Summary:

- Amazon’s stock has performed very well this year so far, but I expect it to continue its upward trend.

- The company’s long-term strategy and “bar-bell” business model will continue to contribute to the stock’s success in the long term.

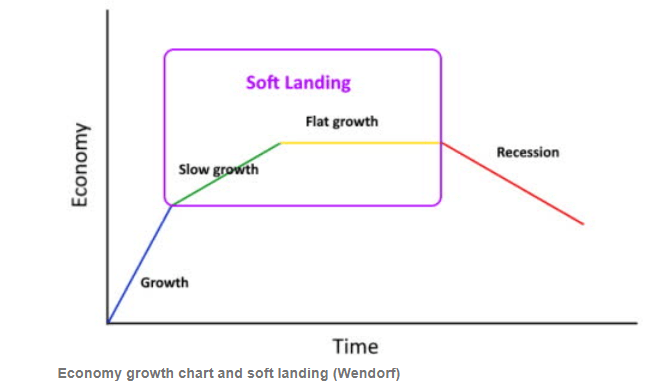

- Amazon’s North America segment is predicted to perform well in a soft- or no-landing scenario for the US.

- The firm’s sprawling nature makes it much better to compete in the age of AI than recent headlines around Generative AI would suggest.

Dan Kitwood

Amazon (NASDAQ:AMZN) is one of the world’s largest companies, and it has a storied history of rewarding shareholders on their unlikely journey from a pioneering online bookstore to the second-largest employer in the United States. Unlike many Megacap Tech peers, Amazon’s rise was much more controversial. It used to be known as the most hated stock on Wall Street. And, of course, the firm has had a prolific run this year. The natural question is whether the run can continue in the last part of the year. I’m convinced it can.

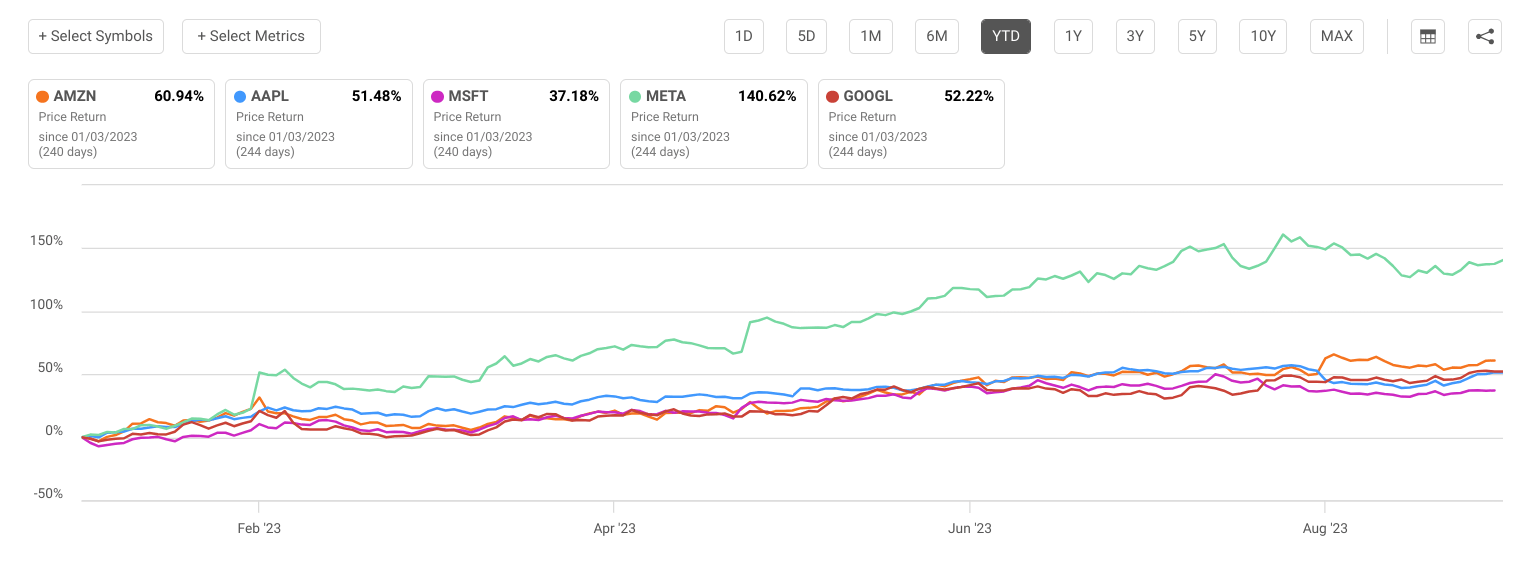

Seeking Alpha

As you can see, aside from Meta, the stock has performed the best of the Tech Titans on a YTD basis. However, I always think there’s much to learn from looking at any stock and its significant peers over several different periods. Amazon has ebbed and flowed over the years, but one of the significant lessons of the prolific rise of Technology in the US stock market and worldwide has been to be a long-term owner of Amazon.

