Summary:

- Super Micro Computer’s delayed filings have eroded my confidence, leading to a Sell downgrade.

- The company’s reliance on potential dilutive PIPE financing raises serious concerns about its financial stability, making it impossible to justify the odds of it getting back to good health.

- Valuation premiums are hard to justify given the unknowns in Super Micro’s forward projections and deteriorating margin profile.

- Elevated short interest and volatility make Super Micro a risky investment, with no clear path to regain investor trust.

Saturated/E+ via Getty Images

Investment Thesis

GenAI has created incredible opportunities for companies to globally benefit from surging productivity gains and unlocking efficiency. As a result, organizations have demonstrated strong ambitions in investing in and upgrading their technology infrastructure to support their GenAI investments, demarcating several AI infrastructure companies as strong beneficiaries from the others.

Super Micro Computer (NASDAQ:SMCI) was one of those companies that strongly benefited from the rising infrastructure investments that companies were making into upgrading their data center infrastructure. In August, I had issued a Buy rating expressing my optimism on Super Micro, based on the GenAI narrative staying elevated.

Unfortunately, the now-embattled company lies tangled in a web of problems that are still not fully visible to investors. I remained on the sidelines, hoping to see the company’s filings being released by the end of the year as previously promised.

But with its management now further postponing the date of publishing its filings to February, I have lost all confidence in the board and its management. It is virtually impossible now for investors to expect timely reports from management.

I am now moving to downgrade Super Micro Computer to a Sell.

The Narrative Has Shifted Away From Core Fundamentals

Despite publishing a Buy recommendation in August, I waited on the sidelines hoping to get my hands on the FY24 10-K and FY25 Q1 10-Q that the company is legally supposed to provide.

The rack scale solutions company originally moved to delay its FY24 10-K filing to a later unspecified date shortly following a short seller report.

Super Micro’s Founder and CEO also published a letter at the time focused on shoring up confidence among its customers & investors. The CEO said that they had formed a committee “to review our [their] internal controls and other matters” and that “neither of these events affects our products or our ability and capacity to deliver the innovative IT solutions.” The events that the CEO referred to was the short seller report, and the company’s decision to delay its 10-K.

Apart from that letter, there is extremely limited visibility for investors to understand, not just how Super Micro might financially perform, but even how Super Micro has been performing in the past few months.

The narrative for investing in Super Micro has completely moved away from fundamentals and now hinges on the probability of the company getting delisted from NASDAQ. As of writing, the company has secured an extension from NASDAQ to file all its reports. I still hoped that the company would file all the necessary filings by Dec 31st this year, as it committed to in a filing.

But comments from Super Micro’s CEO at a fireside chat last week confirm that Super Micro will now file all its reports at the end of NASDAQ’s previously granted extension, in February 2025.

In my view, these comments put investors’ expectations in unchartered territories, since the track record so far in this year stands against the company with prior report filing timelines getting pushed out. This only raises more questions about the nature and depth of its issues at the center of the company’s “internal controls and other matters” addressed by Super Micro’s Liang in the letter.

