Summary:

- It’s always and forever a market of stocks, not a stock market. The Nasdaq is up 45% YTD, while Pfizer Inc. stock is down 40%.

- Pfizer’s yield is at 14-year highs, nearly 30% undervalued. The collapse in earnings this year is pure pandemic vaccine boom fading.

- Pfizer’s long-term growth prospects are slightly better than the industry average, though it is growing 6X slower than Eli Lilly, which is powered by obesity drugs.

- In the medium term, patent cliffs on key drugs mean Pfizer is being left for dead in favor of its obesity drug-powered rivals. If you’re comfortable with its risk profile, Pfizer offers Warren Buffett-like 22% annual returns over the next 2 years.

- For those who don’t like Pharma or want superior yield, growth, and over 300% better long-term return potential than Pfizer, these five 9%-yielding blue-chip bargains are a fantastic opportunity to lock in as much as 150% returns in just the next two years, 7.5X more than the S&P 500.

Khosrork

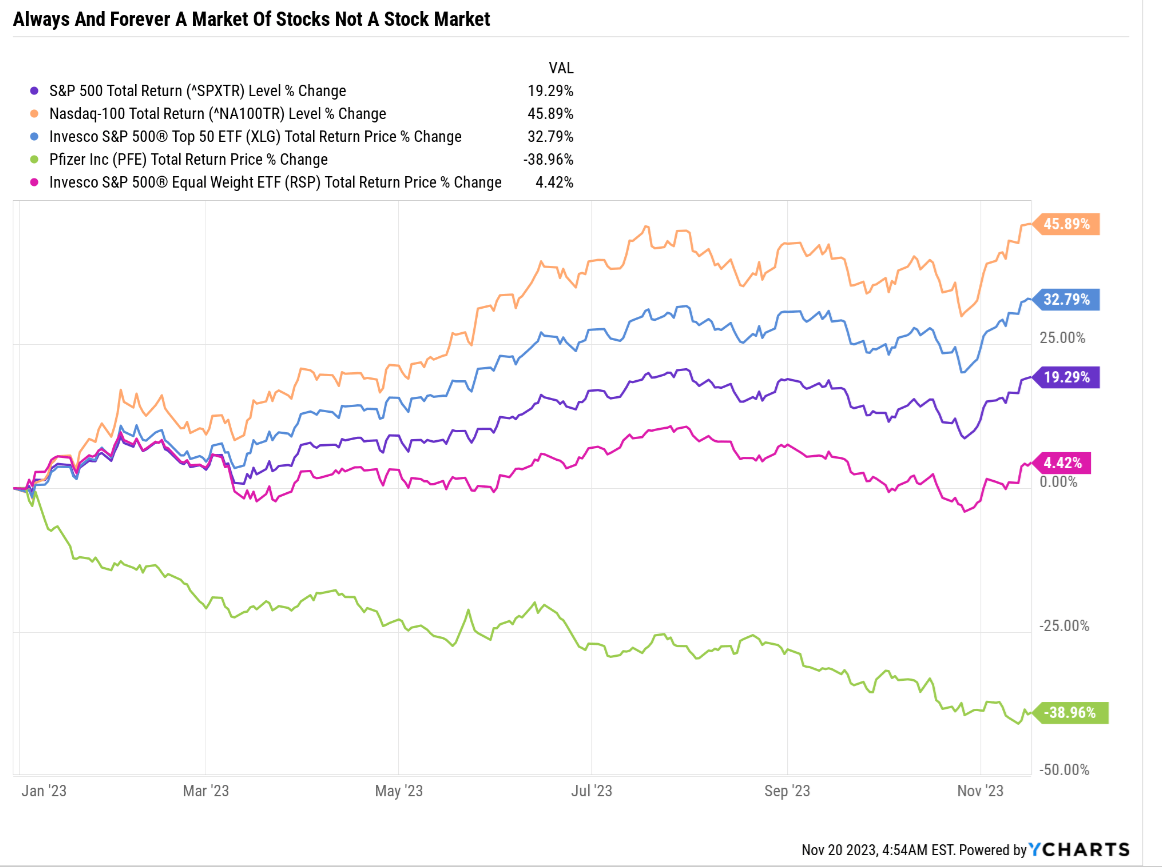

The market is red hot this year…or is it?

YCharts

The S&P 500 (SP500) is up almost 20%, and the Nasdaq 100 (NDX) almost 50%. But in reality, the S&P equal weight is only up 4%.

It’s the S&P 7, while the S&P 493 is flat.

This year, the only thing working well is mega-cap tech.

Pfizer Inc. (NYSE:PFE) is a great example of how it’s always and forever a market of stocks, not a stock market.

PFE is down 40% YTD and has been cut in half off of Pandemic highs.

