Summary:

- For 1Q25, PG generated $21.7 billion in revenue, declining by 0.61% year-on-year and missing estimates by $239.84 million. Net margin deteriorated to 18.22% from 20.67% due to higher non-operating expenses.

- Despite a poor consumer environment, organic sales surged by 2%. Recent trends in disinflation and strength in retail sales will continue to serve as tailwinds, supporting demand for PG’s products.

- Other factors such as productivity gains, weakening dollar, and growth in under-represented markets will provide PG with more opportunities to enhance the company’s bottom line.

- Valuation analysis suggests that further upside potential exists. DCF based valuation model suggest a potential upside of at least 18%.

RobsonPL

Introduction

Protect & Gamble (NYSE:PG) is on the world’s largest consumer goods companies and owns iconic household brands such as Gillette, Oral B, Pantene, Vicks and more. The company currently has more than 107k full-time employees and sells their products to more than 180 countries and territories.

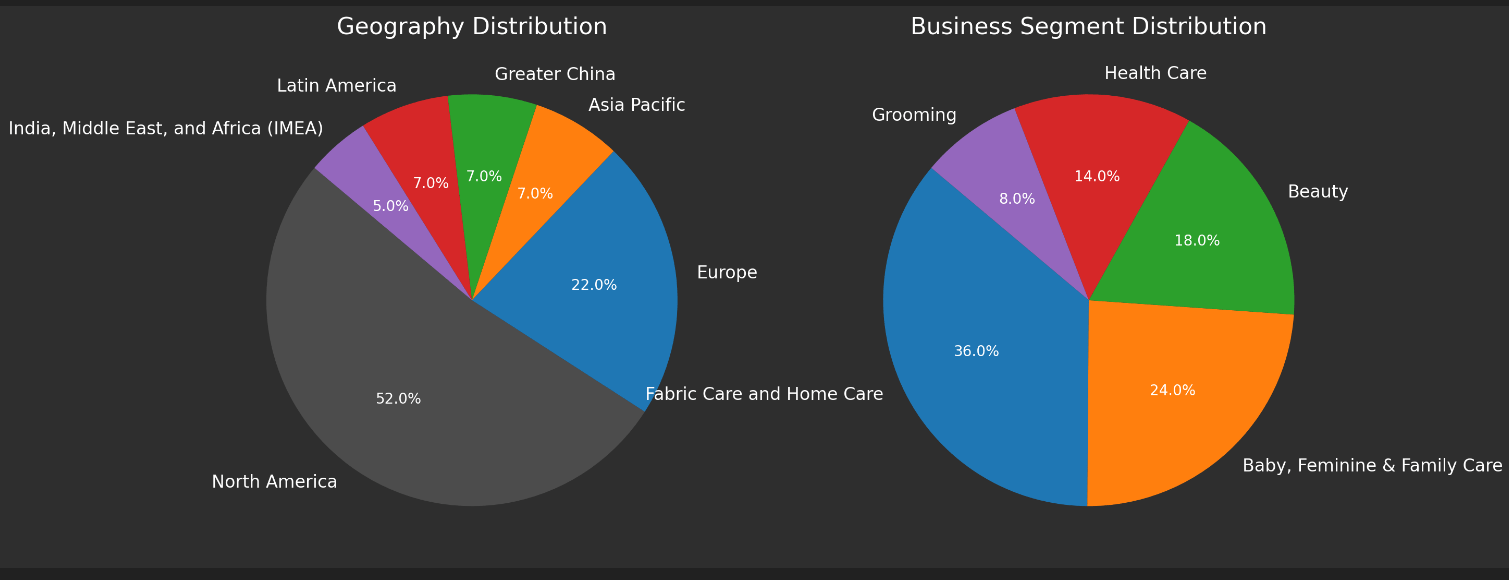

P&G’s Revenue Breakdown By Geography & Business Segment (Company Website, Author Illustration)

PG reports its sales through five segments: (1) Beauty, (2) Grooming, (3) Health Care, (4) Fabric & Home Care, and (5) Baby, Feminine, and Family Care. Baby, Feminine, and Family care represents the biggest segment, contributing at least 36% and 34% of the company’s sales and net income. PG distributes its items through e-commerce channels, mass merchandisers, drug stores, department stores; top ten customers account for more than 40% of the company’s net sales but no single customer represents more than 10% of total sales.

