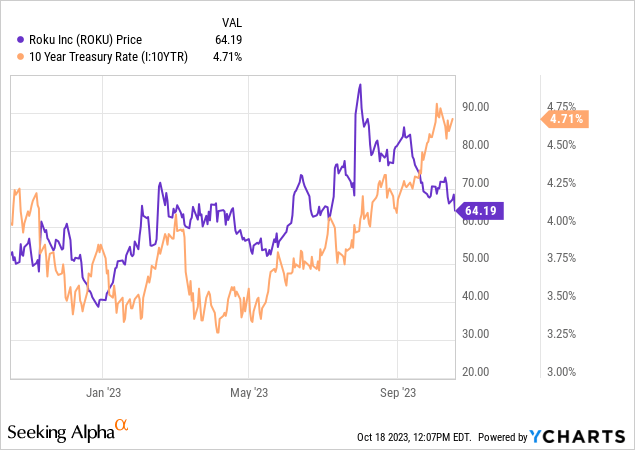

Amid a surge in long-duration treasury yields, Roku’s stock has suffered a sharp pullback in recent weeks, along with several other growth-tech names.

With leading economic indicators pointing to an economic recession in the next 12 months, Roku’s near-term [ad] business outlook remains shrouded in uncertainty.

Despite near-term macro pressures, the long-term outlook for Roku remains bright as the shift in ad spending to connected TV is inevitable.

Furthermore, management’s recent cost-cutting initiatives and improved guidance for Q3 paint a robust outlook for 2024 and beyond.

lucky336

Introduction

Back in early 2023, I rated Roku, Inc. (NASDAQ:ROKU) a “generational” buy in the $40s as the connected TV ad giant embarked on its journey of building a walled garden akin to Apple (AAPL):

Despite an uncertain macroeconomic environment, Roku’s key business metrics are heading in the right direction, with growth in active accounts and streaming hours re-accelerating in Q4 2022.

Starting in March, Roku will design and build its own TVs. By adding TVs to its rapidly-growing smart home product lineup, Roku is taking charge of its own destiny [reducing its dependence on OEM partners like TCL and HiSense]. The timing of this move is off-putting due to the capital-intensive nature of this business; however, Roku is building a powerful ecosystem of hardware and software to serve as a walled garden for selling ads. With its net cash balance of $2B+, Roku could easily afford to invest aggressively during this economic downturn. The long-term outlook for Roku remains bright as the shift in ad spending from linear TV to connected TV is only a matter of when not if, and hence, ignoring near-term macro pressures is of critical importance for investors. At ~2x annual Platform revenue, Roku is dirt cheap, and long-term investors buying it at $47 could potentially generate a CAGR return of ~42% over the next five years.

Key Takeaway: I rate Roku a generational buy in the $40s.

Despite a sharp (-35%) rate-induced pullback in recent weeks, Roku’s stock is still up by nearly +35% since the publication of my previous report on the company. And while surging long-duration yields can continue to exert pressure on Roku’s stock in the near term due to its lack of profitability, management’s recent cost-cutting initiatives and improved revenue guidance bode well for existing ROKU shareholders and potential investors.

Data by YCharts

In today’s note, I shall provide a brief update on Roku’s business and share my outlook for Q3 and the rest of 2023. Furthermore, we will take a fresh look at Roku’s fair value, expected return, technicals, and quant factor grades to make an informed investment decision for the stock.

Brief Review Of Roku’s Business

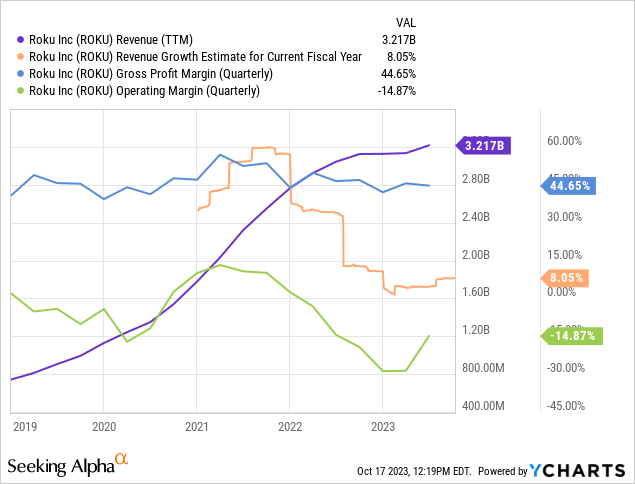

If you have been following my work, you already know that I view Roku as a $30-40B annual advertising (high margin) business by the end of this decade. While these projections may seem like a pipedream at a time when Roku’s growth has slowed down to low double digits and operating losses have widened, I continue to believe in my long-term outlook given strong user acquisition and engagement numbers shown by Roku during the recent slump in its financial performance.