YCharts

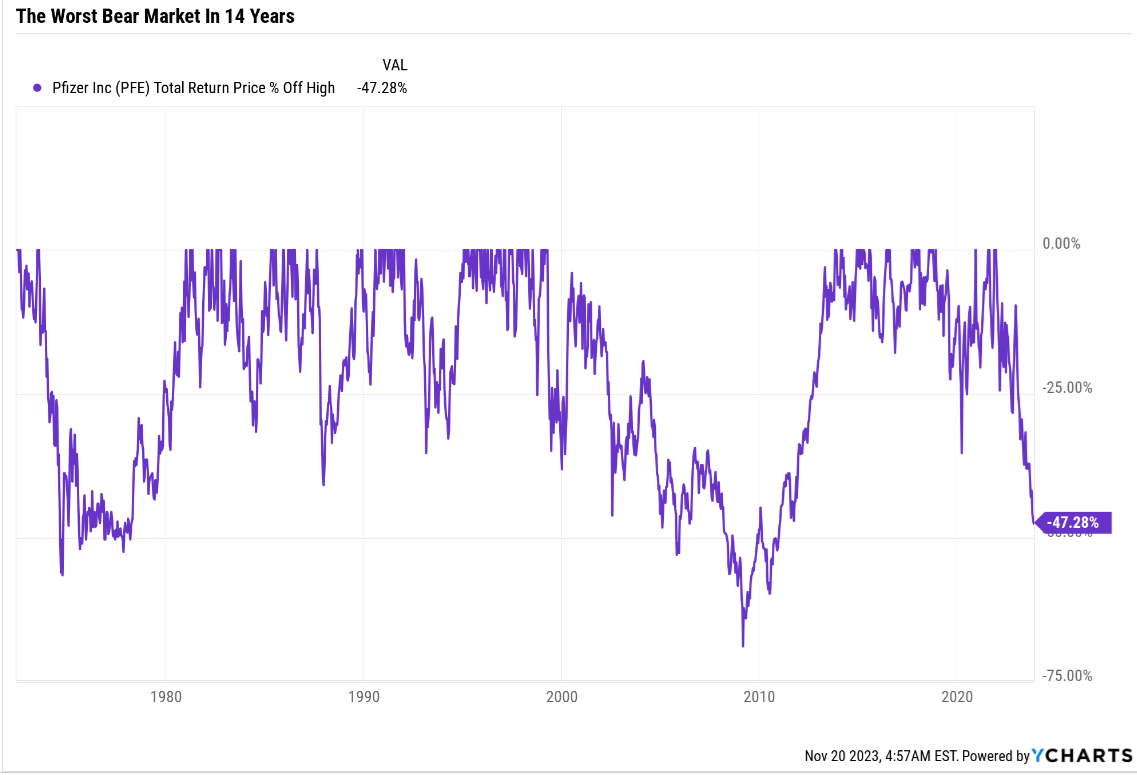

Why? Was PFE in a massive bubble in recent years? Is the highest yield in 14 years a sign of a value trap? Or the best buying opportunity in a generation?

YCharts

Here’s a short update on why Pfizer isn’t broken, is a potentially screaming buy…but if you don’t like its risk profile, how to find 9%-yielding blue-chip bargain alternatives that offer more than 4X the superior long-term return potential.

