Summary:

- It is unclear what kind of company Rivian will be in 3–5 years. A niche EV manufacturer, the next Tesla, or the next Fisker?

- The most likely outcome in the long term is a slow demise until Rivian either fades away or is taken over by a larger auto manufacturer.

- Rivian cannot generate the cash flows from its business to scale up and needs additional capital, diluting shareholders.

- Stock-basedcompensation adds to the dilution.

Klaus Vedfelt

Investment Thesis

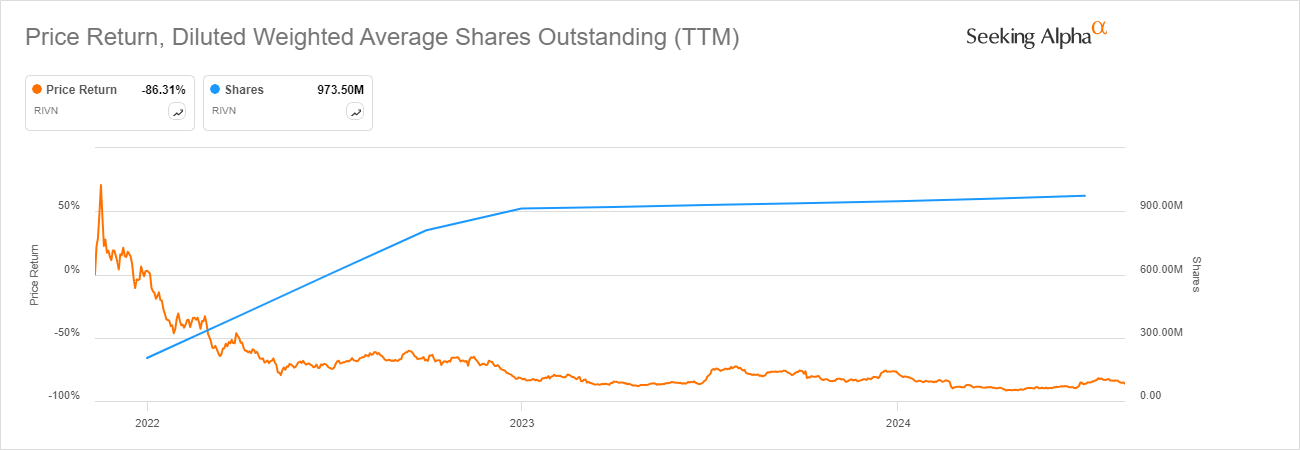

After its IPO in 2021, Rivian (NASDAQ:RIVN) was valued at over USD 100bn, more than Ford (F) or General Motors (GM). That has now come down to less than 14bn, after a 50% rally last month. Rivian had announced a deal with Volkswagen Group (OTCPK:VWAGY), where it will receive USD 1bn in December this year and possibly 4bn more until 2026 for a joint venture to develop software-defined vehicle platforms together.

Source: Seeking Alpha

It remains to be seen what kind of company Rivian will be in 3–5 years. Rivian could be the next Tesla (TSLA) (although I consider this highly unlikely) or continue to be a niche EV manufacturer. It could also be the next Fisker and on the way to bankruptcy. The most likely outcome, in my view, is that Rivian will face a slow demise until it either fades away or is taken over by a larger auto manufacturer (which could be Volkswagen). But that would be at a significantly lower share price than now.

If I am right, this will not happen because Rivian makes bad cars or has no demand. The auto business is capital intensive, and Rivian does not have enough cash left to scale, nor will it be able to produce the necessary cash flows. So far, Rivian has burned through over USD 21bn of shareholder equity. Still, the company has only 3.8bn on its books for Plants, Property & Equipment – the industrial base an auto manufacturer needs to manufacture its products. Rivian will need to increase its industrial base to scale. I do not see a credible path to how Rivian can do so within its current financial means. Oddly, the stock-based compensation expense (a non-cash expense, but still), is almost the same as CAPEX. The Volkswagen deal improved the picture and gave Rivian a fighting chance, but I do not think it changed the long-term trajectory.