Data by YCharts

Roku Q2 2023 Shareholder Letter

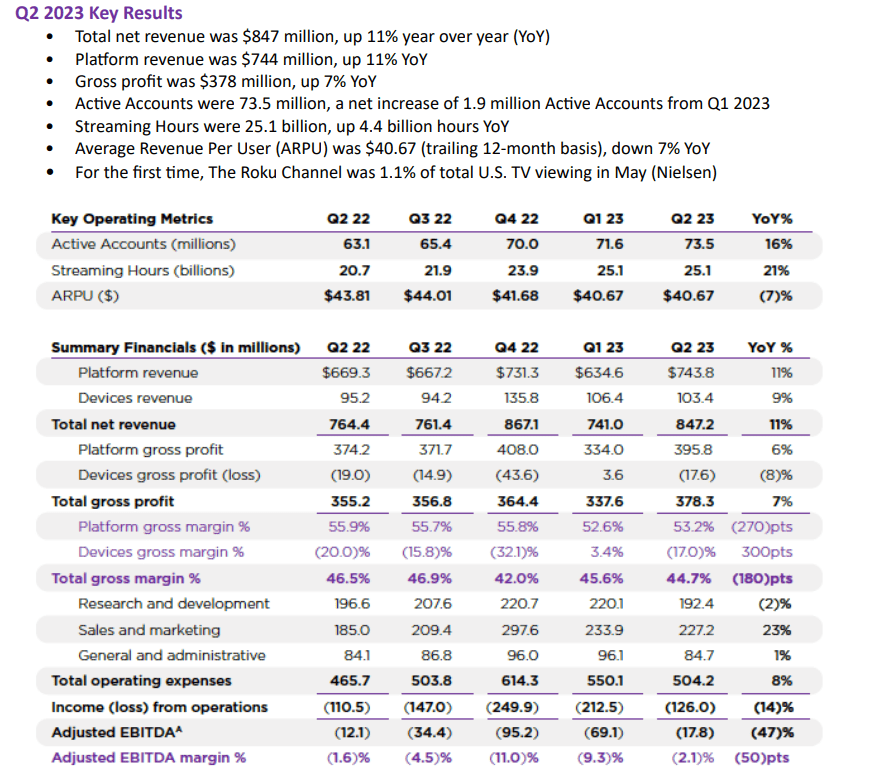

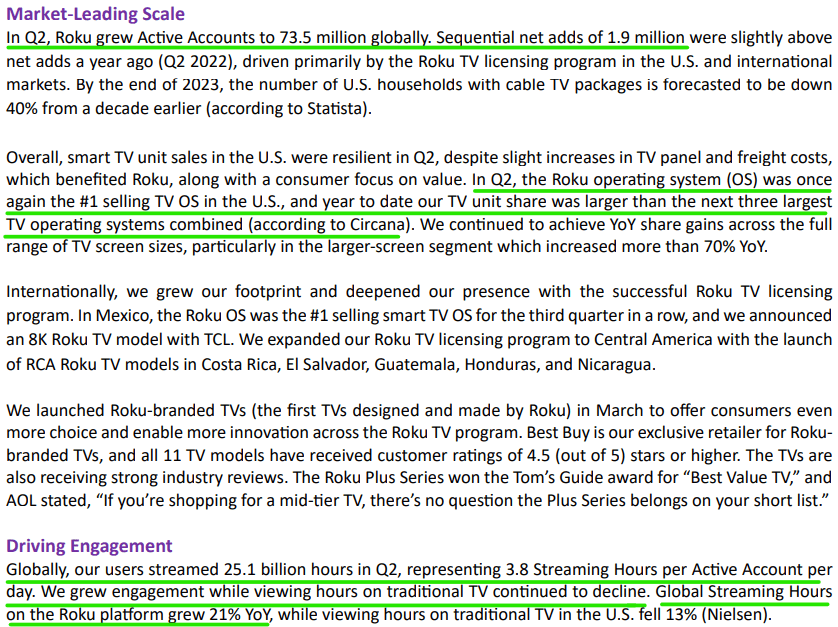

In the first half of this year, Roku has added nearly 3.5M net new active accounts to reach 73.5M active accounts as of the end of Q2 2023. With streaming TV continuing to take share from cable TV and broadcast, Roku looks primed to expand its user base at a healthy clip for several years to come as the No. 1 TV OS platform in the United States, Mexico, and Canada.

Roku Q2 2023 Shareholder Letter

Roku Q2 2023 Shareholder Letter

According to my estimation (based on past user acquisition trends and current trajectory), Roku will end 2023 with ~78-80M active accounts. Ongoing macroeconomic uncertainty has negatively impacted TV Ad spending (and by extension, Roku’s platform ARPU) in recent quarters; however, Roku’s monetization efforts look promising [i.e., unique brand advertising in Roku city (screensaver), the Roku Channel (original and licensed content being monetized via Ads), Shoppable Ad technology partnerships with Walmart (WMT) & Shopify (SHOP), and the gradual opening up of Roku’s platform to third-party demand-side platforms (DSPs) to fill ad slots].

