Summary:

- Qifu Technology is a Chinese Credit-Tech firm that provides digital lending services to consumers and SMEs.

- Q2 2023 results showed a decline in revenue but an increase in net income, leading to a restrained stock market response.

- The company’s long-term growth outlook is positive, with projections for the Chinese consumer credit tech market to grow.

goc/E+ via Getty Images

Thesis Summary

Qifu Technology, Inc. (NASDAQ:QFIN) is a Chinese based Credit-Tech firm. It’s a digital lending company that provides accessible and personalized credit services to consumers and SMEs. Qifu Technology utilizes big data, machine learning, and AI to streamline its target audience’s decision-making process. Its consumer-based target audience comprises young urban Chinese professionals doing white-collar jobs.

The company recently announced its Q2 2023 results. Results were slightly disappointing as its revenue was lower than last year’s quarter. Due to this, the QFIN stock didn’t surge much. The global digital lending market is increasing yearly, so investors are likely optimistic about the company, and the stock hasn’t declined heavily.

In my last article on QFIN, I talked about how the company had become a profitable enterprise over time and traded at a favorable valuation. Though growth has slowed since then, the company has continued to deliver shareholder value.

On top of that, China’s recent commitment to monetary and fiscal stimulus could pave the way for a renewed surge in consumer lending.

Q2 2023 Highlights

On August 21, 2023, the company announced its second-quarter results. As soon as the news of its results hit the stock market, its stock slightly surged. Even though the company saw a decline in revenue year over year, its net income increased. Its revenue missed the estimates, but investors appear to be betting on the company’s net income and increased customer base.

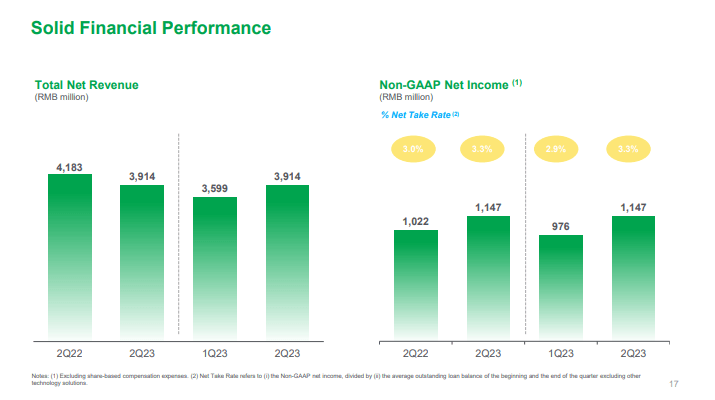

The company announced its revenue was RMB3,914.3 million or US$539.8 million, slightly lower than RMB4,183.2 million in the same period last year. On the contrary, its net income surged slightly to RMB1,093.4 million or US$150.8 million, compared to RMB975.0 million in the same quarter last year. At the end of the quarter, the company had around RMB8.5 billion in cash and cash equivalents and generated around RMB1.8 billion in cash from operations. The company is dedicated to delivering value to shareholders. QFIN announced a 20-30% dividend payout and a $150 million share repurchase program.

Revenue and Income (Investor slides)

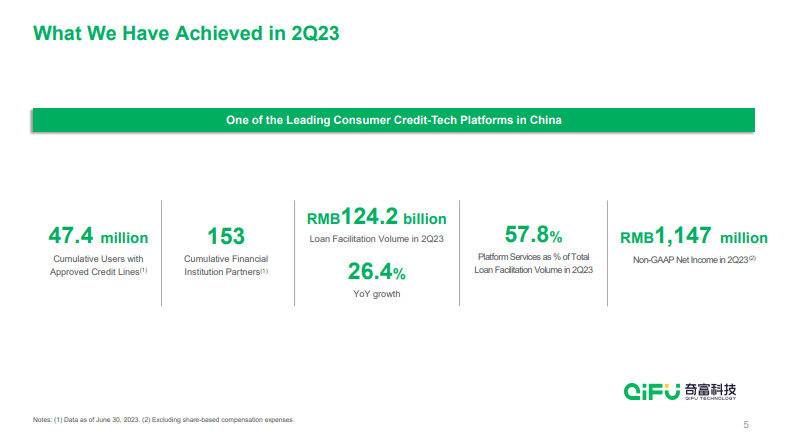

If we look at the company’s operations, it achieved significant milestones. They have connected over 153 financial institutional partners and 220.6 million consumers, surging 11.5% from 197.9 million 12 months ago. In Q2, its total facilitation and origination loan volume reached RMB 124,225 million, a significant increase of 26.4% from last year, with 47 million users having approved credit lines.

