Summary:

- Tesla, Inc. is recalling 2 million vehicles due to issues with its Autopilot driver assistance system.

- The direct costs of the recall are relatively low, but the indirect costs, such as brand damage, could be significant.

- The recall highlights the risks of investing in Tesla, as the company’s high valuation is based on its (presumed) progress in full self-driving technology.

ch1kyr/iStock Editorial via Getty Images

Article Thesis

Tesla, Inc. (NASDAQ:TSLA), a leading electric vehicle (“EV”) player that is also ambitious in the area of full self-driving (“FSD”) vehicle technology, was forced to recall 2 million of its vehicles due to problems with its Autopilot. While the direct costs of this recall are pretty low, the indirect costs, e.g., due to brand damage, could be more relevant. Overall, this issue showcases the risks of an investment in this highly-valued, expensive automobile company where significant progress in self-driving tech is baked into the stock price.

What Happened?

On Wednesday, Tesla filed a recall for more than 2 million of its vehicles. The issue at hand is that Tesla’s Autopilot driver assistance system is not going far enough when it comes to making sure that drivers are engaged and ready to step in when needed.

Overall, a pretty large portion of the vehicles that Tesla has sold in the United States are affected — the recall includes vehicles that were produced between 2012 and 2023.

Another important point in the release is that the NHTSA is continuing its investigation into Tesla’s Autopilot. While we don’t know yet what the outcome of that ongoing investigation will be, there is a possibility that further required updates, further recalls, and so on will be announced in the future.

Impact Of Autopilot Recall: Direct And Indirect

Let’s first start with a point that is positive for Tesla: this recall can be solved via an over-the-air update. This means that the direct costs of this recall are relatively low, compared to a recall that requires vehicles to be manually adjusted at a shop.

Still, there are some direct costs for this recall: when millions of customers are affected, there will surely be at least some customers that require explanations, that demand refunds, that will sue, and so on. This will cause some expenses for Tesla, although the costs will not be dramatic. Compared to other recalls, e.g., a required substitution of faulty airbags, this will be a pretty low-cost recall — many of the affected customers that do not require assistance, explanations, that do not sue, and so on, will essentially cause zero costs. Also, Tesla is still a pretty profitable company in absolute terms, having generated around $3.7 billion of free cash flow over the last year, according to YCharts. On top of that, Tesla has a sizeable cash position on its balance sheet. Some additional direct expenses will thus hardly be a major issue for Tesla.

And yet, Tesla’s market capitalization declined by a pretty hefty $15 billion on the day the news broke, while the broad market rose substantially (the S&P 500 (SP500) was up 0.6% at the time of writing). Since the direct costs of this recall are by far not as high as $15 billion, then the explanation for this market reaction could be the indirect costs this issue could cause.

While those indirect costs are very hard to forecast, it seems logical to me that there will be some. Let’s take a look. First, the news about Tesla’s Autopilot requiring a recall will cause some brand damage. Millions of people will read about this recall, while others will hear about it on the news. Not all of these will delve into the details to see what the issue is about and what Tesla will do via its over-the-air updates. Some will only read the headline, and the “Tesla’s Autopilot has issues” bit of information will settle in their minds. This naturally will hurt the brand image of Tesla, which also happens when other automobile brands do recalls when something is wrong with their vehicles.

Even for those consumers who are more interested in the subject and who delve into the details of this recall, some negative associations when it comes to Tesla could emerge. After all, the recall means that Tesla wasn’t doing enough to keep its drivers safe — which is why an update of the Autopilot is needed. If Tesla’s Autopilot had been perfect in the past, then no update/recall would be required. Some consumers could interpret this as “Tesla wasn’t doing enough to keep its drivers safe” or “Tesla was risking the health of its customers,” and so on. Of course, not everyone will think this way — many will just not care about the issue too much, and some will think that Tesla was right in the way they had set up Autopilot in the past. But even if only some people end up thinking badly about Tesla due to the way the company had set up its Autopilot driver assistance system in the past, then Tesla’s brand value in the eyes of these consumers will be hurt. This, in turn, could decrease the likelihood of these consumers buying a Tesla vehicle in the future.

Other potential customers will not mind the safety angle of this recall but might end up thinking worse about Tesla for another reason. When they delve into the details of this recall, they might end up thinking something along the lines of “Tesla’s Autopilot is not as advantaged as I had previously thought,” which could also lower the likelihood of these consumers buying a Tesla vehicle in the future.

