TSM Q2 results beat expectations, but the stock price suffered a pullback amid market panic.

The price corrections, combined with the growth drivers reported in Q2, made it a strong GARP (growth at a reasonable price) candidate.

This sector leader is currently trading at 0.91x PEG (P/E growth ratio).

The majority of its revenues come from advanced nodes (7 nm and below), offering superior pricing power and margin expansion potential.

sefa ozel

TSM stock Q2: Strong results met market panic

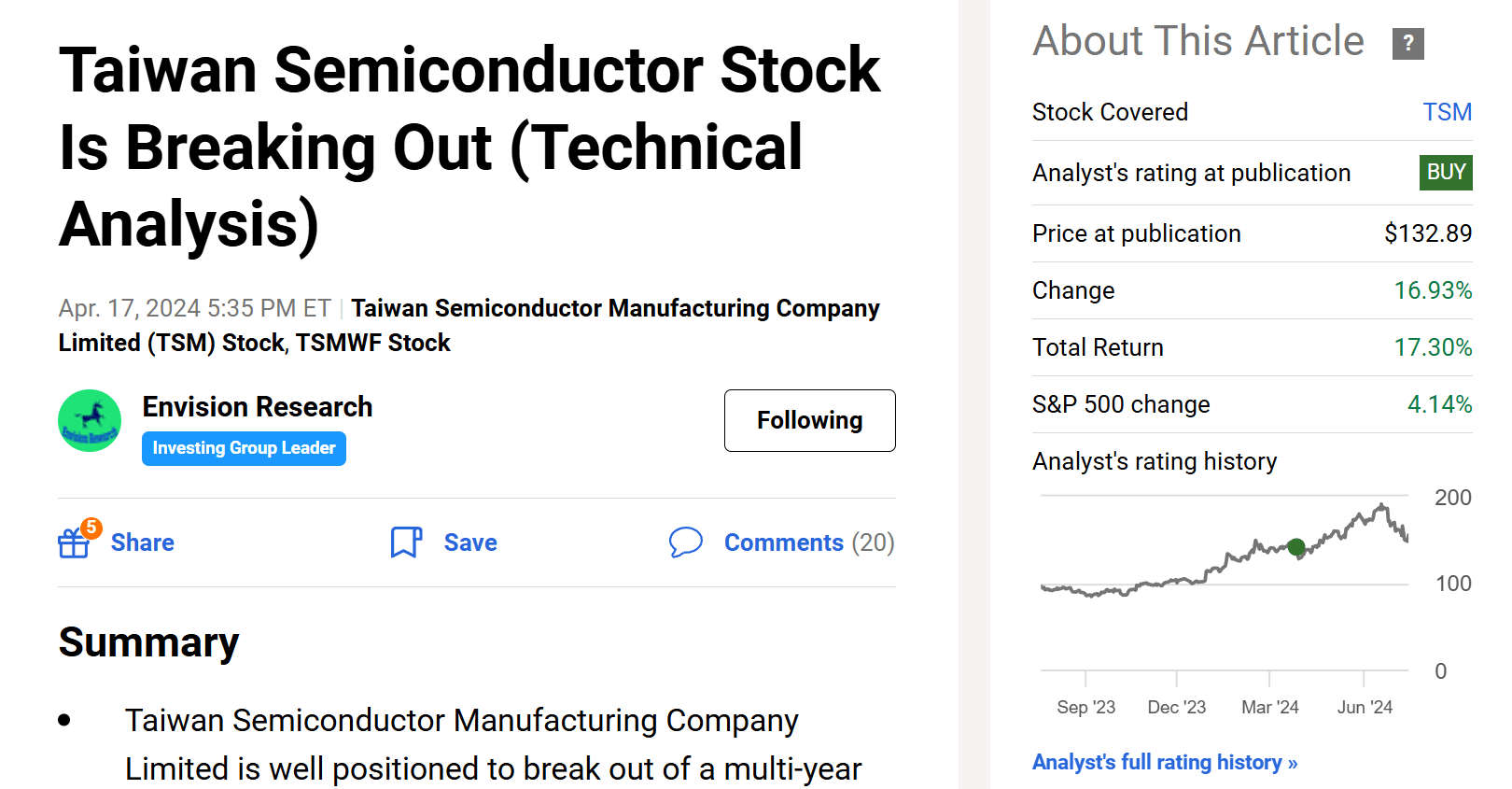

I last wrote on Taiwan Semiconductor Manufacturing Company Limited (NYSE:TSM) back in April 2024. As you can see from the chart below, that article, titled “Taiwan Semiconductor Stock Is Breaking Out (Technical Analysis),” was published on April 17, 2024. As the title suggests, the article was more focused on the technical trading patterns of the stock. In particular, I argued for a bull thesis based on the following considerations:

Taiwan Semiconductor Manufacturing Company Limited is well positioned to break out of a multi-year resistance level near $130. I see both strong technical and fundamental signals that can support such a breakout. Judging by Taiwan Semiconductor’s revenue trends, the contracting phase of the current cycle is ending, while the expansion phase is starting.

Seeking Alpha

Since then, there have been a few key developments surrounding the stock. First and foremost, the company has released its 2024 Q2 earnings report (ER). The results were quite strong in my view (more on this in a minute) and the ER also described several key developments in its business operations. Second, the recent stock market panic has caused quite a large price volatility for the stock. As seen in the chart above, the stock did break out of the $130 level since my last writing and has staged an exceptional rally to a peak of around $193. The price has corrected amid the market turbulence to its current level.

These developments motivated this follow-up coverage on the stock. In contrast to my last article, this article will be entirely focused on the fundamentals. And you will see that my updated assessment still points to a buy rating. More specifically, the combination of its price pullback and growth drivers made the stock an ideal GARP opportunity (growth at a reasonable price).

TSM stock Q2 recap

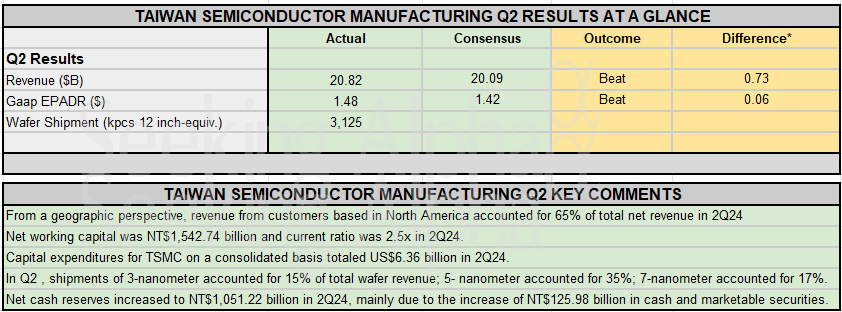

As aforementioned, the company delivered a robust Q2 in my view. The financials beat consensus on both lines and the business made considerable progress on several key fronts. The chart below shows the highlights of TSM’s 2024 earnings results. As seen, revenue reached $20.82 billion, exceeding expectations by $0.73 billion. Earnings per share came in at $1.48, beating estimates by $0.06. In terms of business operations, wafer shipment reached 3,125 thousand (12-inch equivalent wafers).

Also, notably, in terms of product mix, leading-edge 3-nanometer shipments accounted for 15% of wafer revenue, followed by 5-nanometer for 35%, and 7-nanometer for 17%. In other words, advanced technologies (seven nanometers and below) accounted for 67% of its Q2 wafer revenue, which compares favorably to last year’s comparable-period tally of ~51%. Advanced technologies carry higher margins than other products, which provides more growth potential for earnings. I will revisit this point a minute later.

