Summary:

- Roku is trying to replicate Apple’s playbook of creating a robust ecosystem of hardware and software around the home, with TV as the centerpiece of this walled garden.

- Despite a challenging macro environment, Roku’s key business metrics are improving consistently, and Roku is set to emerge as a larger and stronger connected TV ads platform beyond this downturn.

- In this note, we shall analyze Roku’s latest announcements, preview its Q4 results, analyze its technical charts, and determine its fair value and expected returns.

- With Roku trading at ~2x its annual Platform revenue (high-margin ads and content business), I continue to rate it a generational buy in the $40s.

Justin Sullivan/Getty Images News

Introduction

Roku (NASDAQ:ROKU) just took a leaf out of Apple’s (AAPL) vertical integration playbook by adding televisions to its product lineup. Over the last decade and a half, Apple has built a powerful ecosystem (walled garden) of devices (smartphones, laptops & PCs, wearables) and software for these devices. In a similar vein, Roku is attempting to build an ecosystem with its Smart Home products (TVs, cameras, video doorbells, lighting, plugs, and more) and the software to power these solutions. Now, I am not saying that Roku is the next Apple; all I am saying is that Roku’s strategic plan is to build a walled garden similar to what Apple has built for itself.

Roku Investor Relations

Last week, Roku surpassed 70M active accounts, and it remains the No. 1 TV OS platform in the US, Canada, and Mexico. For years, Roku has outcompeted bigger rivals such as Amazon (AMZN) [Fire TV OS] and Alphabet (GOOG) [Android TV OS]. While Roku’s custom-built TV OS system is better than both of those Android OS systems, a big part of Roku’s success stems from the fact that its brand (Roku Tv) has become synonymous with streaming!

Google Trends

Launched in 2014, the Roku TV program (licensing arrangements with OEM partners like TCL, Hisense, and others) powered Roku’s admirable rise over the last eight years or so. However, Roku’s reliance on its OEM partners has always been viewed as a risk factor; and in recent quarters, Roku’s rivals, such as Google (GOOG) [Android TV OS], have partnered up with its OEM partners like TCL to build Android TV models.

Considering these dynamics, the threat of Roku being gazumped by its big tech rivals has been rising, and its dependency on OEM partners put Roku in a vulnerable situation. Hence, I see this move from Roku to design and build its own TVs as more of a necessity than a choice. From a long-term perspective, I believe this is a big step in the right direction, as Roku now has better control of its business. In my opinion, the risk of Roku being gazumped by its TV OS rivals is greatly reduced with this strategic move.

That said, the timing of this move is not great. For the last six quarters, Roku has been subsidizing its hardware (selling below cost) to boost user acquisition. While the user acquisition strategy is clearly working (Roku added ~10M active accounts in 2022), Roku’s profit engine (advertising business) is going through a slump due to macro pressures, which has turned Roku into a loss-making entity for the time being. Therefore, entering a capital-intensive business at this moment is not ideal for Roku.

Roku Q3 2022 Shareholder Letter

In the post-pandemic world, a growth slowdown combined with margin compression has led to a dramatic collapse in Roku’s stock, which is still down around -90% from its all-time highs. And at these depressed levels (~2x Platform revenue), I rate Roku a generational buy for the reasons we will discuss in today’s note and all the reasons shared in the note linked below:

-

Roku Stock: An Opportunity Of A Lifetime Or A Tragic Mistake? [Post Q3 report; released on Nov 7th, 2022]

In today’s note, we will first discuss Roku’s technical chart, and then, I will provide a Q4 preview for Roku. Finally, I will share my updated fair value and expected return projections. Without further ado, let’s get started!

ROKU Stock: Is The Bottom In Already?

In recent weeks, Roku has formed a nice little “V-shaped” reversal pattern with a (local) bottom at ~$38. As long as the stock continues to climb up in a series of higher highs and higher lows, Roku seems destined to re-claim the $50 to $60 range it traded in during mid-September to early December.

WeBull Desktop

The neckline of the V-shaped reversal pattern is slightly above $60, and a breakout of that level could propel Roku’s stock back over $80, which would be a 70% move from current levels. As I see it, the $50-$60 range is certainly in play here (in the short-term), especially if Q4 earnings come in better than expected and management provides positive guidance for 2023.

