Tesla, Inc. stock price plunged about 12% after the Q2 earnings report.

The lackluster Q2 results have been dissected by many investment websites.

This article focuses on two issues that are less discussed but contain crucial leading information on its profitability going forward.

They are the inventory buildup and declining automotive gross profit margin when adjusted for regulatory credits.

boygovideo/iStock via Getty Images

TSLA stock: Q2 earnings overview

In my last article on Tesla Inc. (NASDAQ:TSLA), I presented a preview of its Q2 earnings report (“ER”). As illustrated by the chart below, the article was titled “Tesla Q2 Preview: Lease Accounting In Focus.” As the title suggested, the goal of the article was to caution investors about A) the inventory buildup due to slower delivery, and B) the uncertainties in inventory and delivery data caused by its use of lease accounting. More specifically,

Its inventory buildup remains a key concern despite Q2’s consensus-beating delivery data. Uncertainties around lease accounting further cloud the signal from the delivery data. I urge you to pay close attention to additional information that can provide clarity in its Q2 earnings report.

Seeking Alpha

Since then, the company has reported its 2024 Q2 ER. By these times, you must have had plenty of time to dissect the numbers, and several other SA authors have written review articles on it already. So I won’t add onto what has already been said. Overall, it was a lackluster quarter and TSLA’s stock prices plunged by about 12% (translating into a loss of ~$100 billion in market cap) during intraday trading after the release of the ER.

In this article, I will focus on two issues that are less often discussed in other review articles but provide crucial leading information on its profitability going forward.

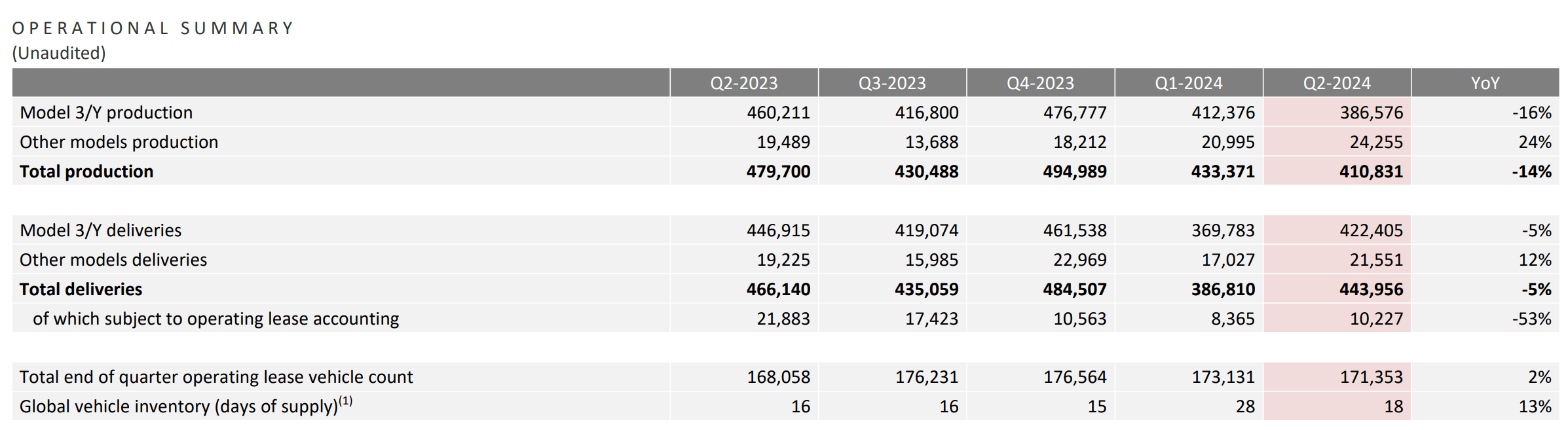

First, I want to follow up on the concern I had in my preview article. On this front, unfortunately, the numbers reported in the ER did not ameliorate my above concerns. The chart below shows Tesla’s total deliveries, lease vehicle count, and inventory from Q2 2023 to Q2 2024. As seen, total deliveries decreased from 466,140 in Q2 2023 to 443,956 in Q2 2024, a 5% decline. Meanwhile, the total end-of-quarter operating lease vehicle count increased from 168,058 in Q2 2023 to 171,353 in Q2 2024, a 2% increase. The final piece of bad news on this front was that its global vehicle inventory (in terms of days of supply outstanding) dialed in at 18 days in Q2, a 15% increase from 16 days a year ago.