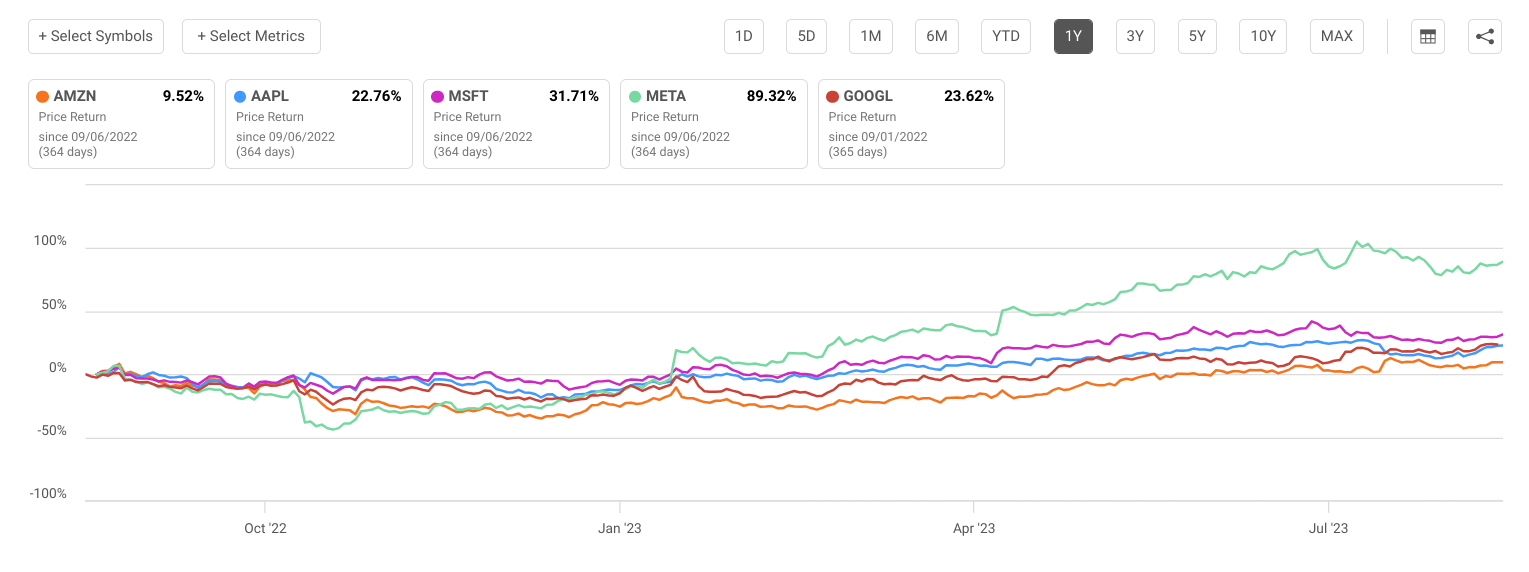

Seeking Alpha

The firm has actually lagged a bit on a 1-year basis compared to peers. To me, this is actually an encouraging fact. It makes it more possible that the recent performance on a YTD basis could be a more sustainable uptrend. But of course, you only have to look at the very long term to see that Amazon is a stock you want to own over the long term that has given the best stocks in history a run for their money.

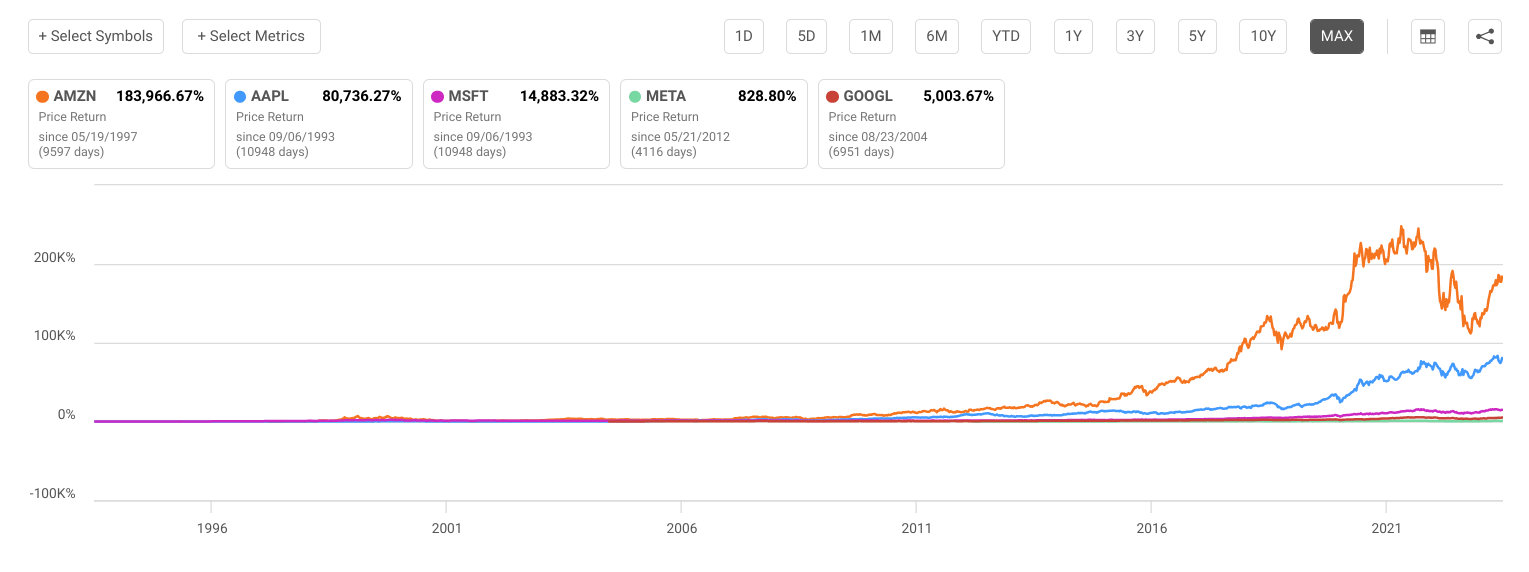

Seeking Alpha

Another thing to remember about Amazon is that it is a complex business that is hard to understand. But, in this fact, a major strength of the company also lies: it is an all-in-one barbell. The AWS segment has high growth and high margins, while the other parts of the business have razor-thin margins, high revenue, and relative stability. It has the benefits of a fast-growing, high-margin segment in AWS, but it also has businesses that will make money throughout the cycle and grow at much more subdued but consistent rates.