The last time ROKU’s stock showed a similar reversal pattern was in late 2018, and here’s how it played out:

WeBull Desktop

From a technical perspective, Roku’s stock is showing positive momentum. And the recent active accounts and user engagement (streaming hours) data are encouraging. Let’s check out this data and preview Roku’s Q4 report.

Roku Q4 Preview And Future Outlook

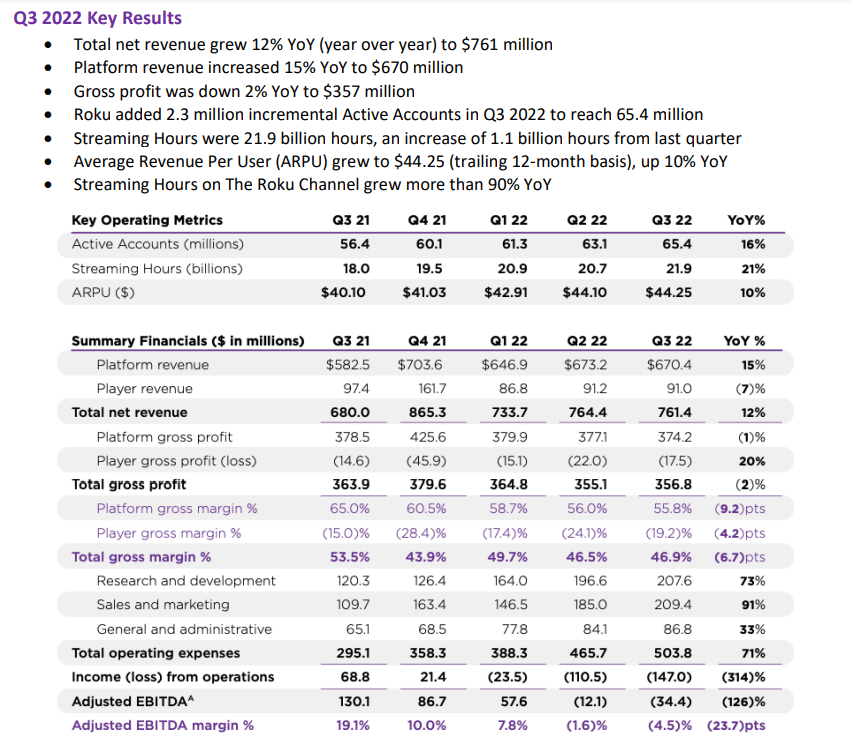

Back in early November, Roku’s management guided for Q4 revenues to come in at $800M (y/y growth of ~14%), with gross profit expected to drop by ~24% to $325M. This drop in margins is projected to result in widening losses.

Roku Q3 2022 Shareholder Letter

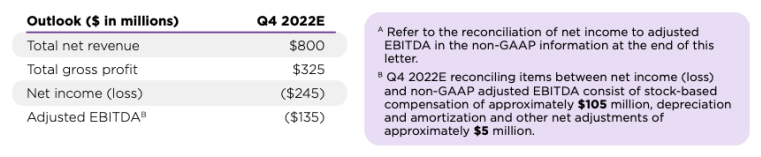

According to its latest announcement, Roku’s active accounts surpassed 70M in the first week of January. Additionally, Roku reported Q4 streaming hours of 23.9B, a growth of +22.5% y/y. Both active accounts and streaming hours paced faster than in Q3 2022.

Roku Press Release

Alright now, Roku started Q4 at 65.4M active accounts and announced reaching 70M accounts on Jan 5th, 2022 (just after Q4). So let’s assume Roku added ~4.5M active accounts during Q4 2022. Over the last two quarters, Roku’s TTM ARPU has remained over $44, and hence, I think it is safe to assume that Roku generated ~$10-11 in platform ARPU in Q4.

Assuming a weighted average count of 67.6M active accounts for Q4 (avg. of starting and ending figures for active accounts) and multiplying this figure by $10, we get to Q4 Platform revenues of $676M.

Based on historical numbers, an addition of ~4.5M active accounts in Q4 should result in player revenue of $170-$180M. Given Roku’s use of hardware as a loss leader to acquire customers, I am not sure where the gross margin will land this quarter; however, inflation has been declining for several months now, and that’s a tailwind for Roku’s Player margins.

According to my calculations, Roku’s total net revenue for Q4 could be greater than $850M. The macroeconomic environment remains uncertain and predicting Roku’s Platform revenues reliably is hard. However, I continue to believe that Roku’s management set a low bar that they can beat with ease since this is how they have operated over the years.