As argued in my earlier article, I view these numbers as reliable indicators that TSLA’s EVs no longer enjoy the demand, popularity, and pricing power they used to.

Next, I will explain another key issue that has surfaced from its Q2 ER – the continued decline of gross profit margin (GPM) when regulatory credits are excluded.

TSLA Q2 ER

TSLA stock: gross margin

In the Q2 ER, TSLA reported a GPM of 18%. To better contextualize things, the chart below shows Tesla’s gross profit margin from Q2 2023 to Q2 2024. As seen, the gross profit margin has remained relatively stable, fluctuating between 17.4% and 18.2% in the past 4 quarters. And the GPM of 18% reported in Q2 2024 was only 23 basis points below the level a year ago and about 60 basis points above the level a quarter ago.

Thus, on the surface, there is nothing alarming here. However, the reported margin is very misleading in my view as it lumped the regulatory credits as elaborated on next.

TSLA Q2 ER

TSLA stock Q2: regulatory credits in focus

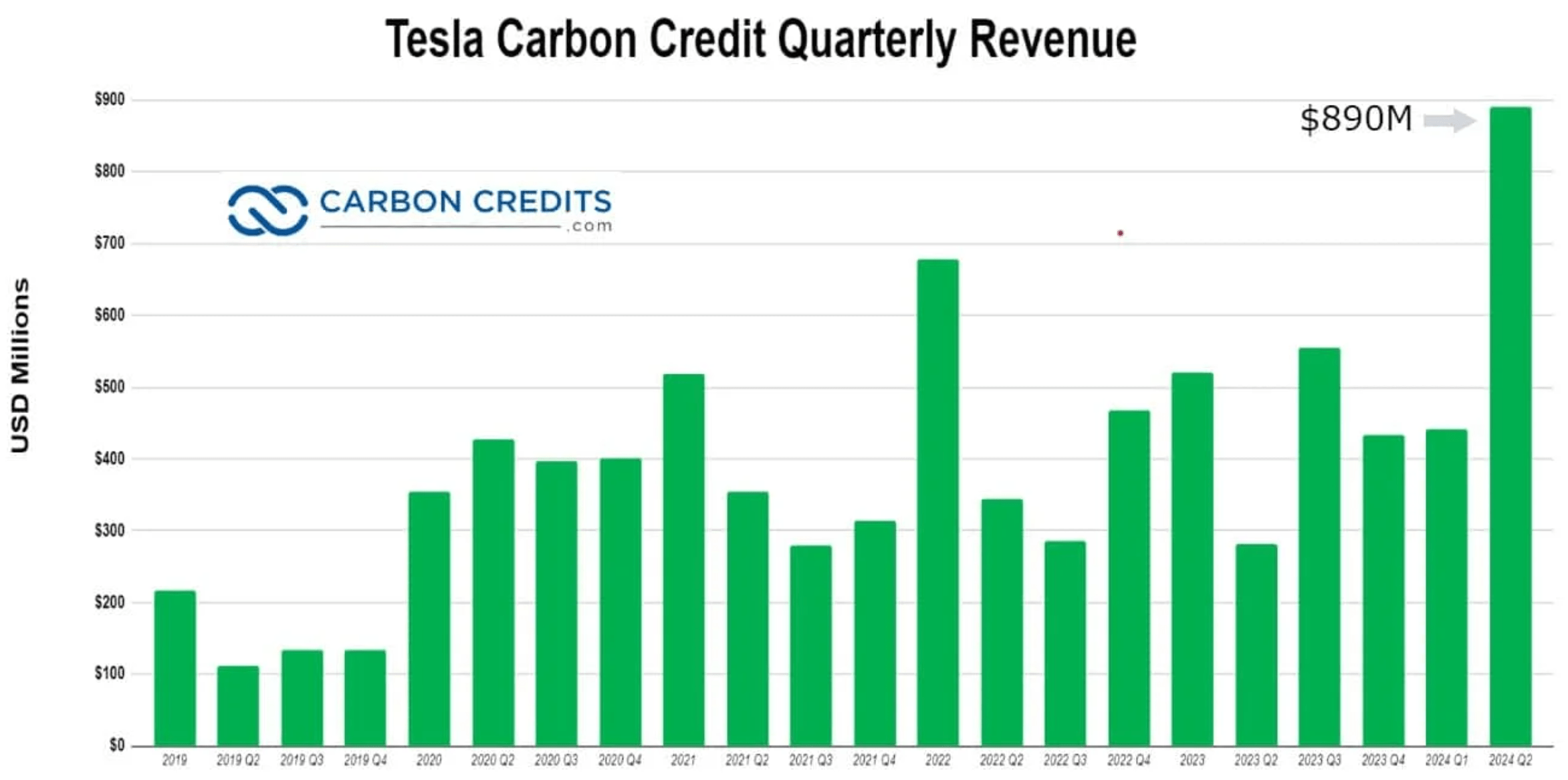

While the vehicle delivery (and unit price) dwindles, TSLA’s sales of carbon credits have been steadily increasing over the years, as illustrated by the chart below. According to statistics provided by Carbon Credits (the emphases were added by me):

