Summary:

- Salesforce’s Q2 2023 results exceeded expectations, with total revenues and normalized EPS coming in at $8.6B (up 11% y/y) and $2.12 (up 78% y/y), respectively.

- Despite ongoing macroeconomic challenges, Salesforce is delivering profitable growth at scale, whilst investing aggressively to maintain its market leadership position in the era of AI.

- The stock is reasonably valued, and the risk/reward remains tilted in favor of long-term investors.

- Hence, I continue to rate Salesforce a “Buy” in the $210s.

Stephen Lam

Introduction

In my previous note on Salesforce (NYSE:CRM), we talked about its game-changing AI + Data + CRM partnership with Google Cloud (GOOGL) serving as the next leg of growth for the business:

Alphabet and Salesforce are two prominent technology companies, but they operate in different sectors and offer distinct products and services. As you may know, Alphabet focuses on internet services, digital advertising, cloud computing, and hardware, whereas Salesforce specializes in cloud-based CRM solutions for businesses.

While this new AI partnership between Salesforce and Google Cloud is mutually beneficial to both companies, (in my view) Salesforce’s stock and business are likelier to get bigger gains from this expanded partnership. Despite rapid growth in Google Cloud revenues, Alphabet continues to generate the bulk of its revenue (and almost all of its profits) through digital advertising. And given the sheer size and scale of Alphabet’s business, this partnership with Salesforce is unlikely to move the needle for Alphabet.

On the other hand, this strategic partnership with Google Cloud can unlock the next leg of growth for Salesforce and help fortify its position as the leading CRM provider in the era of artificial intelligence.

Source: Salesforce And Google: 2 Winning Tech Titans In A New AI Partnership, One Winning Stock

Last week, Marc Benioff hammered home Salesforce’s AI advantage at the Dreamforce 2023 conference. And recent news reports suggest that Salesforce is hiring 3,300 employees across departs as management’s confidence in a new AI-fueled tech investment cycle has grown. While some investors are rightly concerned about Salesforce’s recent profitability improvements amidst this news, CRM’s leadership remains committed to striking a balance between growth and profitability. Here’s what Benioff said at Dreamforce:

Our job is to grow the company and to continue to achieve great margins

– Marc Benioff, Salesforce CEO

In this note, we will review Salesforce’s Q2 2023 results and re-evaluate its fair value using TQI’s Valuation Model to see if it remains a buy.