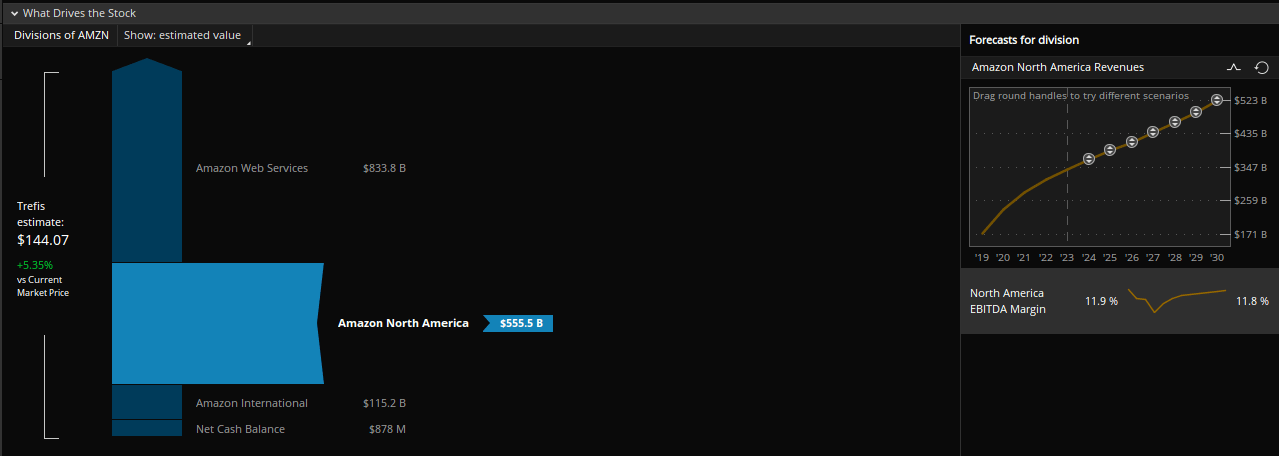

ThinkOrSwim

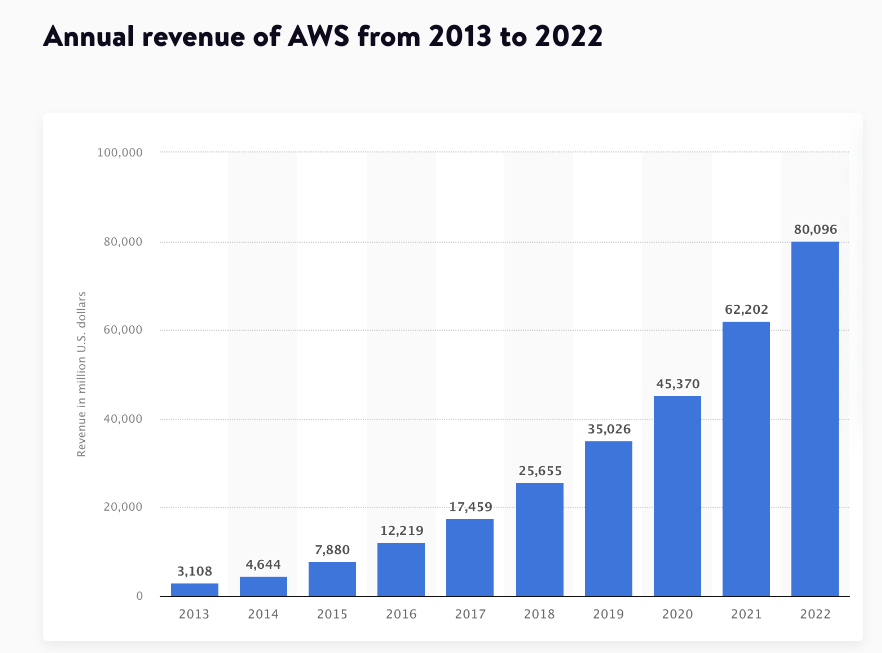

Despite the massive size in revenue of the sprawling giant, its main growth driver of cloud has fantastic margins and double-digit revenue growth. An important fact to remember about Amazon’s stock is that the AWS segment comprises the least proportional amount of revenue but is responsible for the lion’s share of proportional valuation. This is because it is the highest growth segment and also has the highest margins.