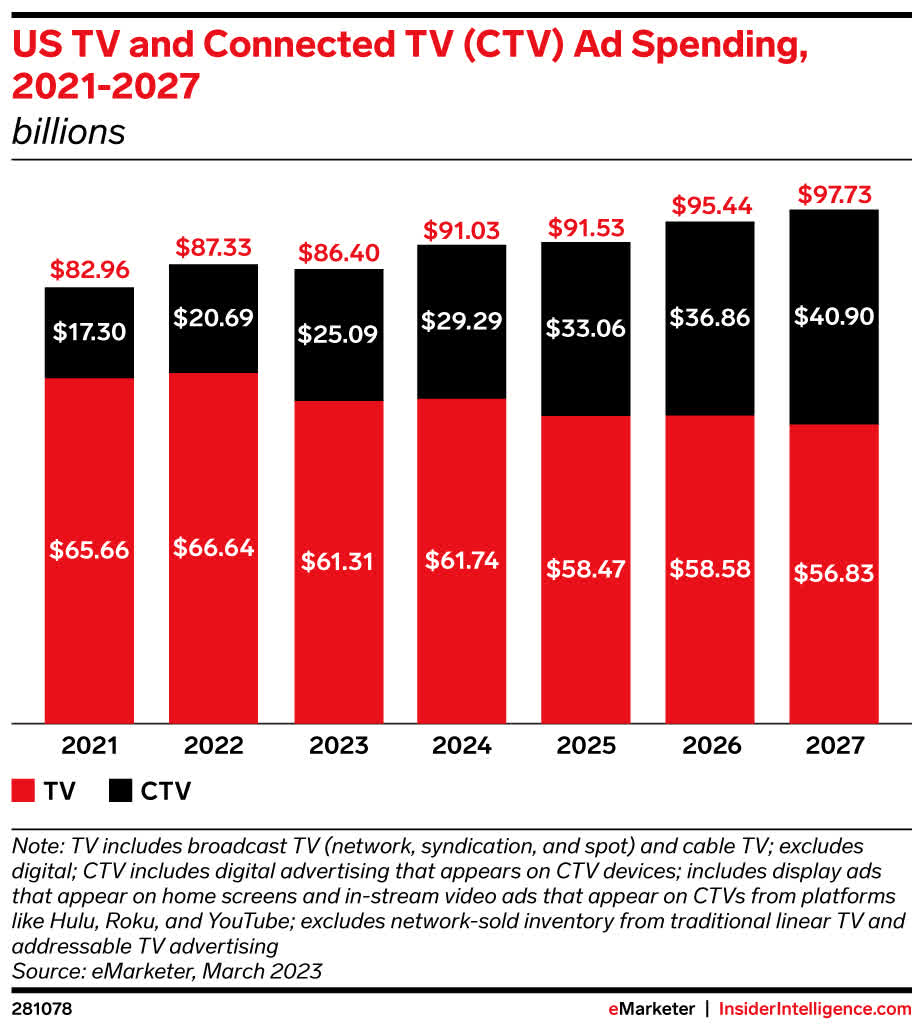

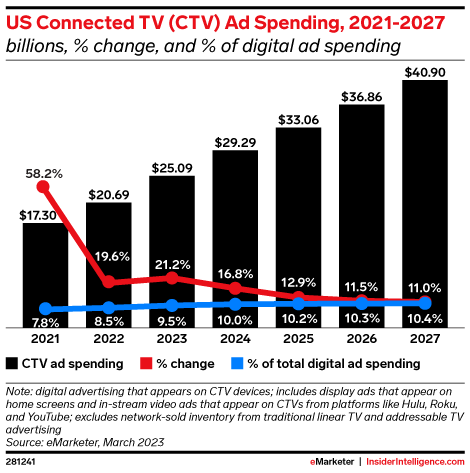

With the ongoing secular shift in consumer viewership from traditional TV to streaming TV, Roku remains well-positioned to benefit from the natural impending shift in advertising dollars to connected TV platforms.

Roku’s founding vision remains true: All TV and all TV advertising will be streamed. Almost every major media company is reorienting its business around streaming and has launched a flagship service, spending billions on content and marketing to attract and retain subscribers. At the same time, with the significant gap that exists between viewership (45%) and ad budgets (18%), we are still in the early days of the secular shift to streaming. Our competitive advantages — the Roku® operating system, The Roku Channel, and our ad platform — position us strongly to continue leading this shift in the years ahead.

eMarketer

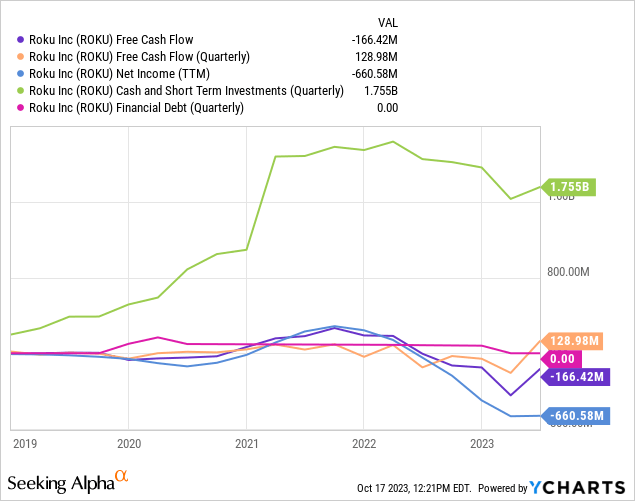

Now, despite reporting strong user acquisition and engagement numbers (indication of robust future revenue and profit growth), Roku’s losses have piled up in recent quarters as operating expense growth has outpaced revenue and gross profit growth. Coming out of the pandemic, Roku’s management increased employee headcount aggressively and expanded into capital-intensive projects (content production and hardware ecosystem) in the hunt for growth. Unfortunately, ongoing macro uncertainty has caused a drastic slowdown in Roku’s profit engine (advertising business), creating massive pressure on the bottom line.

Data by YCharts

Fortunately, Roku has no debt and $1.75B in cash & short-term investments to see the company through this challenging macroeconomic environment. Last quarter, Roku turned free cash flow positive, and while management expects negative adj. EBITDA through the rest of this year, Roku is all set to return to positive cash generation in 2024 and build on it in the coming years.