The Perfect Storm Of Negative Growth Headwinds

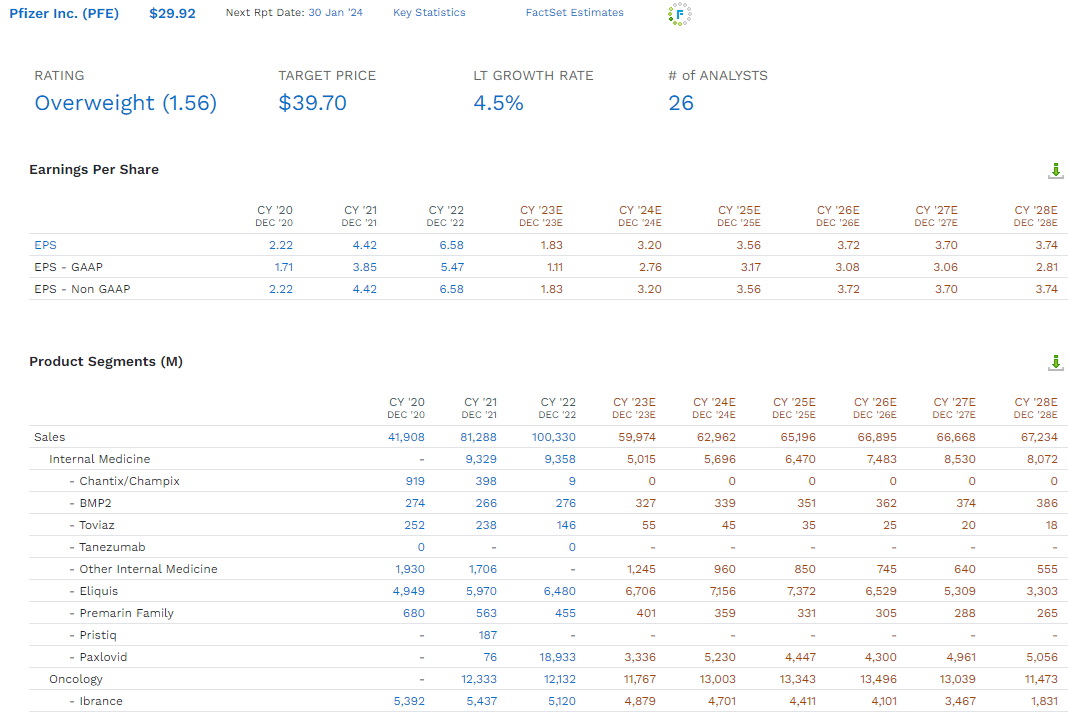

During the Pandemic, thanks to the COVID-19 vaccine, Pfizer’s earnings grew 196% in two years. Tripling your earnings in 2 years is 73% annual growth, and most start-ups struggle to achieve that. Never mind a company with $13 billion in 2020 net income.

FactSet Research Terminal

The Covid Vaccine is called Comirnaty.

$38 billion in peak annual sales is a record for any drug in history.

This is still expected to generate $7 billion in annual sales or more going forward, but compared to $38 billion? You can see why Wall Street is a bit upset with Pfizer’s results.

But Pfizer’s bear market isn’t just about earnings falling 76% in 2023.

FactSet Research Terminal

Long-term analysts expect Pfizer to grow 4% to 5% per year—Moody’s estimates the entire industry will grow earnings by 4% annually.

So, if Pfizer is expected to grow slightly faster than average, why all the hate from investors?

It comes down to the patent cliffs Pfizer is facing in the next few years.

Ibrance is a breast cancer drug that had $5.5 billion in peak sales in 2021 but has a patent cliff of 2027. By the next year, sales of Ibrance are expected to fall to $1.8 billion.

Eliquis is a joint venture heart drug Pfizer developed with Bristol-Myers (BMY) that is expected to see peak sales of $7.4 billion in 2025. And then a 2026 patent cliff means sales by 2028 are expected to fall to $3.3 billion.

The Comps Have Never Looked Worse For Pfizer

Let’s not forget what is taking Wall Street by storm this year.

- AI and GLP-1 obesity drugs.

Look at some of these analyst consensus estimates for obesity drugs.

- Mounjaro (LLY): $20 billion in 2028 sales (2036 patent cliff)

- Wegovy (NVO): $16 billion in 2028 sales (2031 patent cliff)

- Ozempic (NVO too): $21 billion in 2028 sales (2031 patent cliff).

What to do when all Wall Street wants is obesity drugs and Pfizer’s GLP1 drug is an oral medication that hasn’t been approved for obesity and isn’t as effective at rapid weight loss?

Just take a look at Pfizer’s medium-term EPS forecasts.

- 2022: $6.58

- 2023: $1.83

- 2024: $3.20

- 2025: $3.56

- 2026: $3.72

- 2027: $3.70

- 2028: $3.74

That’s 4% EPS growth from 2024 to 2028. Industry average…in a world where Eli Lilly and Novo Nordisk are expected to deliver the following earnings growth.

- LLY 2024 to 2028 EPS growth: 142% (25% annually)

- NVO 2024 to 2028 EPS growth: 78% (16% annually).

Pfizer’s 4% annual growth looks pretty unimpressive compared to the 16% to 25% growth LLY and NVO are expected to deliver.

But is there actually anything wrong with Pfizer’s dividend safety or fundamentals? Nope. The best available data says the company is just fine.

Fundamentals Summary

- yield: 5.5% (3X S&P 500 and above SCHD or VYM)

- dividend safety: 78% safe (2.3% dividend cut risk)

- overall quality: 82% low-risk SWAN

- credit rating: A+ negative outlook (0.6% 30-year bankruptcy risk)

- S&P LT Risk management global percentile: 70th = low risk (good risk management)

- long-term growth consensus: 4.5%

- long-term total return potential: 10.0% vs 10.2% S&P 500

- Current Price: $29.92

- Fair Value: $41.66

- discount to fair value: 28% discount (potential good buy) vs 11% overvaluation on S&P

- 10-year valuation boost: 3.3% annually

- 10-year consensus total return potential: 5.5% yield + 4.5% growth + 5.4% valuation boost = 13.3% vs 9% S&P

- 10-year consensus total return potential: = 249% vs 137% S&P 500.

FAST Graphs, FactSet

Yes, Pfizer is expected to recover strongly from the epic collapse in the pandemic COVID vaccine boom.

However, some people don’t want to own pharmaceutical companies because of the specific risk profile of the industry, including patent cliffs and government regulatory risk. So here’s how to find much better 9% yielding alternatives that offer 50% better long-term return potential with equal or better quality and dividend safety.

How To Find 9% Yielding Alternatives To Pfizer Video

Here is how I have used our DK Zen Research Terminal to find the best 9% yielding alternatives to Pfizer.

From 505 stocks in our Master List to the best blue-chip aristocrat bargains.

