Tesla, Inc. has outperformed the market since my last “Neutral/Hold” update. However, I believe this is temporary. I maintain my earlier stance:

The input commodities outlook is favorable. Many of Tesla’s raw material markets such as lithium, nickel, cobalt, and graphite are in a state of oversupply with a dampened price outlook.

Tesla’s revenue mix shift away from automotive and toward the energy business is another accretive factor to gross margins.

The recent run-up in prices seems to be driven by multiple expansion rather than expectations of earnings growth. I doubt the sustainability of this amid the higher-for-longer rates narrative.

The relative technicals also point toward a negative to neutral outlook for Tesla vs. the S&P 500.

Olivier Le Moal

Performance Assessment

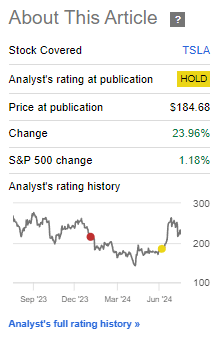

In my last coverage of Tesla, Inc. (NASDAQ:TSLA), I issued a “Neutral/Hold” rating to reflect my view that the stock would perform in line with the S&P500 (SPY, SPX) going forward. This has led to a missed opportunity, as Tesla has beaten the market by more than 20% since then:

Performance since last update on Tesla (Seeking Alpha, Author’s Last Article on Tesla)

However, I am not too fussed about this, as the time horizon I had in mind for my view is a bit longer. And there are reasons to believe the sharp spike up in prices is temporary, as discussed later in this article:

Thesis Update

After Q2 FY24, a key change in my fundamental view is my outlook on Tesla’s margins; I believe they have bottomed out for these 2 key reasons:

Input commodities outlook is favorable.

Revenue mix shift is margin accretive.

