Summary:

- Tesla shares have soared after the U.S. election, reached a new all-time high on Tuesday, and now trade significantly above the historical average P/E ratio.

- While Tesla has shown strong delivery momentum in the long term as well as in China in the last month, shares are likely fully valued now.

- BYD Company Limited offers a more sensible valuation with comparable delivery volumes and gross margins, making it an attractive alternative in the large-cap EV market.

- Given the extremely bullish sentiment toward Tesla, it is prudent to scale back TSLA-related return expectations and reduce exposure, which is why I have decided to take profits here.

Martin Barraud/OJO Images via Getty Images

Tesla, Inc. (NASDAQ:TSLA)’s shares have passed their previous 3-year-old highs amid a massive post-election surge that has lifted the EV maker’s valuation to ~$1.5T. While I have been optimistic about Tesla’s recovery potential in FY 2024 and FY 2025 and specifically mentioned the autonomous vehicle market opportunity as a reason to own shares, I believe shares of Tesla are now trading significantly above fair value. This exposes investors to the risk of a potentially significant valuation draw-down once the current excitement dies down.

While I like Tesla’s long-term delivery up-trend and strong margin picture, I believe the company’s current opportunity in electric and autonomous vehicles is fully reflected in the company’s market cap. Therefore, I have decided to take profits and recommend investors to be fearful considering how greedy investors have become lately.

Previous rating

I rated shares of Tesla a strong buy before and after the company’s robotaxi event in October, which was widely received negatively by investors: Elon Musk Teaches The Market A Lesson. Tesla really benefited from positive delivery momentum in the third quarter, and the EV maker guided for up to 30% delivery growth in FY 2025. Now, with shares trading at 1.85X the three-year average price-to-earnings ratio, I believe Tesla’s market potential has been fully realized, and I see the shares as having run ahead of the EV company’s fundamentals.

Tesla’s revenue and delivery growth acceleration in FY 2025 is now fully priced in

Before I explain why I changed my opinion on Tesla, I would like to say that I continue to expect Tesla’s margin and delivery picture to improve in FY 2025. Recent delivery data from China showed strong momentum in sales for companies like NIO (NIO), XPeng (XPEV), and Li Auto (LI), and Tesla has guided for up to 30% delivery growth in FY 2025.

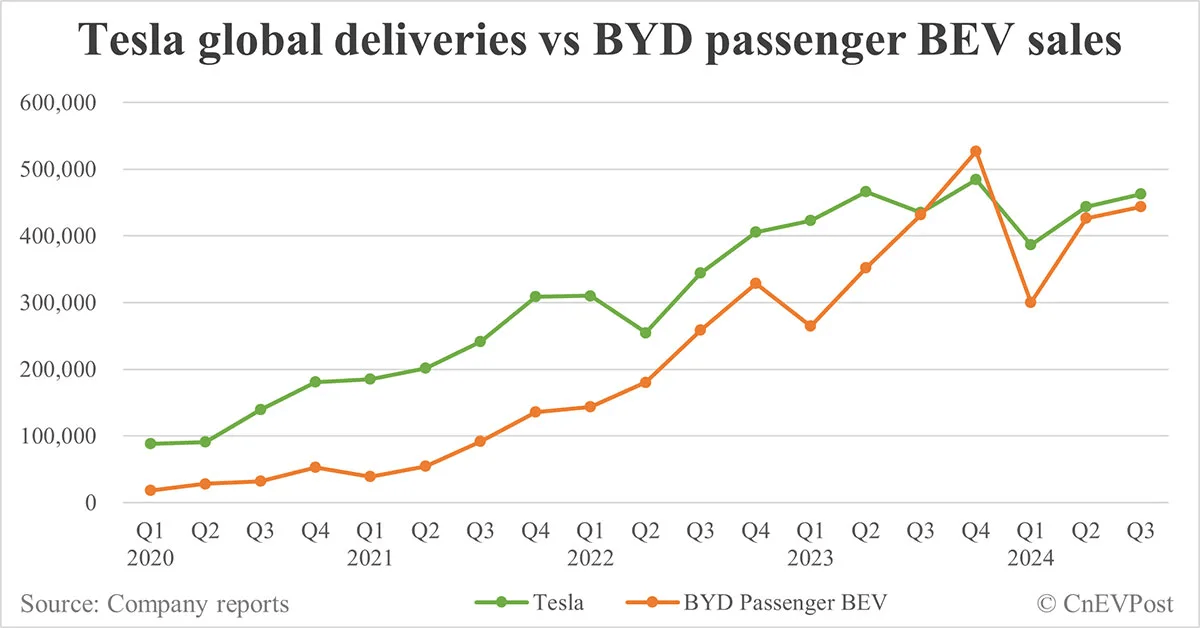

Tesla is in a neck-to-neck race with BYD Company Limited (OTCPK:BYDDF) which is by far Tesla’s most formidable competitor in China, but also on a global basis. Both companies roll hundreds of thousands of electric vehicles each quarter from their factory belts, and both EV makers are also very close in terms of gross margins.

In the most recent quarter, Q3 ’24, Tesla delivered 462,890 electric vehicles, showing approximately 6.4% year-over-year growth and 4.3% quarter-over-year. BYD sold 443,426 battery electric vehicles, implying 2.7% year-over-year and 4.1% quarter-over-quarter growth. However, BYD also makes hybrid models, which Tesla doesn’t, so BYD’s total delivery volume in the third fiscal quarter was significantly higher: in total the Chinese EV firm sold 1,129,256 new energy vehicles, showing 37.4% growth Y/Y and 14.9% growth Q/Q.