Kinsta.com

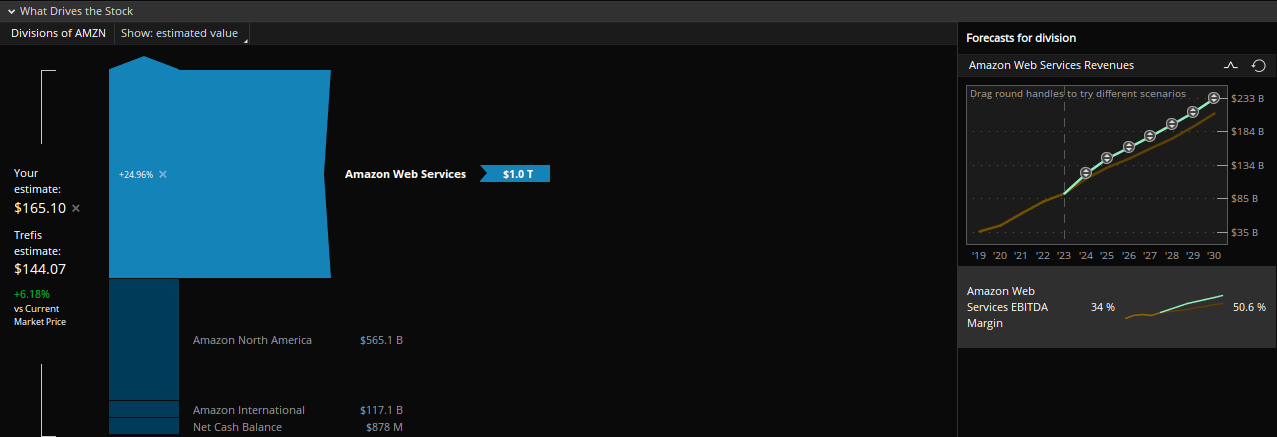

For example, in the Trefis model above, AWS constitutes 55% of the price estimate, while the prodigious Amazon North America only constitutes 37% of it despite most revenue coming from it. This means that relatively small forecasting errors in the AWS segment can lead to considerable differences in potential earnings power. As you can see, when I modify the forecast to be about 10% higher at the end of the period, it has a measurable effect on the implied intrinsic value of Amazon.

ThinkOrSwim

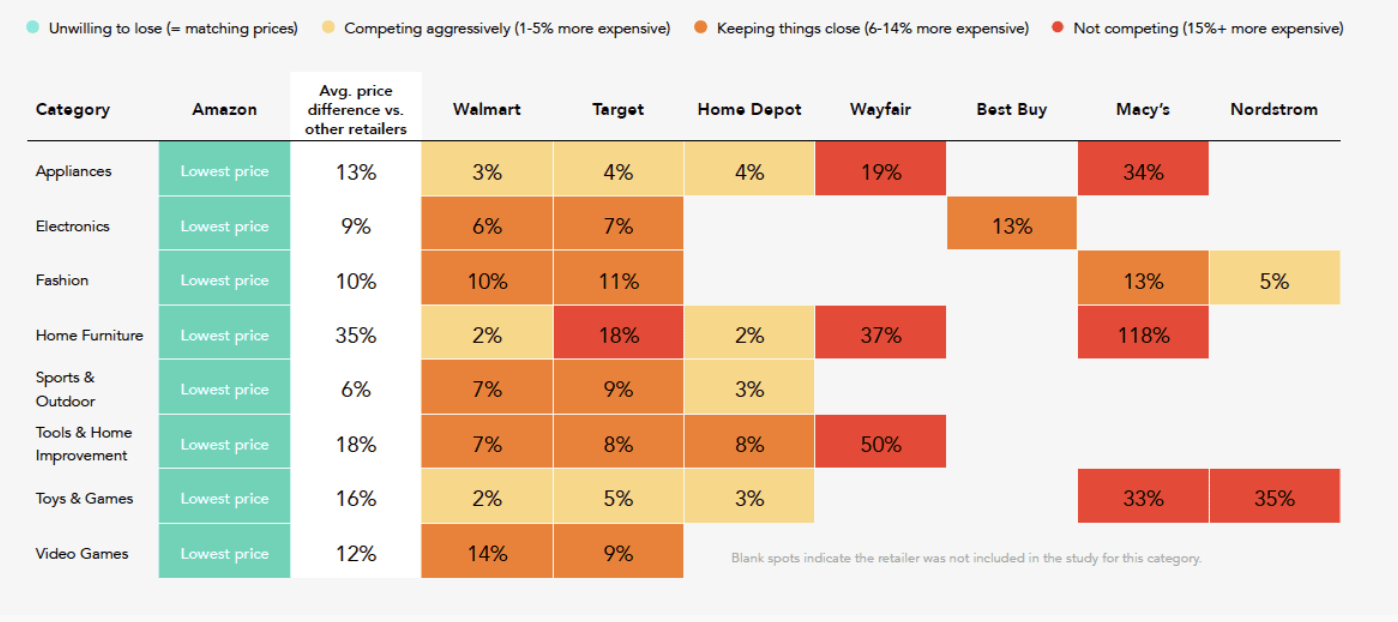

Many assume Amazon is on its heels in the cloud, but if this assumption proves incorrect, the stock likely has a lot of upside in the coming months. Indeed, the recent earnings report suggested cloud concerns may be in the rearview mirror. What I really like about the stock is that I think potential strength in the cloud will co-occur with strength in its retail/e-commerce section. Price becomes a more prominent consideration for consumers in an environment of slowing growth, and Amazon obviously has the advantage on price.