TSLA started selling these regulatory credits in 2017 and the proceeds from these sales just reached a record of $890 million in the past quarter. This revenue stream is up 216% from $282 million a year earlier and a 102% increase from Q1 ($442m). When excluding these regulatory credits, automotive gross margin was 14.6% for Q2.

Carbon Credits

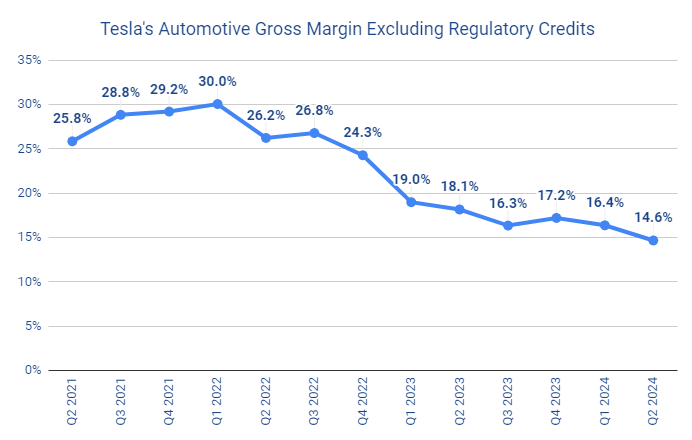

The automotive gross margin is thus substantially below the above 18%. The real concern lies in the trend, though. To provide a broader context, the next chart shows Tesla’s automotive gross margin, excluding regulatory credits, in the past 3 years. As seen, the current level of 14.6% is less than half of its peak of 30% in early 2022. Over the years, Elon Musk has been telling investors that Tesla is NOT a car company, it’s a technology and AI company. That positioning, of course, made sense at a gross margin of ~30% which was about 2x higher than the average gross margin for the automobile industry and close to Apple’s gross margin. And if you recall, 2022 was also the time when Tesla’s market capitalization peaked at around $1.2 trillion as investors happily paid triple-digits P/E for its shares.