We don’t know yet how large this impact will be, but logic and the market reaction suggest that this issue affecting millions of vehicles and customers will cause at least some longer-lasting brand issues. Of course, Tesla will still sell basically all the vehicles that it manufactures — but brand damage could impact the price these vehicles will sell for. Tesla had to lower the price of its vehicles repeatedly over the last year, and negative news that could negatively affect the company’s image might force further price reductions in the future in order for Tesla to sell its entire production. Other automobile companies sell more or less all the vehicles they produce as well, by the way, but like Tesla, they sometimes have to incentivize consumers by lowering prices.

The Risk Of Self-Driving Success Being Priced In

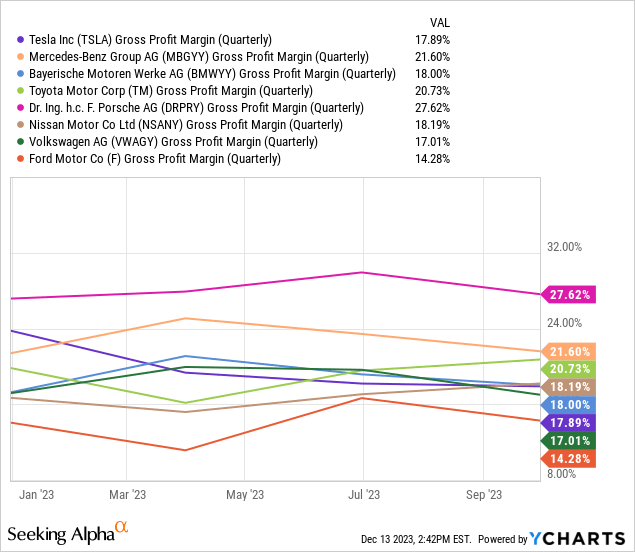

Tesla’s current Autopilot issue also brings up another risk for Tesla’s share price, I believe. Right now, Tesla trades at more than 70x net profits. That is a very high valuation for a company that has average margins at best:

In the most recent quarter, Tesla’s gross margin was lower than that of premium peers such as Mercedes (OTCPK:MBGYY), Porsche (OTCPK:DRPRY), etc., and even lower compared to mass market manufacturers such as Toyota (TM) and Nissan (OTCPK:NSANY). Tesla marginally outperformed Volkswagen (OTCPK:VWAGY) and beat Ford (F), but that’s hardly a reason for Tesla to trade at an ultra-high valuation.

Tesla is growing faster than most of its legacy peers, but that alone does not warrant a 70x earnings multiple — and Tesla’s growth hasn’t been especially compelling in recent quarters anyway, as revenues rose by just 9% during the most recent quarter. Nissan, for example, grew faster during the most recent quarter, yet it trades at 5x net profits, meaning lower-growth Tesla trades at a ~1,300% premium.

The explanation for a significant portion of Tesla’s massive valuation premium compared to other automobile companies is that massive success in the self-driving tech space is priced into Tesla’s stock — even bullish analysts and investors such as Cathie Wood (ARKK) acknowledge that Tesla’s self-driving ventures are a big part of their bullish thesis. And this might eventually pay off, if Tesla can indeed deliver the best self-driving tech product in the world and if the company captures a massive market share in a market that might turn out to be highly profitable. These are some big ifs, however, and in case Tesla is not able to deliver what Elon Musk promises/hopes the company will deliver, then the stock price could suffer significantly.

Tesla, Inc. has, so far, underperformed the company’s expectations and promises in the self-driving tech space repeatedly. If that continues, then the market could eventually start to value Tesla more in line with other automobile companies. For a company trading at more than 70x net profits, that could spell trouble. For me, very expensive Tesla remains an avoid (but not a short).

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Is This an Income Stream Which Induces Fear?

The primary goal of the Cash Flow Kingdom Income Portfolio is to produce an overall yield in the 7% – 10% range. We accomplish this by combining several different income streams to form an attractive, steady portfolio payout. The portfolio’s price can fluctuate, but the income stream remains consistent. Start your free two-week trial today!

The primary goal of the Cash Flow Kingdom Income Portfolio is to produce an overall yield in the 7% – 10% range. We accomplish this by combining several different income streams to form an attractive, steady portfolio payout. The portfolio’s price can fluctuate, but the income stream remains consistent. Start your free two-week trial today!