Summary:

- The resignation of Supermicro’s auditor, Ernst & Young, signals deeper compliance and accounting issues, posing significant risks and opportunities for SMCI shares.

- SMCI’s growth is slowing, margins are contracting, and cash flow issues suggest potential fundamental problems, making the stock a speculative trade.

- The company faces delisting risk from NASDAQ due to non-compliance with annual report submission, with a possible grace period extension as a near-term catalyst.

- Despite uncertainties, hiring a new auditor and releasing the annual report could drive significant upward price movement, but SMCI is no longer a growth play.

Erik Isakson

Investment Thesis

Disagreements over accounting methods are common. Even the most seemingly straightforward accounts, such as Revenue, can be complicated by a sales contract’s terms and conditions, i.e. do we recognize sales when we ship a server? When is it installed? When is it accepted by the customer? Or when we receive a payment? What about costs? Do we match revenue with costs, or record costs once incurred?

But make no mistake. The resignation of Supermicro’s (NASDAQ:SMCI) auditor is unusual. On Wall Street, such a move signals issues that go beyond typical disagreements. The strong language in the resignation letter suggests deeper compliance, internal controls, and accounting practices issues. Today, SMCI finds itself late on its 10-K report for FY ’24, and its 10-Q for Q1’25, nearly exhausted its 60-day grace period after receiving a non-compliance notice from the NASDAQ last September, and still doesn’t have an auditor. In 2018, the company was delisted from the NASDAQ because it failed to report its quarterly and annual results, highlighting the delisting risk it faces today.

But with any volatility comes risks and opportunities. A favorable outcome to this compliance knot will alleviate significant uncertainty around the ticker, and one can safely expect an upward rebound in the same magnitude as the downward pressure resulting from this issue in the first place. On the other hand, a negative outcome increases the risk of SMCI being delisted from the NASDAQ, which will likely have a detrimental impact on the share price. Whether you hold a buy or a sell position, this issue shouldn’t be taken lightly, regardless of the strength of its unaudited financial results and low valuation.

In the last article, the thesis was purely anchored by financial performance, and little weight was put on SMCI’s past compliance issues and its narrow tech moat, which, I thought, were overshadowed by its position in the AI server supply chain, translating into billions of dollars in sales.

Has the thesis changed? Not really, unless there is a misrepresentation in the financial results that necessitates restatement of previous financial reports. What we know for certain is that growth is slowing and margins are contracting, but even if this is the case, there is still value in SMCI based on its unaudited figures. Listening to cloud providers and semiconductor manufacturers, the AI trade is in full swing, and SMCI plays a crucial role, in doing all the low-margin grinding work of server assembly.

Still, there are new variables now that warrant a rating downgrade, as discussed below.

Delisting Risk

SMCI received a non-compliance notice from the NASDAQ on September 17th, 2024, after failing to submit its annual report due August 29, 2024.

SMCI has 60 days from the date of the notice to either:

- Submit its annual report

- Provide a convincing plan that culminates in the submission of the annual report

- Delist from the NASDAQ and trade OTC

The 60 days have almost passed (only 3 days left until the November 16 deadline). Since the company doesn’t have an Auditor yet, SMCI will most likely go with option #2, submitting a plan basically telling the NASDAQ that it will soon hire an auditor and get this annual report to the public.

In normal circumstances, the NASDAQ would most likely approve the plan. It is straightforward, simple, and easy to execute by merely hiring a replacement auditor to check the books.

But it is possible that the NASDAQ put more weight on the intricacies of the situation, including the DOJ probe, SMCI’s past compliance issue the 2018 delisting and the 2020 SEC fine), EY’s resignation letter, and the lack of progress in addressing the problem.

SMCI’s CEO didn’t do himself a favor when he assured the public that the company didn’t expect a restatement of previous financial reports. A sales contract’s terms and conditions often complicate the interpretation of accounting guidelines. The new auditor may deem restating previous financials necessary, contradicting management’s prior statements. Despite controlling the Board of Directors and the Executive team, the decision of whether to adjust the previous accounts falls in the hands of the new auditor, not the CEO or the audit committee. It is worth noting that EY questioned the independence of SMCI’s audit committee, as noted in its resignation letter to management.

SMCI is also being probed by the DOJ concerning accounting violations raised by a whistleblower who has recently come forward.

With this level of scrutiny, the new auditor will feel the heat. The delay in announcing a new auditor is likely tied to a vetting process to ensure that what happened with EY doesn’t happen again, and at the same time, ensure that the new auditor has the necessary resources to address regulators’ concerns.