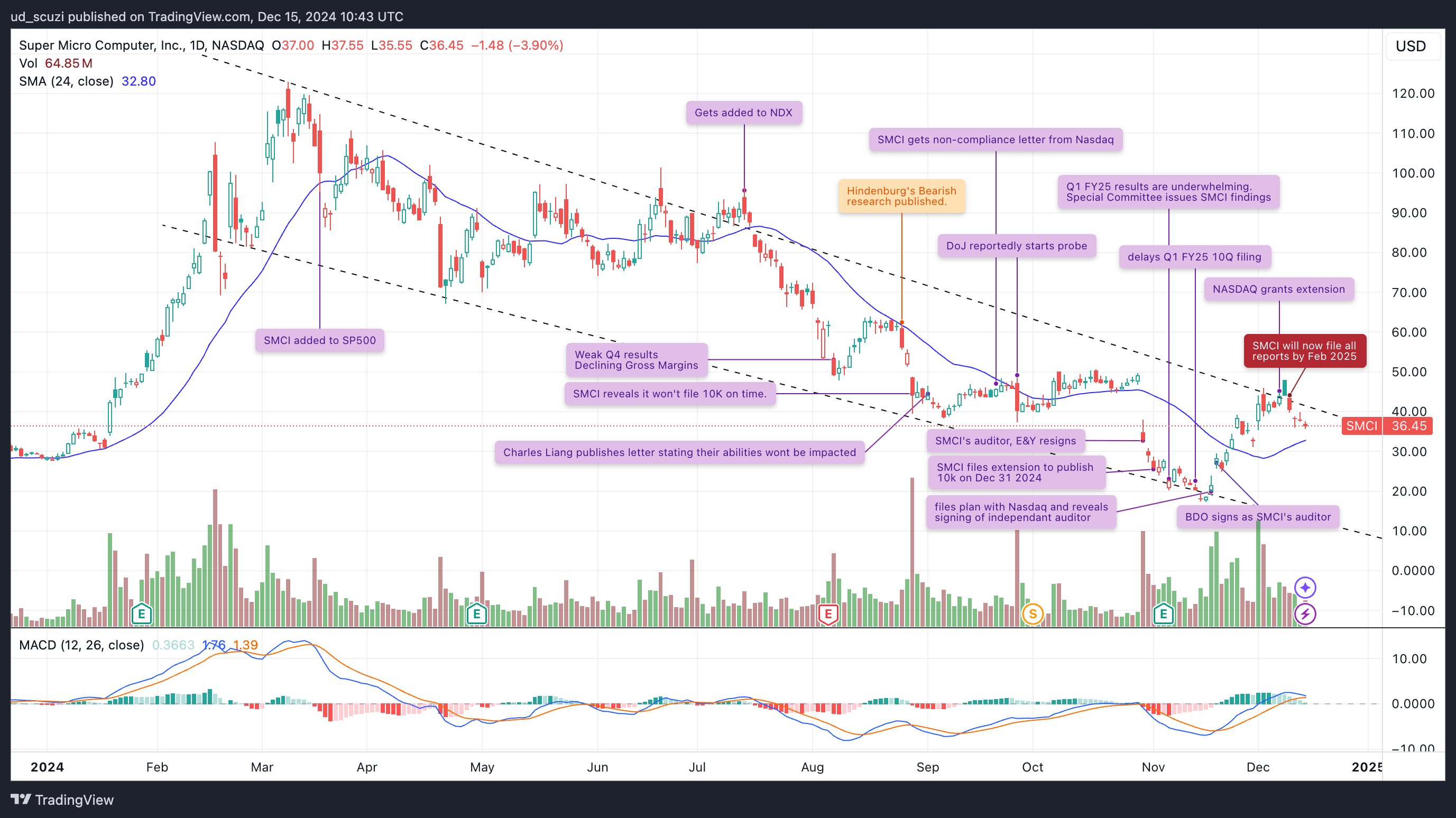

Exhibit A: Super Micro’s timeline of events as its stock collapsed under broader scrutiny. (Author’s compilation of events)

In the age of GenAI, when the narrative should be more on estimating the outlook on sales of its rack-scale solutions and its market share, investors appear focused on trading the stock on the sentiment surrounding compliance events, which is unsustainable.

PIPE: Significant Potential Shareholder Dilution Coming Up

Since the short seller report, the only two pieces of quantitative information that Super Micro’s management has released are: its preliminary Q1 FY25 results, and an 8-K filing advising investors that it had “prepaid in full and terminated its obligations.”

On the face of it, the latter actually should be a good thing, except it is not, if recent reports are to be believed.

According to Bloomberg, Super Micro has reportedly approached PE firms to raise equity and debt via the PIPE vehicle (private investment in public equity). It’s not clear yet how the PIPE will be structured, but regardless of whether it is an equity offering or a convertible, PIPEs are dilutive to Super Micro’s current shareholders. PE firms get cheaper access to Super Micro’s shares for a discount, while also giving them the ability to sell them at a higher spread and rapidly expanding the supply of the company’s shares, leading to share dilution.

I suspect management is attempting to prop up its capital structure with shareholder-dilutive methods such as PIPEs after the company recently disclosed it prepaid and terminated loan agreements with two lending firms. According to its preliminary 1Q FY25 release, Super Micro “expects to report total cash and cash equivalents of approximately $2.1 billion and total debt of approximately $2.3 billion with bank debt.” Per SA data, the company had ~$1.7 billion in cash+ST investments and ~$2.2 billion in debt as of June 2024.

Even if the company did require more capital after prepaying/terminating its loan agreements, it could have used secondary offerings to issue more shares. PIPEs allow Super Micro express access to capital without the hassle of more SEC approvals. The SEC does require Super Micro to obtain shareholder approval if the company is going to dilute more than 20% of its last known number of 602 million shares outstanding. Therefore, I would not be surprised if the company ends up diluting to 20% of its shares outstanding, or about ~$4.4 billion in share sales proceeds.

As of the last known report, Super Micro had ~$4.5 billion in liabilities and ~$9.9 billion in assets on its balance sheet.

Valuation Premiums Are Difficult To Justify

Consensus estimates expect Super Micro to report $25 billion worth of sales, growing 67% for the FY25 year ending in June. EPS growth rates are falling faster, with consensus estimates projecting Super Micro to report FY25 EPS of $2.8, growing 27%.

