Summary:

- SMCI’s stock has suffered significantly after the resignation of its external auditor, Ernst & Young, casting doubt on the accuracy of its financial statements and raising red flags about controls.

- Publicly listed companies, such as Super Micro Computer, Inc., are mandated to have external auditors and internal audit committees to ensure accurate financial reporting and compliance with SEC and exchange regulations.

- SMCI has experienced delisting before, from 2018 to 2020, and if it fails to file audited financials timely, it risks being delisted again, which would reduce liquidity.

- Despite current issues, SMCI’s tangible book value suggests a baseline for its share price. A shift to more conservative accounting could paradoxically lead to higher P/E ratios and potentially higher share prices in the long term if investor trust is restored.

luza studios

Thesis

Super Micro Computer, Inc. (NASDAQ:SMCI) is a company heavily in the news as of late. After a massive surge earlier in the year which saw the stock up 300%, the name has cratered, now negative for 2024. SMCI falls in the ‘special situations’ case for us because it is a prime example of a company which is driven by non-standard factors. The latest blow to the name has been the resignation of its auditor, Ernst & Young, which has cast serious doubts regarding the validity of SMCI’s books and records.

In today’s article we are going to explore lesser known topics regarding SMCI, namely structural issues such as the impact of a delisting to investors, governance and regulatory factors, and our take on this special situations case.

Why do companies have auditors? Regulatory requirements.

Let us first take a step back and go to basics. A company, in essence, in an enterprise that produces widgets. A part of a company’s process is producing books and records (i.e. accounting statements of what it does). You might be surprised to find out that most private companies do not have auditors or audit functions, just internal accountants who prepare books and records (inventory, balance sheets, income statements, etc.)

A company’s accountants do not prepare financial statements for prospective shareholders, but they do it in order to pay taxes and fall within the governance standards imposed by each jurisdiction. Auditors come into play only when a third party wants to certify the books and records prepared by a company. Let us revisit what an auditor actually does:

An auditor is a person authorized to review and verify the accuracy of financial records and ensure that companies comply with tax laws.

An auditor is therefore a third party, independent of the company, who comes and ensures the books and records are in-line with accounting standards and with the receipts and internal documents presented by the company. If an enterprise presents a revenue figure of say $100, but only has a paper trail of signed contracts for $80 worth of goods, an auditor might force the enterprise to re-state its income statement and thus net profit. This is just an example, but as a reader, you should get the flavor of audit work. It represents a close review and verification of a company’s books and records by a third party.

As stated above, most private companies do not have auditors because there is no need to pay the expenses associated with auditors. If a company does not want to sell itself or is not listed on a public exchange, it does not have the need for somebody else to verify its books and records.

On the other hand, companies that have their shares listed on a public exchange and are regulated by the SEC, are required to have an external auditor:

Publicly traded companies are required to submit an external audit as part of their annual filings to the Securities and Exchange Commission (SEC). These can be found on the SEC’s Edgar database.

Furthermore, there are requirements regarding internal audit committees within said companies:

Audit committees of companies that are publicly traded in the United States are subject to rules of the Securities and Exchange Commission (SEC) and listing standards of the exchange on which the company’s securities are listed, such as the New York Stock Exchange (NYSE) or Nasdaq. These include rules and standards related to committee composition, the charter, and committee evaluations. Indirectly, audit committees may be subject to additional requirements resulting from rules and standards for independent auditors under the Public Company Accounting Oversight Board (PCAOB).

The takeaway from this section is that listed companies have a higher standard, which includes the need for external auditors and internal company committees to ensure the books and records are correct. At the end of the day, the regulators want to ensure there is oversight over what a listed company does, and the presented books and records are fair and accurate.