Note – I will compare Rivian to Tesla, BMW Group (OTCPK:BMWYY), and Volkswagen Group in the article. Tesla is an obvious choice, as it is the largest EV manufacturer and a direct competitor in the North American market. I chose BMW Group and Volkswagen Group because they are mid-sized and large-sized established auto manufacturers, and because I am familiar with them (and have written Seeking Alpha articles about them).

Q2 earnings and Rivian’s financial situation before the Volkswagen deal

Rivian released its Q2 2024 earnings after the market closed on Tuesday. A static view of the balance sheet gives a positive impression. At the end of Q2 2024, Rivian still had net cash of USD 2.37bn (cash, cash equivalents, and short-term investments of 7.87bn, and 5.5bn long-term debt), about 1/6 of the current market cap (USD 13.7bn). The picture gets decidedly more negative when we look at the income statement and cash flows. Rivian lost USD 1.46bn on revenue of just 1.15bn (including USD 17mn from the sale of regular credits) and had a negative free cash flow of USD -1.037bn.

Rivian has never made a profit but has previously given two profit targets. The company wants to reach “modest” gross profitability in Q4 2024, and it aims to be “adjusted EBITDA-positive” in 2027. The long-term financial goal is to achieve a 25% GAAP gross margin and a 10% free cash flow margin, but there is no timeline.

I think both targets are not very helpful when answering the key question, which is (in my view): Does Rivian have enough cash, and can it produce enough positive cash flow, to finance its path to profitability?

Profitability on a gross margin basis is important as it takes Rivian out of the death loop where making more cars results in an even higher loss. Manufacturing more products should provide additional money to a company, not burn more cash. Some analysts argue that the company is still in start-up mode, although it is now 15 years old. Rivian aspires only to a “modest” gross profitability, so we should not expect much here. Rivian confirmed its previous guidance and expects to produce 57,000 vehicles in 2024, which is about the same volume as in 2023.

Gross profit (loss) in Q2, 2024 was USD -451mn (down from -412mn a year ago), around USD -33,000 per car delivered. The total operating loss – which includes selling, general, and administrative costs, as well as research and development – was -1.375bn. Even if Rivian managed to break even on a gross profit basis in Q4 (and there are promising signs, like a 20% reduction in material cost between first and second generation R1), it would still be loss-making on every other level, and the net loss in Q4 2024 would still be 1bn.

Rivian’s non-GAAP adjusted EBITDA target is not especially helpful either here, leaving aside the problem that this is supposed to be achieved only in 2027. Rivian excludes the cost of product changes through adjustments. Besides the usual stock-based compensation, the adjusted EBITDA excludes “costs incurred as we transition between major vehicle programs, cost incurred for negotiations with major suppliers regarding changing demand forecasts or design modifications” Management thinks those are special one-time items, but to me, this seems a questionable assumption. Auto manufacturers need to introduce new vehicle line-ups all the time, it is part of the business.

Larger manufacturers are outspending Rivian

CAPEX was USD 283mn in Q2 2024, down -10% YoY. This does not look like an especially high number. But that is deceiving, the 283mn is almost 1/5 of revenue. Other manufacturers, through their scale, have significantly lower ratios, although they spend billions on CAPEX every quarter. BMW Group had a capex ratio of 3.6% in Q1 2024. Including capitalized development cost, the ratio goes up to 5%, but is still only 1/4 of Rivian’s ratio. Volkswagen Group had a capex ratio of 7.4% in Q1 (I have again added capitalized development costs, which are significant and over EUR 2.8bn). Tesla was at 13%.

It seems to me that Rivian needs more scale to be competitive. So far, the company has not been very successful in converting cash burn into a viable industrial footprint.