What To Expect From Roku’s Q3 2023 Results

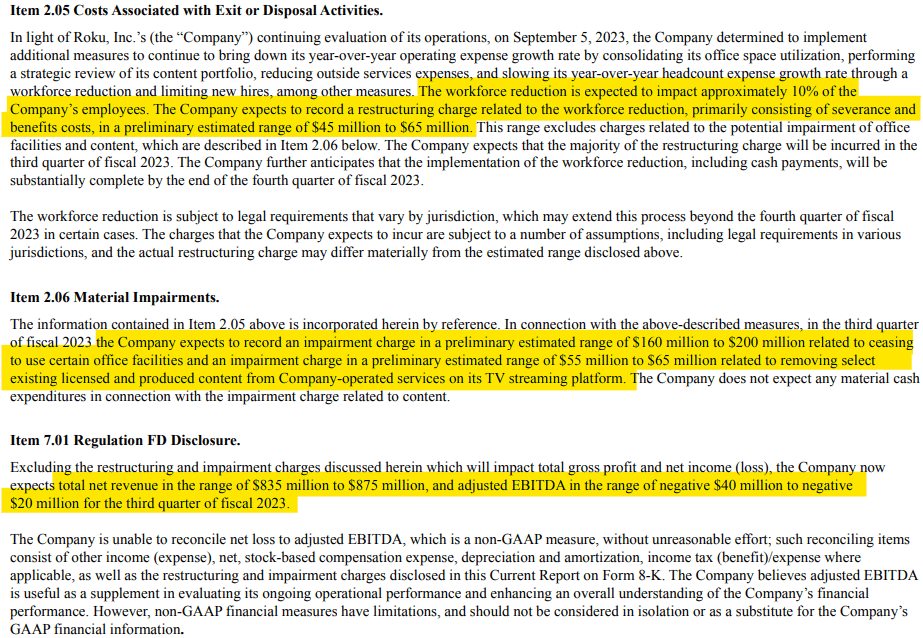

In a recent 8-K filing (5th September 2023), Roku’s management announced several cost-cutting initiatives [10% workforce reduction, limiting hiring, office space reduction, and TRC content cuts] that are set to negatively impact the bottom line to the tune of ~$260-330M in the remaining quarters of 2023.

Roku 8-K filing

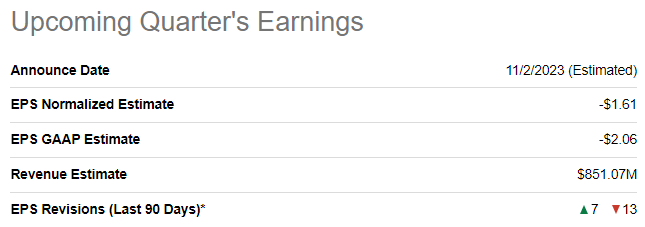

While these cuts may prove to be insufficient in the event of further macroeconomic deterioration, Roku’s management is confident about delivering positive adj. EBITDA in 2024. This confidence stems from stronger-than-expected top-line performance based on improvement in the TV ad market, with Q3 revenues now set to come in at $835-875M [ahead of management’s previous guide of $815M].

Roku Q2 2023 Shareholder Letter

SeekingAlpha

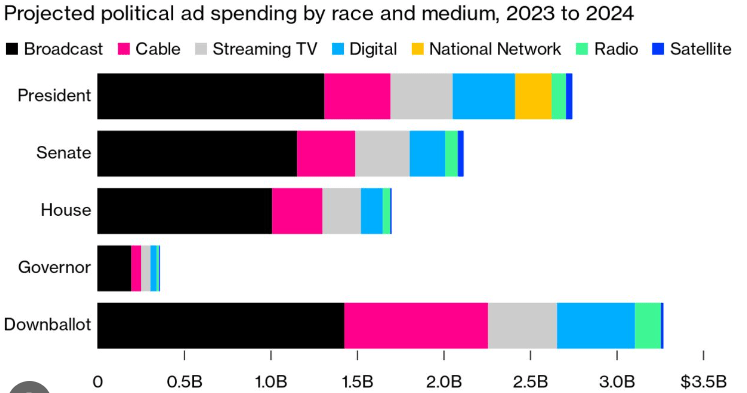

With leading economic indicators still pointing towards an imminent recession (hard landing for the economy), the near-term outlook for Roku’s ad business (platform revenues) remains highly uncertain. That said, we are heading into an election year, and political ad spending (est. for 2024 cycle: $10.2B) should serve as a strong tailwind for Roku’s ads business over the coming quarters.

