Summary:

- Starbucks has a strong competitive moat and turnaround plan focused on service efficiency, digital engagement, and extended operating hours.

- Technical analysis suggests a price target of $107 for SBUX stock, with potential upward momentum and bullish indicators.

- Starbucks appointed former Chipotle CEO Brian Niccol as its new CEO to drive growth and digital transformation, focusing on employee experience and digital advancement.

- Cold beverages, now 76% of Starbucks’ mix, grew 4% annually in Q3 2024, driven by new products like Summer-Berry Refreshers, reflecting Starbucks’ agility in meeting consumer demand.

- Starbucks stock is currently at $92, with a target price of $107. It is supported by bullish RSI and VPT trends, which indicate potential upward momentum and a balanced risk-reward scenario for August.

Hasan Ashari/iStock Editorial via Getty Images

Investment Thesis

In our latest coverage and initiation of a “Buy” rating on Starbucks (NASDAQ:SBUX), we underscored that the strong competitive moat underpins a turnaround plan featuring initiatives around service efficiency, digital engagement, and extended operating hours, key ways to surmount operational challenges and position Starbucks for long-term growth.

I opened a position in SBUX near its 52-week high three months ago, and I remain bullish on Starbucks due to its solid fundamentals and moats, which would help it overcome these challenges. We believe in Starbucks’ strategic position and long-term growth potential, supported by a leadership shift and operational improvement. Finally, we hold our 2024 price target at $107 based on expectations regarding revenue growth, margin improvement, and deepening digital and global footprints.

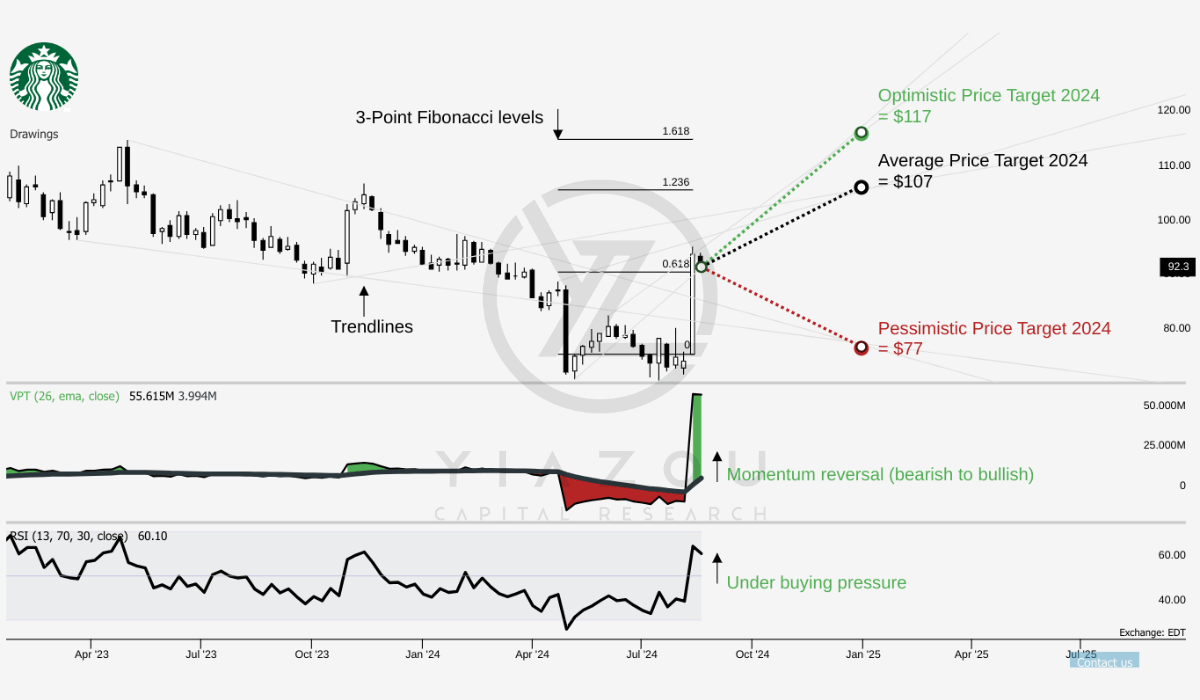

Technical Take: $107 Is The 2024 Price Target

SBUX is currently trading at $92 with an average price target of $107. This target aligns with the 1.236 3-point Fibonacci extension, suggesting potential upward momentum. An optimistic projection of $117 matches the 1.618 level, a key area often associated with strong bullish trends.

On the downside, the pessimistic target of $77 aligns with the 0 level, implying a full retracement if bearish pressures prevail. Further, the Relative Strength Index (RSI) at 60.10 indicates bullish momentum, reinforced by a bullish divergence. The RSI line is trending upward, signaling a potential rally continuation. The critical level of 50.00 has acted as a support level, further supporting a bullish bias.

Moreover, the Volume Price Trend (VPT) points to a significant upward reversal, with a current line at 55.62 million, compared to a moving average of 3.99 million. This sharp divergence indicates increasing buying pressure. If the VPT line makes a touchdown on its moving average, then there may be a solid possibility of sustained upward movement.