All in one minute, thanks to the DK Zen Research Terminal. This is how I find all my investment ideas.

| Screening Criteria | Companies Remaining | % Of Master List | |

| 1 | Blue-Chip Quality (10, 11, 12, and 13 quality scores) | 467 | 93.40% |

| 2 | BHS Rating “reasonable buy, good buy, strong buy, very strong buy, ultra value buy” | 345 | 69.00% |

| 3 | Non-Speculative (No Turnaround Stocks, investment grade) | 303 | 60.60% |

| 4 | 5.5+% Yield | 31 | 6.20% |

| 5 | 11+% Long-Term Return Potential | 18 | 3.60% |

| 6 | 5 highest yielding PFE alternatives | 5 | 1.00% |

| Total Time | 1 minute |

9% Yielding Blue-Chip Alternatives To Pfizer

Bottom line up front on these Pfizer alternatives.

Fundamentals Summary

- yield: 8.9% (5X S&P 500 and above SCHD or VYM)

- dividend safety: 85% safe (1.8% dividend cut risk)

- overall quality: 84% low-risk SWAN

- credit rating: A+ negative outlook (0.6% 30-year bankruptcy risk)

- S&P LT Risk management global percentile: 60th = low risk (above-average risk management)

- long-term growth consensus: 5.5% vs 4.5% Pfizer

- long-term total return potential: 14.5% vs 10.2% S&P 500

- discount to fair value: 34% discount (potential very strong buy) vs 11% overvaluation on S&P

- 10-year valuation boost: 4.2% annually

- 10-year consensus total return potential: 8.9% yield + 5.5% growth + 4.2% valuation boost = 18.7% vs 9% S&P

- 10-year consensus total return potential: = 455% vs 137% S&P 500.

And here they are with links to articles with more information and their consensus two-year return potential.

S&P 500

FAST Graphs, FactSet

The S&P offers a 20% upside over the next two years if earnings grow as expected (recession risk makes that unlikely) or 9% per year.

These 9%-yielding blue-chip bargains offer 84% two-year return potential or 31% yearly.

4X the market’s return potential in the short term, with 5X the very safe yield.