Bloomberg

Long-Term Risk/Reward For Roku Is Attractive

Assuming a weighted average active account figure of 74M and a conservative ARPU estimate of $40-42, I see Roku’s platform revenues landing at ~$3B for 2023. As a greater share of TV ad spending (~$90B market) shifts to streaming/connected TV in the US, Roku is primed to experience secular growth for several more years to come with the company boasting >30% market share of TV OS aggregator platforms in its domestic market [US].

eMarketer

As we have discussed in the past, Roku’s international expansion is still in the nascent stages, and I think the strong performance in Mexico and Canada speaks volumes for Roku’s long-term growth potential.

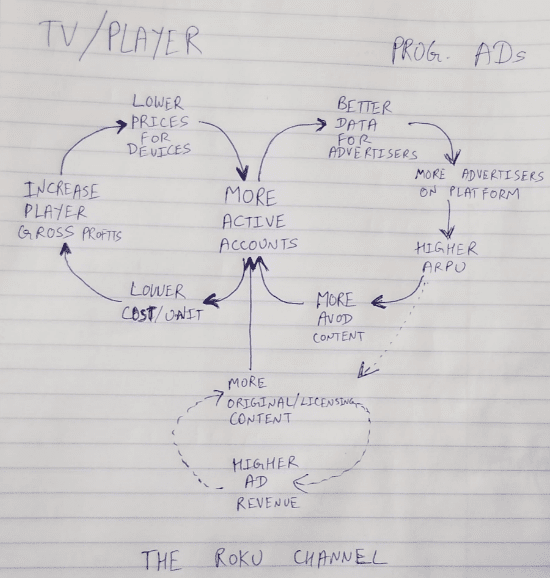

In the long run, I see the global TV OS market consolidating into 2 to 3 players (similar to what we have seen with the mobile OS and PC/Desktop OS markets), and given Roku’s current market-leading position and powerful flywheel, I think it is primed to be a top player in this attractive arena [$100B+ advertising TAM].

Roku Flywheel (Author)

By the end of this decade, I view Roku as a $30-40B annual ad revenue business [200-250M active accounts (globally) & ARPU of ~$150]. While net losses are set to widen in the next quarter or two, Roku’s underlying business trends are getting stronger, and the business is set to turn free cash flow generative in 2024. The near-term macroeconomic [ad market] outlook remains uncertain; however, Roku’s long-term future looks brighter than ever.

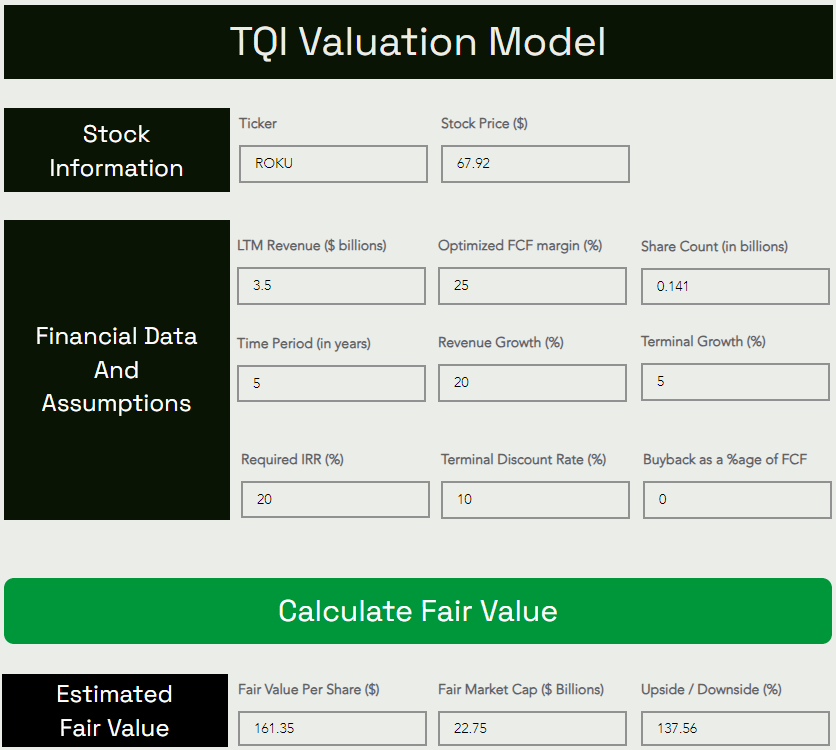

Here’s my updated valuation model for ROKU:

TQI Valuation Model (TQIG.org)

TQI Valuation Model (TQIG.org)

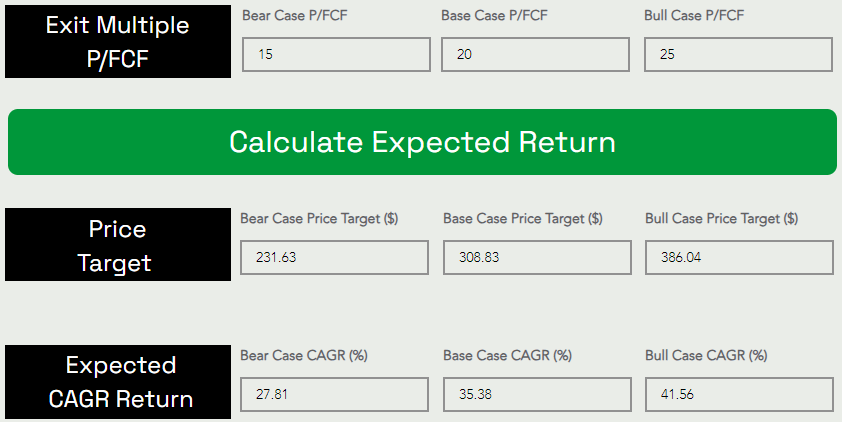

According to TQI’s Valuation Model, Roku is worth $161.35 per share ($22.75B in market cap), i.e., it is currently trading at a significant discount to its fair value. Furthermore, the base case assumption of ~20x P/FCF for exit multiple resulted in a 5-year expected CAGR of 35.38% for Roku. Since this expected return is far greater than our investment hurdle rate of ~20% for growth stocks operating near FCF breakeven, I rate Roku a “Strong Buy” in the $60s.

ROKU’s Technicals And Quant Factor Grades

In relation to technicals, I made the following comments on ROKU stock in early 2023 –

ROKU Stock: Is The Bottom In Already?

In recent weeks, Roku has formed a nice little “V-shaped” reversal pattern with a (local) bottom at ~$38. As long as the stock continues to climb up in a series of higher highs and higher lows, Roku seems destined to re-claim the $50 to $60 range it traded in during mid-September to early December.

WeBull Desktop

The neckline of the V-shaped reversal pattern is slightly above $60, and a breakout of that level could propel Roku’s stock back over $80, which would be a 70% move from current levels. As I see it, the $50-$60 range is certainly in play here (in the short-term), especially if Q4 earnings come in better than expected and management provides positive guidance for 2023.

The last time ROKU’s stock showed a similar reversal pattern was in late 2018, and here’s how it played out:

WeBull Desktop

From a technical perspective, Roku’s stock is showing positive momentum. And the recent active accounts and user engagement (streaming hours) data are encouraging.