ThinkOrSwim

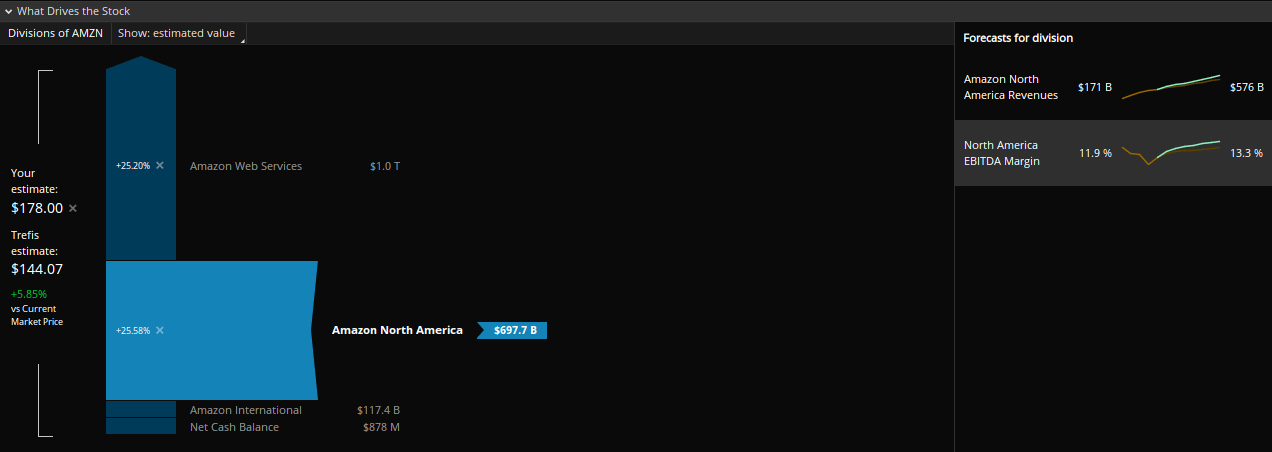

Amazon’s North America segment’s extensive and lumbering asset profile was definitely a downside during COVID-19. Still, many of Amazon’s more traditional assets should outperform and grow faster than expected if the soft landing scenario I expect comes to fruition. You can see above how lucrative the potential impact of better AWS performance and better-than-expected performance in the North American segment could affect the share price.

Amazon North America Should do Particularly Well in a Soft or No Landing Scenario for US

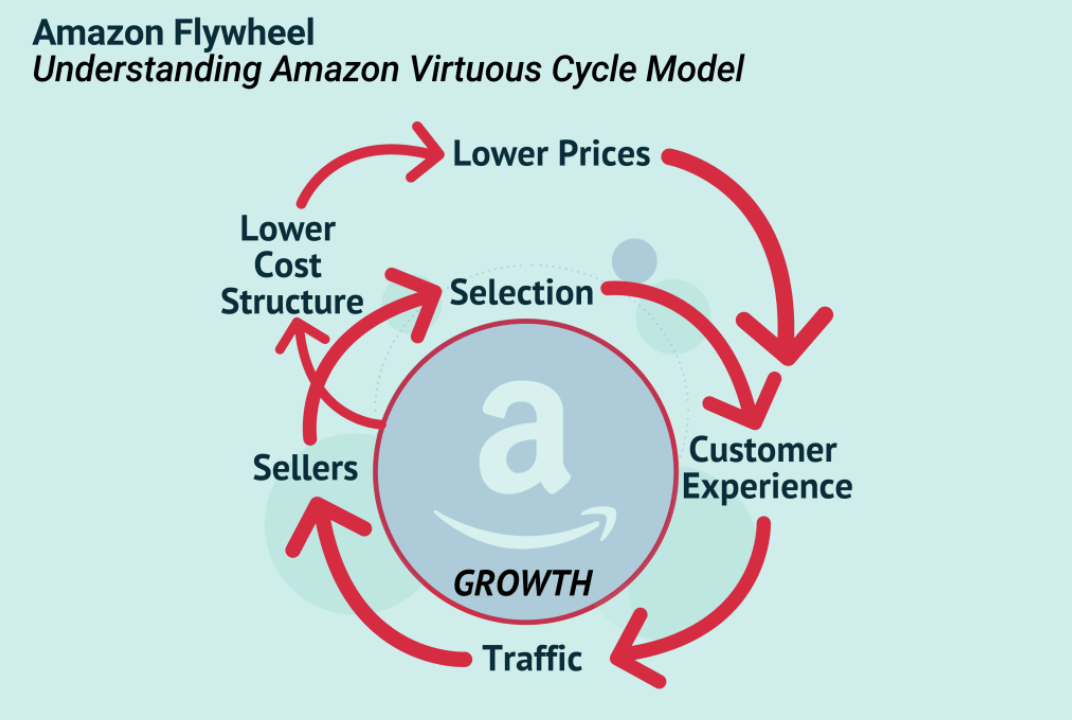

Those who have doubted Amazon in the past have been brought out on stretchers, and I don’t think now that the stock dominates much of the high ground in the US economy, it is time to start siding with those doubters. It always prioritized long-term strategy and revenue growth over short-term profitability. This strategy has been validated, but its fruits are only starting to be fully realized.

FourWeekMBA.com

And while the massive assets acquired and business models checkmated over the years are cumbersome in hard times like pandemics, they are nice to have during periods of economic strength. Amazon’s seamless integration of the grocery experience at Whole Foods into its Prime Membership ecosystem is a testament to this.

