Summary:

- China sales analysis demonstrates Tesla, Inc. price elasticity of demand, but price cuts are a two-edged sword.

- Tesla can no longer be assured of capturing demand created by price cuts, as it is no longer a single large player in a market it has created and nurtured.

- A large number of capable and growing new entrants to the BEV space create a new dynamic for Tesla.

- I am downgrading Tesla to Hold pending seeing how continuing cuts to BEV prices play out over the next couple of quarters.

Sky_Blue

Above: Tesla Gigafactory 3 Shanghai.

Investment Thesis

Tesla Price Elasticity –

In my recent article, “Tesla’s Elon Musk, Modern-Day Henry Ford With A Twist?” I wrote:

Anyone who thinks Tesla price cuts are driven by reduced demand, fails to understand the Tesla business model. The Tesla business model is about contributing to world decarbonization by replacing ICE vehicles with BEVs (battery electric vehicles) powered by renewable energy. To achieve that objective requires continuing decreases in Tesla BEV prices to make them more affordable, enabling wide uptake.

That does not mean Tesla, Inc. (NASDAQ:TSLA) does not concern itself with elasticity of demand when setting prices. Excerpted from a reply by Elon Musk in the Q&A session of Tesla’s 2023 Investor Day:

…one of the things we weren’t sure about was the price elasticity of demand for Teslas so like as we lower the price how much does the demand increase…and we found that even small changes in the price have a big effect on demand – very big – so that was a good thing to learn…

I thought Tesla’s Q1 2023 might provide an opportunity to analyze and understand Tesla’s price elasticity in the Chinese market. While there is no question lower prices are attractive to buyers, I found a number of factors confound any analysis of the impact of elasticity of demand on the volume of Tesla autos sold in China.