Input commodities outlook is favorable

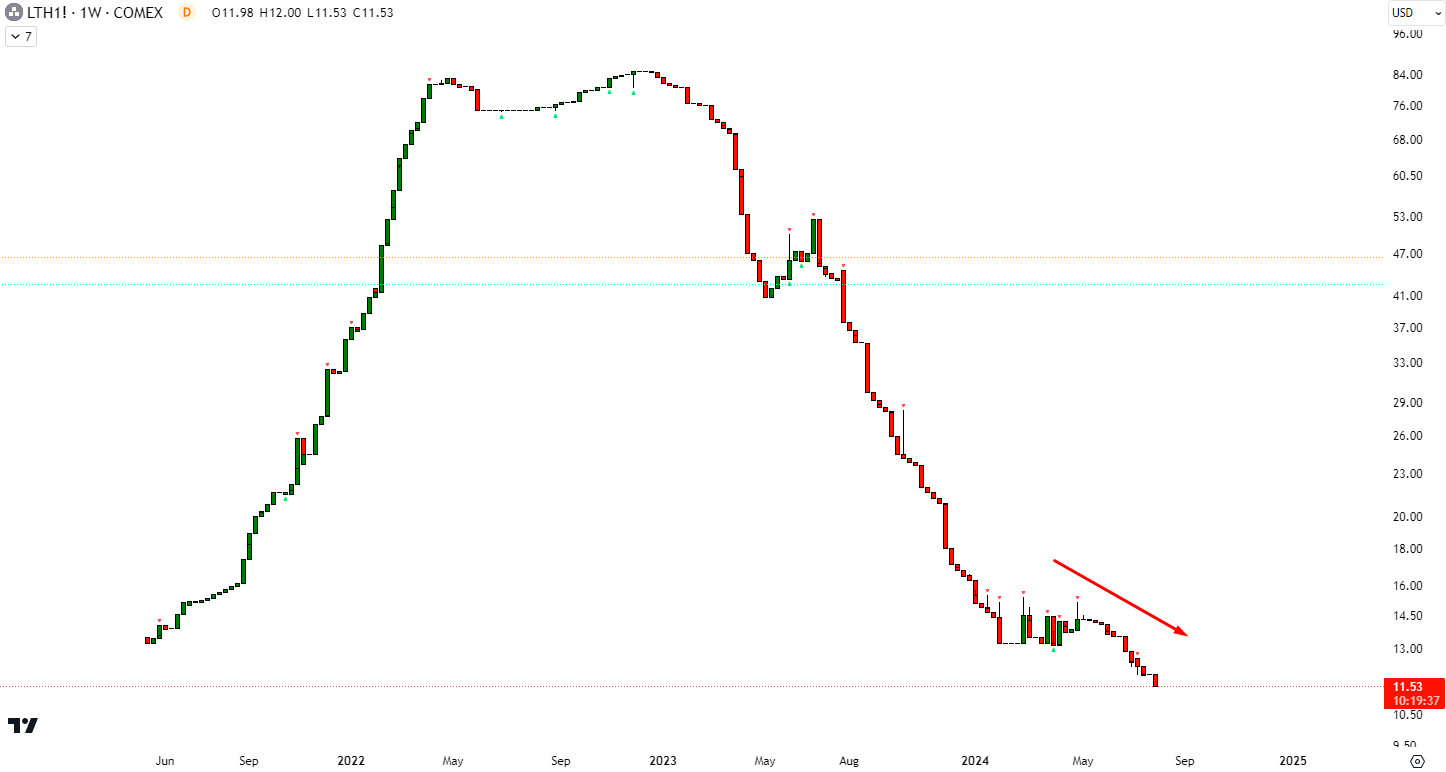

In the latest Q2 FY24 earnings call, CFO Vaibhav Taneja noted that they are “experiencing material costs trending down.” These refer mostly to input commodity costs. In addition to lithium, this includes nickel, cobalt, and graphite. Looking at the current and expected demand-supply situation in these key commodities, I believe commodity costs are likely to stabilize or see further price falls:

… lithium market is consolidating in an environment of oversupply, weak demand, and high inventory. …there is a risk of further price weakness due to the continued oversupply.

– Will Adams, Head of Base Metals Research at FastMarkets.

Lithium Futures Prices (TradingView)

Given this, I believe lithium prices are likely to continue falling, which is beneficial for Tesla, particularly in its energy business.