Seeking Alpha (Wendorf)

The firm’s competitive strategy always revolved around margin-eating races to the bottom on price, and it has been accused of lacking expertise in areas where it made huge acquisitions. It spread through the economy to dominate areas many would have never imagined twenty years ago. But in a soft landing, the massive infrastructure and footprint it has invested in become particularly lucrative as price consciousness likely grips the consciousness of the US consumer in the coming months.

Digital Commerce 360, Profitero

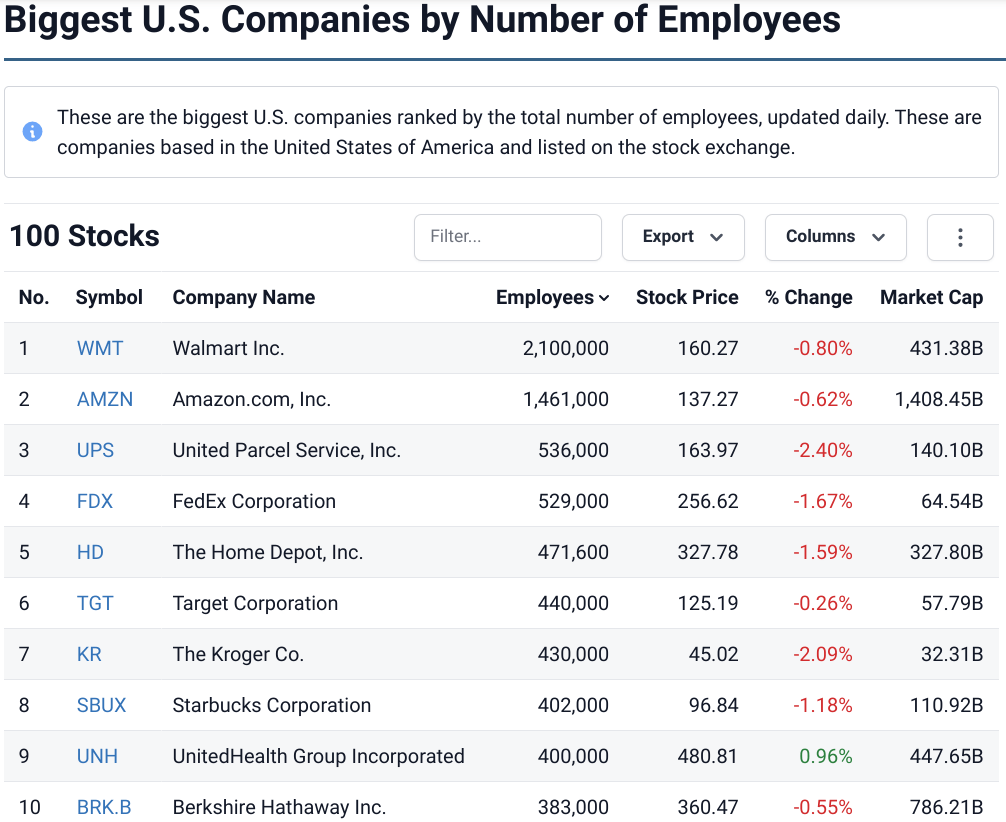

The firm now has an asset footprint larger than most nation states, owns vast quantities of land and warehouses, fleets upon fleets of trucks, and about a million and a half employees. But of course, in addition to its massive e-commerce and retail footprint, Amazon also has the incredible growth of cloud in its prolific AWS segment.

There were significant concerns in April about a potential cloud slowdown after the company issued tepid guidance in its most important segment for growth. However, those concerns were alleviated by the recent earnings report, which showed unexpected strength in cloud demand and suggested a trough in spending may be in the rearview mirror.

Risks and Where I Could be Wrong

With size comes risk, and of course, those risks can be magnified if they affect the costs of core operations. Amazon now employs a million and a half people, and its cost consciousness has run up against the interests of its workers. While efforts to organize at Amazon have primarily died in the crib, there is a chance that changing dynamics in our society that favor organized labor will eat into the already thin margins that the firm is famous for.