Source: X.com

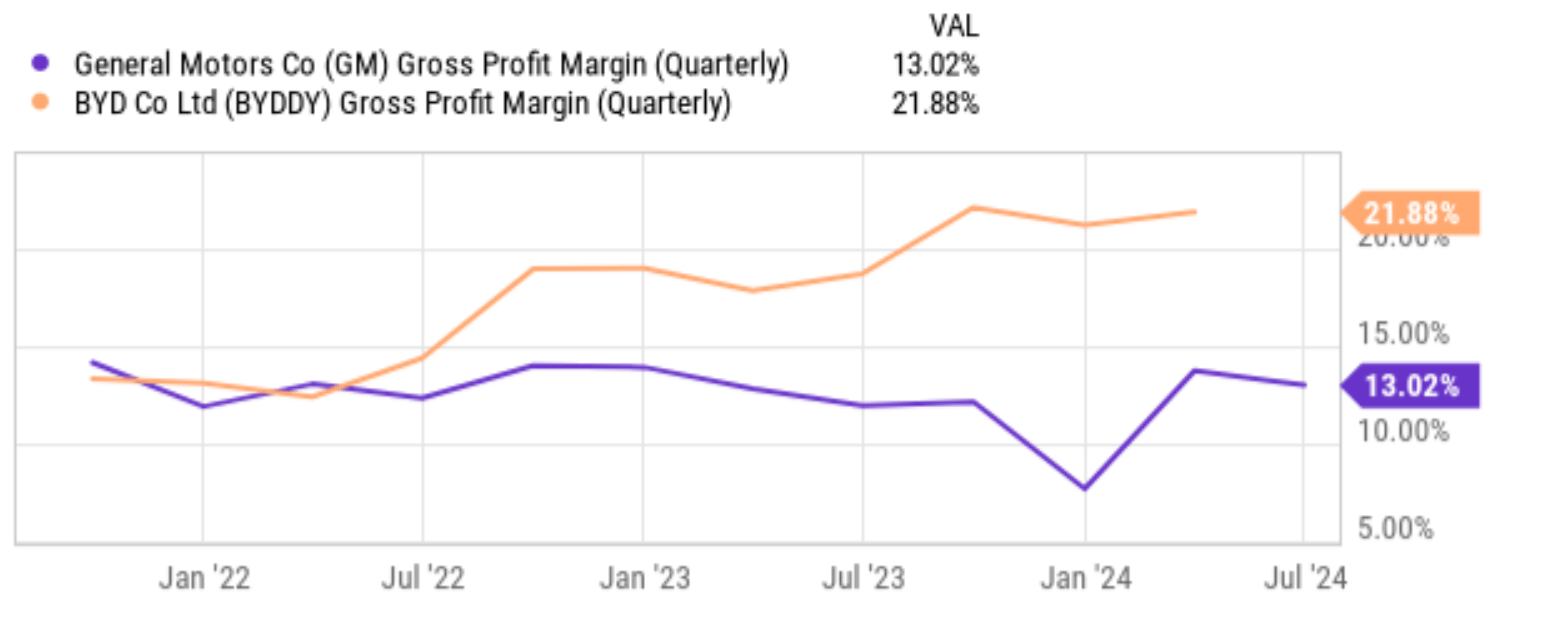

Now, with an automobile gross margin of around 14%, TSLA has become just “another” automobile company both in comparison to the traditional ones and the newer EV ones. As an example, the chart below shows the gross profit margin of General Motors (GM) and BYD Company (OTCPK:BYDDF) in the past 3 years. As seen, BYD has been able to consistently maintain a gross profit margin of around 20% in the past ~2 years. BYD’s current margin hovers around 21.88%. GM’s margin fluctuated around an average of 13% most of the time.