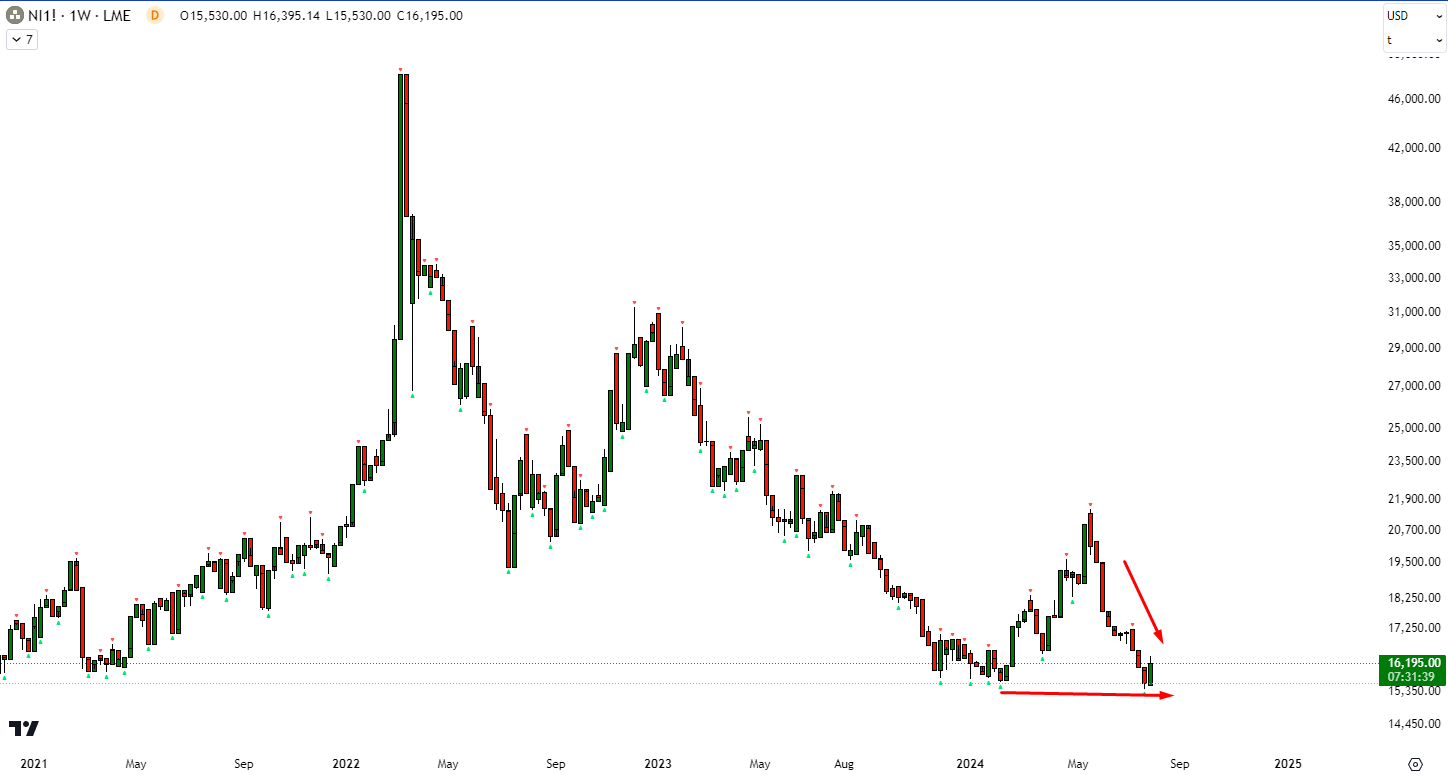

Nickel

Indonesia is the world’s largest supplier of Nickel. So far, this country has been responsible for higher than normal production of Nickel, which has led to an oversupplied market. This paints a backdrop that is favorable for continued low and stable pricing:

Looking ahead, we believe nickel prices are likely to remain under pressure, at least in the near term, amid a weak macro picture and a sustained market surplus.

– Ewa Manthey, ING Commodities Strategist

Nickel Futures Prices (TradingView)