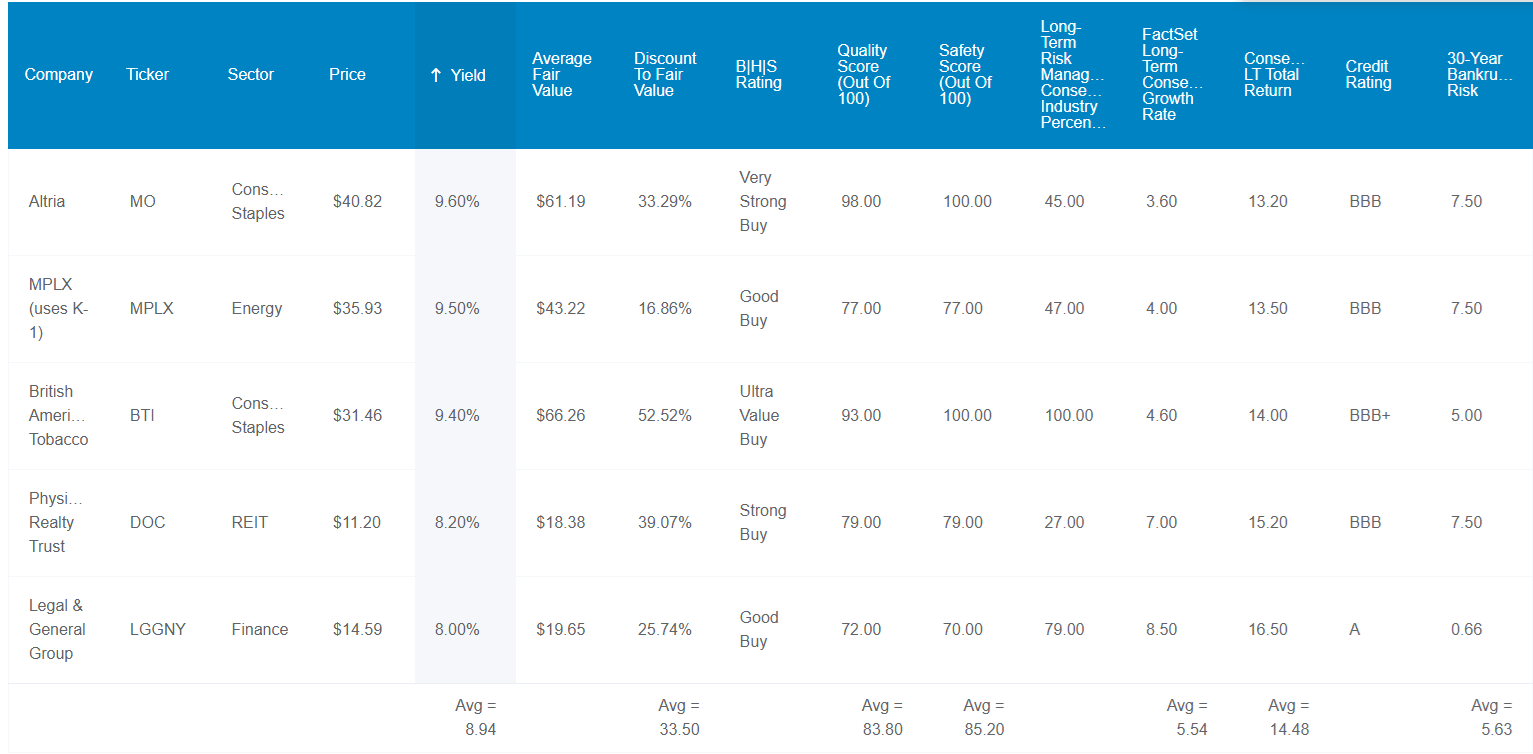

Dividend Kings Zen Research Terminal

- Altria Group (MO)

- MPLX (MPLX) – K1 tax form

- British American Tobacco (BTI)

- Physicians Realty Trust (DOC)

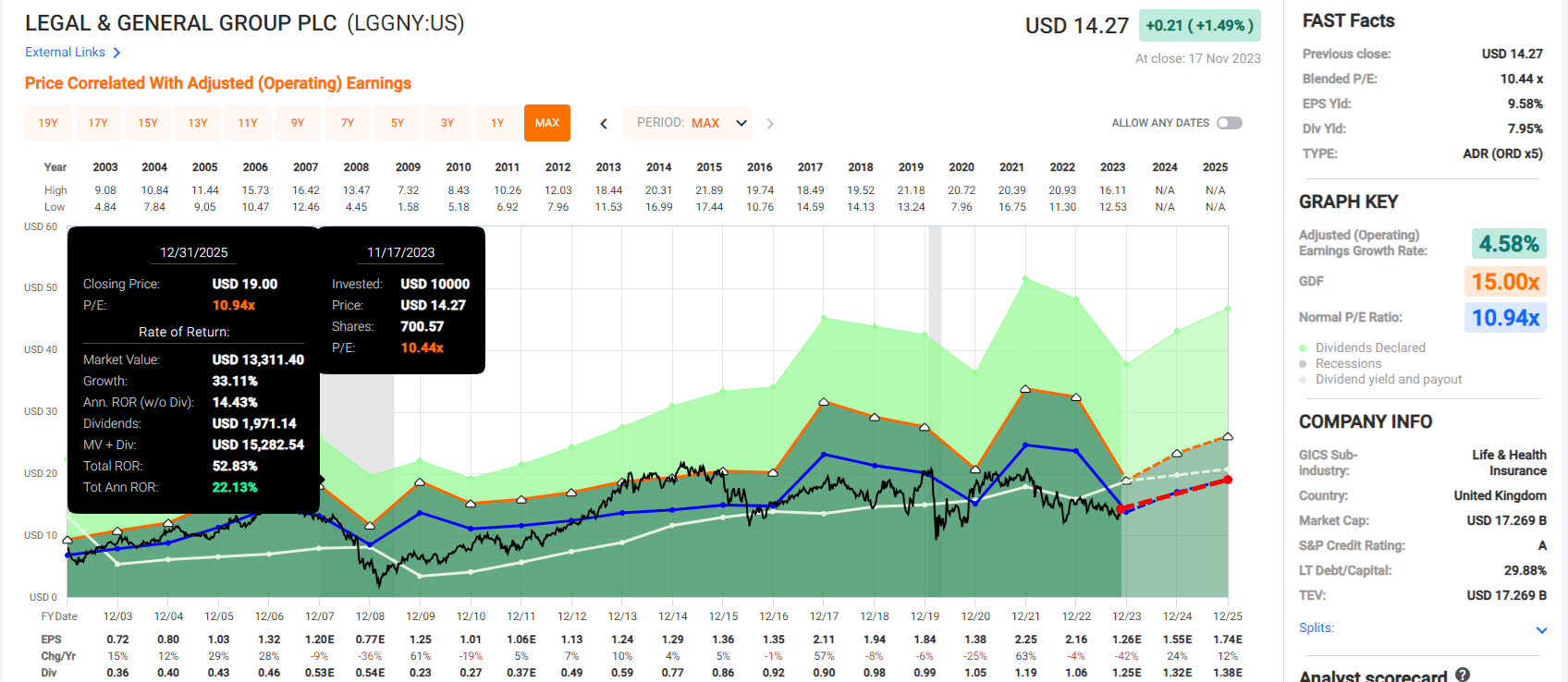

- Legal & General Group (OTCPK:LGGNY).

Consensus Total Return Potential Through 2025

- if and only if each company grows as analysts expect

- and returns to historical market-determined fair value

- this is what you will make.