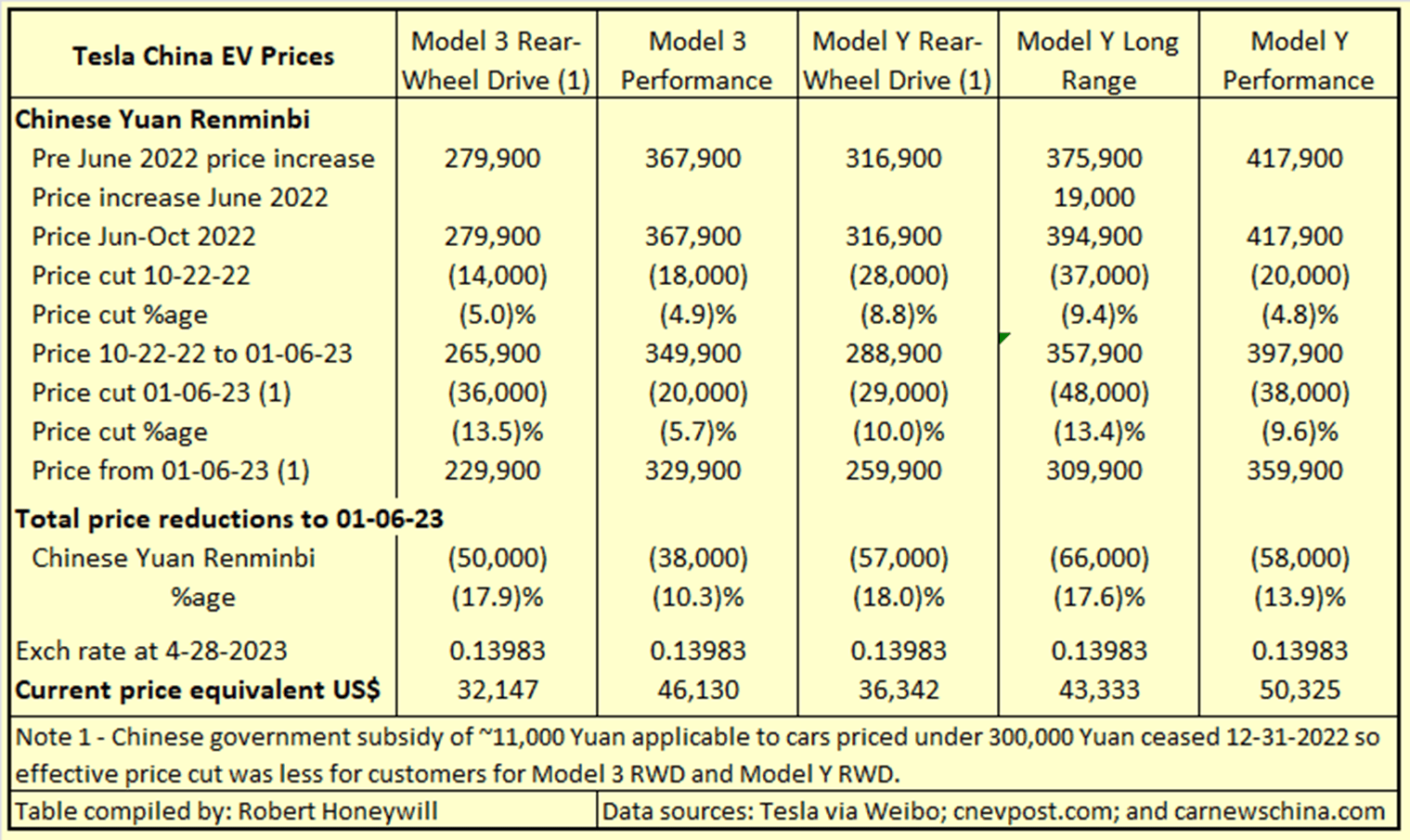

Table 1 below shows Tesla EV prices in China over the period June 2022 to January 2023.

Table 1

Tesla via Weibo; cnevpost.com; carnewschina.com

Tesla increased prices in June 2022 to dampen demand for Model Y Long Range, as COVID restrictions and lockdowns had severely impacted production. Once production had resumed full time, prices were cut for all models in October 2022 to stimulate demand. Demand was also stimulated in this period by the impending cessation of a Chinese government subsidy of 11,000 Yuan for electric vehicles (“EVs”) priced under 300,000 Yuan.