Author (trendspider.com)

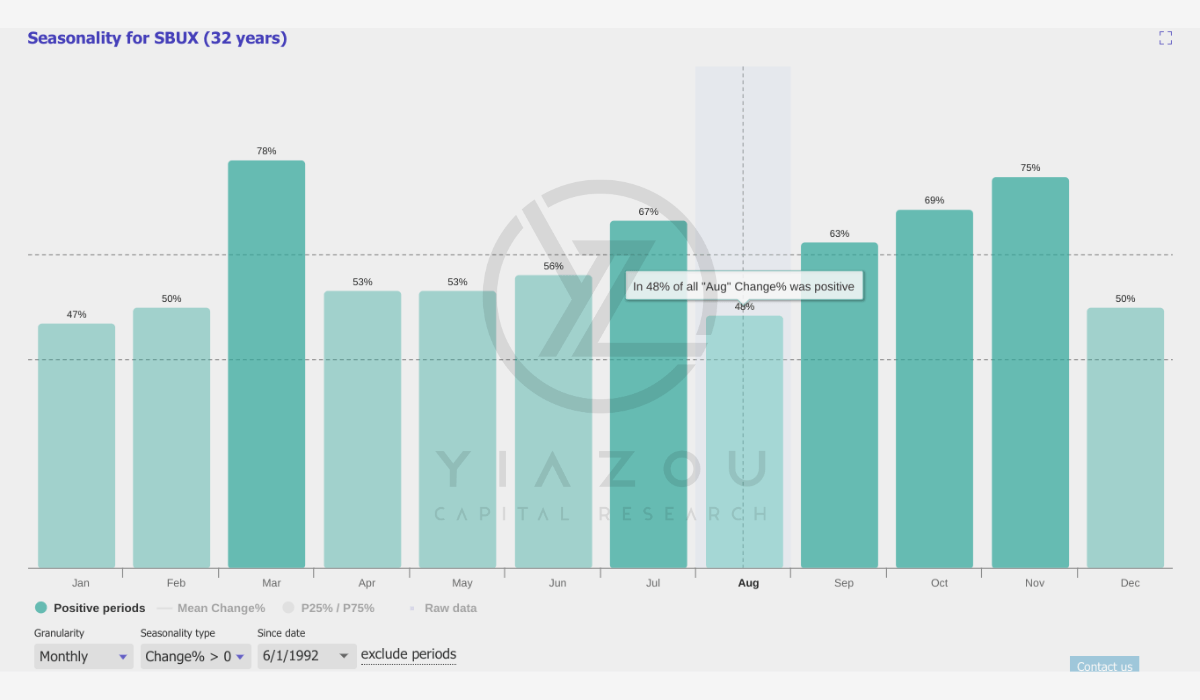

Finally, given the 48% historical probability of a positive return in August based on 32 years of data, the current month offers a balanced risk-reward scenario.

Author (trendspider.com)

Starbucks Taps Former Chipotle CEO Brian Niccol to Fuel Growth and Digital Transformation

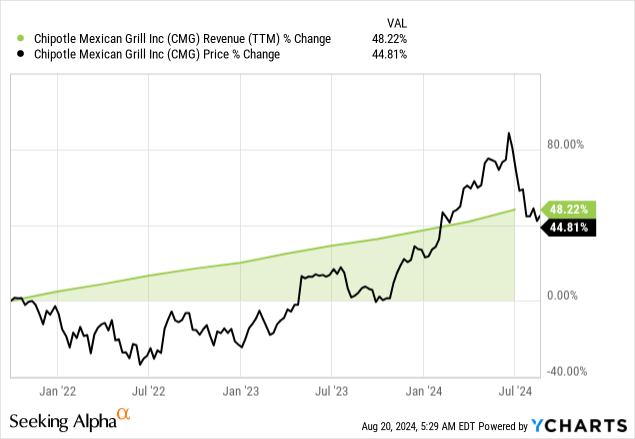

Starbucks is undergoing a core leadership transition, with the appointment of Brian Niccol as Chairman and CEO set to begin on September 9, 2024. Niccol’s solid track record at Chipotle (CMG) highlights his potential to drive substantial growth at Starbucks.

During his leadership, Chipotle saw its revenue nearly doubled, profits increased nearly 7X, and the stock price rose by approximately 8X. Niccol’s appointment as CEO is now vital for Starbucks, as he focuses on boosting employee experience, which he considers fundamental to customer experience and strategically aligns with Starbucks’ values.

Moreover, Niccol’s success in driving digital transformation at Chipotle is particularly relevant for Starbucks. Starbucks’ existing investments in mobile order and pay systems and its rewards program can benefit significantly from Niccol’s expertise in digital advancement. This synergy may accelerate Starbucks’ growth by attracting new customers and increasing customer loyalty through enhanced digital engagement.

Beyond Chipotle, Niccol has much more experience in the food and beverage industry, such as his leadership roles at Taco Bell and Pizza Hut, further bolsters his qualifications to lead Starbucks. Niccol’s leadership may have a significant quantitative impact on Starbucks’ growth potential. If he can replicate the fundamental progress at Chipotle, Starbucks could see similar improvements in key financial metrics such as revenue, profit margins, and stock price.