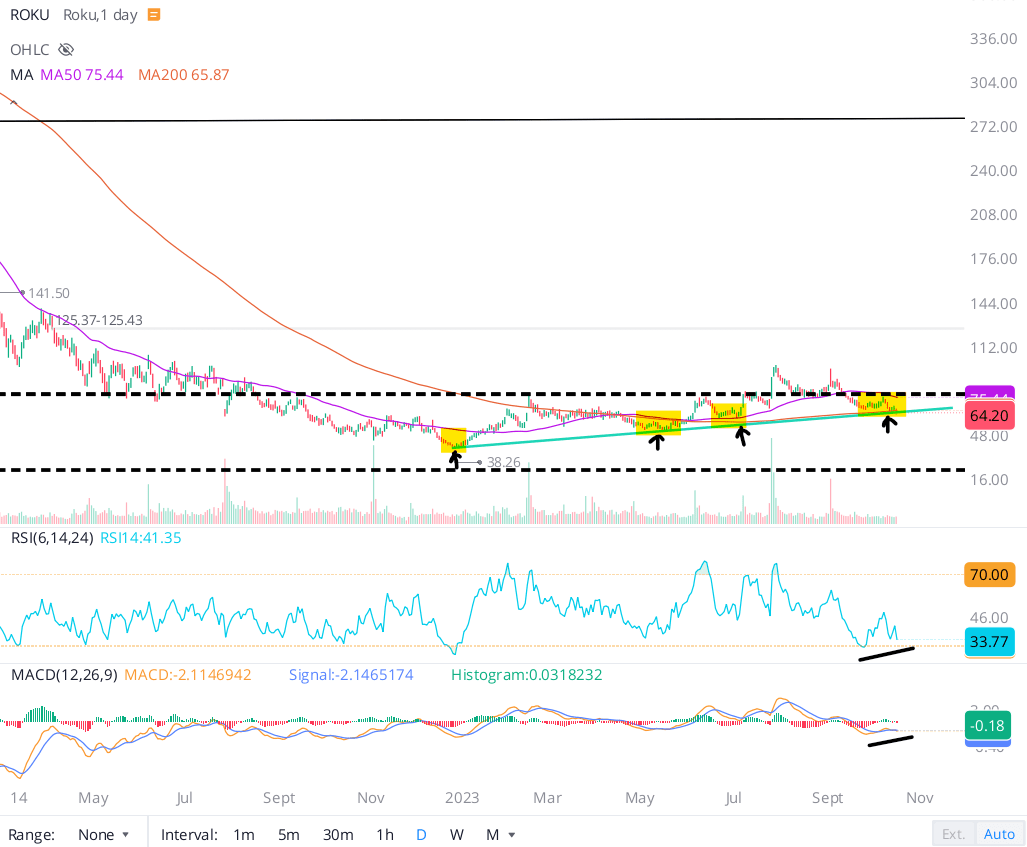

After a run to ~$98 per share by late July 2023, Roku stock has pulled back by -35% in recent weeks and now sits at the 200-DMA support level & the rising trendline (marked in green on the chart below). With daily RSI (nearly oversold) and MACD indicators showing positive divergence, Roku’s stock looks ripe for a bounce from current levels (low to mid $60s):

Roku stock chart (10/18/2023) (WeBull Desktop)

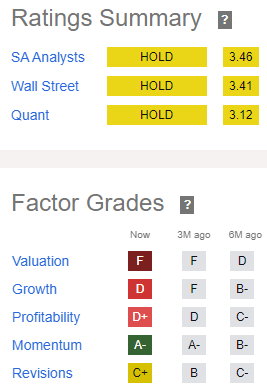

With the uptrend off of late 2022/early 2023 lows still intact, Roku’s technical momentum remains strong as evidenced by an “A-” quant factor grade for “Momentum” in SA’s Quant Rating system. That said, a technical breakdown here (amid a broader market decline) could easily open up a downside move to the $40-50s. Hence, Roku’s near-term technical setup is finely poised.

SeekingAlpha

Furthermore, Roku is currently rated a “Hold” with an overall score of 3.12/5 on SA’s Quant rating system due to weak (relative) grades for “Profitability”, “Growth”, and “Valuation”.

Final Thoughts: Is ROKU A Buy, Sell, Or Hold?

Given Roku’s recent financial performance (& near-term business outlook), unsupportive quant factor grades, and precarious technical setup, I wouldn’t recommend a short-term position in Roku stock. However, the long-term risk/reward for ROKU is lucrative (5-year expected CAGR: >35%), and bold active investors should utilize this rate-induced sell-off in Roku as a buying opportunity. As we saw in this note, Roku’s business fundamentals are improving underneath the surface [strong user growth & engagement], setting the business up for re-acceleration for when the ad market recovers.

In order to eliminate guesswork, I prefer using staggered accumulation via DCA plans and/or option-based risk mitigation strategies for Roku stock.

Key Takeaway: I rate Roku a “Strong Buy” in the $60s for long-term investors, with a preference for staggered accumulation and/or proactive risk management.

Thanks for reading. Please let me know if you have any thoughts, questions, or concerns in the comments section below.

Analyst’s Disclosure:I/we have a beneficial long position in the shares of ROKU either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

At The Quantamental Investor, we make investing simple, fun, and profitable. To get more market-beating stock ideas –> Click Here