Summary:

- Tesla, Inc. not changing their growth plans is introducing major risk to the company.

- The only reason Tesla’s margins got crushed is because they have way too much capacity for this level of demand.

- They’ve been on an amazing run, but this environment has changed, and they should react accordingly, which they are not.

Justin Sullivan

I hear a lot of people trying to defend Tesla, Inc. (NASDAQ:TSLA) Q1 earnings, but I don’t see how you can. The margin hit they took was out of the blue and enormous. As much as Tesla says they have their ear to the ground in a direct-sales-system, something is for sure not quite right to see that type of margin hit. I’ve been doing this for a while (a few decades), and the answer circles around to Tesla not giving up on their hoped-for 50% growth. They need to cut Giga factory square footage growth, otherwise, at this pace, they are in trouble.

The Margins: No Way

Oh my goodness. Seriously. There is no way to sugarcoat this margin report.

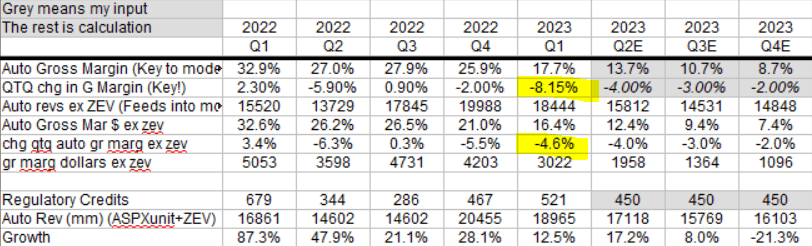

Tesla Gross Margins (Elazar Advisors Model and Tesla Reports)

Above is our model; inputs taken from Tesla reports and some math.

The company at their analyst day touted that they were dropping expenses big time. I came out pretty concerned about Tesla after that analyst day. And as seen by this recent earnings report, that expense drop was not enough to cover this demand pullback.

When they reported deliveries on April 2nd, I said this:

“There’s a good shot that the average price drop can surprise the Street to the downside and a drop in costs may not be enough to save margins.

The biggest driver to my EPS model since following Tesla has been auto gross margins. They were down about 200bp last quarter and based on the price cuts I think they can be down again, maybe more than last quarter.”

That’s what exactly took place.

We discover based on this earnings report’s margin drop that the price cuts we saw all quarter were not solely because of lower lithium or cost reductions, but rather because demand was falling off. Because demand fell off, Tesla needed to incentivize potential customers to keep buying. If demand was fine, there is no way you’d need to see this type of margin hit.

The company said on this recent Q1 earnings call that orders were above production. But that’s only because they dropped prices by so much taking such a big hit on margins. Without that margin hit, orders probably would have been below production, and that’s the problem I’ll discuss further down.

There is no way to look at revenues and orders and say everything’s fine without looking at margins. This is analysis 101.

Stocks run on valuation based on EPS. If revenues are good and margins are not, then there is no way to make lemonade out of the lemons.

And because CEO Elon Musk did not see any letup in economic headwinds, there’s risk for further margin deterioration.

At This Pace, There Is Risk To The Earnings And Stock

You saw above my expected margin drops going forward. I think that’s frankly even probably aggressive. Still, it gets my numbers way below the Street. When a company’s margins drop off fast in a quarter, the risk is that they continue at that pace or faster for the following quarters. The risk is that margins continue down 4-8% from the previous quarter.

A couple of more quarters like that and Tesla has no earnings and maybe quarterly losses reported in a few quarters.

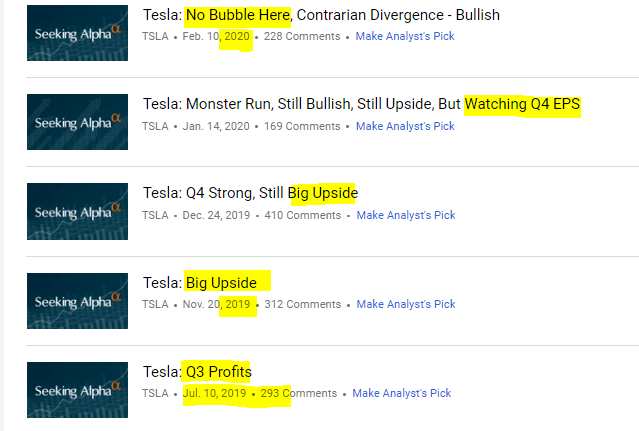

Our Tesla Calls Have Been Pretty Spot On, Solely Focusing On Earnings Trends

I was a big bull for a few years until late 2021.