Q2 achievements (Investor slides)

Growth Outlook

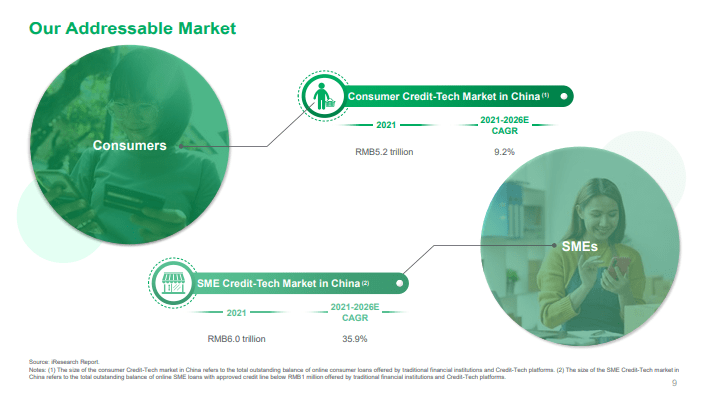

According to the company, China’s consumer credit tech market in 2021 was RMB 5.2 trillion and is expected to grow at a CAGR of 9.2% between 2021 and 2026. Similarly, the SME Credit-Tech market of China in 2021 was RMB 6 trillion and is expected to grow 35.9% between 2021 and 2026. Looking at these estimates, the company has projected some long-term goals.

Addressable market (Investor slides)

Though the Chinese economy has no doubt faced a significant slowdown, the next few quarters could see some recovery as both the PBoC and the government begin to ease conditions.

Back in August, the PBoC surprised investors with a rate cut, and signalled that it would begin easing conditions. Though pre-mature, we already have some evidence this is working. New bank loans jumped more than expected in August.

To top things off, Beijing is now considering fiscal stimulus of around $137 billion, which could help boost the economy even further,

With all of this, I believe there are some reasons to believe the Chinese consumer could surprise us in the next year, and QFIN would be one of the primary beneficiaries.

Valuation

QFIN stock has been on a roller coaster ride since it announced its Q2 results. This irregular pattern can be explained by the declining revenue.