Rivian has spent over USD 21bn of shareholder equity, but the company currently only has 3.8bn on its books for Property, Plants & Equipment. After retooling its facility in Normal, Illinois, (which was subsidized with USD 825mn by the State of Illinois), Rivian will have a manufacturing capacity of 215,000 vehicles. In comparison, BMW Group had a value of EUR 35.3bn for Property, Plant & Equipment on its books at the end of 2023 (USD 38.75bn at the current exchange rate), Volkswagen Group an astounding EUR 66.8bn (USD 72.45bn, and more than its market cap of EUR 52bn), and even Tesla has USD 31bn (Note – Tesla’s value looks inflated to me, though. It includes separate line items of USD 9.8bn for land and buildings and USD 5.9bn for construction in progress. Both line items have been increasing yearly, which would concern me if I were a Tesla shareholder. But this article is not about Tesla.). Both BMW Group and Volkswagen Group have no debt in their industrial businesses. The financial liabilities are only in their large financial services segments, where lease assets back them. Tesla also has a positive net cash position.

With its greatly reduced cash position and negative cash flows, it will be difficult for Rivian to get where those companies are. Rivian does not only compare negatively to those. Chinese auto manufacturers scale much quicker and at a lower cost. For example, Xiaomi (OTCPK:XIACY) needed less than three years to build a manufacturing capacity for 150,000 vehicles.

Is the deal with Volkswagen a game-changer?

Rivian announced a deal with Volkswagen where Volkswagen will invest up to USD 5bn into Rivian and a joint venture. Both Volkswagen and Rivian have provided investor information. Rivian also did an analyst call and the webcast can be found here.

As per Rivian’s investor information, the investments are anticipated to provide the necessary capital to fund the company’s operations during the ramp-up of the R2 vehicle line at its current facility in Normal, Illinois, and a new plant in Stanton Springs, Georgia, thereby enabling “a path to positive free cash flow and meaningful scale.”

The deal has different parts and stretches out from Q4 2024 to 2026.

- Volkswagen will provide Rivian with USD 1bn in the form of a convertible note. The note will convert into a direct stake in Rivian Automotive after December 1, 2024, assuming all regulatory approvals are received. As of July 30, the German Bundeskartellamt has already approved. USD 500mn will convert into Rivian equity at a share price of USD 10.84 (Note – I have not seen this number written down anywhere, but it was mentioned by Rivian during the webcast), and the remaining 500mn will convert based on the average price of Rivian shares in the 45 days before the conversion date. If the share price does not move much until December, Volkswagen will get 8-9% of Rivian shares for the one billion.

- Volkswagen and Rivian will form a 50:50 joint venture to develop a software-defined vehicle architecture based on Rivian’s R2 platform. After the creation of the JV, Volkswagen will have access to Rivian current software architecture, but the establishment of the JV is contingent on additional technical feasibility evaluations.

- If the JV is successfully established, Volkswagen will invest a further USD 4bn. 1bn will go in 2024 to the JV, and Volkswagen will grant a loan of another 1bn USD to the JV in 2026.

- Contingent on Rivian and the joint venture achieving certain technical and financial milestones (we do not know the details), Volkswagen will invest USD 2bn in Rivian directly in two tranches of 1bn each in 2025 and 2026. The amount of equity Volkswagen will receive for the 2bn will again depend on the average price of Rivian shares in a period before the conversion. Hypothetically, if the share price does not move, Volkswagen will own above 20% of Rivian and replace Amazon as the largest shareholder. However, as Rivian is diluting shareholders by about 5% yearly through stock-based compensation, the actual stake will be below 20% in 2026 (again assuming the share price stays the same). The bottom line for current shareholders is that they will own 40% less of the company in 2026.

