Summary:

- Tesla has designed battery systems, electric vehicles and solar panels with the highest technological advancements. It has advanced technology to cool and heat their batteries which greatly extends battery life.

- These technological advances are resonating with consumers, Tesla’s market share has skyrocketed and they have become the largest manufacturer of electric vehicles.

- Recent car price cuts are improving affordability, and in January, the number of orders rose twice as fast as production; demand is very high.

- Tesla has several competitive advantages over competitors, and now that the stock price is in favorable territory, Tesla stock is worth buying.

Justin Sullivan/Getty Images News

Introduction

Tesla (NASDAQ:TSLA) is a well-known electric vehicle company in the world. The company with Elon Musk as CEO went through an upswing since the announcement of the first Model S; a fuel-efficient electric car with very fast acceleration, as well as an attractive design.

The stock is a household name on Wall Street, as its total return over 10 years is a whopping 7278% (73x times your initial stake 10 years ago). Tesla is one of the most profitable mass-market automakers on the market. And with strong growth in electric vehicles, battery storage systems and solar panels, Tesla is well positioned for further growth.

Phil Fischer devised a list of 15 questions, with each question worth one point.

If you answer the 15 questions for Tesla, Tesla gets all the points. Of those 15 questions, I think the following question is the most important:

Is the company providing a product or service that has sufficient market potential for a sizable increase in sales for several years?

Tesla offers state-of-the-art products with huge market potential which are superior compared to competitors. I find the innovation around Tesla batteries particularly fascinating. In my article, I explain in 3 reasons why Tesla is an attractive investment.

- The best energy storage systems on the market.

- Fast-growing company in a growing total addressable market.

- Recent share price correction presents an opportunity.

Tesla Offers The Most Advanced Energy Storage Systems

The first reason Tesla is buy-worthy is that Tesla applies advanced technology in its batteries, which are superior to those of competitors. Tesla batteries have higher energy density, better efficiency and longer life.

The longer life is because Tesla has developed an advanced cooling and heating system to manage the temperature of the battery. The battery is cooled in the summer and heated in the winter for optimal battery life. Battery life can be obtained by looking at the so-called discharge state. This is the percentage of the total battery capacity that has been used up.

A low discharge state is desirable because it promotes battery life, better performance and faster charging. A battery with a high discharge state should be replaced sooner. And since the replacement cost of an EV battery is quite expensive ($13,000 – $20,000), this is not an option for the average consumer.

