Summary:

- Rigetti Computing offers speculative upside, with significant catalysts ahead that could push its share price into double digits by the end of 2025.

- Milestones include the 84-qubit Ankaa 3 system in 2024, modular architecture validation in mid-2025, a 100+ qubit system by the end of 2025, and the future 336-qubit Lyra processor.

- Collaborations with NVIDIA, Fermilab, and NQCC, coupled with potential DARPA contracts and increased quantum funding in the US, are strong growth drivers for this stock.

- Risks include unstable revenue, high R&D costs, technological challenges, and competition from giants like IBM. Cash reserves project a runway until Q1 2026, however, further dilution is likely to happen.

- Despite a $17.3 million operating loss in the past quarter and liquidity concerns, I believe Rigetti’s narrative justifies my strong buy rating.

da-kuk

Rigetti Computing (NASDAQ:RGTI) represents what I believe is a high-risk, high-reward opportunity in the quantum computing space.

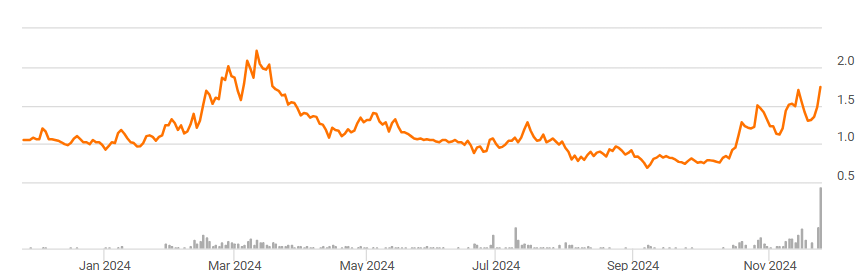

In the past six weeks, the share price has increased over 100%, followed by a sharp increase in volume, especially in the last few days.

seeking alpha

Could this be the start of a multi year bull run?

Considering the factors that I discuss in this article, I have a high conviction that the answer is yes.

In this article, I will provide the rationale behind my strong buy rating, including an overview of four different catalysts in their technology roadmap that, if realized, could drive the share price into the double digits by the end of 2025.

Aside from technological developments, I will discuss some of the current and future partnerships that could drive even more growth moving into next year.

Big rewards often come with big risks. Rigetti reported a staggering $17.3 million operating loss last quarter, with R&D expenses dwarfing revenue. Cash flow remains deeply negative, with current reserves of $92.6 million expected to sustain operations only until Q1 2026.

Additionally, at this early stage, it’s impossible to perform a reliable valuation analysis based on traditional ratios.

Instead, the narrative plays a heavier role in my strong buy rating than the current fundamentals. Let’s dive into this topic first.

Compelling Narrative, Dire Fundamentals

Let me be clear from the start: this is not a stock that a rational investor would buy based on pure fundamentals.

The company is still in the development stage, with a long journey ahead in its technology roadmap toward the 336-qubit Lyra superconducting quantum processor.

At the moment, the only revenue streams are development contracts with research and defense organizations in the public sector.

As one should expect, these are low margin, unstable contracts, that can’t even sustain the R&D costs of the company.

Let’s use the last quarter as an example: R&D expenses totaled $12.8 million, while revenue was only $2.4 million.

A quick look at the income statement confirms the choppiness of their revenue, with an operating loss in the last quarter of $17.3 million.

The cash flow statement conveys a similar message, with a TTM cash outflow from operations of $54.5 million.

Before I touch on the narrative topic, I think it is important to visit the balance sheet to estimate how much runway the company has left before it runs out of cash.

Rigetti has $92.6 million in cash and short-term investments. Considering the negative free cash flow of $65.8 million, the company should run out of cash in approximately 17 months (Q1 2026).

That estimation is based on the (naive) assumption they will not issue more shares or debt. Considering that the company raised $51.7 million (from selling 40.7 million shares) in the first nine months of 2024, I would expect to see further dilution in the near term, which could give them a few more years to complete their development roadmap.

Aside from issuing shares, the company raised capital through a loan agreement in 2021 with Trinity Capital Inc. This agreement was amended in June 2024, however, the terms are not particularly favorable, considering the effective interest rate at the end of last quarter was 23.1%, with $12.9 million still outstanding in principal balance.

Aside from the high interest, the scheduled principal payments are as follows:

- 2024: $3.4 million

- 2025: $9.1 million

- 2026: $0.4 million

The amended loan agreement contains covenants restricting the company from incurring additional indebtedness. However, the company could use non-traditional debt instruments, like convertible debt, to further expand its runway.

Let’s touch base now on the narrative.

The Development Roadmap

I’d like to start first with their recent achievements.

In the last conference call, management announced the successful tiling of 9-qubit chips without performance degradation, achieving high gate speeds of 60-80 nanoseconds.

Why is this a big deal?

Well, from a scalability perspective, manufacturing larger, single-chip quantum processors becomes exponentially harder due to physical, design, and manufacturing limitations.

Tilting smaller chips enables scaling qubit counts without being limited by the size and complexity of monolithic chip designs.

So far, Rigetti has been able to manufacture 9-qubit chips with a 99.4% median 2-qubit gate fidelity and 99.9% median 1-qubit gate fidelity.

The current efforts are focused on delivering the 84-qubit Ankaa 3 system by the end of 2024, with a 99%+ median 2-qubit fidelity. As a side note, this is the first catalyst in my bull thesis.

At the moment, Rigetti is collaborating with Riverlane to integrate quantum error correction techniques into its systems.

So far, they published a paper demonstrating real-time, low-latency quantum error correction. In their research, they used Riverlane’s decoder integrated into the control system of Rigetti’s 84-qubit Ankaa 2 system.