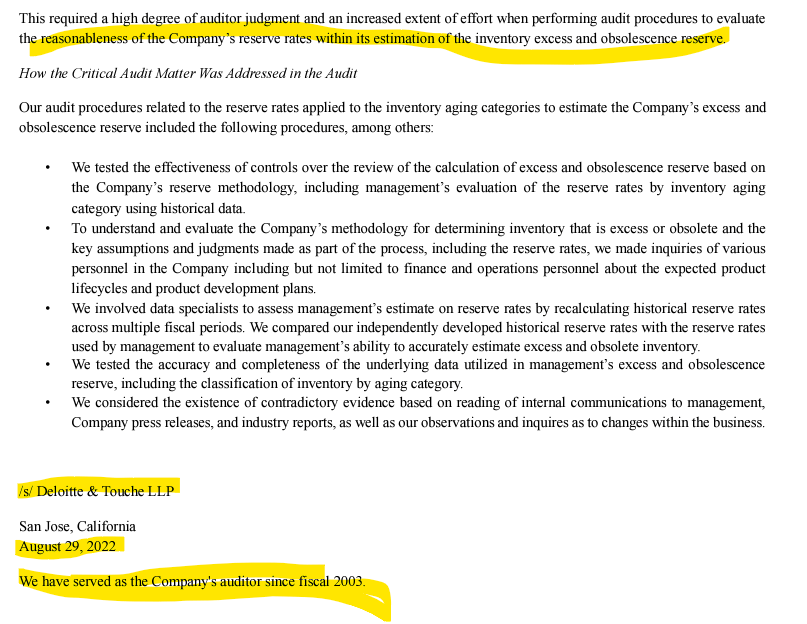

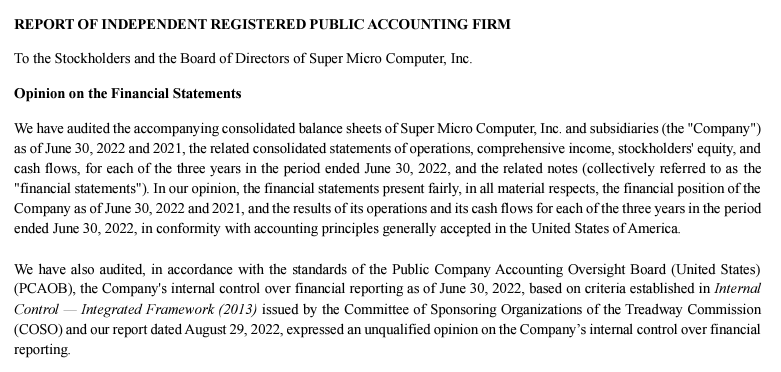

Who is SMCI’s auditor? It was Deloitte before Ernst & Young.

Prior to Ernst & Young, Deloitte served as an external auditor since 2003:

Annual Report Audit Opinion (Annual Report)

Deloitte was of the opinion that the financial statements for the periods ending June 2021 and June 2022 presented figures in accordance with accounting practices:

Annual Report Audit Opinion (Annual Report)

What happens next, then? SMCI will need an external auditor and a re-thinking of internal audit controls in order to continue being a publicly listed company. They need to find a new external auditor and solve their issues.

External factors to consider

SMCI is doing all that it can to buy itself time and bring in a new team of auditors to satisfy the Nasdaq requirements and its bank covenants:

Super Micro Computer (SMCI) has announced an amendment to its loan agreement with Cathay Bank that, among other things, extends the date by which the company is required to deliver its annual results.

The amendment allows Super Micro (SMCI), which has been grappling with financial reporting and governance issues, to extend the deadline to file its audited financial statements for its fiscal year ending June 30, 2024, from Oct. 28, 2024 to Dec. 31, 2024. It also extends the date by which the company is required to report its balance sheet and income statement for its fiscal quarter ending Sept. 30, 2024, from Nov. 29 to Dec. 31.

Please note that from a Nasdaq perspective, the company needs to get approval for a later submission date, approval which can buy up to 180 days:

September 20, 2024 SAN JOSE, Calif.–(BUSINESS WIRE)– Super Micro Computer, Inc. (SMCI) (“SMCI” or the “Company”) announced that the Company received a notification letter from Nasdaq stating that the Company is not in compliance with Nasdaq listing rule 5250(c)(1), which requires timely filing of reports with the U.S. Securities and Exchange Commission. The September 17, 2024 letter was sent as a result of the Company’s delay in filing its Annual Report on Form 10-K for the period ending June 30, 2024 (the “Form 10-K”). The Form 10-K was due on August 29, 2024. The Company filed a Form 12b-25 on August 30, 2024.

Under the Nasdaq rules, the Company has 60 days from the date of the notice either to file the Form 10-K or to submit a plan to Nasdaq to regain compliance with Nasdaq’s listing rules. If a plan is submitted and accepted, the Company could be granted up to 180 days from the Form 10-K’s due date to regain compliance. If Nasdaq does not accept the Company’s plan, then the Company will have the opportunity to appeal that decision to a Nasdaq hearings panel.

Under the theoretical assumption that a plan is submitted and approved, SMCI would have 180 days from the 10-K due date, i.e. from August 29, 2024.

Can SMCI get delisted? What are the implications?

Investors might be surprised to find out that SMCI was delisted before, notably from 2018 to 2020:

SAN JOSE, Calif., Aug. 23, 2018 – Super Micro Computer, Inc. (SMCI) (the “Company”), a global leader in high performance, high-efficiency server, storage technology and green computing, today announced that, as expected, the Company received a notification letter from The Nasdaq Stock Market Hearings Panel (the “Panel”) on August 22, 2018, indicating that trading in the Company’s common stock on Nasdaq’s Global Select Market will be suspended effective at the open of business on August 23, 2018. The Company previously announced on August 21, 2018 that it did not expect to regain compliance with the Nasdaq continued listing requirements by August 24, 2018, the deadline previously set by the Panel.

