is highly likely sustainable.

Due to its aggressive R&D spending, Pfizer has the potential to release new best-selling products over the next few years. Pfizer’s $10.6 billion R&D budget aligns with BMY, the leading player in the global oncology market. As of October 29, 2024, there were 108 candidates in the pipeline, with Phase 3 trials including 30 potential assets, four of which are under registration.

Conclusion

I remain cautious about PFE and reiterate my ‘Hold’ recommendation. Big secular issues persist despite the recent strong Q3 earnings release. The stock is approximately fairly valued at its current level.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.