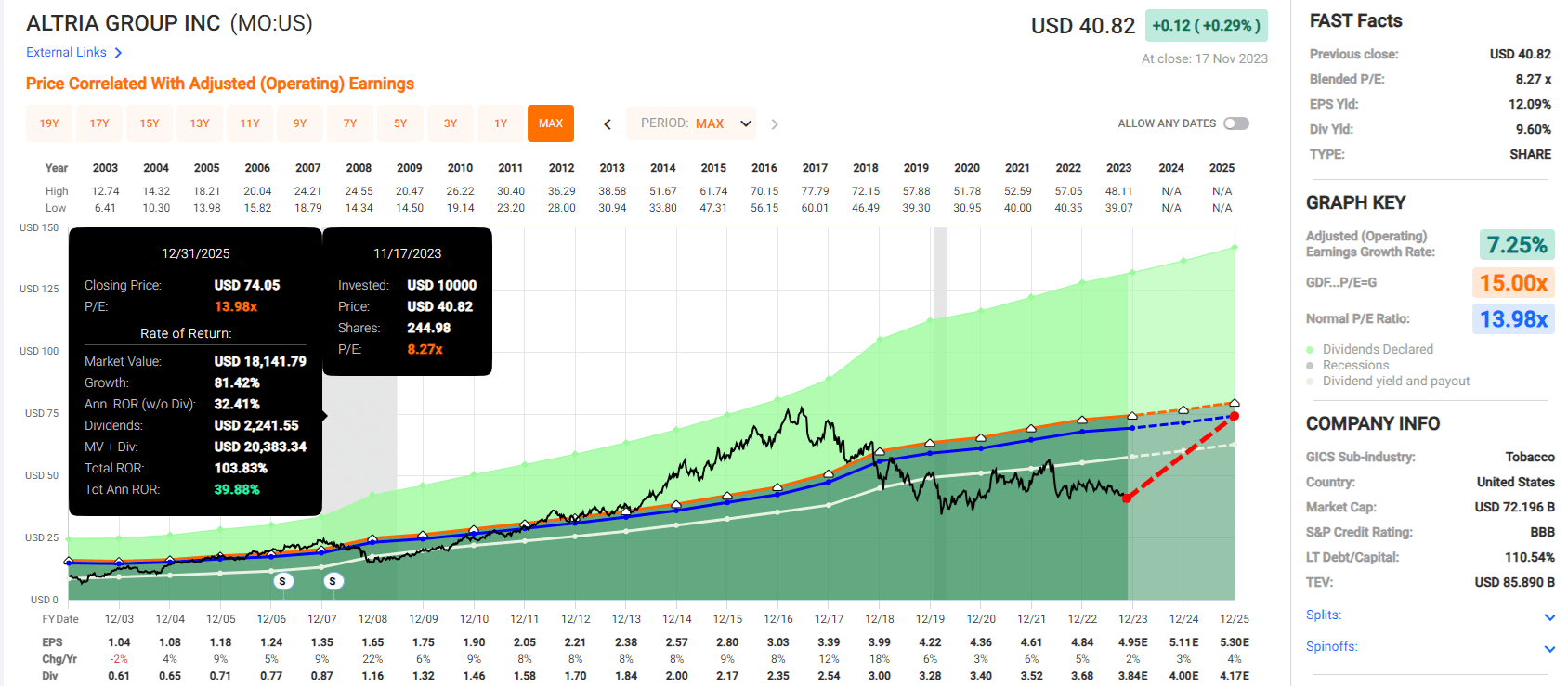

Altria

FAST Graphs, FactSet

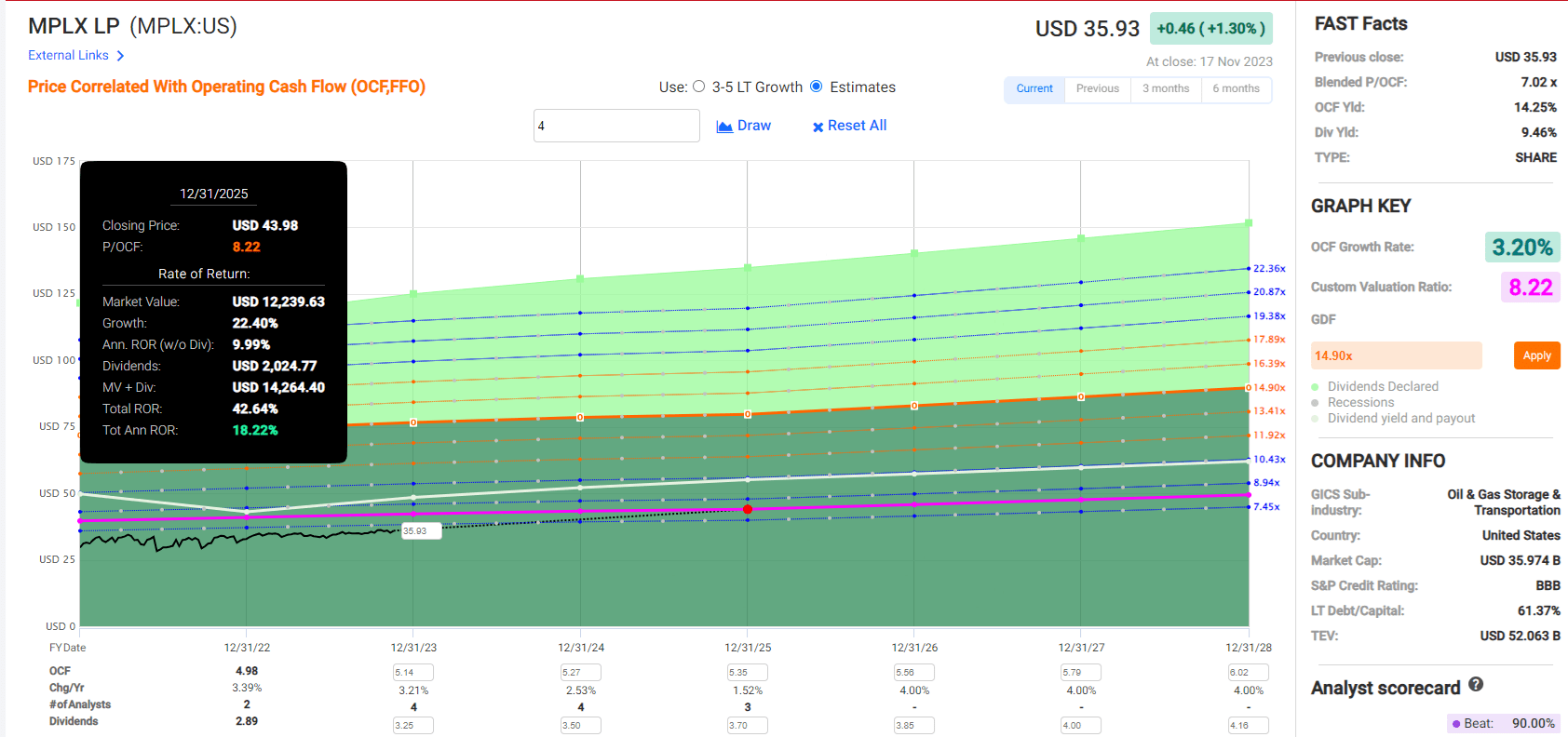

MPLX

FAST Graphs, FactSet

British American

FAST Graphs, FactSet

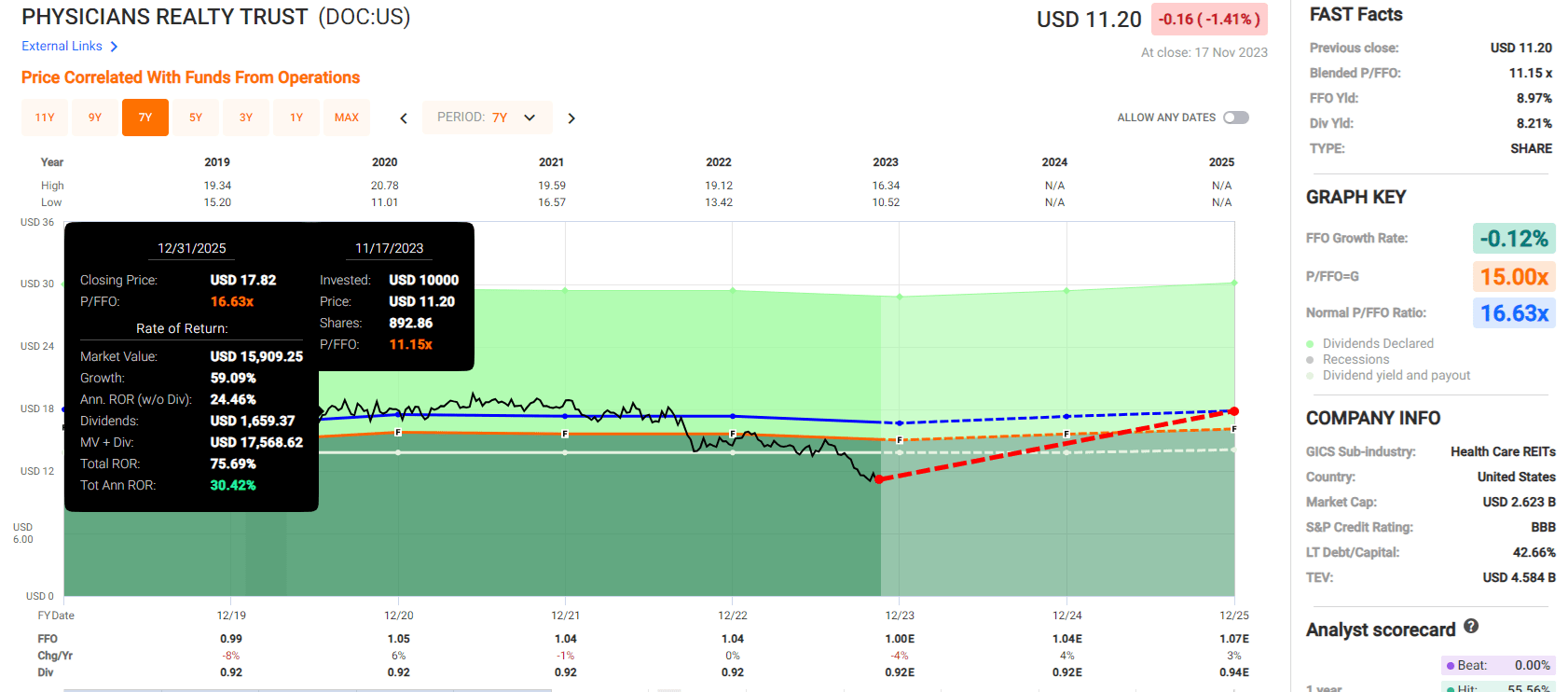

Physicians Realty Trust

FAST Graphs, FactSet

Legal & General

FAST Graphs, FactSet

S&P 500

FAST Graphs, FactSet

The S&P offers a 20% upside over the next two years if earnings grow as expected (recession risk makes that unlikely) or 9% per year.

These 9% yielding blue-chip bargains offer 84% two-year return potential or 31% yearly.

4X the market’s return potential in the short-term, with 5X the very safe yield.

Bottom Line: It’s The Best Time In 14 Years To Buy Pfizer, But Consider These 9% Yielding Alternatives

Pfizer is a wonderful company, and they save lots of lives. In fact, they likely saved millions or possibly tens of millions of people in the Pandemic.