P&G’s Brands & Product Categories (Company Filings)

Although PG had already surged more than 12% this year, my analysis suggests that there will be further upside potential for investors. Global disinflation, productivity gains, potential growth in underpenetrated markets, and the weakening of the dollar will continue to support PG’s operating performance substantially. In this report, I will demonstrate why investors should consider PG as part of their portfolio.

Latest Development

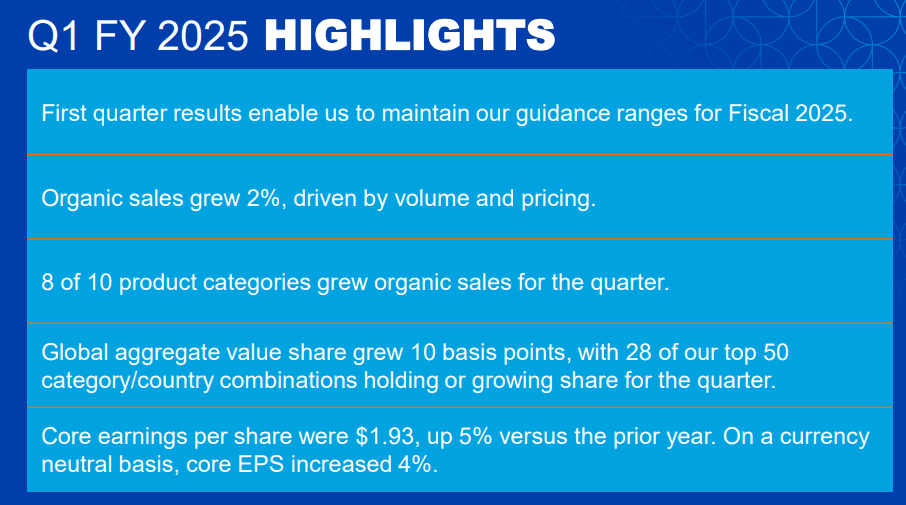

For 1Q25, PG’s generate $21.7 billion in revenue, declining by 0.61% year-on-year and missing estimates by $239.84 million. Due to higher non-operating expenses such as restructuring charges, PG posted a lower net margin of 18.22% as compared 20.67% last year.

1Q25 Highlights (Earnings Presentation)

Looking forward into the rest of FY2025, PG expects organic sales to range between 3% to 5%. Capital expenditures is expected to be within 4% to 5% of total sales while effective tax to range between 20% and 21%. In terms of cashflows, the company expects to achieve a FCF productivity of 90%.