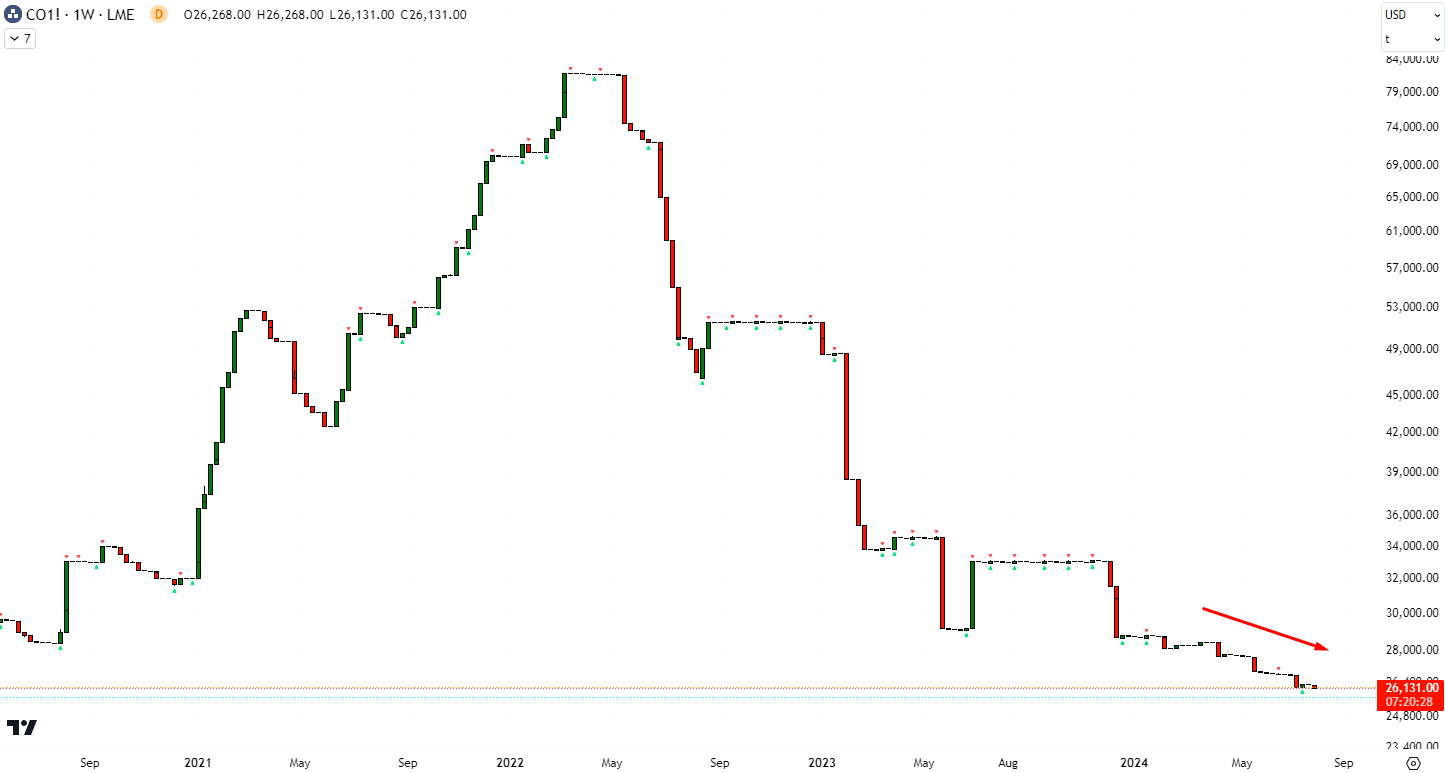

Cobalt

The combination of cobalt and nickel helps improve energy density in lithium-ion batteries. The cobalt market is also in a state of oversupply. This has been driven by increased mine production in the Democratic Republic of Congo, Indonesia. Furthermore, there is higher refinery production coming from China as it aims to ramp up EV production.

Though increased EV demand is constructive to Cobalt prices, the market expects a continued weak pricing environment to continue as the extent of oversupply is far greater.

Cobalt Futures Prices (TradingView)

Graphite

Tesla needs graphite for its EV batteries. Graphite is the key material used in one part (anode) of the lithium-ion batteries. China is the world’s leading graphite supplier, making more than 90% of the world’s graphite. Similar to cobalt, China has recently added new graphite capacity. According to Commodities research firm Wood Mackenzie, this is expected to keep graphite prices low.

There is no financial market for graphite. Hence, it is difficult to provide a price chart.

Summary

Thus, Tesla’s key commodities are all in a state of oversupply, which is expected to keep prices low. Tesla is not completely hedged against these input commodities. Hence, I believe this is a medium to long-term margin tailwind for Tesla’s gross margin profile:

Tesla’s energy business is growing rapidly at almost 100% YoY, leading to a material revenue mix shift:

Energy Generation and Storage Revenues Mix (Company Filings, Author’s Analysis)

I believe this is an additional tailwind to gross margins, as the energy business commands higher margins than the automotive business (mid-20s vs. high teens):

Automotive vs Energy Business Gross Margins (Company Filings, Author’s Analysis)

Valuation driven by multiple expansion and earnings contraction is not as sustainable

1-yr forward P/E and MCAP (Capital IQ, Author’s Analysis)