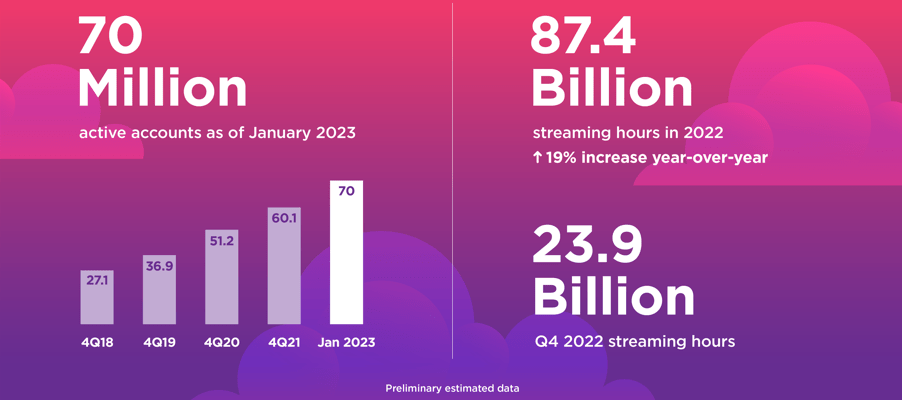

While Roku’s near-term business outlook remains uncertain, the shift from Linear TV to Streaming is chugging along at a healthy clip, and so is the shift of advertising dollars from Linear TV to Connected TV. Over the next four years, US Connected TV [CTV] Ad Spending is projected to grow from $21.16B to $43.59B at a CAGR of ~19.8%.

At ~70M active accounts, a Platform ARPU of $45 gets us to annual Platform revenue of ~$3.15B. Remember, Roku’s Platform business commands robust margins (gross margin: ~55-60%). Hence, Roku trading at ~2x its Platform revenue base is a stunning bargain. That said, let us determine the absolute valuation for Roku.