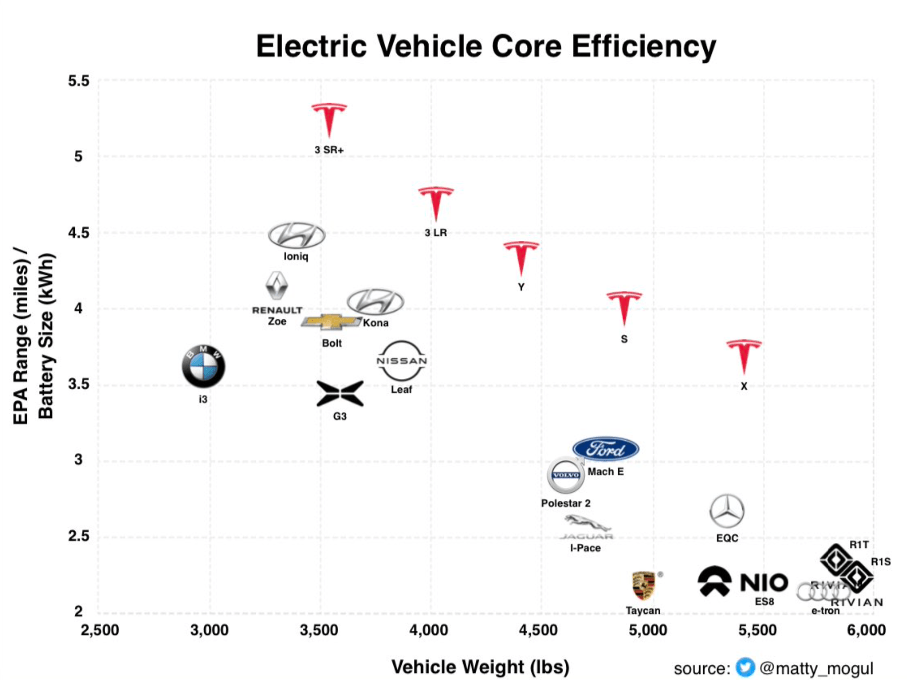

Tesla’s batteries are more efficient than those of competitors. A Tesla’s range is much greater for the same amount of battery weight compared to that of competitors. The production cost of a Tesla battery cell is also lower than competitors. Also, their next 4680 battery cells are even more efficient and have a much greater range than those currently on the market.

Electric Vehicle Core Efficiency (Torque News)

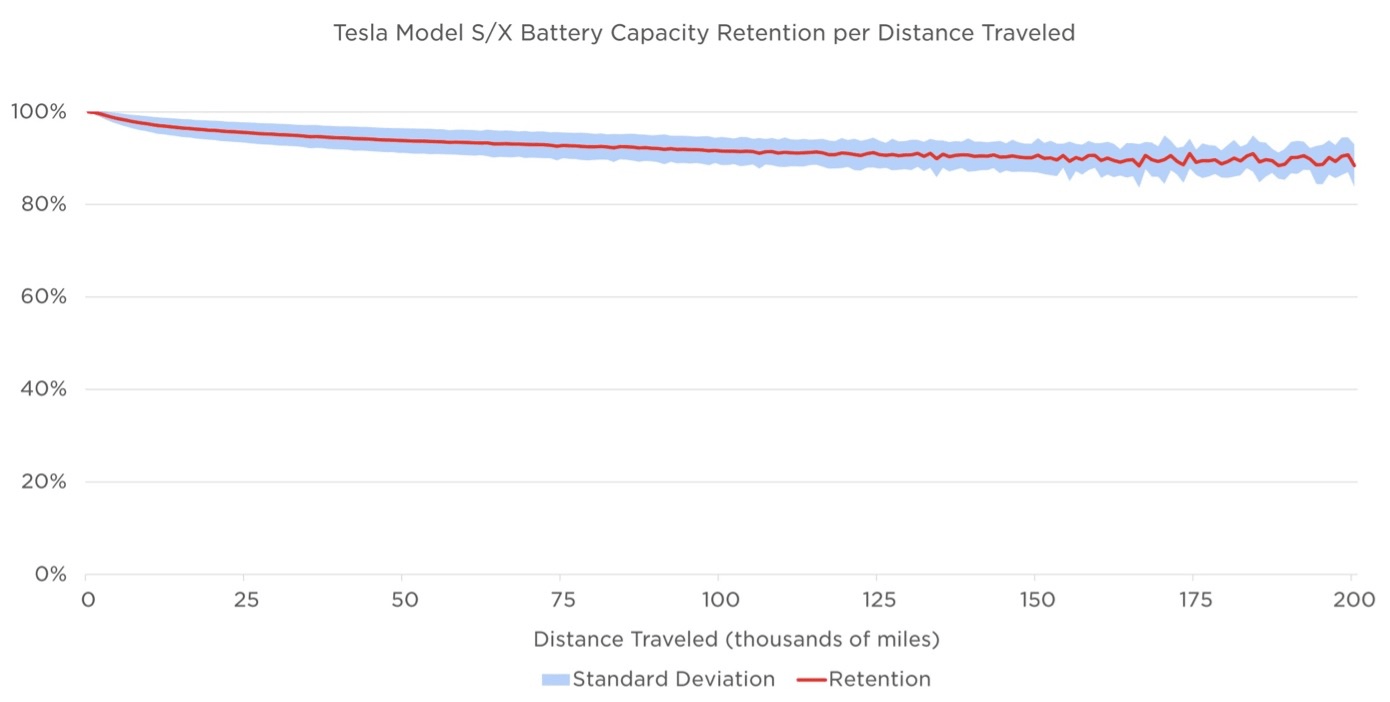

Also, the longevity of Tesla batteries is the best because of their innovative temperature management system. Even after 200 miles, the battery capacity is still above 80%. As shown in the chart below.