Seeking Alpha

TSM stock: Growth outlook and valuation

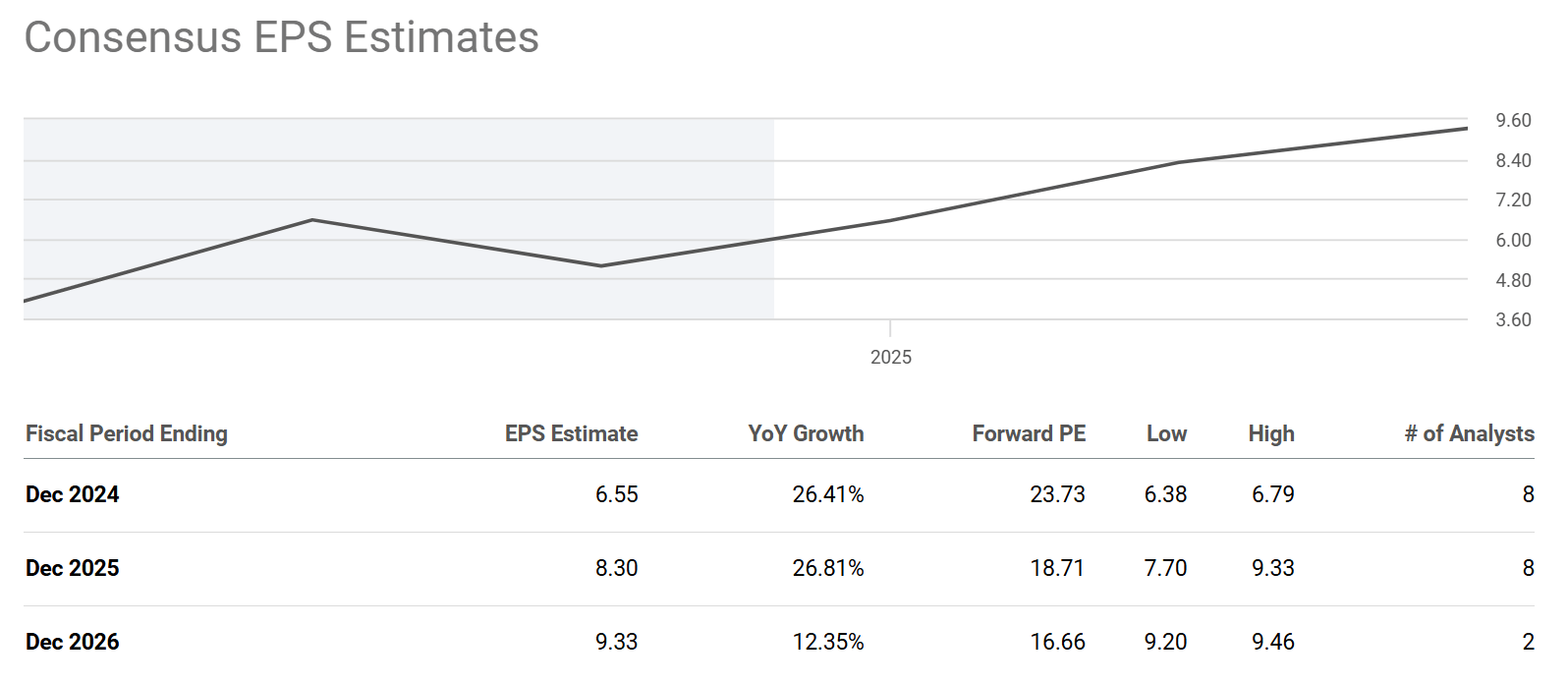

Looking ahead, the market forecasts rapid earnings gains in the next few years. More specifically, the chart below shows the consensus EPS estimates for TSM stock in the next few years. As seen, analysts project a significant year-over-year (YoY) growth in EPS in the next two fiscal years, with an estimated 26.41% increase for FY24. This rapid growth is then expected to continue into FY25, with a projected YoY growth of 26.81%. However, the growth rate is anticipated to decelerate in FY26, but still at a YoY rate of 12.35%.

Trading at a forward P/E ratio of 23.7x currently, TSM is not cheap by any standards. However, considering the rapid growth, the P/E multiple is expected to contract quickly to 18.71 in FY25 and to 16.66 in FY26. In terms of the PEG (P/E growth ratio), a 23.7x P/E and a projected growth rate of 26%-plus translate into a PEG ratio of 0.91 only, noticeably below the ideal threshold of 1x most GARP investors seek.

Seeking Alpha

The question is of course whether TSM can materialize the consensus projected growth rates. I do see good odds for the projected rates to materials for several reasons. The top three on my list include its leading scale and technology, the secular demand for high-performance computing (HPC) chips, and also its margin expansion potential.