Global Disinflation Will Continue Serve As Tailwinds

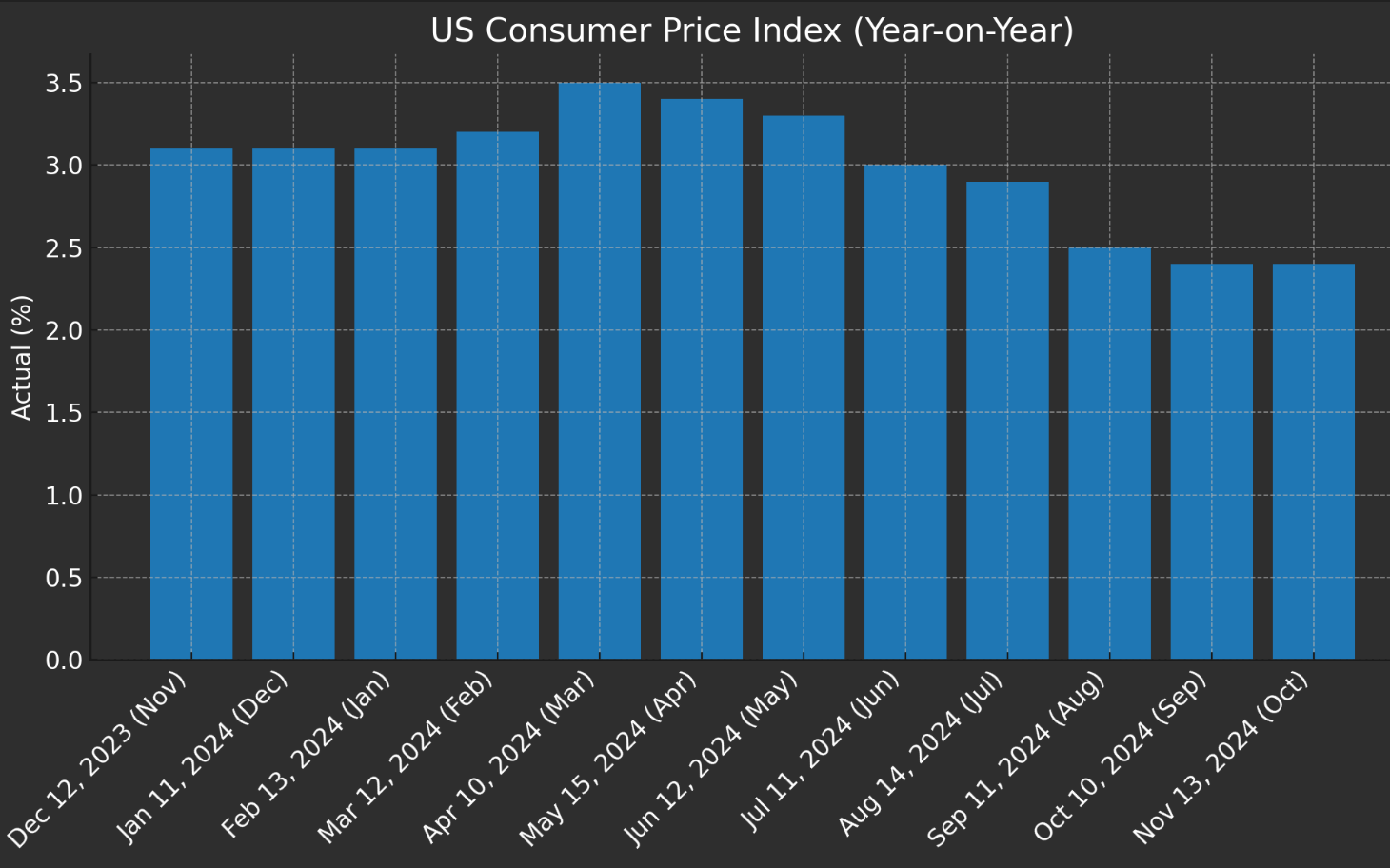

Overall although PG’s net revenue has fell, organic sales increased by 2% despite a high growth of 7% in 1Q24, highlighting that company’s resilience in a poor macroeconomic environment. PG continue to see sustained sales growth in the grooming, healthcare and fabric and homecare segment, increasing by 3%, 4% and 3% year-on-year respectively. In the baby, feminine, and family care segment, organic sales remain flat; in the more discretionary beauty segment, organic sales deteriorated by 2% year-on-year.

According to a recent consumer survey, Upside found that many consumers believe that the economy is worse than before. At least 58% of the consumers indicated that they have reduced spending and 89% stated that they are relying more on discounts and promotions. Given that overall consumer sentiment remains weak, PG’s ability to sustain growth is impress. More importantly, PG engages in the sale of daily necessities. As Andre Schulten, Chief Financial Officer of PG, highlighted in the latest earnings call, “Consumers don’t stop washing their hair, they don’t stop doing their laundry”, regardless of the macroeconomic environment.

US Consumer Price Index (YoY) (Investing.com, Author’s Illustration)

Looking forward, we should expect overall retail sales across the world to improve due to continued disinflation, indicating further tailwinds for PG. In addition, according to the EIU, world retail sales will remain robust for the rest of 2024 and 2025; global retail sales volume expect to grow 2.1% and 2.2% for 2024 and 2025. In terms of gross global retail sales, EIU expects a growth of 5.3% and 6.8%.