Brief Review of Salesforce Q2 2023 Earnings

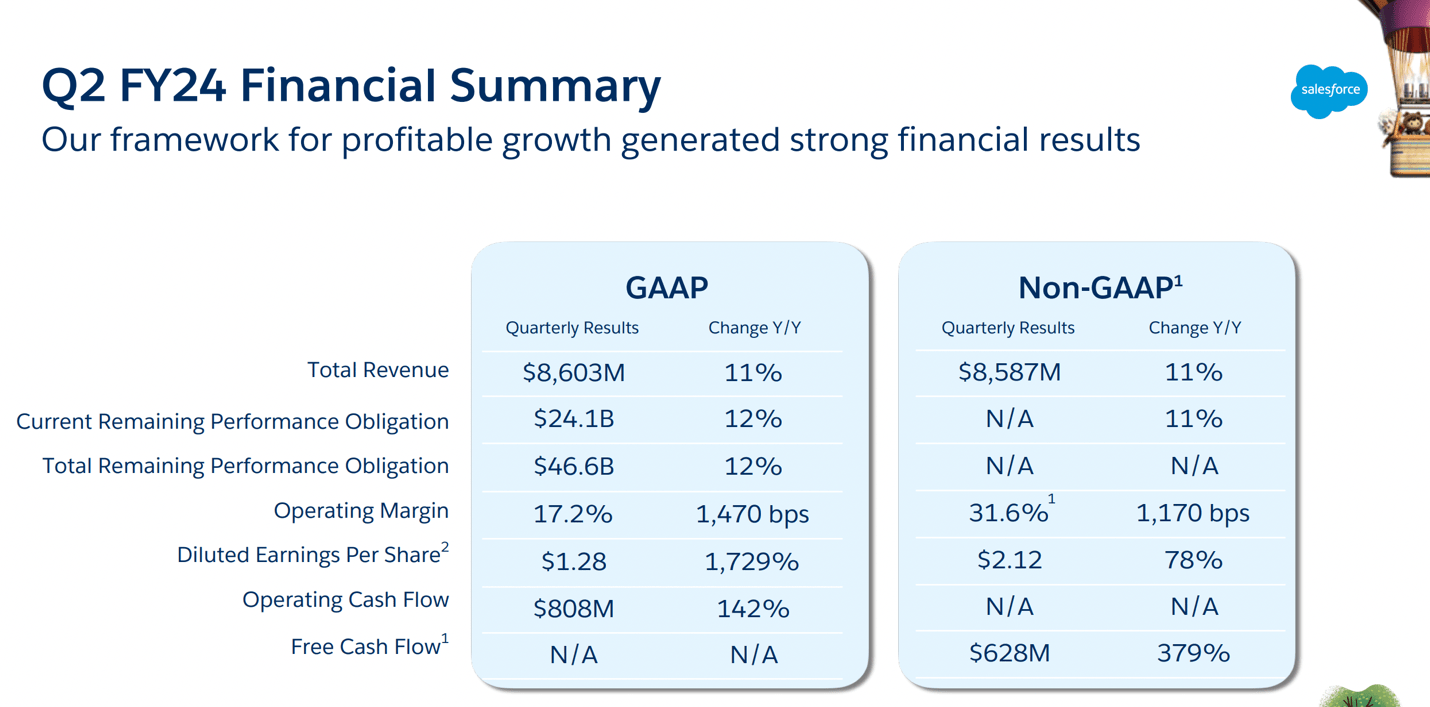

In Q2 2023, leading cloud software company Salesforce recorded total revenues of $8.6B (up 11% y/y), beating the high-end of management’s guidance range by $70M. Despite a stabilization of top-line growth at ~11% over the last couple of quarters, Salesforce is making great strides on the profitability front, with normalized EPS for Q2 coming in at $2.12 (up 78% y/y) well ahead of consensus street estimates of $1.90 by $0.22 per share.

