Summary:

- Snowflake’s disruptive data analytics and machine learning capabilities make it a strong investment opportunity.

- The company’s growth in large customers indicates increasing adoption of data cloud and analytics in the industry.

- Snowflake’s conservative growth forecast for FY25 is likely to be surpassed due to factors such as strong retention rates and sales growth in large enterprises.

Monty Rakusen/DigitalVision via Getty Images

I discussed my bullish view on Snowflake (NYSE:SNOW) in my initiation article published in June 2023, favoring their disruptive data analytics and machine learning for siloed data. I continue to believe Snowflake can continue expanding their data cloud capabilities, powering data sharing, analytics and marketplace listing, etc. I reiterate a ‘Strong Buy’ rating with a one-year price target of $229 per share.

Data Cloud Growth in Large Customers

Snowflake offers a single, self-managed and programmable platform to manage data cloud across different cloud services. As depicted in the chart below, Snowflake delivered 35.9% revenue growth and 39.7% growth in the total number of large customers with more than $1 million in product revenue in the trailing 12 months.

Snowflake 10Ks

The growth in the number of large customers is crucial for Snowflake’s long-term growth prospectus, indicating the industry’s increasing adoption of data cloud and analytics, in my opinion. Enterprises are investing heavily in AI workloads, as evidenced by the explosive growth of GPUs powered by Nvidia (NVDA) and AMD (AMD). TechTarget argues that businesses are putting machine learning at the center of their business models, and AI technology could be used in numerous use cases including recommendation engines, fraud detection, customer analysis, financial trading, and virtual assistance, etc. All these use cases require data cloud and data analytics to feed the related AI models. I think the structural growth in AI will continue to propel Snowflake’s strong business growth in the near future.

I believe large enterprises and hyperscalers are the early adopters of AI technology; therefore, Snowflake has been experiencing strong growth in their large customer base. During their Q4 FY24 earnings call, their management indicated that they have begun to see more large multi-year contracts from the second half of FY24.

Recent Result and Conservative Growth Forecast For FY25

Snowflake released their Q4 FY24 result on February 28th with 31.5% revenue growth and 116.5% adjusted operating income growth. The total number of large customers with more than $1 million in product revenue in the trailing 12 months increased to 461, representing a 39.7% year-over-year growth. For the full year, they generated $778 million of free cash flow and repurchased $591 million of own shares. Overall, they maintain solid revenue and free cash flow growth momentum.

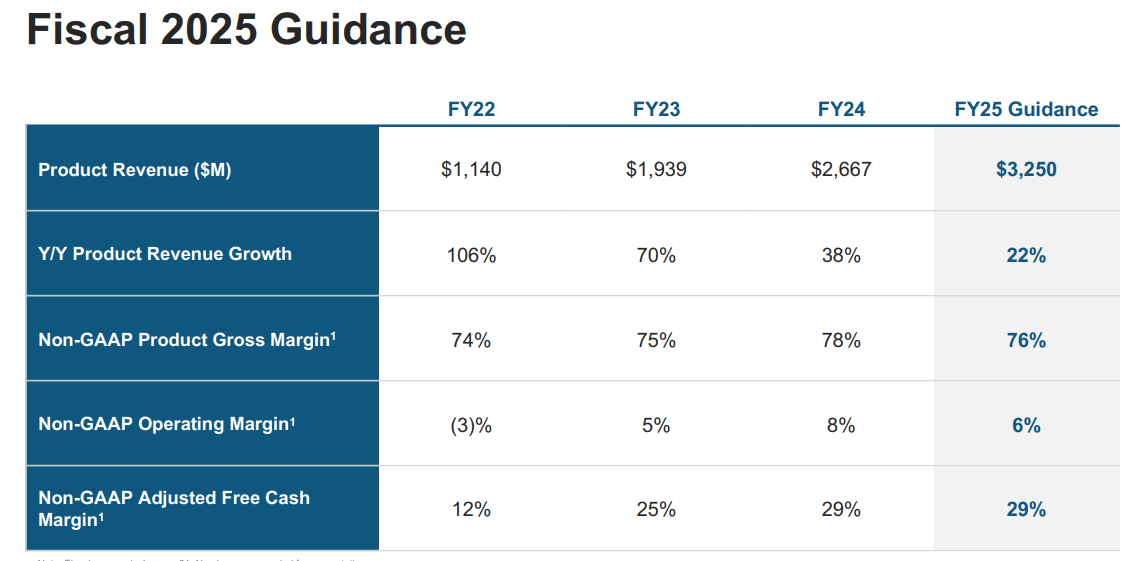

Snowflake guides 22% product revenue growth for FY25, as detailed in the slide below.

Snowflake Investor Presentation

Snowflake achieved 70% product revenue growth in FY23 and 38% in FY24; therefore, the guidance of 22% appears quite conservative, assuming there is no significant macro environment change in FY25. I consider the following factors:

As disclosed over the earnings call, Snowflake has $5.2 billion in remaining performance obligations (RPO) at the end of FY24, and they expect 50% of these RPOs will be recognized as revenue in the next 12 months. Consequently, Snowflake is going to generate $2.6 billion of revenues from these remaining obligations.