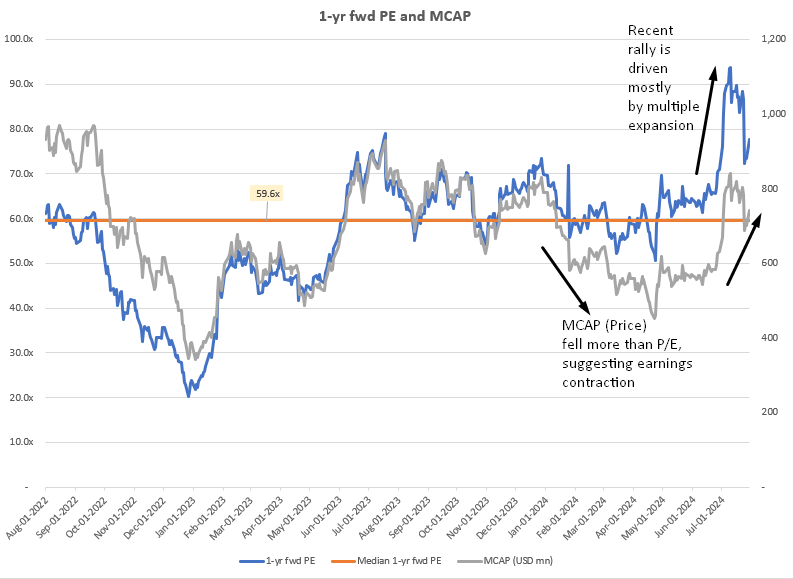

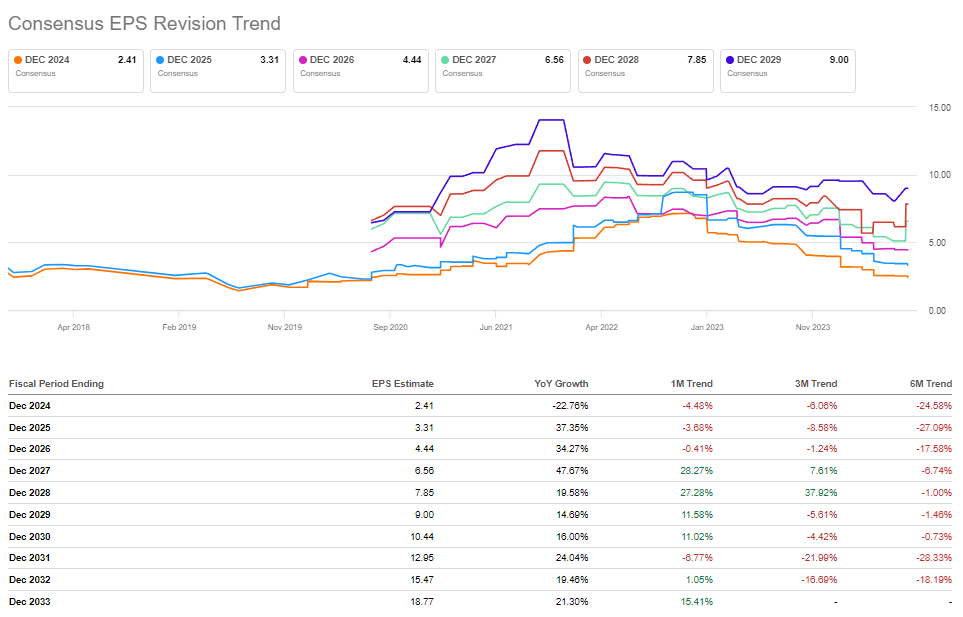

Looking at the valuation and market capitalization (MCAP) movements of TSLA stock, I notice that MCAP had fallen more than the 1-yr fwd P/E earlier this year. This corresponds to the stock’s consensus earnings downgrade trends:

Tesla EPS Revision Downgrade Trends (Seeking Alpha)

More recently, the stock and the P/E multiple have blasted up, with the latter to a seemingly greater extent. These are signs of multiple expansion. I believe in the current context of the Fed’s higher-for-longer rates stance, this may be an unsustainable run-up plus re-rating as growth stocks tend to be more sensitive to rates. Note that the current 1-yr fwd P/E of 77.8x also implies a 30% premium to the 59.6x median level over the last 2 years. Of course, the market may be pricing in growth optionalities such as Robotaxis. However, given the historical and likely continuing track record of overpromising and underdelivering on new product launches, I prefer to be cautious and skeptical in the medium term.

Technical Analysis

If this is your first time reading a Hunting Alpha article using Technical Analysis, you may want to read this post, which explains how and why I read the charts the way I do. All my charts reflect total shareholder returns as they are adjusted for dividends/distributions.