Valuation

SMCI reported preliminary Q1’25 sales between $5.9 billion and $6 billion, falling at the lower range of the August guidance of $6 to $7 billion communicated during the FQ4 2024 earnings call. That’s still a pretty decent figure, but it does confirm the rising competitive pressures as Dell (DELL) and Hewlett Packard Enterprise (HPE) enter the market, attracted by its scale despite its low margin. SMCI expects FQ2 2025 sales between $5.5 and $6.1 billion (or $5.8 billion at midpoint), more or less flat sequentially. Management attributed the slowdown to customers awaiting NVIDIA’s (NVDA) Blackwell GPUs instead of utilizing its predecessor GPUs available in stock. Nvidia adopts an aggressive development strategy with short development cycles to maintain its lead in the AI GPU market, but this makes it hard for its customers to keep up.

Shifting back to SMCI’s valuation, I believe despite these challenges, from a purely financial perspective, and ignoring the possibility of delisting, the $5.8 billion in sales that management expects next quarter, which translates to an EPS of $0.53 per share, or roughly $2 annualized, is a decent figure. This is also a conservative estimate in light of Q1’25 GAAP preliminary EPS of $0.69 (at the midpoint of preliminary Q1’25 estimates reported in its latest earnings call).

Nonetheless, despite SMCI’s forward PE of 7.4x being low relative to peers, the company is hardly undervalued given the delisting risk.

Even if SMCI’s unaudited financials were accurate, being delisted would have a significant impact on SMCI’s valuation given the investment mandates controlling where the whales of Wall Street can invest their client’s money, many of which prohibit investing in OTC companies by default, given the loose regulatory and compliance bar of OTC trading.

Margin Update

SMCI is largely an assembler of third-party components. They do it at scale and cheaply. This explains their thin margins despite selling some of the most in-demand AI servers.

These dynamics exacerbate any accounting issues. Even small potential irregularities in revenue and cost accounting can quickly push the company from profitable to unprofitable. This is the main risk to any buy hypothesis that rests on the company’s unaudited financial results.

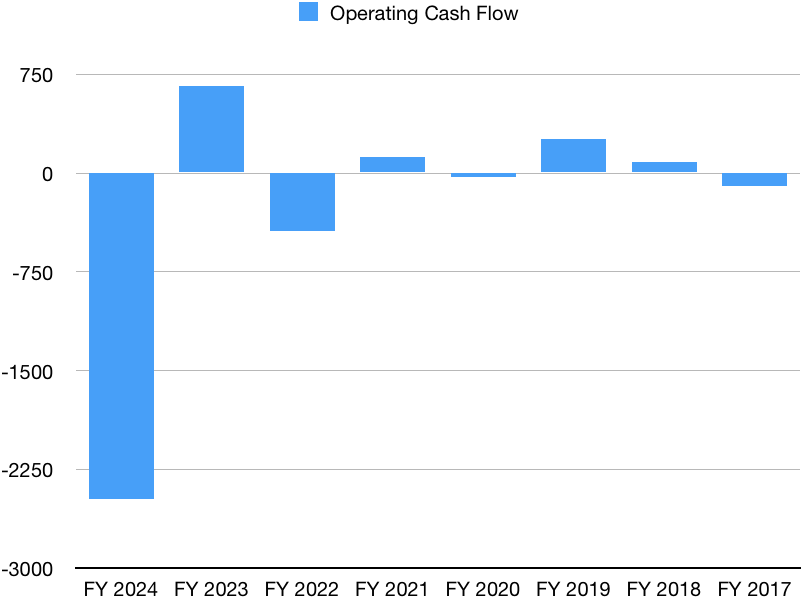

The cash flow picture is muddied by working capital expansion. Despite growth in sales and profits, cash from operations has been flowing the wrong way, pushing SMCI to raise debt to fund the gap.

Author’s estimates based on SMCI filings

Final Thoughts and How I Might Be Wrong

I don’t think that the market is wrong about SMCI. There is a lot of uncertainty. Sure, with this kind of volatility comes opportunities, and I believe that we should see significant upward price movement if the company succeeds in convincing the NASDAQ to give management more time to submit its late financial reports. Another potential catalyst is the hiring of a new replacement auditor and finally the release of its annual report. All these are upward catalysts that underpin the hypothesis of some fellow analysts and investors. On the other hand, one needs to acknowledge that SMCI is no longer a growth play. It is more of a speculative trade now, underpinning our rating downgrade. Going forward, a rating upgrade is conditional on clarity over the DOJ investigation, and a clearer path toward regaining NASDAQ compliance.

From a purely financial perspective, Q1 preliminary results came out solid in terms of margins, but revenue and revenue guidance fell short of expectations. Non-GAAP gross margins stood at 13.3%, down from 17% in the same period of last year, but up sequentially from the 11.3% reported in Q4 2024. Operating margins were slightly lower at 9.9%, vs 10.8% in Q1 2024, but much higher than the 7.8% reported in Q4 2024. Next quarter, however, SMCI expects revenue and margin declines on a sequential basis (at midpoint), mirroring the intensifying competition and loss of market share. SMCI might be cheap right now at 7.4x forward PE, but it is hardly undervalued.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.