Moving beyond 2024, the next big milestone is planned for mid-2025, with the launch of a modular 36-qubit system, targeting a 99.5% median 2-qubit gate fidelity.

This seems to be a pivotal step in Rigetti’s development roadmap. If achieved, this will validate Rigetti’s modular architecture for scaling to higher qubit counts without fidelity loss. In fact, by the end of 2025, the company plans to launch a 100+ qubit system with 99.5% median 2-qubit fidelity.

To put things into perspective, these new systems are expected to operate at gate speeds of 60-80 nanoseconds, which are four orders of magnitude faster than competing ion-trap and neutral-atom systems.

Therefore, 2025 has two major catalysts with its technology roadmap.

Beyond 2025, Rigetti aims to develop a high-qubit count system capable of addressing real-world problems at scale: the 336-qubit Lyra system. If achieved, this will be a cornerstone for quantum advantage and practical applications.

However, management hasn’t committed to a specific date for Lyra, as its development depends on the success of these earlier systems.

To conclude this section, I foresee 4 big catalysts: one expected by the end of this year, two more in 2025, and a final one without a set timeline, as it heavily depends on the outcomes of the first three.

Partnerships and Government Engagement

Yet another catalyst could be the reauthorization of the NQI Act, expected in 2025.

This could significantly increase US quantum funding, from $500 million over five years in the initial act to a proposed $2.5 billion.

Rigetti is actively lobbying to secure a share of this funding. If successful, I expect dilution to slow down.

Another near term achievement could be securing part of the $300 million DARPA benchmarking contract with the DoD.

At the moment, the company has long term collaborations with national laboratories such as Fermilab and Oak Ridge. If the DoE expands funding to support large scale quantum initiatives, Rigetti could be a good candidate to receive part of these funds.

In regards to strategic partnerships, Rigetti has co-located its 9-qubit Novera QPU at the Israeli Quantum Computing Center, alongside NVIDIA’s Grace-Hopper Superchip and OPX1000 control systems.

This partnership is about figuring out how Rigetti’s QPUs can work with today’s GPUs and CPUs to help solve real life problems in areas like AI and machine learning.

In my view, the most important part of this partnership is the collaboration with NVIDIA, as it could unlock future opportunities.

Other partnerships include the UK National Quantum Computing Centre (NQCC), where Rigetti already installed a fully operational 24-qubit Ankaa System.

The current NQCC contract is expected to continue through Q1 2025, after which Rigetti is negotiating a potential new contract with updated terms.

Additionally, Rigetti has been collaborating with organizations such as Moody’s, HSBC, and Standard Chartered to explore practical applications of quantum computing in financial modeling.

Risks

I’ve already highlighted some of the risks in the first section of this article, including revenue volatility, high operating costs, and liquidity risks, which I believe are the most concerning issues for this company.

Aside from these financial challenges, the company also faces technological risks.

Advancements in its development roadmap, like achieving the 100+ qubit system by the end of 2025, hinge on its ability to maintain performance while tiling multiple chips. There is no doubt that any technical issues related to the scalability of their systems could push the development roadmap further in the future.

Additionally, implementing real time, fault tolerant QEC at scale is another obstacle they will have to overcome before they can commercialize their systems at scale.

Finally, from a competitor perspective, the company faces stiff competition from industry giants like IBM, AWS Braket, Azure Quantum, Google, and emerging players like IonQ (see my article here), D-Wave Quantum (QBTS), and Quantinuum.

Additionally, there are some European startups, like IQM (Finland) and Quantware (Netherlands), that are targeting modular and on-premises quantum systems similar to Rigetti.

Out of all these players, the one that presents the biggest threat is IBM, with its IBM Quantum platform providing access to quantum systems via the cloud. There is no doubt that IBM’s resources and scale dwarf Rigetti’s, making it harder for Rigetti to compete on infrastructure, cloud access, and customer acquisition.

Conclusion

To wrap up, I rate Rigetti as a strong buy due to its asymmetric risk to reward profile, with several catalysts within the next two years that could push the stock price up in the double digits.

By the end of this year, the company aims to deliver an important milestone in its development roadmap: the 84-qubit Ankaa 3 system, with +99% 2-qubit fidelity. If achieved, I expect the share price to double, just on the news release.

Moving into 2025, the potential renewal of the National Quantum Initiative Act could increase US quantum computing funding to a proposed $2.5 billion. In my view, Rigetti’s active lobbying efforts and long term collaborations with national laboratories make it well positioned to secure a portion of this expanded funding.

More funding contracts could come from the $300 million DARPA quantum benchmarking initiative.

By mid-2025, the company aims to validate the modular architecture of its systems with the launch of a modular 36-qubit quantum system with 99.5% median 2-qubit fidelity. If they achieve this milestone, scaling further with a 100+ qubit system by the end of 2025 should be doable, in my view.

If the company achieves these two milestones in 2025, I can easily see the share price trading in the double digits.

However, this is a high-risk play.

From a liquidity perspective, the company has a cash runway projected until Q1 2026. I believe this could be extended by at least one more year, at the expense of further diluting the stock.

From a technological perspective, there are big execution risks, including challenges in scaling large modular systems, achieving reliable error correction, meeting performance targets, and avoiding delays in its development roadmap.

Additionally, from a competitor’s perspective, industry giants like IBM and smaller players like IonQ could dilute Rigetti’s market share.

Overall, despite these risks, I bought OTM calls expiring in 2026, as I have a high conviction that the risk-to-reward profile makes sense for this speculative bet.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of RGTI either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.