Roku’s Fair Value And Expected Returns

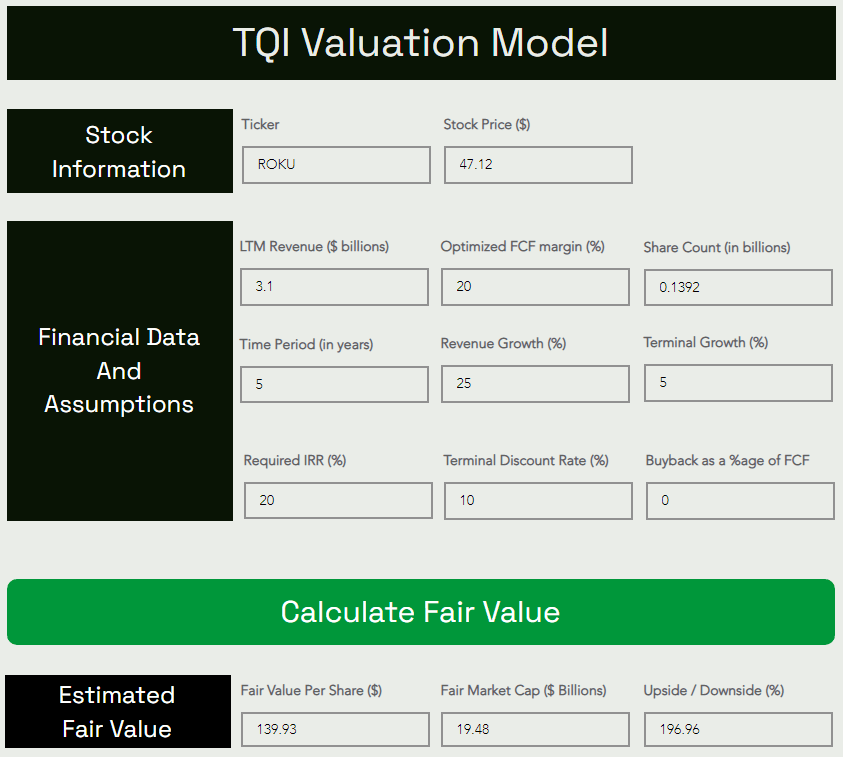

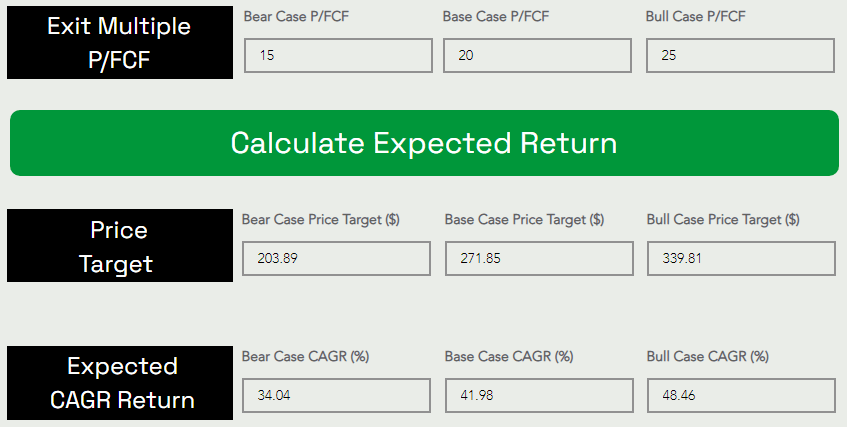

To evaluate Roku’s absolute valuation, we will use the TQI Valuation Model:

TQI Valuation Model (TQIG.org)

TQI Valuation Model (TQIG.org)

According to TQI’s Valuation Model, Roku is worth $139.93 per share ($19.5B in market cap), i.e., it is currently trading at a significant discount to its fair value. Furthermore, the base case assumption of ~20x P/FCF in 2027 resulted in a 5-yr expected CAGR of 41.98% for Roku. Since this expected return is far greater than our investment hurdle rate of ~20% for growth stocks operating near FCF breakeven, I rate Roku a “Strong Buy” at current levels.

Final Thoughts

Here’s what I said about Roku after its Q3 earnings report in November –

In the past, I have laid out my bullish thesis for Roku doing ~$40B+ in advertising revenue by the end of this decade, and despite Roku’s share price action, I am still confident in my projections for Roku becoming a very large and profitable (monopolistic TV OS and connected-TV advertising) business. If you are interested in learning more about my original investment thesis for Roku, please refer to this note:

Roku’s business fundamentals could get worse over coming quarters as advertising headwinds are set to persist amid a weak macroeconomic environment. While the rising probability of a recession and Roku’s financial underperformance (or I would say lack of outperformance) are causing a capitulatory sell-off in the stock, I think the valuation moderation has gone too far, and the risk/reward from here is asymmetrically in favor of long-term bullish investors. With a 5-yr expected CAGR of 40%+, Roku is an opportunity of a lifetime!

Source: Roku Stock: An Opportunity Of A Lifetime Or A Tragic Mistake?

Despite an uncertain macroeconomic environment, Roku’s key business metrics are heading in the right direction, with growth in active accounts and streaming hours re-accelerating in Q4 2022.

Starting in March, Roku will design and build its own TVs. By adding TVs to its rapidly-growing smart home product lineup, Roku is taking charge of its own destiny [reducing its dependence on OEM partners like TCL and HiSense]. The timing of this move is off-putting due to the capital-intensive nature of this business; however, Roku is building a powerful ecosystem of hardware and software to serve as a walled garden for selling ads. With its net cash balance of $2B+, Roku could easily afford to invest aggressively during this economic downturn. The long-term outlook for Roku remains bright as the shift in ad spending from linear TV to connected TV is only a matter of when not if, and hence, ignoring near-term macro pressures is of critical importance for investors. At ~2x annual Platform revenue, Roku is dirt cheap, and long-term investors buying it at $47 could potentially generate a CAGR return of ~42% over the next five years.

Key Takeaway: I rate Roku a generational buy in the $40s.

Thanks for reading. Please let me know if you have any thoughts, questions, or concerns in the comments section below.

Disclosure: I/we have a beneficial long position in the shares of ROKU, AAPL either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Are you looking to upgrade your investing operations?

Your investing journey is unique, and so are your investment goals and risk tolerance levels. This is precisely why I tailored my marketplace service – to help you build a robust investing operation that can fulfill (and exceed) your long-term financial goals.

TQI’s core idea is to generate wealth sustainably through tailored portfolio strategies that meet investor needs across different investor lifecycle stages. Each of our five model portfolios comes with thoroughly vetted investment ideas, embedded risk management, and specialized financial engineering for alpha generation.