stockanalysis.com

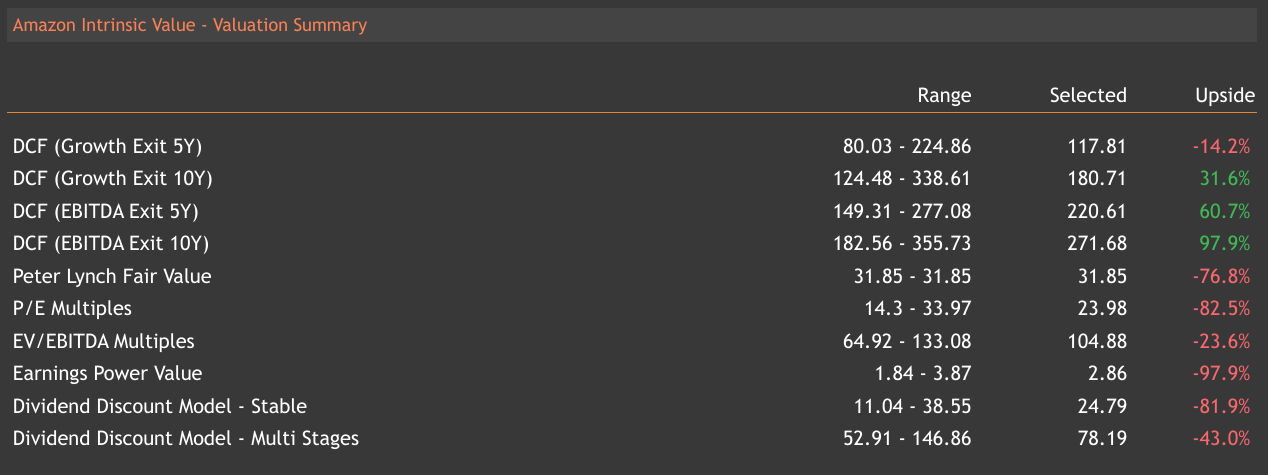

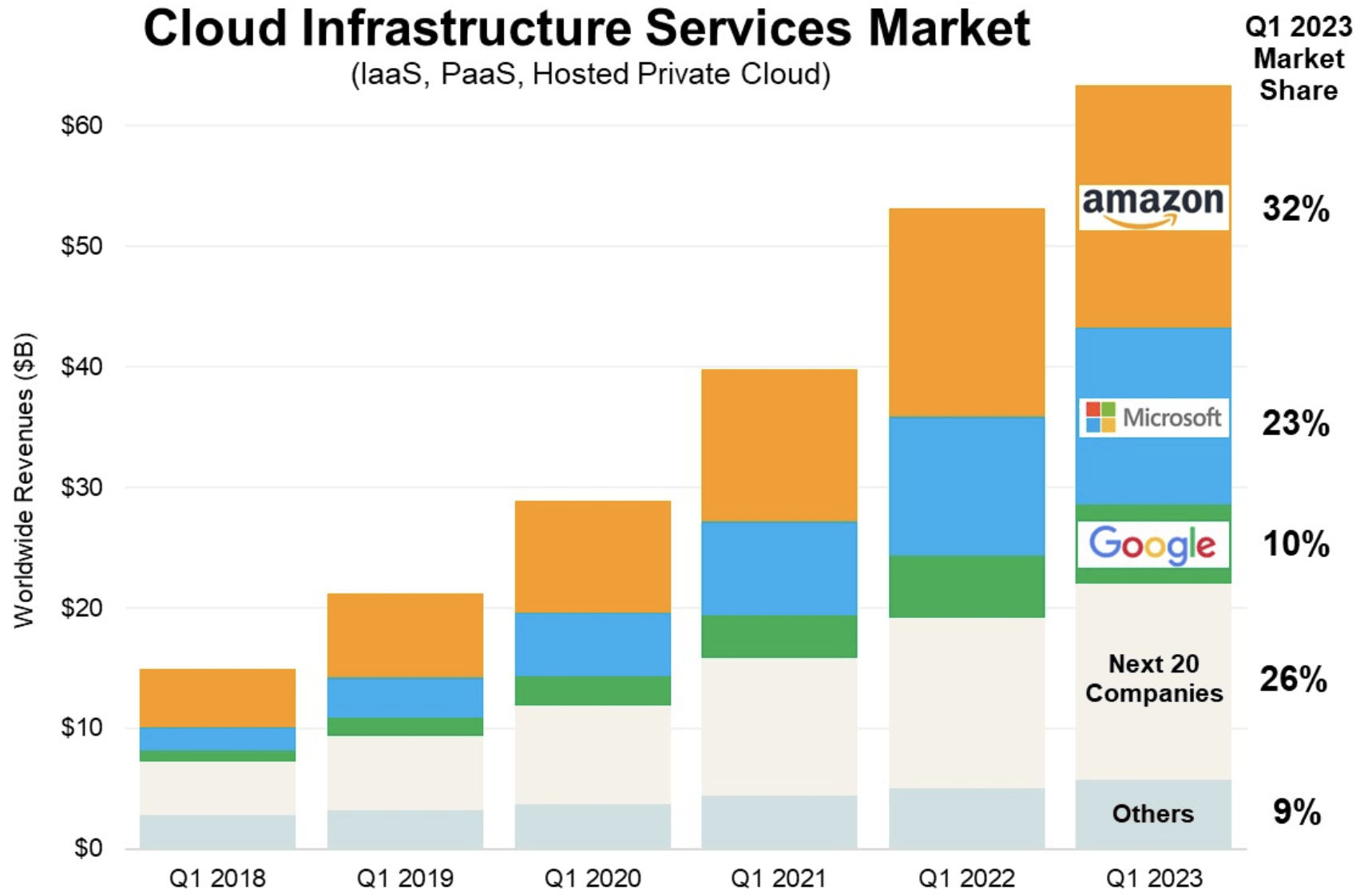

As I mentioned, AWS is the most considerable portion of any respectable valuation of Amazon due to its highly favorable properties. Growth is decelerating in this segment despite outperforming recent expectations. There is also growing competition from Google, Microsoft, and others. If it becomes apparent that Amazon is consistently losing market share or competitive dominance in the cloud segment, then Amazon’s price will likely head down.

valueinvesting.com

Part of this is because Amazon has an elevated valuation risk. It has long had a P/E ratio that makes value investor blush or scratch their heads, and many folks don’t want to overpay for a stock that already has such prolific gains behind it. Being so big exposes you to a lot of risks. Indeed, economic weakness will be felt by Amazon if we don’t get a soft landing. And all of these risks are pernicious for investors because of the inherent valuation risk in this name.

There are many other risks for such a large stock, including anti-trust, litigation, reputational risk, management transition, and the always nipping-at-the-heels competition of Big Tech rivals. One Seeking Alpha author did an excellent job of outlining a specific risk tied to rising retail theft.