Salesforce Q2 2023 Earnings Presentation

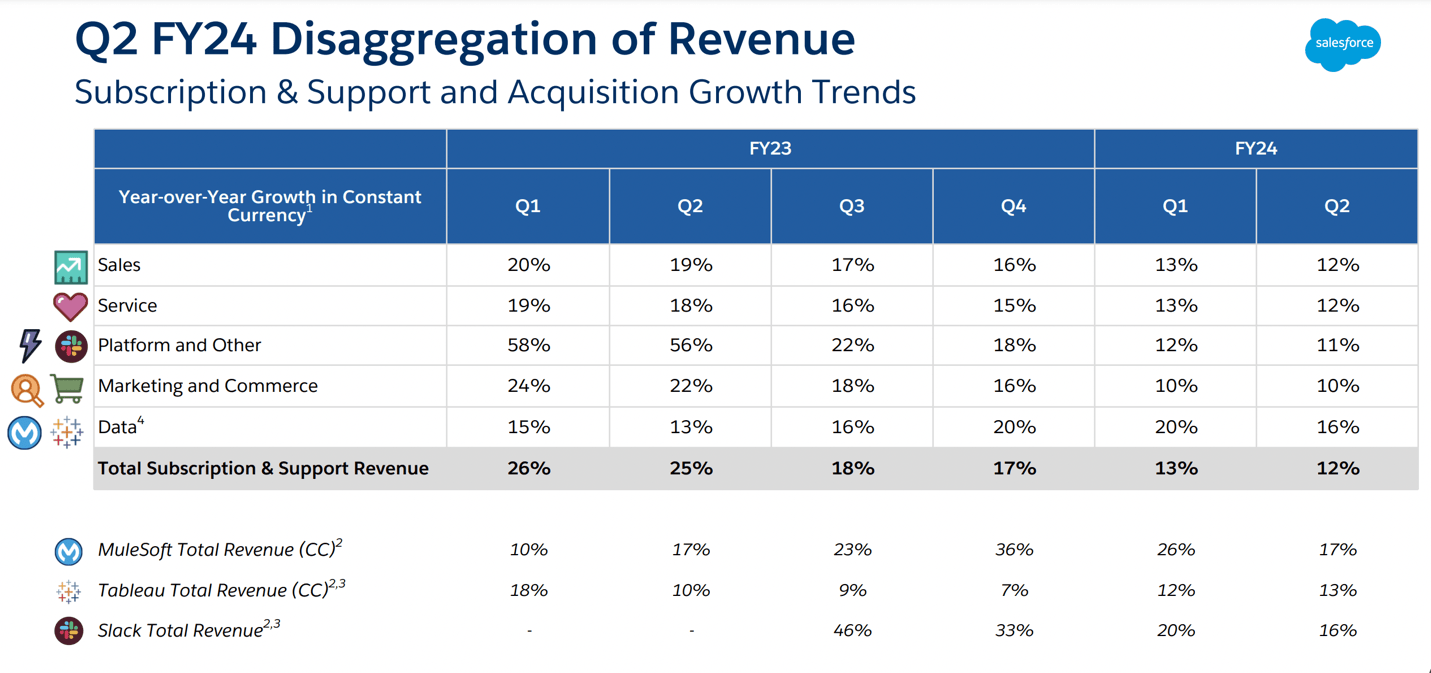

Amid ongoing macroeconomic challenges, Salesforce has reported a sharp moderation in growth since 2021-22, with the slowdown affecting all segments of its business as evidenced by the disaggregated revenue table shown below:

Salesforce Q2 2023 Earnings Presentation

While growth has moderated down to low-double-digits, Salesforce is racing to bring Einstein AI to the market in order to increase its share of wallet among existing enterprise customers in a ~$70B CRM software market that’s expected to grow at ~12% per year until 2030.

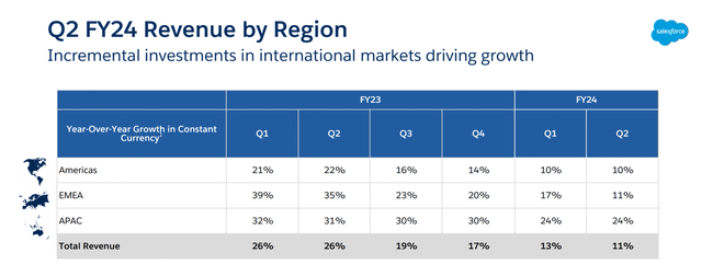

From the geographical standpoint, Salesforce’s revenue growth stayed resilient in the Americas (at 10% y/y) and APAC region (at 24% y/y), but moderated sharply in EMEA from the previous quarter.

Salesforce Q2 2023 Earnings Presentation

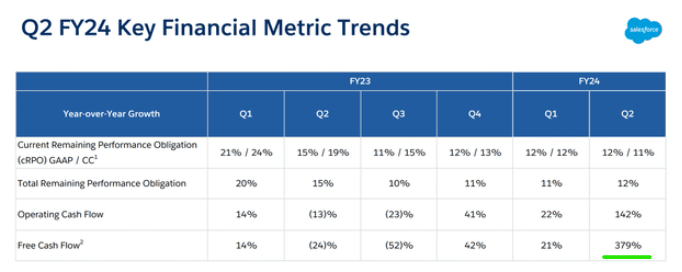

Over the last few quarters, Salesforce has made tremendous strides on the margin front as management embarked on cost-cutting exercises amid pressure from activist investors. In Q2 2023, Salesforce’s non-GAAP operating margins reached 31.6% [GAAP operating margins: ~17%], with significant moderation in CRM’s D&A and stock-based compensation expenses.

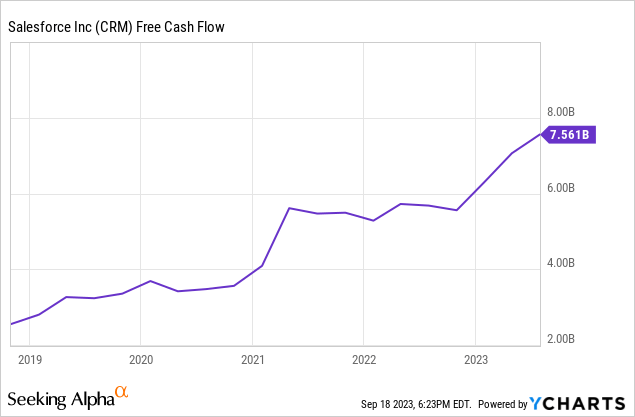

With healthy double-digit revenue growth and robust margin expansion, Salesforce has seen a big jump in its free cash flow generation over the last year or so. In Q2, Salesforce recorded operating cash flows of $808M (up 142% y/y) and free cash flows of $628M (up 379% y/y), owing to the cost-efficiency initiatives taken by the firm.

