Summary:

- Roku, Inc.’s Q2 2023 earnings call should focus on monetizing its user base of approximately 72 million active accounts.

- Anticipation for details on the tie-up with Shopify and prospects of making ads more shoppable.

- Expectation for Roku to address its lackluster progress in monetization and potential EBITDA margins for 2024.

- Importance of improving revenue growth rates in H2 2023 to regain momentum in the market.

simpson33

Investment Thesis

Roku, Inc. (NASDAQ:ROKU) is about to report its Q2 2023 earnings on Thursday, July 27, after the close. I believe that its earnings call will be dominated by its strategy to better monetize its user base.

How can Roku take its approximately 72 million active users and provide end users the capabilities to make its ads more shoppable?

Furthermore, can Roku provide any further insight into what sort of EBITDA margins could be possible in 2024? According to my estimates, the stock is priced at approximately 50x forward EBITDA.

Paying $70 for Roku is an interesting entry point, if Roku’s prospects are able to re-start and gather momentum.

What Do We Know From This Earnings Season So Far?

We are still early into the earnings season, but the message that we can thus far discern from both Snap (SNAP) and Alphabet (GOOGL, GOOG) is that there’s demand for advertising. But it’s patchy.

By this, I mean that there’s a significant appetite for brands to advertise. Also, there doesn’t appear to be an imminent recession in the cards. That being said, advertisers are being highly cautious about where they deploy their advertising dollars.

Compared with the previous two years, when brands believed in spending their ad dollars across an array of distribution platforms, today brands are being significantly more selective.

Essentially, brands have 4 key wants. They want access to high-quality data on their ad. To know exactly what sort of individual is watching their ad? How long did they watch the ad? And perhaps, most crucially, what did the individual do next?

In a cookie-less environment, where privacy is of course paramount, what sort of ROIs can the platform deliver? Because advertising is not cheap. However, marketers are more than willing to pay up for ads provided they get ”measurable” high-quality views.

Within this context, I expect to hear from Roku’s earnings call a lot more details on its framework around its tie-up with Shopify (SHOP). More specifically, what are the near-term prospects of making ads shoppable?

Think about this: for years, Pinterest (PINS) has sought to embrace these exact same prospects. Getting users to go from viewing an ad to shopping for that product. It’s an idea that in principle makes a lot of sense. But we’ll have to tune in on Thursday after hours to get more details on tangible aspects of making this a reality in the near term.

What else to look towards in Roku’s Q2 earnings?