As shown in the chart below, Snowflake has been delivering a net revenue retention rate of above 130% over the past period. The strong retention rate is driven by Snowflake’s efforts to migrate additional customer workloads to Snowflake’s platform and increase customers’ consumption. As discussed in my initiation report, Snowflake has been investing heavily in R&D, launching more product features around their data cloud platform. The expansion of their data cloud enables the company to achieve higher consumption by their large enterprise customers and a higher retention rate. The strong retention rate would be attributed to Snowflake’s growth from existing customers in FY25.

Snowflake Investor Presentation

Lastly, Snowflake should continue to benefit from their sales growth in large enterprises. In FY24, the number of large customers increased by 39.7% year-over-year. For large enterprises customers, Snowflake could benefit more from workload migration and increasing consumption, in my opinion.

As such, assuming spending patterns of enterprises data cloud remain stable, I think their product revenue growth guidance is quite conservative.

Valuation

As discussed, I anticipate Snowflake will continue their strong growth momentum, driven by large customer growth, high retention rate and data cloud expansion. I assume they will deliver 30% revenue growth in the next few years. Fortune Business Insights predicts that the data analytics market will grow at a CAGR of 27.3% from 2023 to 2030. Consequently, I believe Snowflake will benefit from the rising demand for data cloud.

As shown in the slide below, Snowflake’s operating leverage has been coming from sales and marketing, as well as G&A expenses. They achieved 7% margin improvement over the past two years, driven by revenue growth and larger renewal mix towards lower commissions.

Snowflake Investor Presentation

I assume their operating margin will be expanded by the following moving pieces: gross margin expanding by 250bps annually, S&M improving by 320bps, and G&A expanding by 50bps. The assumptions for operating expenses are consistent with their historical average.

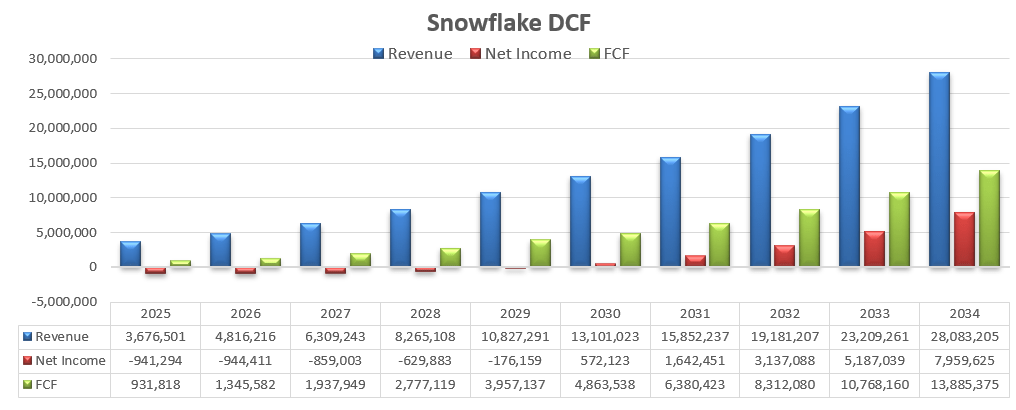

Snowflake DCF – Author’s Calculation

The model uses a 2-stage FCFE model, and the calculation of free cash flow to equity can be found in the table below:

Snowflake DCF – Author’s Calculation

The cost of equity is estimated to be 14.6% with the following assumptions:

-risk-free rate: 4.22%. 10-Y gov yield

-market risk premium: 7%

-beta: 1.49. SA’s 24-month data

Discounting all the future FCFE at a discount rate of 14.6%, the one-year price target is calculated to be $229 per share, as per my calculation.

Key Risks

Snowflake announced their CEO change in February 2024, and Sridhar Ramaswamy has become CEO. Since he joined Snowflake in 2023, Sridhar has successfully led the launch of Snowflake Cortex. It is worth noting that he brings strong leadership experiences from Google (GOOGL) and Neeva to Snowflake. However, he is relatively new to Snowflake, and investors need to pay attention to his strategic plan and action plans in the near future.

Snowflake allocated $1.16 billion in stock-based compensation in FY24, representing 41.6% of total revenue. The SBC ratio could be one of the highest among software companies. Although it is likely that the SBC as a percentage of total revenue will decrease over time when their business scales, the high payout would impact their GAPP margin expansion in the near future. Additionally, the assumption of margin expansion in my DCF model relies on the declining ratio of SBC as a percentage of total revenue.

Over the earnings call, Snowflake’s management indicated that they have been competing against Databricks on some large enterprise deals. While Databricks remains a private company, their lakehouse platform is competing against Snowflake head-to-head. I suggest investors monitor Snowflake’s growth in large customer deals, consumption growth and net retention rate.

Conclusion

I admire Snowflake’s technology in data cloud market, and their heavy investment in R&D has been expanding data analytics offerings in the growing data cloud market. It remains one of the core growth stocks in my portfolio. I am confident that they will deliver above 30% revenue growth in the near future. I reiterate a ‘Strong Buy’ rating with a one-year price target of $229 per share.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of SNOW either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.