A company being delisted from a stock exchange does not equate to bankruptcy. It simply means the shares of the company will not benefit from the liquidity and distribution capacity of a large exchange. SMCI’s shares went on to be listed OTC (over the counter) after its Nasdaq delisting:

SMCI Price Aug 2018 – Jan 2020 (Seeking Alpha)

The company was relisted on the Nasdaq in January 2020:

SAN JOSE, Calif. – January 9, 2020 (BUSINESS WIRE) — Super Micro Computer, Inc. (SMCI), a global leader in high-performance, high-efficiency server, storage technology and green computing, today announced that The Nasdaq Stock Market LLC (“Nasdaq”) has approved its application for relisting of the Company’s common stock on the Nasdaq Global Market. It is expected that the Company’s common stock will begin trading at the opening of trading on or about January 14, 2020 under the ticker symbol “SMCI”.

While a delisting does not equate to bankruptcy or the end of trading of shares, it does mean less liquidity, a lower P/E level (and implicitly price) and less interest in a company, all while large indices will remove the stock from their composition. Please note below the S&P 500 Index stock inclusion requirements:

S&P 500 Methodology for Inclusion (S&P 500 Methodology Paper)

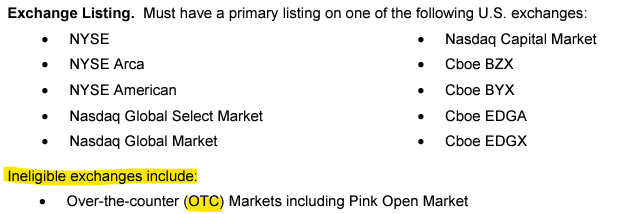

As noted in the index methodology, equities traded OTC are not eligible for inclusion. The Nasdaq-100 index has a similar requirement:

Nasdaq eligible exchange (Nasdaq methodology paper)

A company moving to OTC from the Nasdaq would then become ineligible for the Nasdaq-100 index.

Our take on this ‘Special Situations’ case

Readers need to understand that accounting standards allow for various recognition methods and standards, and certain companies might pursue a more aggressive interpretation of certain provisions. We do not know what is actually happening, and only auditors do. Now Deloitte is on the hook for past financial statements, and SMCI itself has been very prescriptive around stating that past income statements will not be re-stated.

Assuming theoretically that the company was overly aggressive around revenue recognition, this simply translates into lower future EPS figures, a fact which in and of itself is not that bad. Let us take a look:

EPS Estimates (Seeking Alpha)

The above table represents the Seeking Alpha EPS estimates compiled from various external analysts. Let us look at 2026 – the EPS estimate here is $4.38 per share. Let us theoretically assume for example purposes that under a very conservative accounting standard, the EPS goes down to $2.2/share. When looking at other semiconductor companies, the share price using a 20x and 30x multiple is as follows:

- Share price at 20x is $44/share

- Share price at 30x is $66/share

The point here is that the market is already embedding lower EPS via its very low P/E assigned to the company. In effect, under this theoretical scenario, the company would have achieved a higher share price by being more conservative from an accounting standpoint!

From a fundamental perspective, we are of the opinion that the company’s balance sheet is ‘clean’, with issues only in the income statement. Therefore, the reported tangible book value per share of $9.32 is real and can be considered a theoretical floor for the shares. Furthermore, we think that the switching to a more conservative accounting view might perversely result in higher prices for the equity, since the market will revert to a higher P/E ratio even if the EPS might decrease. Again, these are only speculations and our view, and the market will get an answer when a new auditor is brought in and audited financial statements are released.

Conclusion

SMCI has been a tech darling in 2024, with an astounding stock move of 300% earlier in the year. With issues around its internal governance and financials, the company saw its stock price crater, especially after its external auditors resigned. If the company is not able to file audited financials with the SEC and Nasdaq, it will get delisted. A retail investor might be surprised to find out that SMCI has been delisted before, notably from August 2018 to January 2020. Delisting does not mean bankruptcy, but simply the move to OTC trading, where liquidity and volumes are low. Upon delisting from the Nasdaq (theoretical) the company would be removed from all the market-based indices, thus putting further pressure on share price. Having vetted financials and robust internal controls are regulatory requirements for a publicly listed company, and represents a way for regulators to ensure the public has access to fair and transparent financials.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.