If you’re a fan of Pfizer’s business, it’s the best time in 14 years to buy this company.

If you’re not thrilled by the complex risk profile, including regulatory risk, patent cliffs, and new drug development risk, consider MO, MPLX, BTI, DOC, and LGGNY as faster-growing 9% yielding blue-chip bargains.

With almost double the very safe yield and 1% faster growth than Pfizer is expected to deliver long-term, these five blue-chip bargains offer about 50% superior long-term returns.

- 332% better 30-year inflation-adjusted total return potential

Morningstar Morningstar

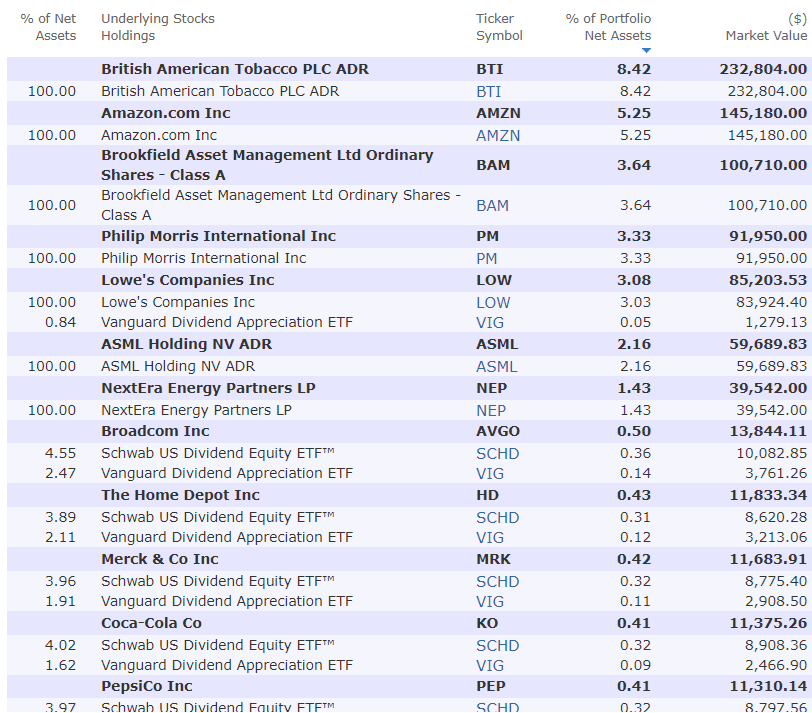

I own about $8,000 worth of Pfizer via ETF and I’m happy to own them. But if I could afford to buy anything right now (family medical emergencies), I would go with BTI as the best risk-adjusted ultra-yield investment opportunity.

BTI is my biggest stock holding and I’m sleeping very well at night.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of BTI either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

—————————————————————————————-

Dividend Kings helps you determine the best safe dividend stocks to buy via our Automated Investment Decision Tool, Zen Research Terminal, Correction Planning Tool, and weekly screening videos.

Membership also includes

-

Access to our 13 model portfolios (all of which are beating the market in this correction)

-

my family’s $2.5 million charity hedge fund

-

50% discount to iREIT (our REIT-focused sister service)

-

real-time chatroom support

-

real-time email notifications of all my retirement portfolio buys

-

numerous valuable investing tools

Click here for a two-week free trial, so we can help you achieve better long-term total returns and your financial dreams.