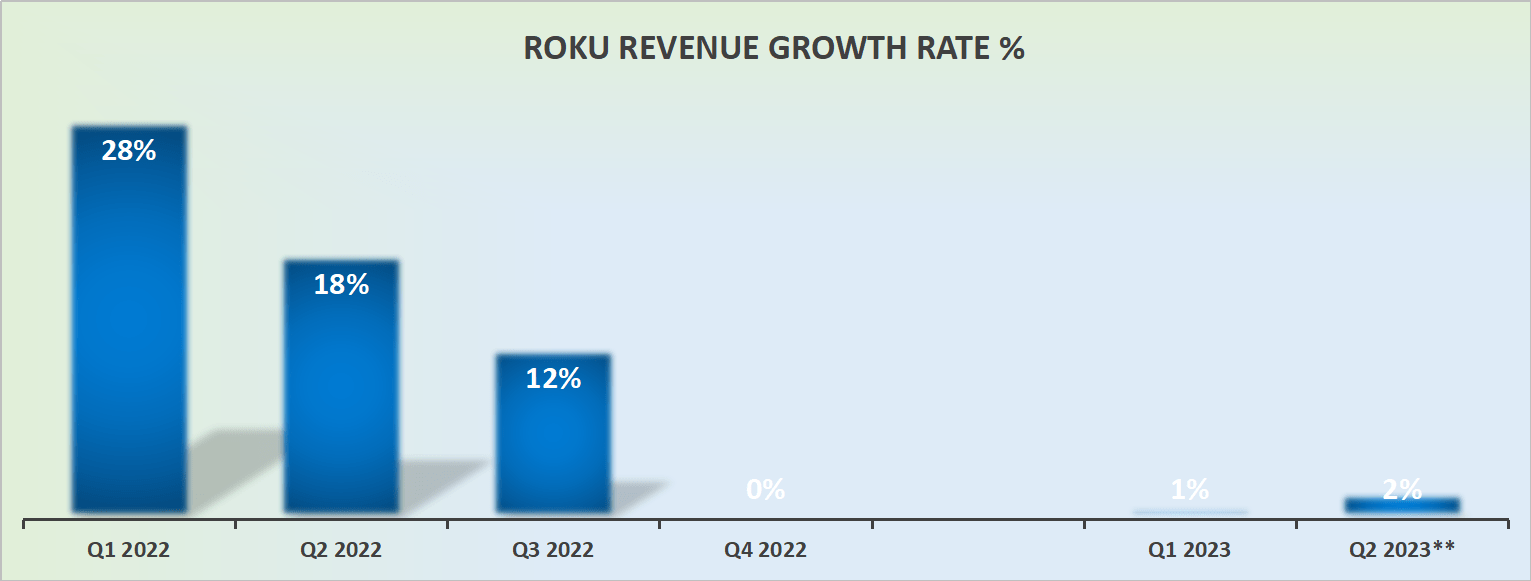

Roku’s Revenue Growth Rates Should Improve in H2 2023

ROKU revenue growth rates

I believe that the unavoidable reality is that Roku absolutely needs to deliver to investors a view that H2 2023 will be significantly better than H1 2023.

I believe that this should be easy enough to accomplish, at least on the surface. After all, Roku’s H1 2023 was its toughest comparable period, and the tone from both Alphabet and Snap earnings calls is that advertisers are very eager to enter the market and start spending.

Put another way, with the present much easier macro environment, I believe that we are very likely to see Roku’s earnings call giving investors the impression that its results have crossed through revenue growth rates and that Roku can now be back again on the front foot.

Roku’s Biggest Issue: ARPU

The issue for Roku hasn’t been one of a lack of users on its platform. Indeed, I wouldn’t be surprised to see Roku’s Q2 2023 ending with 72 million active accounts.

Rather, to put it concretely, the issue that has recently plagued Roku has been its lackluster progress on better monetizing its user base.

That being said, if Roku can convincingly reaffirm to investors that it’s succeeding in turnaround its operations and that around 5% EBITDA margins are possible in 2024, this could see Roku delivering around $200 million of EBITDA in 2024.

This would put the stock priced at around 50x forward EBITDA.

Note, back in 2021, Roku’s EBITDA margin reached 17%. Therefore, my 5% estimate is a relatively easy hurdle.

The Bottom Line

For Roku’s upcoming Q2 2023 earnings, I anticipate a focus on the company’s strategy to better monetize its user base of 72 million accounts.

I am particularly interested in learning about Roku’s plans to make its ads more shoppable and its potential EBITDA margins for 2024.

As the advertising landscape evolves, marketers are becoming more selective about where they deploy their ad dollars, seeking high-quality data and measurable views.

Roku’s tie-up with Shopify could hold the key to making ads shoppable, a concept that has intrigued platforms like Pinterest as well. Additionally, I expect Roku to address concerns about its lackluster progress in monetization, and if the company can demonstrate successful turnaround efforts and achieve around 5% EBITDA margins in 2024, it may lead to positive investor sentiment.

Improving revenue growth rates in H2 2023 will also be crucial for Roku to regain momentum in the market.

I believe there’s a positive risk-reward in the stock right now.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Strong Investment Potential

My Marketplace highlights a portfolio of undervalued investment opportunities – stocks with rapid growth potential, driven by top quality management, while these stocks are cheaply valued.

I follow countless companies and select for you the most attractive investments. I do all the work of picking the most attractive stocks.

Investing Made EASY

As an experienced professional, I highlight the best stocks to grow your savings: stocks that deliver strong gains.

-

- Deep Value Returns’ Marketplace continues to rapidly grow.

- Check out members’ reviews.

- High-quality, actionable insightful stock picks.

- The place where value is everything.