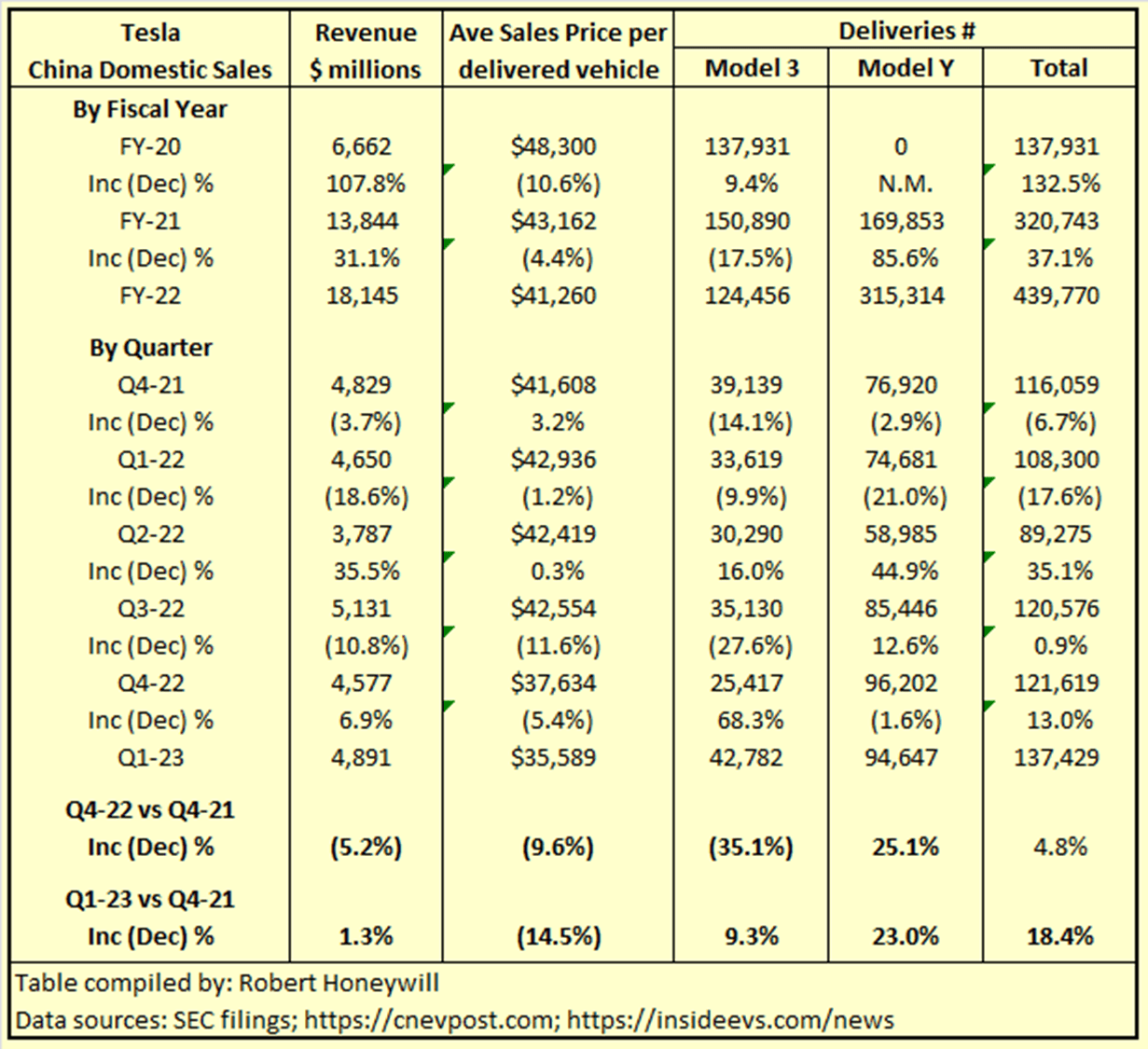

Table 2 below shows Tesla China sales, including for the same period covered by Table 1.

Table 2

SEC filings; cnevpost.com; insideevs.com

Comments on Table 2 –

Analysis By Fiscal Year –

FY-21 versus FY-20

A decrease of 10.6% in the average price per delivered vehicle, for FY-21 compared to FY-20, is accompanied by a 132.5% increase in total deliveries, and an increase of 107.8% in revenue in FY-21. At first glance, this is supportive of elasticity of demand. Looking more closely at the numbers, I can see that growth in FY-21 was greatly influenced by the commencement of production and sale of Model Y in China.

Accordingly, the average price reductions per delivered vehicle of 10.6% would be understated, due to the effect of the higher priced Model Y on the average sales price per delivered vehicle in FY-21. And most of the increase in delivered vehicles is Model Y vehicles which increase comes off a zero base year. I believe it is difficult to draw any meaningful conclusions on elasticity of demand from the FY-21 versus FY-20 statistics.

FY-22 versus FY-21

A decrease of 4.4% in the average price per delivered vehicle, for FY-22 compared to FY-21, is accompanied by a 37.1% increase in total deliveries, and an increase of 31.1% in revenue in FY-21. Again, at first glance, this is supportive of strong elasticity of demand. But looking at the detail, Model 3 deliveries declined by 17.5%, while Model Y increased by 85.6%. Of course, Model Y production would still be ramping up in the period, which would account for some of the higher growth rate.

Also, according to this cnevpost.com article, “… the Chinese population’s preference for SUVs has allowed the Model Y to perform better than the Model 3 for most of the past year.” The early and middle part of the year were also beset by COVID lockdowns and restrictions, limiting production for periods. In the circumstances, it is understood priority was given to production of the more popular Model Y. The section of Table 2 by quarter allows a more granular analysis.