CnEVPost

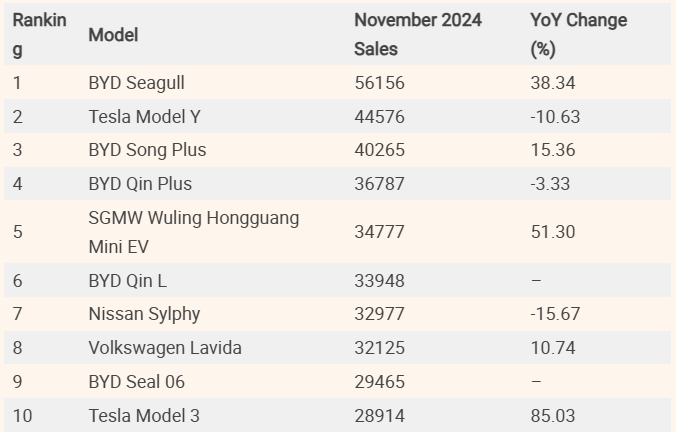

Tesla’s deliveries in China, numbers of which were released earlier this month, rebounded in November as well: last month the EV maker sold and delivered 78,856 electric vehicles in China, including 5,366 vehicles that were exported from China to other countries. Tesla’s China-made EV sales rebounded 15.5% month-over-month in November but were still down 4.3% Y/Y.

BYD, on the other hand, sold 504,003 passenger new energy vehicles in November, showing 0.7% growth month-over-month and 67.2% growth year-over-year. On a year-over-year basis, BYD is massively outperforming Tesla. Although Tesla is still leading BYD in terms of global BEV deliveries, there is a good chance that BYD will overtake Tesla in FY 2025 if BYD can sustain its current growth.

BYD is also the most popular EV and hybrid brand in China, with BYD having five of its available new energy vehicles ranked in the top ten best-selling EVs/hybrids in the month of November, according to CarNewsChina.

CarNewsChina

Tesla and BYD are also very close in gross margins, which isn’t surprising since both companies are the two largest new energy vehicle manufacturers globally. BYD overtook Tesla in terms of gross margins in FY 2023 and currently still has a slight lead: Tesla’s gross margin in the September quarter stood at 19.8% compared to 21.9% for BYD.

BYD’s gross margin trend is also pointing upward, while Tesla’s gross margins have dropped off. A very favorable delivery picture as well as a strong margin profile were two reasons why I continue to see a lot of valuation upsides for BYD, as I explained here.

Tesla is now widely overpriced

Tesla is currently valued at a forward price-to-earnings ratio of 147X—forward meaning based off FY 2025 consensus estimates. The forward P/E ratio is significantly detached from the company’s longer-term valuation average P/E ratio of 79.5X, which was already a high valuation multiplier. Currently, shares of Tesla are trading at an 85% higher valuation than they used to on average in the past three years. This enthusiasm is driven chiefly by Elon Musk being expected to be a beneficiary of Donald Trump’s election victory in November.

In my last work on the EV company, I have said that I saw a fair value for Tesla’s shares in the neighborhood of $293—based off a historical P/S ratio of ~8.0X—which Tesla now obviously widely exceeds. Tesla’s shares closed at $479.86 on Tuesday, a new all-time high for the EV maker.

BYD, on the other hand, offers investors a similar delivery volume than Tesla (excluding hybrids), an even more impressive up-trend in deliveries, comparable gross margins, and a much more sensible valuation. The reason for the large discount for BYD, relative to Tesla, is that the EV maker is operating mainly in China, although it has sizable export operations as well.

U.S. investors especially have been reluctant to invest money into Chinese EV makers given transparency and accounting concerns, as well as China’s 2020 crackdown measures. However, BYD offers one of the best values in the large-cap EV market segment, in my opinion. It is trading at a very attractive 0.8X price-to-revenue ratio, and BYD actually outperformed Tesla by a considerable margin in terms of Y/Y delivery growth in November.

| Tesla vs. Large-Cap Rivals | Tesla | BYD | Rivian | Average |

| Market Cap ($B) | $1,490.0 | $105.3 | $15.7 | $537.0 |

| Est. Revenue FY 2025 ($B) | $116.3 | $124.4 | $5.3 | $82.0 |

| Revenue Growth Y/Y | 16.5% | 18.6% | 12.9% | 16.0% |

| P/S Ratio FY 2025 | 12.8 | 0.8 | 3.0 | 5.5 |

(Source: Author)

Risks with Tesla

The biggest risk for Tesla is a potential decline in vehicle and gross margins in the coming quarters. With competition increasing and more legacy auto companies and EV start-ups launching slates of electric vehicles, margins could come under growing pressure in FY 2025.

XPeng and NIO have both announced low-cost EV brands, dubbed Mona and Onvo, to tap into an underserved segment in the EV market. A trend toward lower-priced EVs is most likely going to have a negative margin impact, on both a vehicle and a gross margin basis, for all EV makers, including the largest-volume producers. What would change my mind about Tesla is if the company were to see a serious margin upswing and accelerating momentum in autonomous vehicles.

Final thoughts

Be greedy when others are fearful, and be fearful when others are greedy. This wisdom has served me very well in the long term. I believe, with sentiment towards Tesla now being extremely bullish, it is time to scale back expectations about Tesla-related stock returns and take on a bit of a contrarian position.

Since shares of Tesla are now widely overvalued, based off the company’s 3-year valuation average, I believe the risk profile is not anywhere near as attractive as it was last year, or even before the U.S. election. While Tesla certainly has a considerable growth opportunity in both electric and autonomous vehicles, I believe shares of Tesla are more than fully valued and now significantly trade above my fair value estimate of $293 per share. With BYD also offering very serious value here, I believe the Chinese EV firm may be the better deal going forward.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of BYD, NIO, LI either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.