Enhanced Profitability Through Underpenetrated Markets, Productivity Gains, and Weakening Dollar

Although PG’s business has largely mature, the company still sees multiple opportunities for growth, allowing PG to possibly beat estimates. According to PG, these underpenetrated markets represents a $5 billion potential growth opportunity in the United States alone. For context, $5 billion represents about 6% of the company’s FY2024 revenues.

Currently, PG is focusing on multiple consumer groups where it is still underpenetrated, providing opportunities for PG to further expand and capture additional revenues. For example, household penetration on liquid fabric enhancer and laundry beads is only about 30% and 20% respectively. In addition, oral care presents another growth opportunity that is currently underpenetrated. As compared to other segments where growth is in the low single digits, PG’s oral care business has increased by 8%.

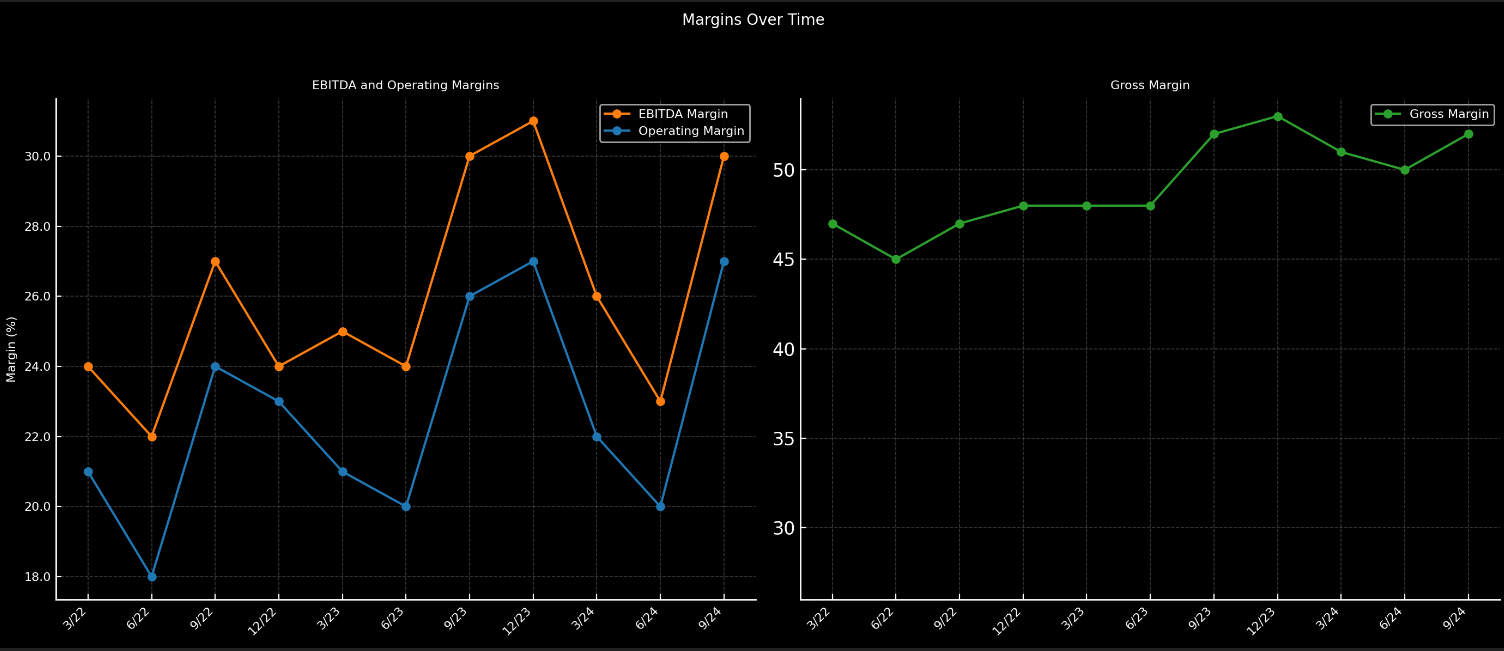

P&G Margins Over Time (Company Filings, Author’s Illustration)

Apart from additional growth opportunities, PG’s focus on optimizing its cost is likely to continue benefiting investors through margin expansion. In the past three quarters, margins have deteriorated significantly; however, PG has managed to improve its margins by optimizing costs and enhance productivity gains. According to the latest earnings call, PG achieved productivity gains of more than 230 basis points. As percentage of revenues, PG managed to reduce its COGs and SG&A by 219 bps and 524 bps respectively on a sequential basis. For reference, a 100 bps saving represents $217 million.

