Summary:

- First TFLN photonic chip order from a major Asian institute shows strong signs of early demand for this technology prior to the commissioning of the Arizona foundry.

- TFLN chips could double data transmission speeds while reducing energy use, addressing surging demand from AI and quantum computing.

- Shareholder dilution remains a concern, especially if new orders lag. Competition from well-funded players like HyperLight could challenge market share if delays occur with the Arizona foundry commissioning.

- I see a massive upside if QCi secures additional contracts, making this a strong buy for high-risk, high-reward speculative investors, like myself.

- Am I off base here? Did I overlook anything? I’d love to hear your thoughts.

narong sutinkham/iStock via Getty Images

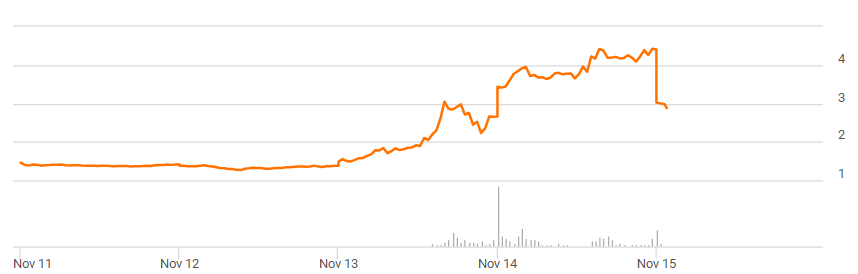

Quantum Computing Inc. (NASDAQ:QUBT) just made headlines with two major announcements that sent its stock soaring by close to 100% in the last 2 days.

seeking alpha

First, the company received its first order for photonic integrated circuits from its TFLN photonic chip foundry.

Adding to the momentum, QCi secured $40 million in a registered direct offering to support the completion of its TFLN foundry in Tempe, Arizona, set to begin production in early 2025.

Why does all of this matter?

Well, research points out that TFLN technology can transmit data at speeds at least twice as fast as traditional silicon chips, all while using much less energy.

I believe the potential of this technology is huge, given the growing data center demand from AI and quantum computing.

Therefore, in this article, I considered reviewing the implications of these two announcements to the future growth of the company, looking at both the broader market trends and the company’s core fundamentals.

I will also include a risk section to discuss the main challenges that the company is currently facing, including shareholder dilution, competition, and unstable revenue streams.

Overall, I see this stock as an asymmetric risk-reward opportunity. As a result, I purchased shares during the pullback following the market open on November 15.

What Caused The Rally?

On November 13, the company announced the first order for the thin film lithium niobate (TFLN) photonic chip foundry.

The press release didn’t disclose the name of the customer, aside from mentioning it is a prominent research and technology institute in Asia.

You might wonder why this announcement is relevant.

I’ll explain below in layman’s terms. However, I recommend consulting this source for full details on the TFNL technology.

Research shows that TFNL is turning out to be a groundbreaking material in the field of photonics. Again, to keep things clear, photonics is the technology behind fiber optic communication, sensors, and quantum computers.

Well, it turns out that this material is perfect for building superfast optical modulators, which can be used in data center applications to replace traditional semiconductor materials like silicon.

To put things into perspective, the operational limit of silicon semiconductors is 800 gigabits per second, while TFNL offers transmission rates up to 1.6 or 3.2 terabits per second.

For a no-nonesense, sub-blue collar Wall Street ex-pit trader, this means that data centers could use this new material to, at least, double their transmission rates. Source here.

Another advantage of TFNL is its ability to interact with light so efficiently that it significantly reduces energy consumption. Why is this a big deal?

As I’ve already mentioned in my previous article for Micron (MU), IEA’s projection for electricity consumption could double by 2026. Among the key drivers, data centers and quantum computing are at the top.

Therefore, aside from a performance perspective, there is a cost-saving argument to use this new material.

Let’s leave science class, and return back to finance.

According to the latest earnings report, QCi is in the final phase of commissioning its TFLN foundry in Tempe, Arizona.

This phase marks an important step in the company’s strategy to establish itself as a leading supplier of high-performance photonic integrated circuits and nanophotonic devices.

However, I have to mention that QCi faces competition in this field, which I will cover in the risk section of this article.

To be specific, the commissioning of the TFLN foundry is scheduled to be completed by the end of 2024, with production expected to start in early 2025.