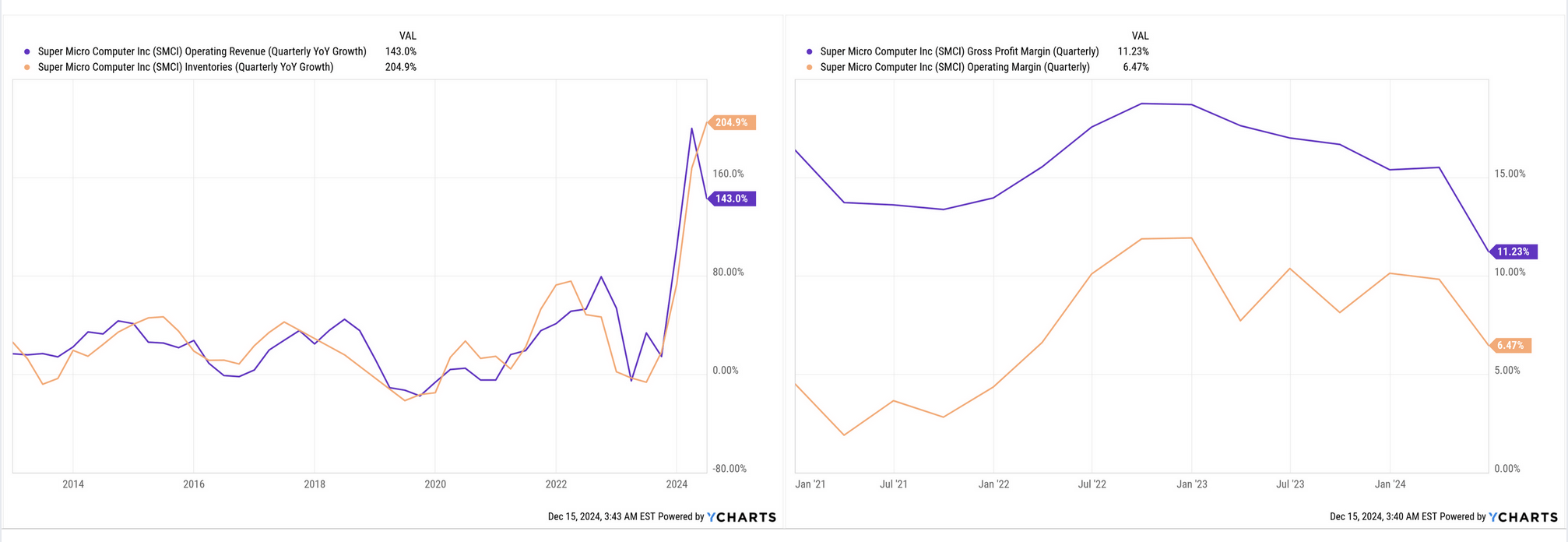

At this point, it is difficult for me to have confidence in Super Micro’s forward projections, because there is quite a bit of unknown that is baked in here. Plus, per Exhibit B below, its margin profile was already falling, and if revenue slows further, it is going to put enough pressure on its margins, which creates further problems for its EPS growth.

Exhibit B: Super Micro’s revenue, inventory levels and margins per last known reports filed earlier this year. (YCharts)

With inventory growing faster than revenue, the company could also have to mark down the ASPs of the product it holds, which will further impact margins. Further, with the current situation that Super Micro finds itself in, its high-profile customers (etc., hyperscalers) might not want to associate themselves with the company’s financial troubles, leading to the company further marking down its inventory.

The company does trade at valuations of 14x GAAP 2025 earnings that seem ‘attractive,’ but as I noted earlier, these are based on 2025 EPS that I do not have any confidence to justify.

It is difficult to estimate the odds of the company delivering earnings in such an environment. It is also difficult for investors to expect the company’s reports to be filed in February after management moved the dates twice already.

Quite frankly, the Powerball lottery has better-defined odds than investing in Super Micro’s growth story, which is now impossible to estimate.

Other Factors To Consider

Super Micro is a heavily shorted stock.

As of writing, the company has ~15% of its stock shorted. This is going to increase the volatility with the stock mostly trading on sentiment. The elevated volatility might cause the stock to trade against my bearish thesis.

It is also possible that Super Micro’s management files its reports before February, which could improve sentiment again.

Takeaway

At the moment, there is no reason for me to remain optimistic about Super Micro Computer anymore. After having patiently waited for the company to reveal their financial numbers, which management is legally responsible for, the company has, yet again, pushed out its filings to next year.

This makes it impossible for investors to evaluate the prospects of Super Micro’s business any longer. This story has only transformed into a guessing game where the odds are impossible to define.

This leaves me with no option but to recommend a Sell rating on Super Micro.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.