Finally, close to half of PG’s sales is outside of North America. We have already reached the peak of inflation and elevated interest rates. Recently, the US Fed had reduced interest rates by another 25 bps; currently the Fed Fund Rate is between 4.5% to 4.75%. By mid-2025, markets are expecting US to further reduce rates to about 4.00%. Although interest rates will remain elevated, it is likely that the US Fed will continue continues reducing rates in an effort to prop up the economy, resulting in a weakened dollar but highly beneficial to PG’s overall revenues.

Commitment To Returning Value to Shareholders

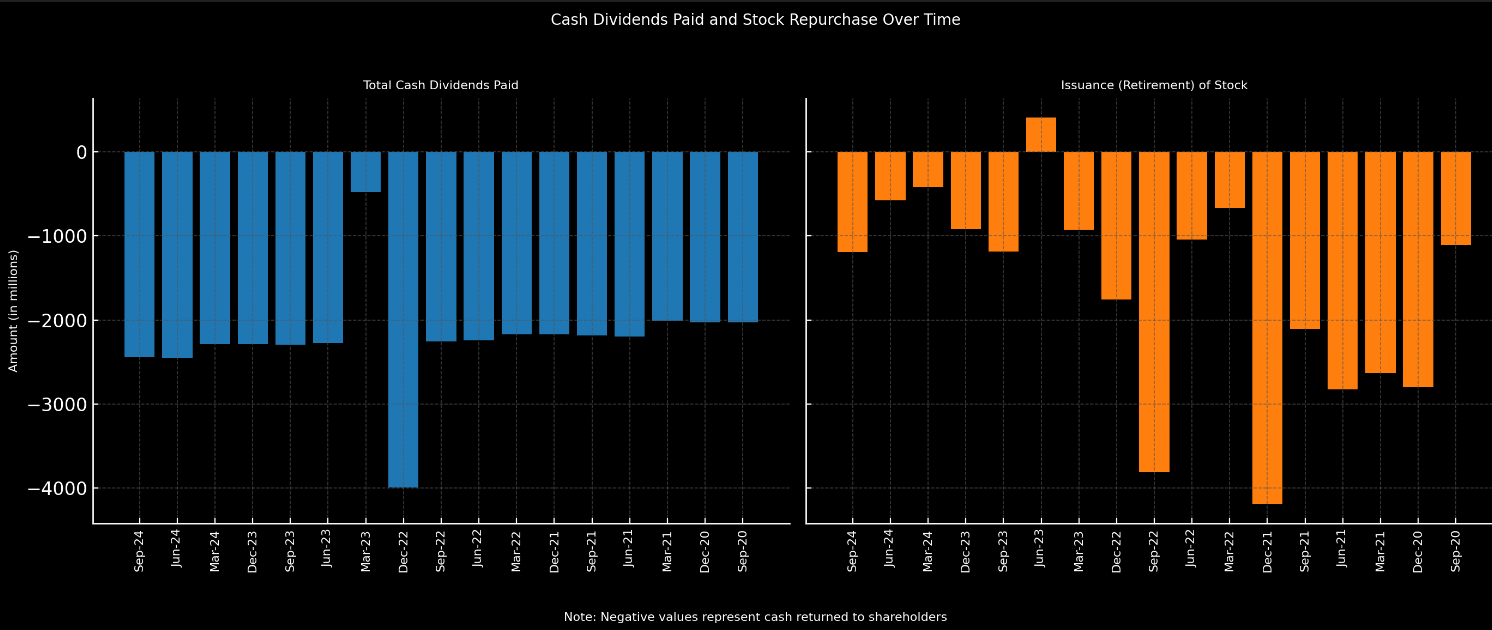

More important to shareholders, PG remains committed to return value. In the past four quarters, PG has returned approximately $12 billion to shareholders through dividends and stock repurchases. In the latest quarter, the company returned $4.4 billion through $2.4 billion in dividend payments and $1.9 billion in share repurchases.