Therefore, the pre-sale order from the leading Asian research institute is, in my view, a strong indication of demand for this material.

The scope of this order includes two fabrication runs for custom photonic chips. The first chips are to be delivered in December 2024, with the full order to be completed by the end of Q1 2025.

I anticipate the share price will rise further if the company secures more contracts before the end of the year.

Another factor that fueled the rally was the November 14 announcement of a registered direct offering of 16 million shares of common stock at $2.50 per share, generating $40 million in gross proceeds. This gives the company extra oxygen to complete the TFLN foundry and further expand if more customers place new orders. However, the share issuance had a negative side, which I’ll explain in the next section.

Risks

Let me be clear right off the bat: despite my strong buy rating, this stock is a highly speculative bet.

The main reason I rate it as a strong buy is due to its asymmetric reward potential, particularly with deep OTM call options, though owning shares reduces slightly the risk (at the cost of reduced reward potential).

So, here we have the first risk.

Before the announcement of the $40 million from the registered direct offering, the balance statement showed a net debt of $4.7 million.

In my view, considering the decent liquidity ratios of the company prior to the stock issuance (see below), raising $40 million may have been an overkill.

| Liquidity Ratios | Value |

|---|---|

| Current Ratio | 1.61 |

| Quick Ratio | 1.51 |

| Cash Ratio | 1.26 |

However, this is not the first time the company has diluted the value of its shares.

As a matter of fact, since the start of the year, QCi raised $14.6 million from issuing 16,604,770 shares of common stock (this excludes the recent $40 million announcement).

Additionally, in August, they issued a secured convertible promissory note to Streeterville Capital for $8.25 million. As you may know, conversion rights may dilute shareholders since it allows the holder to convert debt into common stock at a discounted conversion price (92% of the volume-weighted average price, according to the last 10-Q).

As you may know, stock options and other equity incentives could lead to additional dilution. At the end of the last quarter, unvested restricted common stock, options, and warrants could potentially convert into 17,616,000 common shares.

Another risk includes the current inconsistent revenue streams. Before the recent announcement of the first order of TFNL, the revenue of the company was mainly driven by two contracts with Johns Hopkins University and NASA.

If the company doesn’t secure more orders for TFNL, I believe there is a high risk for further dilution once the $40 million raised is used.

Finally, as I already mentioned in the previous section, the company faces competitive pressures in the TFLN field. Among the different competitors, I am concerned with HyperLight Corporation, as they secured in September a $37 million series B investment led by Summit Partners.

As an additional note, HyperLight Corporation is a private US-based company, founded in 2018, specializing in TFLN photonic integrated circuits.

Therefore, QCi could lose market share if there are any delays in the final stages of commissioning its TFLN photonic chip foundry in Tempe, Arizona.

Valuation

Considering the close to 100% increase in the share price since November 14, I am not surprised to see a P/S ratio of 971.

Looking at the valuation ratios of the company, there is no doubt that the company looks overvalued. As I mentioned before, their revenue comes from two small contracts with Johns Hopkins University and NASA, barely surpassing $100k in the last quarter.

For this reason, at this early stage, the narrative of the company plays a more fundamental role in its future growth.

Once the company secures additional contracts for TFNL, I’ll revisit its valuation ratios. Until that happens, I believe the narrative holds more weight than these ratios.

Conclusion

To wrap up, I rate QCi as a strong buy based on its asymmetric reward potential. For full transparency, I own shares in the company at the moment of writing this article.

I believe the narrative of the company makes sense, considering the strong demand for quantum computing and data centers, mainly driven by AI applications.

The company’s recent order from a top Asian research institute shows there’s real demand for its photonic chips.

This technology could revolutionize data centers by doubling transmission speeds and cutting energy use. With the global push for faster, greener tech, I see massive growth potential here.

The $40 million cash infusion will help QCi finish its TFLN foundry and ramp up production in early 2025, putting the company in a strong position if additional contracts are secured.

I believe the upside here is huge, but so are the risks.

QCi has a history of diluting shareholders, and if they don’t land more orders soon, they may have to raise more cash, further diluting the value of their shares.

The company also faces stiff competition, especially from HyperLight Corporation, which recently secured $37 million in funding. On top of that, QCi’s revenue is still weak, mostly coming from two small contracts.

In conclusion, this is a highly speculative investment with the potential for disproportionate rewards. While I maintain a strong buy rating, conservative investors should approach this stock with caution.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of QUBT either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.