Conclusion: Still at the Top of the Cloud

Amazon has a business that is difficult to understand, given its sheer scale and the very different nature of its core segments. However, I am issuing a BUY on the stock because I see tailwinds across Amazon’s entire business if a soft landing occurs. I’m convinced that the long-term nature of Amazon’s plan requires long-term stock ownership for maximum benefits. Despite a recent runup, strong recent earnings and tremendous growth ahead make me think it’s a great time to add to or start a position in Amazon.

TD Ameritrade

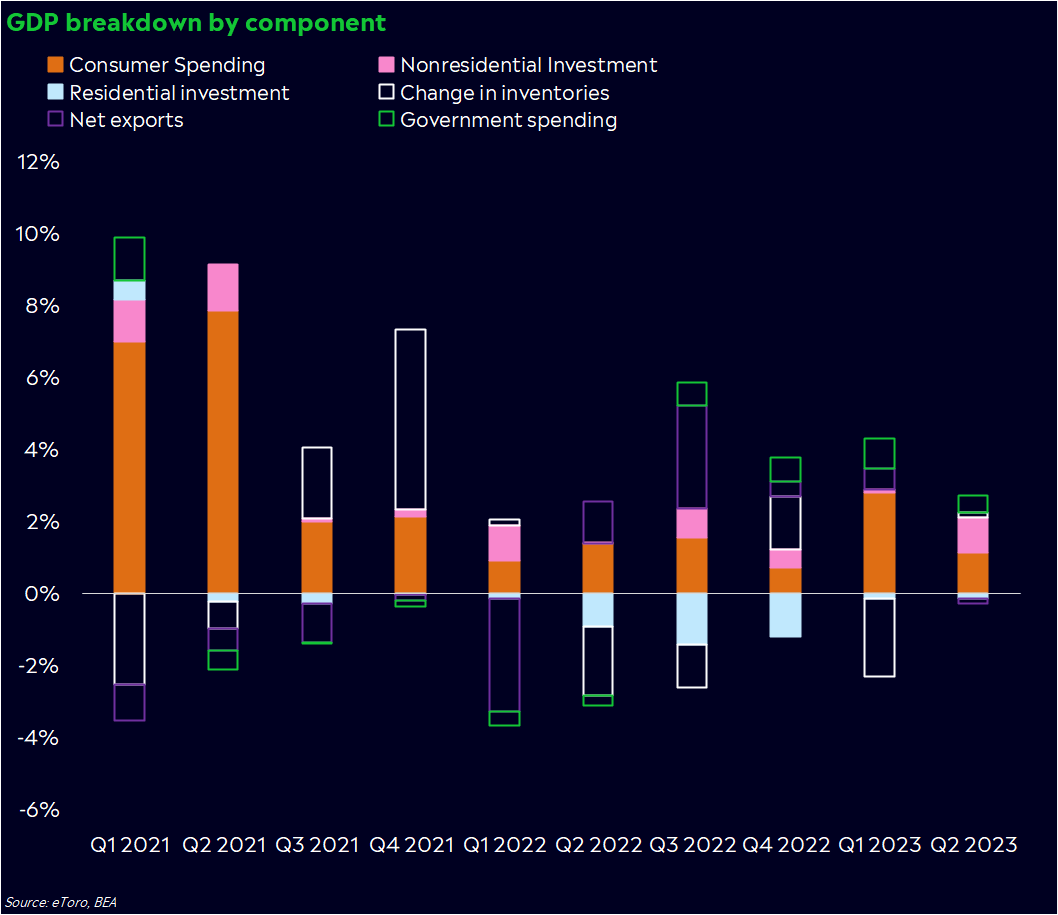

However, it is not just that a soft landing is occurring; it is also the nature of the economic activity occurring at a granular level. On the one hand, economic activity is likely to slow in coming quarters despite that headline-catching Atlanta Fed NowCast number. This increase in enterprise spending was at the heart of Amazon’s recent earnings beat, and I suspect it will continue to drive outperformance in the still dominant AWS segment.

eToro

This strengthens Amazon’s relative competitive advantage on price and steers commercial activity toward its consumer-centric ecosystem. But this economic slowdown and burdened consumers is happening concurrently with accelerating business spending, which reached its highest level in 6 quarters in the Q2 GDP Report.

Data Science Dojo

Some may have been disheartened that Amazon, once the household-name leader in AI, seems to be trailing behind rivals Microsoft (MSFT) and Google (GOOGL) in the flashy new area of Generative AI. However, it’s important to remember that Generative AI is only one component of a sprawling list of AI functionalities. While Amazon isn’t grabbing headlines, it’s still collecting cash from the Generative AI trend as the dominant cloud provider. It has a lot of incredible AI functionality for enterprises outside of the hottest new thing.

Furthermore, there is increasing evidence that Generative AI, as we currently understand, could be reaching a peak of commercial utility. Amazon has been consistently investing in AI despite the perceptions around ChatGPT’s recent gains. Furthermore, Amazon continues to give far more AI-centered offerings in AWS than its primary competitors. And its size in the cloud market is an underappreciated AI strength.

Kinsta.com

However, I believe many folks are missing a fundamental aspect of AI and its commercial application. Whereas the internet favored small companies that operated on an asset-light basis, I think the age of Artificial Intelligence will actually confer an advantage to the exact opposite kind of company: huge, possessing a lot of data, and asset-heavy. Amazon fits this bill nicely.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.