Summary:

- TSM has delivered good results in the recent quarter and is showing strong tailwinds in key metrics.

- TSM’s Arizona plant yield has surpassed that of comparable facilities in Taiwan, which can lead to greater support from the U.S. government.

- Intel is being bogged down by company-specific issues and has postponed or canceled several semiconductor plants.

- TSM can continue to deliver good revenue growth and margins as the demand for AI chips continues to increase and the company has become the main supplier.

- The forward P/E ratio for the fiscal year ending 2026 is 20, which shows that the stock is still quite attractive despite the massive bull run in the past few quarters.

Sundry Photography

TSMC (NYSE:TSM) continues to show strong results which is improving sentiment on Wall Street despite geopolitical headwinds like the recent ban on export of its chips. YTD TSM’s stock has shown total returns of 109% compared to 37% by S&P 500. Besides the solid performance in the recent earnings, TSM has also reported good news from its Arizona plant. According to Bloomberg, the yield for Arizona plant has surpassed the yield for comparable facilities in Taiwan. This should help the company gain good support from U.S. government. On the other hand, Intel (INTC) has faced a number of challenges and is now postponing or canceling a number of factories in Germany, Poland and other regions. Earlier this year, I published the reasons why TSM can be a great pick-and-shovel stock in the AI race.

Over the last few quarters, I have had a Buy rating for TSM stock and a Sell rating for Intel. This has proved right as TSM continues to enjoy a good runway. The EPS growth projection for the next two years is quite strong. The EPS estimate for the fiscal year ending Dec 2026 is $10.36 which gives it a forward P/E ratio of 19.6. This is quite modest when we look at the moat of the company and its role as a key supplier to many big tech companies.

Good runway for growth

TSM was able to beat the EPS and revenue estimate in this earnings. Close to 70% of the total revenue comes from 7nm or lower nodes, which shows the rapid progress made by the company in the last few quarters. It is now the sole supplier for several key big tech companies, making it an integral part of the supply chain.

Company Filings

Figure: Revenue of TSM from different nodes. Source: Company Filings

We have already heard about the massive CapEx by hyperscalers in the AI chips. Most of these chips are manufactured by TSM and the company is showing strong revenue growth potential due to AI demand.

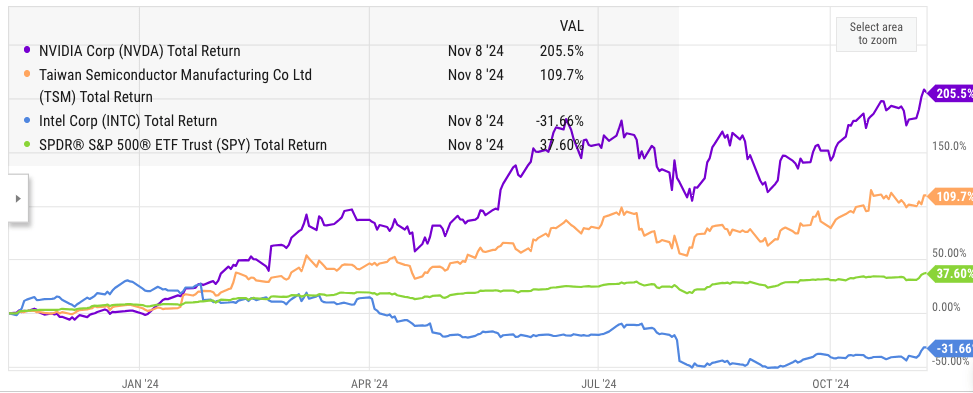

YCharts

Figure: Performance of TSM and other peers in YTD.

In YTD, TSM’s stock has been a clear winner with 109% total returns. Other than Nvidia (NVDA), this is one of the highest returns, and it leaves many other competitors behind.

Lower competition, better moat

Intel wanted to invest massively in the foundry segment to gain market share. It has invested close to $25 billion annually for the past two years in building different factories. However, it is now facing a big headwind as Wall Street is spooked over the ability of the company to deliver good results in the near term. This has led to a massive correction in Intel stock in YTD. Intel has already postponed many new factories in Germany, Poland, and other regions. Intel continues to face yield challenges in lower nodes and is planning on reducing the CapEx significantly to soothe investor nerves. Samsung is also facing challenges in its chip production capabilities and is ceding market share to TSM.

Lower competition from Intel will improve the sentiment for TSM, and we could also see better margins from the company over the next few quarters as it controls massive market share. Nvidia’s stock performance has been better than TSM in YTD, but I believe that TSM has a better moat. Nvidia is seeing competition from AMD (AMD) and other tech giants, who are building their own AI chips. Most of the chip fabrication is done by TSM. It is highly likely that Nvidia will lose market share in the AI segment, but the total revenue for TSM will likely not be negatively impacted, as TSM is the main supplier of fabrication facilities to most of the competitors.

EPS growth and geopolitical risk

TSM continues to show a strong momentum in EPS growth. The consensus EPS estimate for fiscal year ending Dec 2025 is $8.79 giving the stock a forward P/E ratio of 23.14. For fiscal year ending Dec 2026, the EPS estimate is $10.36 giving the stock a forward P/E ratio of only 19.64. This is quite modest when we look at the growth runway, moat, and operational efficiency in delivering good yields.

Seeking Alpha

Figure: EPS estimate for TSM in the next few years. Source: Seeking Alpha

TSM will continue to face geopolitical risk but I believe that this risk has been overhyped. An earlier report by Bloomberg mentioned that any Taiwan invasion or blockade could lead to a massive challenge for the global economy. Many major companies will face a big headwind. As an example, Apple (AAPL) receives close to 20% of its revenue from China and a big chunk of its supply chain is based in this region. Any geopolitical issue will likely impact Apple significantly.

Besides the geopolitical risks, TSM has a stable earnings profile. We can see from the above image that for fiscal year ending Dec 2026, the low EPS estimate is $9 while the high EPS estimate is $11.93 or 33% more than the low estimate. This is quite a narrow range for forward EPS estimates, which shows the confidence in future earnings growth. Many other big tech companies, like Nvidia, have a huge variation in forward EPS estimate.

Seeking Alpha

Figure: Forward EPS estimates of Nvidia. Source: Seeking Alpha

We can see in the above image that for fiscal year ending Jan 2027, the high EPS estimate for Nvidia is 4 times that of low EPS estimate. This difference is due to forward estimates of the company’s market share, margins, and revenue growth. In terms of consensus EPS estimate for fiscal year ending Jan 2027, Nvidia stock is trading at 30 times. This is significantly more than TSM’s less than 20 forward P/E ratio for fiscal year ending Dec 2026.

Hence, TSM could be a better investment for investors looking for a stable EPS growth momentum and a more certain forward EPS projection.

Investor Takeaway

TSM has delivered strong results during earnings and continues to show a good growth runway. The company has also announced good yields for its Arizona plant, which should help it receive more support from the U.S. government. On the other hand, competitors like Intel and Samsung are facing significant challenges and announcing the cancellation or postponement of their new plants.

TSM has a better moat than many other big tech companies because it provides fabrication facilities to all of the major players. Any change in market share within the AI segment or other business does not affect the demand for TSM’s facility. We can clearly see this in the narrow forward EPS range by many analysts. For 2 fiscal years ahead, the forward P/E ratio of TSM is less than 20 compared to close to 30 for Nvidia. A lower valuation multiple and certainty in forward EPS estimate makes TSM a good option for investors.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.