Rivian and Tesla are currently the only car manufacturers (at least as far as I am aware) outside of China with a so-called zonal software architecture, and this is what Volkswagen is after. In a traditional domain vehicle architecture, many different hardware ECUs (electronic control units) are responsible for automating specific functions/domains (like adjusting the seats). This makes it very complex and complicated to operate software functions across those different ECUs, and this is a key reason why traditional auto manufacturers are struggling with over-the-air software updates. In a zonal architecture, the vehicle is divided into a few zones (usually around 3 to 5) and general-purpose ECUs automate each zone through software. There are a lot of benefits to this. For example, a zonal architecture greatly reduces and simplifies wiring. In general, a zonal architecture is considered a prerequisite for a software-defined vehicle.

While Ford still seems to think that it can develop such an architecture in-house, Volkswagen either has given up on it, or CEO Oliver Blume wants to hedge his bets. In China, Volkswagen cooperates with XPeng (XPEV) for the same purpose.

Implications from the deal

The Volkswagen deal substantially reduces liquidity risks for Rivian and enables the financing and ramp-up of the upcoming R2 line of vehicles, which are scheduled for 2026. Given the current cash burn, it is hard to see how Rivian could go until 2026 without an additional cash injection.

The upcoming R2 architecture will be the first application of the JV technology. Rivian said clearly during the analyst call that they expect to save on research and development costs, but were somewhat evasive on how large those cost savings are and how future contributions from Rivian to the JV will be structured (there were specific questions in that regard). In the Q-10 SEC filing for Q2 2024, research and development costs were USD 428mn, but a significant part of that will not be covered by the JV. The JV will develop the electrical, network, and software architecture, but not the user experience, autonomy, and other things like battery technology, propulsion, etc.

In a recent interview with The Verge, Rivian CEO RJ Scaringe said that a large part of Rivian’s development and technical design teams will move into the joint venture, and so will probably the associated cost. Rivian also expects benefits from the deal beyond the capital that the Volkswagen Group will provide, namely material cost savings, operating expense efficiencies, and even future revenues associated with the joint venture. There are no details here yet, though, as the JV structure still needs to be agreed between Rivian and Volkswagen.

Whatever the outcome, Rivian will continue to lose money from its operations over the next years, and even if the company reaches its target to be “adjusted EBITDA positive” in 2027, it will have burned through all its cash and the additional investment from Volkswagen.

Risks to the investment thesis

The key risk to this analysis is that Rivian will do much better over the next years than even Rivian management predicts. For example, Rivian has received more than 100,000 pre-orders for the R2 in just a few months. It does not take much to pre-order – customers must pay a refundable USD 100 deposit and can cancel the pre-order. Still, this shows a tremendous interest in the car.

While Rivian will most likely be supply constraint until 2027 as they have decided to pause plans for the factory in Georgia, it is possible that more companies such as Volkswagen will invest in Rivian to benefit from its EV expertise, or Volkswagen could ditch its upcoming Scout brand and manufacture vehicles for Rivian instead. So, a lot of good things can happen over the next two to three years, and investors who sell now could miss out on those.

For completeness, it is necessary to point out that there is the inverse risk too. It is far from assured that the cooperation between Rivian and Volkswagen will be successful. Rivian and Volkswagen are currently in their honeymoon phase. Many things can go wrong, and Rivian already has a history of failed collaborations with Ford and Mercedes (OTCPK:MBGYY).

Conclusion

The cash infusion from Volkswagen gives Rivian a fighting chance. Still, the risk/reward profile does not look good to me – even assuming Rivian management can successfully execute what they are saying now.

Looking forward to 2027: An equity stake in Rivian will have been diluted by around 40% from stock-based compensation and the deal with Volkswagen. Rivian will most likely still be a niche auto manufacturer, selling 200,000+ vehicles annually at best in just one market, North America. The company will have burned through its net cash position, including the inflows from Volkswagen. While positive on an adjusted EBITDA basis, Rivian will not be cash-flow positive yet and will continue to depend on additional capital (or debt) to finance investments.

Since Rivian announced the deal with Volkswagen, shares have surged. I will not invest, and, if I owned Rivian shares (which I do not) I would sell them now.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of VLKAF either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.