Tesla Model S/X Battery Capacity Retention (Electrek)

And because of warranty terms, Tesla owners don’t have to worry about early battery problems. And also because of their free supercharge offers, fuel costs are a lot lower than traditional ICE cars.

Tesla is investing as much as $3.6 billion in their Gigafactory Nevada plant to produce EV batteries, bringing the total amount of investment in the plant to $10 billion since 2014. Their new 4680 lithium-ion battery cells have a higher energy density at a lower cost than the current 2170 battery cells. These batteries are needed, among other things, for their Cybertruck pickup. However, the plant will not make substantial volumes of batteries until 2024.

Tesla has a clear advantage over competitors thanks to its lower production costs, higher energy density and longer battery life.

EV Market Is Huge And Tesla Is The Market Leader

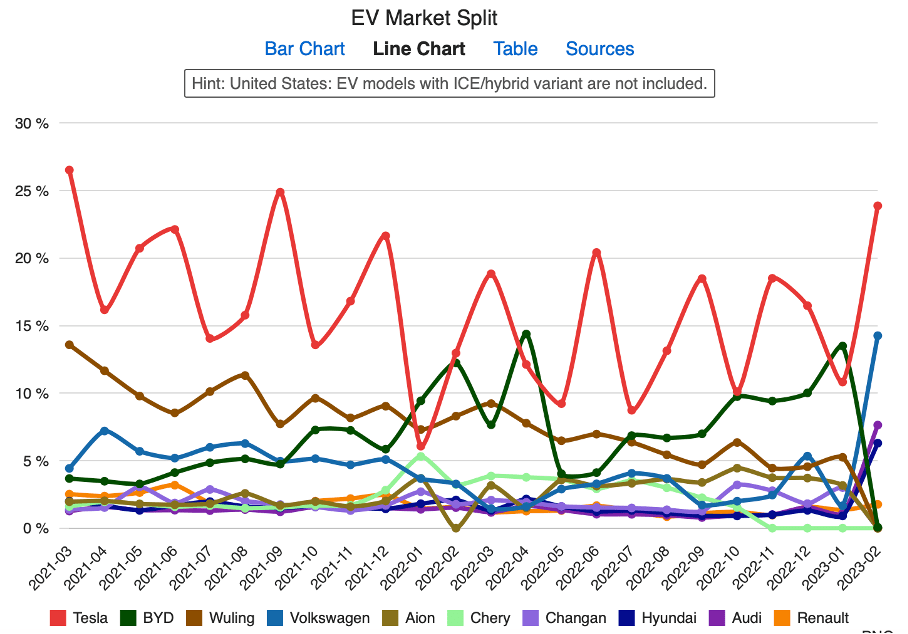

Tesla is grabbing a large market share making it the largest EV manufacturer in the world. Tesla is the leader in the EV market, as shown in the chart below. The EV market took off after the advent of various subsidies made available to allow consumers to drive an EV cheaply.

EV market split (Open EV charts)

Tesla is far from outgrown, the overall addressable market for electric vehicles is growing rapidly. Many governments are encouraging the use of electric vehicles because they want to reduce greenhouse gas emissions in their countries. Therefore, they offer government incentives to make EVs affordable to consumers.

Statista predicts that by 2027, 16.2 million vehicles will be sold and sales will reach $858 billion by then (CAGR of 17%).

Tesla also said the total addressable market for energy storage systems could be larger than EVs, which is why the company is investing heavily in battery production.

Tesla experienced strong sales growth over the past 4 years with a CAGR of 40%. Their outlook is also bright. Next year, 32 analysts predict a 30% increase in sales and a 23% increase is expected for 2024.

Recent quarterly results look strong with 1.3 million car deliveries in 2022, 51% sales growth, $12.5 billion in net income and $7.5 billion in free cash flow.