P&G’s Cash Dividends & Share Repurchases Over Time (Company Filings, Author’s Illustration)

Looking forward, PG expects to pay around $10 billion in dividends and to repurchase up to $6 billion of common shares in FY2025. Investors can expect a reduction of total shares outstanding by approximately 4% based on the current market capitalization of $394 billion.

Valuation Analysis Suggests Further Upside Potential

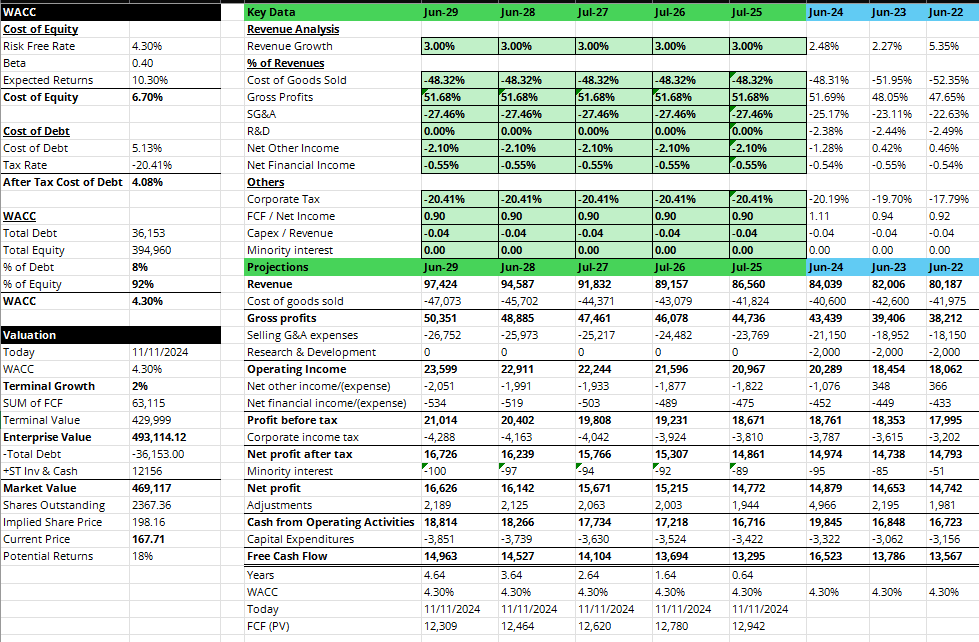

Based on the following assumptions: (1) PG to maintain a revenue growth of 3%, in-line with its guidance, (2) maintain its currently expanded margins, (3) shares outstanding of 2.37 billion representing a 4% potential reduction through share repurchase, and (4) a terminal growth of 2% and WACC of 4.3%, my DCF valuation model suggests that the implied share price of PG is $198.16, representing a potential upside of 18%.

P&G’s Valuation Analysis (Author’s Projection)

It is important to note that these are conservative estimates. If PG is able to accelerate its growth in the underpenetrated markets, maintain all of its current margins, and consistently achieve a growth of merely 5% in the next five years, the model suggests that there will be a potential upside of at least 30%.

Closing Remarks

Overall, although PG has surged 12.75% year-to-date, my valuation model suggests further upside for investors. Apart from global disinflation, other factors such as the weakening dollar, PG’s focus on margin optimization, and potential growth in underpenetrated market will continue support the resilience of PG.

That being said, investors should closely monitor the developments relating to consumption in the Middle East and China. Although these regions represents a relatively smaller market for PG, performance in these two regions represents PG’s greatest risk. Currently, PG is already facing revenue decay in these regions; PG cited continued volatility in the Middle East and a 15% decline in China. Any further deterioration in sales from these regions may affect PG’s target for FY2025.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, but may initiate a beneficial Long position through a purchase of the stock, or the purchase of call options or similar derivatives in PG over the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.