Salesforce Q2 2023 Earnings Presentation

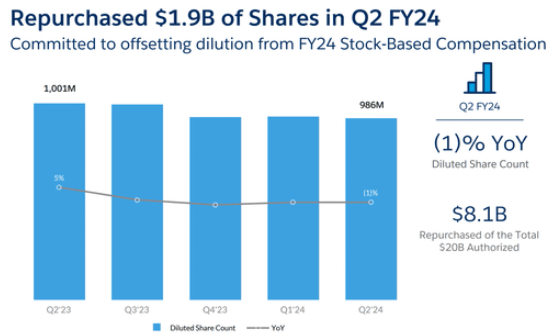

As you may know, Salesforce’s management adopted a shareholder-friendly stock buyback program last year, which has seen them return $8B to shareholders via stock buybacks over the last twelve months. In Q2 2023, Salesforce bought back $1.95B worth of its stock to bring total buybacks in the first half of this year to $4.1B.

Salesforce Q2 2023 Earnings Presentation

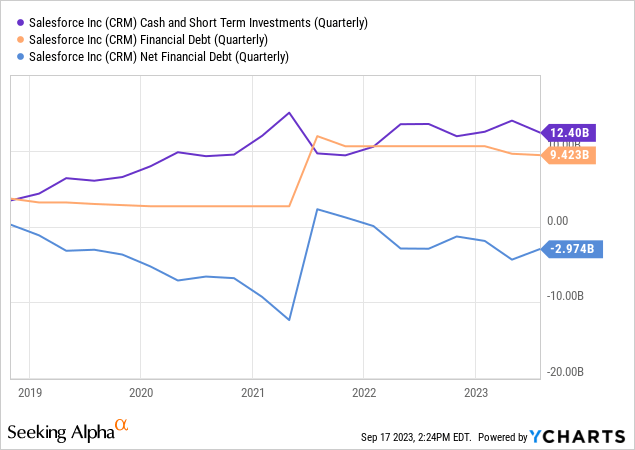

Salesforce is buying back its stock aggressively, and given its strong balance sheet, I expect the company to keep devoting future free cash flows toward share buybacks in the upcoming quarters too. As of Q2 2023, Salesforce held $12.4B in cash and short-term investments against financial debt of $9.4B, resulting in a net cash balance of $3B. Given its hefty net cash balance and robust free cash flow generation, I don’t see any liquidity issues at Salesforce for the foreseeable future.

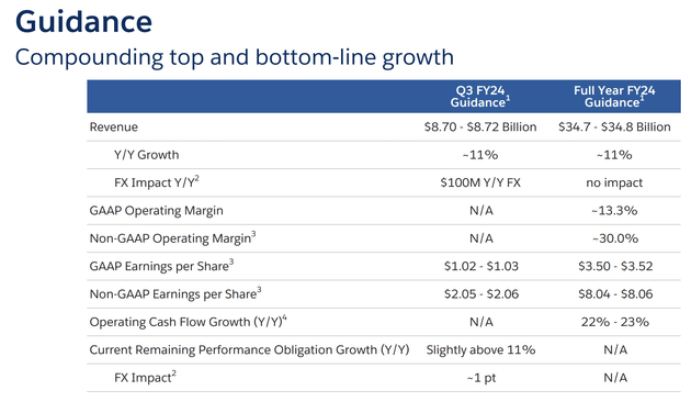

On the back of reporting yet another stronger-than-expected set of results, Salesforce’s management lifted their guidance for Q3 and FY-24. Here’s what Benioff had to say about this increase:

Based on our performance and what we see in the back half of the year, we’re raising our FY-24 revenue, operating margin, and operating cash flow growth guidance. As the #1 AI CRM, with industry-leading clouds, Einstein, Data Cloud, MuleSoft, Slack and Tableau, all integrated on one trusted, unified platform, we’re leading our customers into the new AI era.