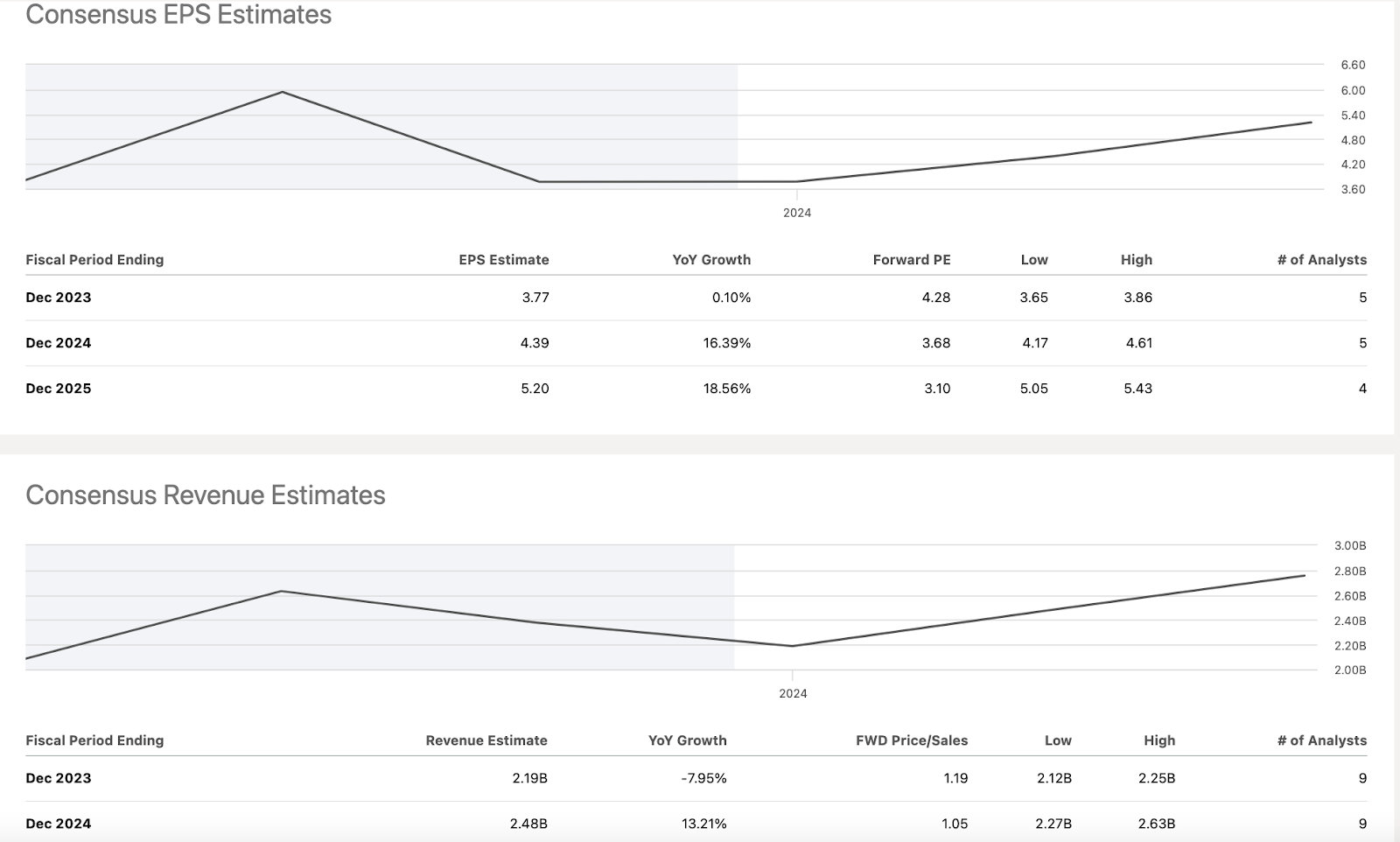

Its EPS is estimated to be approximately $3.77, with a modest growth of 0.10% YoY in FY23. In FY24, it is expected to surge by 16% to $4.39. Similarly, in FY25, its EPS is estimated to reach $5.20 with an estimated YoY growth of 18.5%.

EPS and Revenue estimates (SA)

On the other hand, its revenue is expected to take a slight blow, declining by 8% to $2.19 billion in FY23. But in FY24, revenue is expected to surge by 13.21% to reach $2.48 billion.