Investors are especially curious about demand, especially as a recession may be looming. CEO Elon Musk is confident in the company’s continued growth and spoke as follows:

Thus far in January, we’ve seen the strongest orders year-to-date than ever in our history. We currently are seeing orders at almost twice the rate of production. So it’s hard to say that will continue twice the rate of production, but the orders are high. And we’ve actually raised the Model Y price a little bit in response to that.

…

I think there’s just a vast number of people that wanted to buy a Tesla car, but can’t afford it. And so these price changes really make a difference for the average consumer.

One of Elon Musk’s goals is to make Tesla cars affordable for every type of consumer. Tesla is doing that by introducing affordable models, such as the Model 3, which will boost sales during times of economic stagnation.

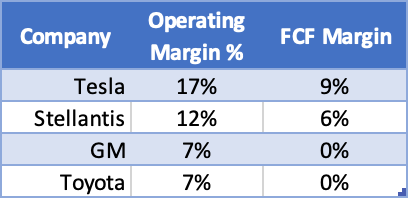

What about the finances? Those look a lot rosier than for other major automakers. That’s because EV production is much less capital intensive, so profit margins are higher. Tesla’s operating margin is 17% and its free cash flow margin is 9%; one of the highest in the auto industry.

Profitability of well-known car manufacturers (SEC and author’s own calculation)

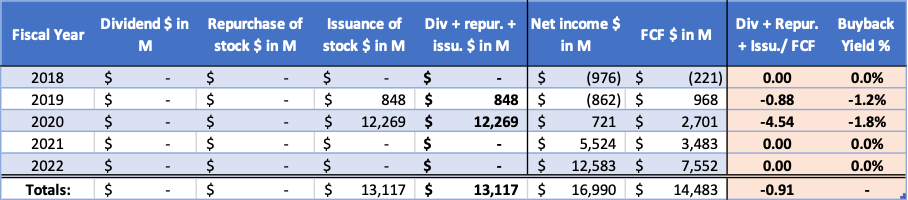

Issuing Shares To Expand Tesla’s Production Facilities

In 2020, Tesla issued an amount of $12.2 billion worth of shares which diluted the shares significantly. The dilution caused the share price to fall from $60 to $30. However, the cash raised from the issuance allowed Tesla to expand its production facilities which leads to more revenue. The share price shot up from $30 to 300 by 2021. It was a good move by Elon Musk.

Tesla’s Cash Flow Highlights (SEC and author’s own calculations)

Tesla Stock Is Now At Buy Level

With a great company in mind, we come to the valuation of the stock before making the buying decision. Tesla has historically been expensive, especially during its peak at the $403 price level in 2021. Now the stock is trading at a favorable level of $180, while revenue, earnings and free cash flow are increasing.

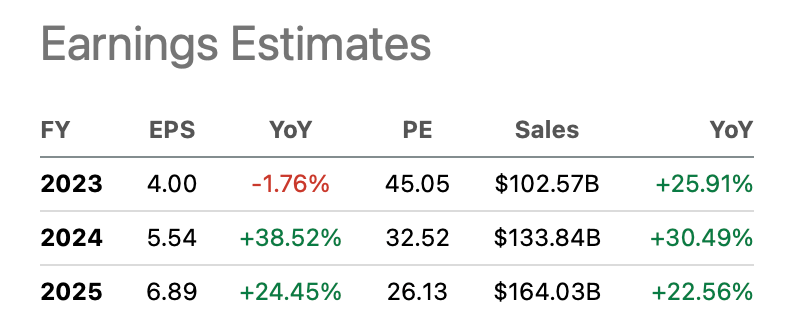

Tesla is currently still far too expensive in current terms, as its PE ratio is 45. However, for the next few years, 32 analysts expect strong earnings growth, leaving the PE ratio for 2025 at only 26. Along with earnings per share, revenue is still expected to grow strongly by double digits, while several analysts have revised their earnings estimates downward. I think the PE ratio of 26 is reasonable, as Tesla is the market leader in electric vehicles and soon to be market leader in battery storage systems.