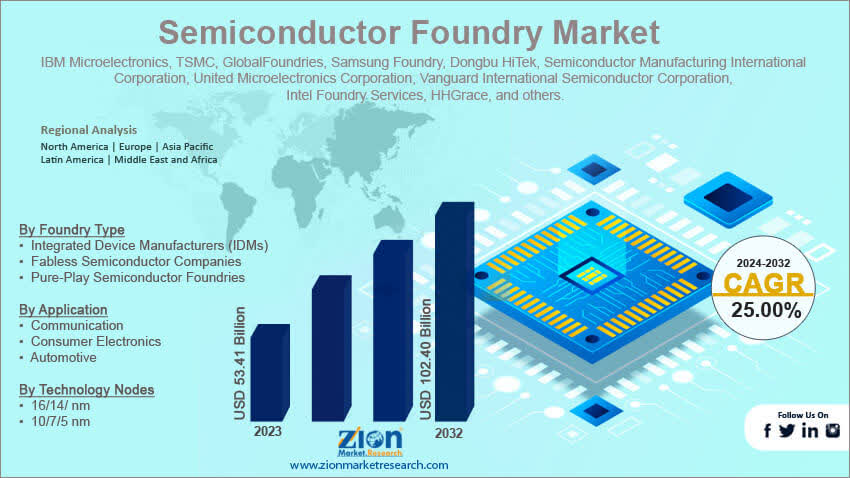

TSM is a leader in the foundry space, which is projected to grow at a CAGR of 25% between 2024 and 2032, according to the following ZION report. I expected TSM to capture a large portion of this growth due to its leading scale and favorable product mix as aforementioned. TSM (and the foundry industry in general) has faced some seasonal weaknesses for smartphone products. However, my view is that solid demand for TSM’s HPC chip capacities should be more than enough to offset such seasonal fluctuations.

ZION

Finally, as aforementioned, advanced technologies (7 nm and below) accounted for more than two-thirds of its Q2 wafer revenue. Such advanced technologies face far lower competition pressure and thus enjoy far higher pricing power. I expect TSM to leverage such pricing power (as it has done skillfully in the past) to improve margins and boost earnings. As a live example, TSM announced price raises on 5nm and 3nm nodes in 2025 shortly after its Q2 ER. Quote:

Taiwan Semiconductor will raise the prices on how much it charges its customers for its 5nm and 3nm manufacturing process nodes in 2025, Digitimes reported. The global foundry has already started to tell clients to expect an increase between 3% and 8%, the news outlet added, citing sources at integrated circuit design houses.

Other risks and final thoughts

In terms of downside risks, TSM and its peers share common risks such as economic downturns (which can reduce demand for semiconductors), intense competition, heavy capex investments, etc. However, TSM faces unique challenges. The top one is its geographical risk. Its concentrated manufacturing in Taiwan exposes it to geopolitical risks, including potential trade restrictions or disruptions due to tensions with China.

Also, TSM in general boasts a superb profitability grade, as seen in the chart below. It outperforms the sector median across all metrics by a wide margin. For example, gross profit margin stands at 53.36%, exceeding the sector by 8.15%. EBIT, EBITDA, and net income margins are exceptionally high at 41.99%, 67.32%, and 37.85%, respectively, each significantly surpassing the sector average by triple-digit percentages. However, its net profit margin is currently below its historical average. And its gross margin is only 0.44% above its historical average as seen. These could be due to the ongoing inflation pressure and/or competition pressure. With the pricing power from its advanced nodes and potential price raises, I expect the margins to further improve.

To conclude, the goal of this follow-up article is to examine the new developments reported in its Q2 ER and the impact of price corrections amid the ongoing market turbulence. My final verdict is to maintain my buy rating. In a nutshell, I see a strong GARP candidate – a leader in a sector that enjoys strong secular growth for sales at 0.91x PEG.

Seeking Alpha

Analyst’s Disclosure:I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

As you can tell, our core style is to provide actionable and unambiguous ideas from our independent research. If your share this investment style, check out Envision Early Retirement. It provides at least 1x in-depth articles per week on such ideas.

We have helped our members not only to beat S&P 500 but also avoid heavy drawdowns despite the extreme volatilities in BOTH the equity AND bond market.

Join for a 100% Risk-Free trial and see if our proven method can help you too.