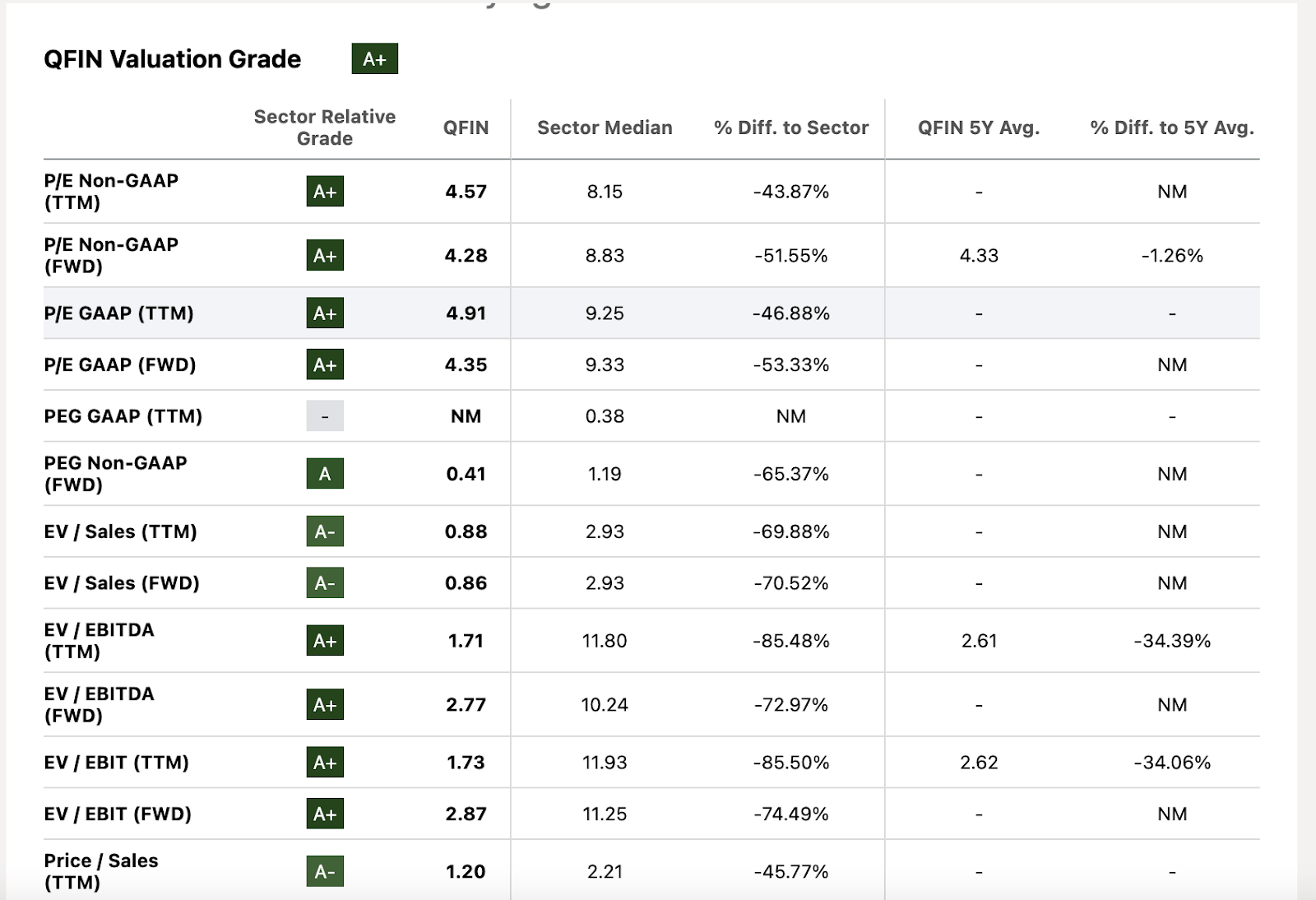

QFIN stock’s valuation metrics appear quite favorable. QFIN’s Non-GAAP P/E ratios are 4.57 (‘TTM’) and 4.28 (‘FWD’), and its GAAP P/E ratios are 4.91 (‘TTM’) and 4.35 (‘FWD’). These numbers are 44% to 53% lower than the sector median. It shows that QFIN might be priced lower concerning its earnings than its competitors.

QFIN’s forward PEG, based on non-GAAP earnings, stands at 0.41, which is 65.37% below the sector median. A low PEG suggests that this might be undervalued, especially when considering its potential for growth in future earnings.

QFIN’s EV-to-Sales ratios are 0.88 (‘TTM’) and 0.86 (‘FWD’), and its EV-to-EBITDA ratios are 1.71 (‘TTM’) and 2.77 (‘FWD’). These ratios are 70% to 85% lower than the sector median. This shows that, concerning its sales and earnings, QFIN’s entire value (including its debt and excluding its cash and cash equivalents) is considerably lower than its sector counterparts.

In summary, QFIN is undervalued compared to other stocks in its sector.

QFIN valuation (SA)

Risks

There are different types of risks attached to a digital lending company. These companies provide fast and short-term loans to borrowers with zero collateral. There is a potential risk that these borrowers could default on their loans. So, the primary challenge for Qifu Technology is to assess the financial standing of its customers, who are likely to avoid defaulting on their loans.

Furthermore, the regulatory authority could change its position on the legitimacy or tighten the rules for them as fast loans are considered bad and could create financial hurdles for the general populace. In such a scenario, a regulatory authority could make rules that are strict to follow and would create hurdles for the company to implement its business model efficiently.

Any cyberattack on its platform could harm its reputation, and its customers could lose trust in the company. It means that customers’ data will be compromised. Not only existing ones but also new customers will avoid their platform. So, their platform must be safe from any such attack.

Increased competition is also a major threat to the company as there are many players in the market. Their lucrative offers make the market more competitive, and the company has to improve its USPs to increase its relevance.

Other risks could be operational, fraud, and reliance on third-party systems. These risks could disrupt its business model. So, to operate in the digital lending space, the company has to address all these potential risks.

Conclusion

Qifu Technology, Inc.’s second-quarter results show a dichotomy. Its revenues declined, but on the other hand, its net income increased. This led to a restrained stock market response. The company’s expansive market strategy in the online loan space, combined with variables that suggest potential undervaluation compared to sector peers, paints a hopeful future. Combined with China’s support to the economy, this makes QFIN a compelling buy, in my view.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of QFIN either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

This is a high-risk/high-reward opportunity, which is exactly what I look for in my YOLO portfolio.

Joint the Pragmatic Investor today to get insight into stocks with high return potential.

You will also get:

– Weekly Macro newsletter

– Access to the End of The World and YOLO portfolios

– Trade Ideas

– Weekly Video