Salesforce Q2 2023 Earnings Presentation

For Q3 2023, Salesforce is now expected to report $8.70-8.72B in revenue, which implies a y/y growth rate of 11%. Since this rate of growth is in line with the growth we have seen at Salesforce in H1 2023, we can say that Salesforce’s growth is stabilizing at ~11%, with no sign of re-acceleration just yet. Now, Salesforce’s rapid growth days are probably a thing of the past; however, I think Salesforce’s AI efforts have the potential to boost growth rates in the near-to-medium term and keep them elevated for several years to come. With all of this in mind, let’s determine Salesforce’s fair value and projected returns to see if it is a good buy here.

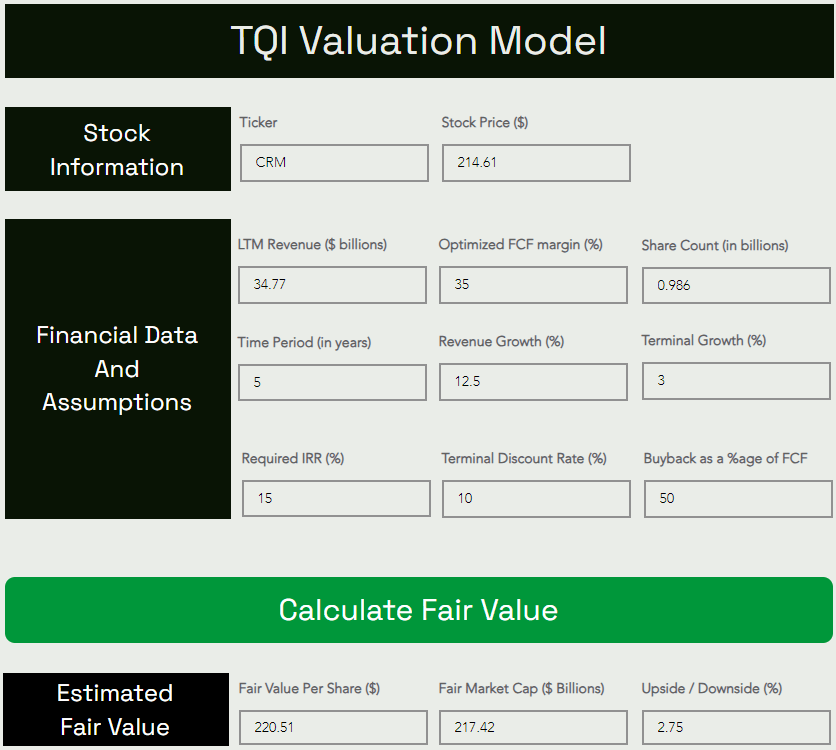

Salesforce Fair Value And Expected Return

Here is an overview of our valuation model assumptions and output for Salesforce:

TQI Valuation Model (TQIG.org) TQI Valuation Model (TQIG.org)

As you can see above, Salesforce is trading just under its fair value. With an expected 5-year CAGR of 18.9%, Salesforce easily beats my investment hurdle rate of 15%. Hence, Salesforce is a “Buy” at current levels under our proprietary valuation methodology.

Concluding Thoughts: Is Salesforce A Buy, Sell, or Hold Right Now?

Salesforce is the leading CRM player, and it looks well-positioned to maintain its leadership position in the era of AI. In Q2 2023, Salesforce beat top and bottom line estimates, and the outlook for H2 2023 remains healthy despite continued macroeconomic pressures.

Based on expected 5-year CAGR returns, Salesforce [18.9%] handily beats my investment hurdle rate of 15% and the stock is still slightly undervalued. While there are a lot of artificial intelligence wannabes out there, Salesforce is not one of them.

Key Takeaway: I rate Salesforce a “Buy” in the $210s.

Thanks for reading, and happy investing. Please share your thoughts, concerns, and/or questions in the comments section below.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of CRM, GOOGL either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Are You Prepared For Whatever The Market Throws At Us Next?

Your investing journey is unique, and so are your investment goals and risk tolerance levels. This is precisely why we designed our investing group – “The Quantamental Investor” – to help you build a robust investing operation that can fulfill (and exceed) your long-term financial goals.

To navigate this highly uncertain macroeconomic environment, we Qvestors [TQI community members] are pursuing bold, active investing with proactive risk management. Join our investing community and take control of your financial future today.