Analysis By Quarter –

Q4-22 versus Q4-21

A 9.6% reduction in average price of delivered vehicles was accompanied by a 4.8% increase in total vehicle deliveries, and a 5.2$ reduction in total revenue. But Model 3 deliveries declined by 35.1% quarter on corresponding previous quarter, while the dearer Model Y deliveries increased by 25.1%. The higher Model Y deliveries in Q4-2022 could be explained by the 28,000 Yuan reduction in Model Y Rear-wheel Drive, which caused the price to fall below 300,000 Yuan and thus attract the 11,000 Yuan subsidy to give a total 39,000 Yuan reduction, provided purchased before December 31, 2022. The difference between Model 3 and Model Y Rear Wheel Drive was reduced to 23,000 Yuan (Model 3 – 254,900 Yuan net of subsidy and Model Y 277,900 net of subsidy). This could have induced potential Model 3 buyers to buy Model Y instead.

Q1-23 versus Q4-21

The massive cuts to prices in January resulted in average sales price per delivered vehicle decreasing by 14.5% between Q4-2021 and Q1-2023. Despite an 18.4% increase in total deliveries, total sales revenue increased by only1.3%. Model 3 deliveries showed a strong recovery from the previous quarter, with Q1-2023 deliveries of 42,782 up 68.3% on Q4-2022 deliveries of 25,417. This resulted in Model 3 deliveries in Q1-2023 being up 9.3% on Q4-2022. The January cut in Model Y prices appears not to have had the same impact, with quarter on quarter deliveries declining by 1.6%. However, Q1-2023 deliveries of Model Y grew by 23.0% over Q4-2022, compared to comparative growth of 9.3% for Model 3.

Price Cuts A Two-edged Sword

With the large price cuts in January 2023, Tesla received a great deal of negative feedback. This came from Tesla customers who bought in December 2022, only to see the new price of their Tesla fall by up to 48,000 Yuan in a matter of days. Tesla representative Grace Tao Lin posted this message on Weibo on Jan. 6, 2023 announcing the price cuts,

Behind Tesla’s price adjustments, there are countless engineering innovations, which are essentially unique and excellent laws of cost control: including not limited to vehicle integration design, production line design, supply chain management, and even millisecond-level optimization of robotic arm coordination Route… Start from “first principles” and insist on cost pricing. Respond to the country’s call with practical actions to promote economic development and release consumption potential. 2023 Let’s welcome a better life together.

A couple of examples of the multitude of angry responses to that message,

How many old car owners’ hearts have been chilled, do you still dare to buy it?

Harm the interests of old car owners! Old car owners are not as good as dogs!

The Impact of Increasing Competition

I don’t believe there can be any doubt that lower Tesla selling prices will increase volume of sales compared to no price cut. But the impact of lower prices has to be considered in the context of price competition from other BEV manufacturers. From a June 8, 2023, article,

BYD begins pre-sales for 2023 Song Plus series SUVs as its model changeover continues…Pre-sales for the new Song Plus DM-i start at RMB 169,800 and the Song Plus EV at RMB 179,800. and

BYD launches revamped Seal with lower prices. The new BYD Seal starts at RMB 189,800, down RMB 23,000 from its predecessor’s RMB 212,800.

So BYD Company Limited (OTCPK:BYDDF) is already selling quality BEVs in China for the equivalent of $23,700 to $26,539. This is significantly below the Tesla China selling prices listed in Table 1 above. These prices are also within or below the target selling price of $25,000 to $30,000 for compact BEVs to be produced by Elon Musk’s next Tesla gigafactory in Mexico.

And BYD is not the only competitor, with numerous BEV start-ups in China, with some reported to be receiving subsidies up to 90,000 Yuan per vehicle from local authorities keen to see BEV development in their region.