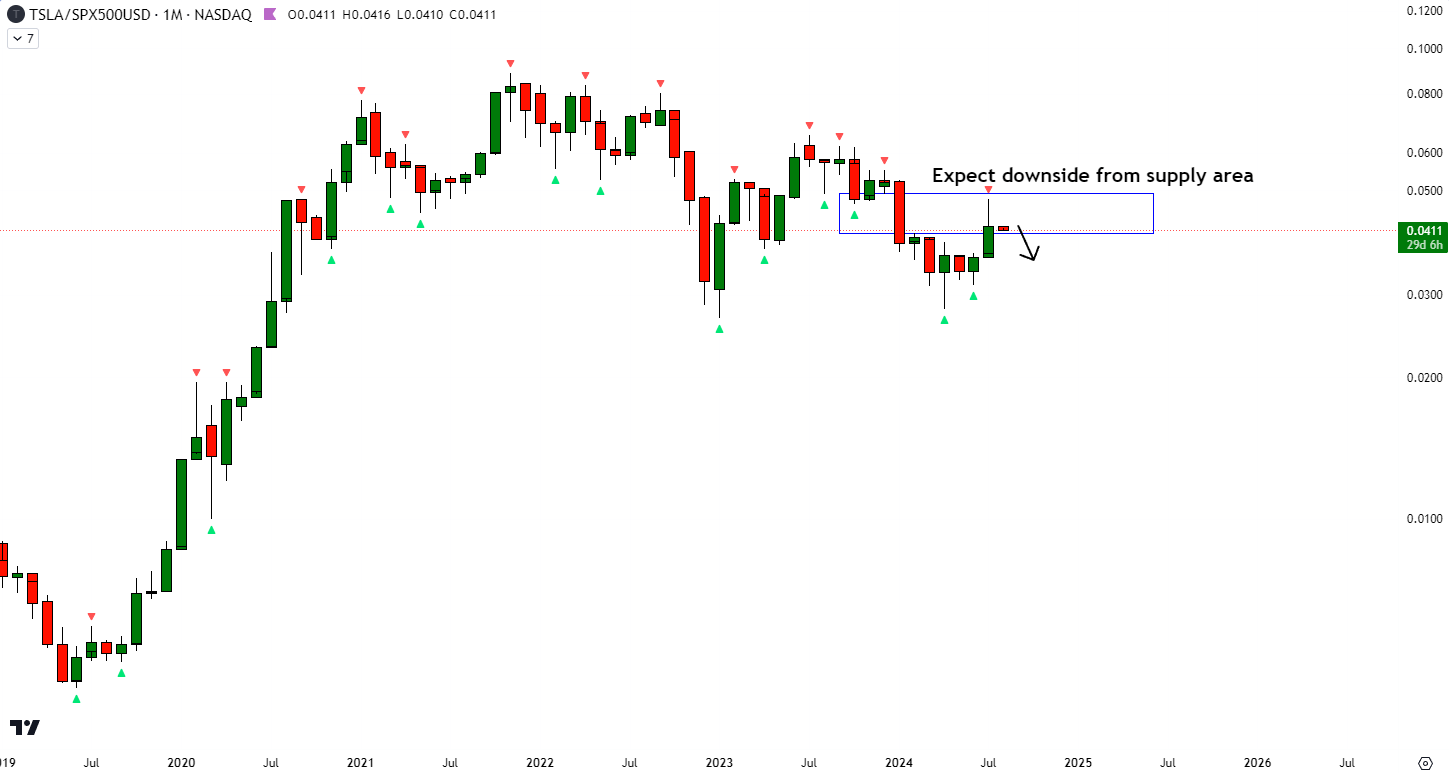

Relative Read of TSLA vs. SPX500

TSLA vs SPX500 Technical Analysis (TradingView, Author’s Analysis)

In the relative monthly chart of TSLA vs. the S&P500, I see that the ratio prices are near a key supply level. However, the approach to the level has been strong and rapid. Hence, I anticipate some downside to sideways action ahead. This would correspond to performance a bit worse or in line with the S&P 500.

Key Risks and Monitorables

Much of my thesis is based on the cost side of gross margins facing favorable tailwinds. However, my overall view that gross margins may have bottomed out may be refuted by pricing cuts on Tesla’s cars. Pricing trends are something I continuously track for Tesla.

Since my last update on Tesla around 19 June 2024, none of the models in the US or China have seen pricing cuts. Rather, prices have been stable in almost all models except the Model X and Model S in the US, which have seen a 2-3% price hike. However, this is of little bullish significance as these premium models make up only 5% of total deliveries.

Takeaway & Positioning

I believe Tesla is set to benefit from 2 key gross margin tailwinds. First, many of the company’s input commodities such as lithium, nickel, cobalt, and nickel are in a state of oversupply with favorable pricing outlooks for the automaker. Second, the company’s energy business is growing rapidly to put into effect a mix shift in the revenue profile of the business that is margin-accretive.

On the valuations side, I believe Tesla, Inc. stock has seen a re-rating recently. However, I doubt the sustainability of the price and multiples run-up, especially considering the higher-for-longer rates stance taken by the Fed.

From a technical analysis perspective vs. the S&P 500, I posit that the stock is poised to move sideways to down, suggesting performance in line with lagging the S&P 500.

Given these mixed signals of both bullish and bearish factors in play, I rate the stock a “Neutral/Hold.”

How to interpret Hunting Alpha’s ratings:

Strong Buy: Expect the company to outperform the S&P 500 on a total shareholder return basis, with higher-than-usual confidence.

Buy: Expect the company to outperform the S&P 500 on a total shareholder return basis.

Neutral/hold: Expect the company to perform in line with the S&P 500 on a total shareholder return basis.

Sell: Expect the company to underperform the S&P 500 on a total shareholder return basis.

Strong Sell: Expect the company to underperform the S&P500 on a total shareholder return basis, with higher-than-usual confidence.

The typical time-horizon for my views is multiple quarters to around a year. It is not set in stone. However, I will share updates on my changes in stance in a pinned comment to this article and may also publish a new article discussing the reasons for the change in view.

Analyst’s Disclosure:I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.