Update On Action Plan, Expansion of Store Network, And Product Advancement

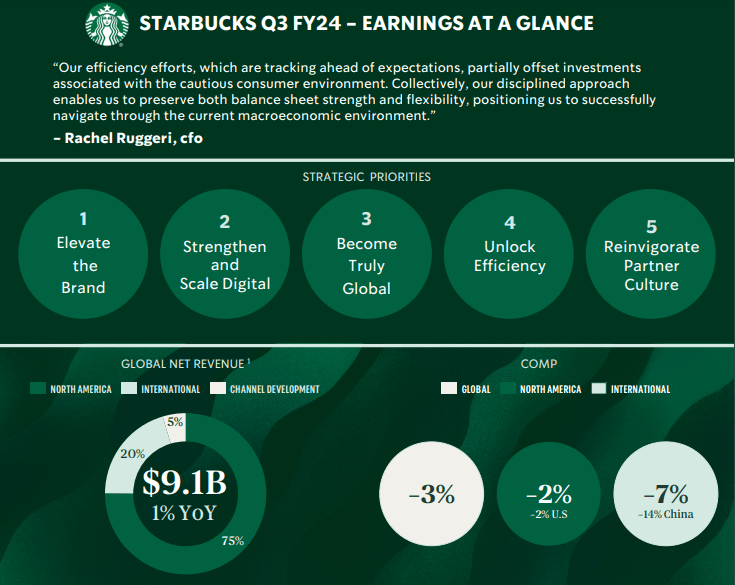

Starbucks has outlined a three-part action plan to drive growth. The plan focuses on unlocking capacity for new demand, attracting new customers, and boosting the Starbucks experience. The company’s relentless focus on improving operational execution across its nearly 10,000 US company-operated stores is central to this plan.

Key performance metrics such as partner scheduling, turnover, and inventory management have shown material improvements. For example, stores ranked in Starbucks’ top two operational performance quartiles reached a new high during the quarter, with a 28% upward shift from Q2. This improvement in in-store performance is expected to drive growth by enhancing the customer experience and increasing operational efficiency.

Similarly, the inventories have improved to $1.5 billion in Q3 fiscal 2024 against $1.8 billion in Q3 fiscal 2023, which shows the company’s preparation for improving potential on the demand side. Additionally, Starbucks’ focus on reducing customer wait times, improving product availability, and enhancing store operations through the Siren Craft systems may drive a 1% to 1.5% comp opportunity.

Moreover, Starbucks is accelerating the pace of its new-store builds and renovations, with 580 net new builds and more than 800 renovations planned in North America for FY 2024. This expansion is focused on Tier-2 and Tier-3 cities, where Starbucks sees population growth and forecasted underserved demand. By expanding its store network in these regions, Starbucks may increase its market penetration.

Further, the company has introduced a pipeline of innovative products supported by integrated marketing campaigns, successfully driving customer traffic into its stores. For instance, cold beverages now represent 76% of Starbucks’ beverage mix, with cold espresso driving 4% annual growth (Q3 fiscal 2024). Additionally, the launch of new products, such as the Summer-Berry Starbucks Refreshers beverages with Pearls, has set new records for product launches, demonstrating Starbucks’ ability to meet evolving customer preferences and drive demand.

Finally, Starbucks is also building out its 24-month product pipeline. The rapid launch of new hand-crafted iced energy beverages across US stores in just three months points to Starbucks’ agility in responding to market trends and consumer demand.

Starbucks

Sharp Decline in China Signals Struggles Amid Rising Competition

Starbucks’s central weakness is its decline in global comparable store sales, which fell 3% year-over-year in Q3 2024. Similar to the previous quarter, the decline was driven by negative 2% growth in North America and a more alarming negative 14% in China. Starbucks needs support maintaining customer traffic and sales momentum in key markets.

Of course, China has been one of the primary drivers of Starbucks’ international expansion, and a sharp decline in comparable store sales suggests that it is losing its competitive edge in this critical region. Several factors are at play: rising competition from local coffee chains, changing consumer preferences, and regional economic uncertainties. It is more worrying that this slump in China isn’t being compensated for with growth elsewhere in international markets, exacerbating the issue into a broader challenge of sustaining global growth.

Takeaway

While Starbucks is wrestling with a decline in its global comparable store sales, particularly in the Chinese market — a critical geography — the new appointment of Brian Niccol to the CEO role brings new optimism about a possible strategic turn in its business fortunes. Growth driving and enhancement of digital prowess, coupled with inspiration toward innovation, are firm grounds for changing the core of the Starbucks business.

As Niccol digs deep into Starbucks’ retooling on price, brand messaging, and digital experience, this can significantly improve customer engagement and sales in the U.S. With international challenges and stronger competition, Niccol’s leadership can boost Starbucks’ turnaround prospects. If done correctly, this positioning of Starbucks could bring long-term success and sustainable shareholder value creation.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of SBUX either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.