Summary and Conclusions:

Initially, Tesla operated in a virtual vacuum, where it needed to create a need and a demand for a BEV, where in the absence of a product there was no established market. Over quite a lengthy period of time, Tesla has created that market, needing at times to juggle with production and demand to balance one with the other.

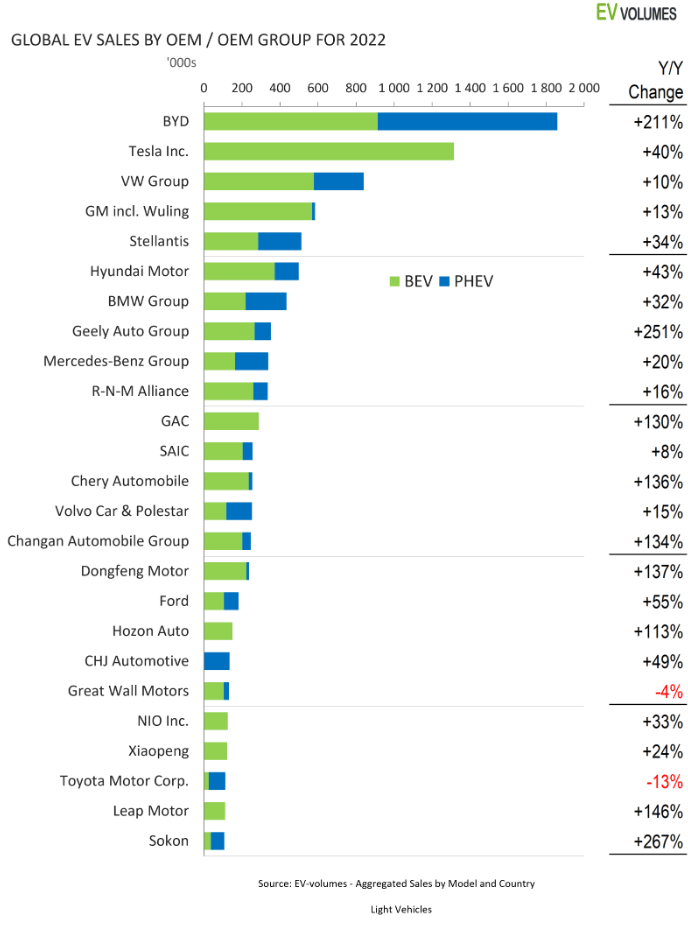

Through experimentation, it became clear to Tesla that there was considerable demand elasticity, and small adjustments to price could significantly alter demand. But Tesla is no longer operating in a vacuum. Numerous other players have entered the BEV industry, per Fig. 1 below from ev-volumes.com, all seeking to capture a share of a market almost single-handedly created by Tesla. And Tesla could soon be overtaken by BYD as the producer/seller of the world’s greatest number of Battery Electric Vehicles (BEVs).

Figure 1

ev-volumes.com

It is no longer the case that Tesla can cut prices to create increased demand, with the knowledge it is the only entity with the capability of meeting that demand. Other BEV manufacturers have already responded, and will almost certainly respond in the future, by cutting their own prices, possibly more than Tesla, in an effort to capture a larger share of a now well established market.

In my two previous articles on Tesla, I have rated the stock a Buy. With the BEV price cuts that have taken place, and which are continuing to the present, and with the growing number and capability of new entrants to the BEV market, I believe Tesla is now at a crossroads. Pending watching and analyzing further developments in this space, I find it prudent to downgrade Tesla, Inc. stock to a Hold for the present.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. I do not recommend that anyone act upon any investment information without first consulting an investment advisor and/or a tax advisor as to the suitability of such investments for their specific situation. Neither information nor any opinion expressed in this article constitutes a solicitation, an offer, or a recommendation to buy, sell, or dispose of any investment, or to provide any investment advice or service. An opinion in this article can change at any time without notice.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.