Elazar Advisors Tesla Calls On Seeking Alpha (Seeking Alpha)

The key to our consistent bullishness was our earnings model. Based on the trajectory of their revenues versus their margins and opex, we were getting huge leverage in earnings. The rest of the sell-side stayed bearish and missed all of that at the time. Our EPS was multiples larger than the Street at that time.

(P.S. In the run-up with us, I had a few subscribers message me they went from a 5-figure portfolio to 7 and 8 figures. I still get those types of messages from subscribers.)

In late 2021, when Tesla’s stock price caught up to our EPS-driven valuation, we went from Buy to Neutral even as the rest of the sell side was going from sells and neutrals to Buy Ratings.

On November 16th, 2021 we were on CNBC announcing how we’re stepping off from our Buy:

“Elazar Advisors’ Chaim Siegel explains his downgrade of Tesla’s stock.”

The peak of the stock was November 4th, 2021. Not bad timing.

Our earnings momentum stopped, and the valuation was full.

Now our earnings are well below the Street. We’ve been below the Street all year, but ahead of this earnings report, we were well below the Street.

Now our next year’s EPS number is under $1.00 when the Street is currently over $5.00. (See Our Full Model: Paywall).

While Cathie Wood and the Street may be looking out to robotaxis, I think the stock has mostly been reacting to the earnings progression over the years. I think Tesla, as most stocks, will continue to respond to future earnings expectations. Those expectations are driven by current trends and markets look out 9-12 months typically. So at this pace of trend, there’s major risk to that EPS outlook.

The Problem And The Major Tesla Risk

I did not hear on last earnings call that they are slowing Giga Factory growth. Just the opposite, they stuck to their 50% revenue growth outlook. That means they need to keep producing lots of cars into a higher interest rate – high ticket goods slowdown environment.

Tesla is not responding to the environment strategically, which is causing a giant risk to their being a going concern.

A few more quarters of these types of margin hits and the stock can be literally a fraction of where it stands today.

While it’s a tough call for management to pull back on their growth expectations, they kind of have to. Their only hope is that the economy picks back up. But that’s based on hope. Musk was clearly concerned on the call about the economy. Based on that concern, Tesla should be slowing production growth.

Why is production growth such an important problem?

The fact that they have too many factories running now means they have too much fixed-cost-per-unit. If demand falls, and they sell fewer units, that fixed-cost-per-unit jumps big-time. Cost of goods sold would jump and that would kill their margins.

That’s why the company’s been forced to cut price so much. They want to keep their units up, so they don’t get hit with that fixed-cost-per-unit problem if they were to deliver fewer units. That’s why they favor showing a quarter of big margin hits led by price cuts. If they didn’t cut price, I think the margin hit of the fixed-cost problem would have made margins even worse.

That’s an incredibly risky position for this company to be sitting in.

We all heard from other big cap companies last quarter that they cut capex and growth plans. Tesla needs to do the same or pit all their hopes on some lucky break with the economy. But that’s gambling and I don’t think proper management. That’s a bet though that risks the company.

Conclusion

It’s pretty incredible that most of the major sell-side analysts defended this Tesla, Inc. margin deterioration. But the company has bigger problems if they don’t step off the growth pedal. A couple of more quarters of margin drop and Tesla earnings get erased. If so, Tesla, Inc. stock would have serious downside risk, and potentially the company would have going concern risk.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

All investments have many risks and can lose principal in the short and long term. The information provided is for information purposes only and can be wrong. By reading this you agree, understand and accept that you take upon yourself all responsibility for all of your investment decisions and to do your own work and hold Elazar Advisors, LLC, and their related parties harmless. Opinions given are at this moment and can change rapidly after this is published. If our calls are made public (outside the service) we may or may not update our opinions publicly.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Be smarter about markets and the Fed’s immense impact on predicting what’s next. Join a pro with 30+ years experience to get markets right.