Tesla’s earnings estimates (TSLA ticker page on Seeking Alpha)

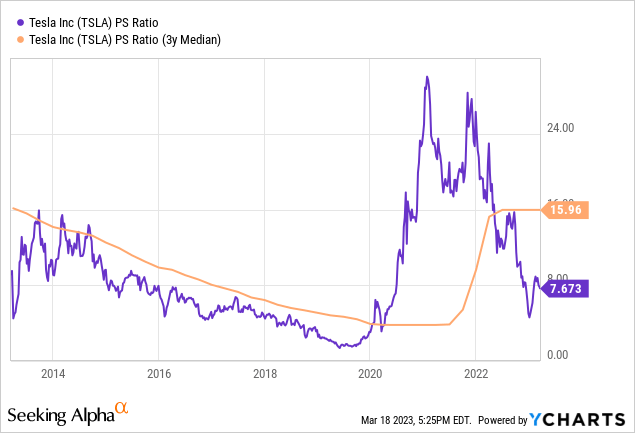

Another way to look at the stock’s valuation is to compare it to historical figures.

Now that Tesla is highly profitable (operating margin of 17%), the PE ratio has dropped significantly. The question is: what is an appropriate PE ratio? That question remains open since the volume/mix of battery production and electric vehicle sales in the future is unknown. The chart does tell us that the valuation is about average compared to historical figures.

Now that the company is profitable and more mature, we have insight into the profit margin of an EV company (Tesla, of course), so the price/sales ratio has less meaning. Therefore, I prefer to count on the 2025 projected PE ratio to assess buyability. Tesla is currently of good value given its strong growth potential for the coming years.

Risks To Mention

High growth comes with high risk, right? Before investing in Tesla, investors should consider macro-economic risks and company-specific risks.

Currently, the Federal Reserve has raised interest rates sharply to reduce the high inflation. While raising interest rates, it is also causing the yield curve to invert, implying that a recession is imminent within now and a year.

The car manufacturing market is highly cyclical, and consumers are reluctant to make large purchases such as a new car. Consumers could also opt for a car that is more fuel-efficient and more affordable than their current car. That changes the whole demand in a few years. Tesla played it well when it released the affordable Model 3 along with its luxury models. During a financial recession, the Model 3 could get a strong sales boost. Tesla is also diversifying its earnings as it looks to get more revenue from its battery storage systems and solar panels. Still, investors should keep in mind that the auto industry is cyclical and therefore risky.

Company-specific risks include the mania surrounding Tesla CEO Elon Musk. Elon Musk is known for his bold and risky statements and wants to colonize Mars. These risky statements could affect investors’ buying or selling of Tesla stock. Some like it, others don’t. Another company-specific risk is component supply problems. Although there were many supply chain issues, the company structurally misses delivery estimates. Also, the new EVs from Volkswagen, Audi and Hyundai pose risks to Tesla, which could reduce their market share.

Conclusion

Tesla has designed battery systems, electric vehicles and solar panels with the highest technological advancements. It has advanced technology to cool and heat their batteries which greatly extends battery life. Even after 200k miles the battery capacity remains above 80%. The innovation in batteries is evident with their new 4680 lithium-ion battery, which has a higher energy density and is sold at a lower price than current batteries. These technological advances are resonating with consumers, Tesla’s market share has skyrocketed and they have become the largest manufacturer of electric vehicles. By 2022, sales were up 51% and operating margin was historically high at 17%, the highest in the mass-produced car manufacturing market. The total addressable market for EVs looks rosy with a CAGR of 17%, and many analysts predict Tesla’s revenue will increase 30% this year. Recent cuts in car prices are improving affordability, and in January the number of orders rose twice as fast as production; demand is very high. A look at the stock valuation shows that the shares are favorably valued; the forward PE ratio for 2025 is only 26. Tesla operates in high-growth markets and is a leader in electric vehicles. The share valuation is attractive for a fast growing company in an expanding market. Tesla is favorably valued given its strong growth potential and therefore buyable.

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, but may initiate a beneficial Long position through a purchase of the stock, or the purchase of call options or similar derivatives in TSLA over the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.