Seeking Alpha

Other risks and final thoughts

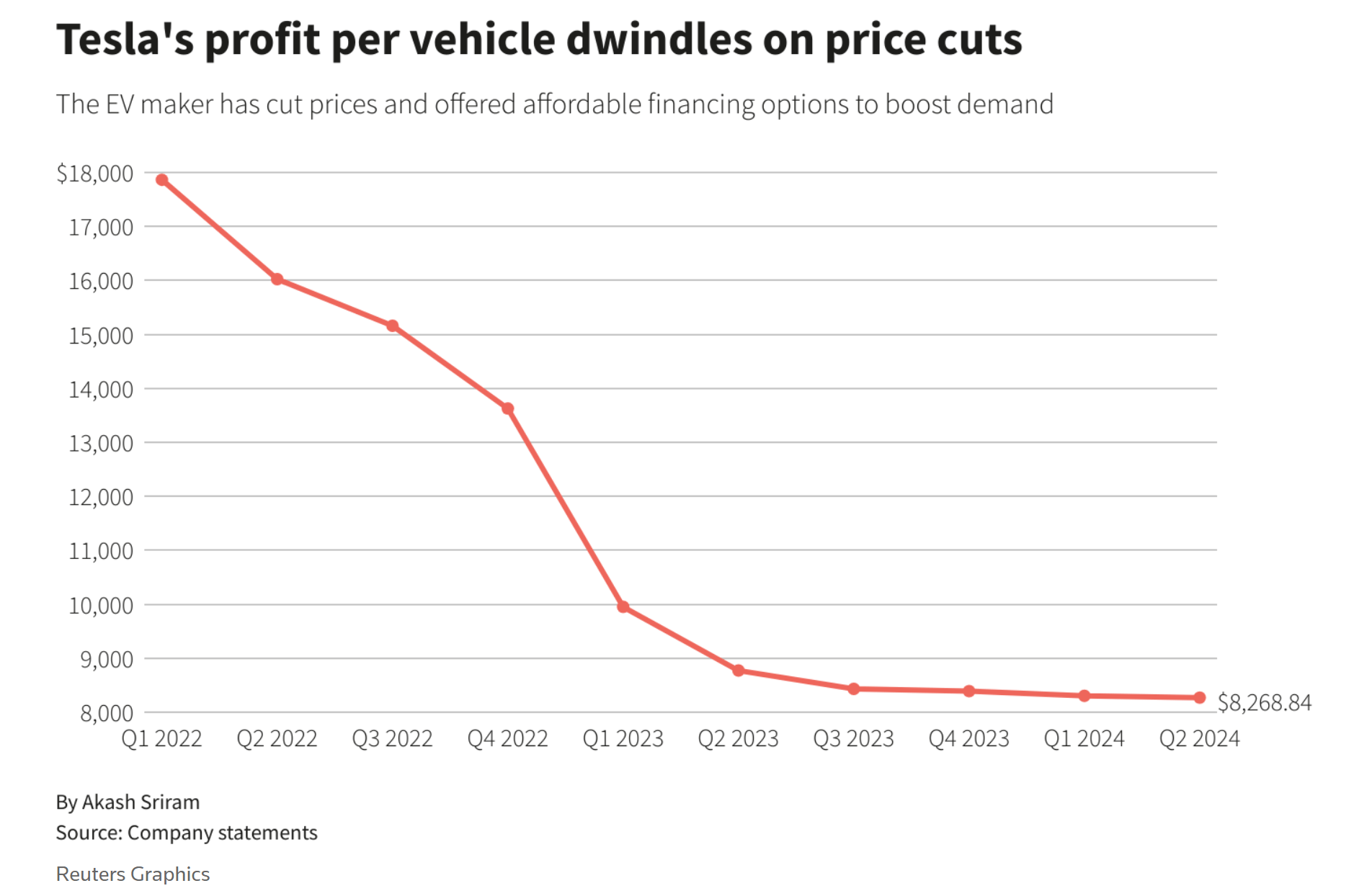

A key cause of (or a response to – depending on your perspective) the above margin pressure is the unit price cuts of TSLA’s vehicles. As seen in the chart below, TSLA has been engaged in an intense price war in the recent 1~2 years to boost demand. However, I don’t think the strategy is working based on the inventory data.

Reuters

On the positive side, I see progress on its plan for the $25,000 affordable model (also known as ‘Model 2’). The model has the potential to push Tesla unit deliveries to the next level. Admittedly, the plan kept getting delayed (among other things). However, I think the progress TSLA made on the battery front (especially the 4680) has laid solid groundwork for the affordable model – but this will be the topic that merits a standalone analysis.

There are other high-risk, high-payoff initiatives afoot at TSLA. In the Q2 ER, CEO Elon Musk provided updates on the humanoid robot project (which had begun performing tasks autonomously in one of TSLA’s facilities), self-driving Tesla technologies, and the development of the robotaxis network. The market interpreted these initiatives quite negatively after Q2, mostly because they are behind schedule. My view is that the prevailing sentiment is too extreme. Given their high-risk and high-return nature, setbacks are expected. They don’t even need to all work out. The possibility of any single one of them working out is a major upside risk in my view.

Putting aside these futuristic bets, the immediate concerns in my mind are the inventory buildup (the focus of my last article) and the automotive gross margin (the focus of this article). Investors should delineate TSLA’s sale of carbon credits from its reported gross margin, as they do not reflect business fundamentals and are subject to policy changes. Once the impact of these credits is adjusted for, TSLA’s automotive margin has shown continued downward pressure in recent quarters and has dropped to the same level as other automotive manufacturers.

It is thus unclear to me if A) Tesla, Inc. can stabilize its automotive margin or B) its other bets can progress enough to support the valuation premium. With these uncertainties, the stock is only for investors with a high-risk tolerance. I am optimistic about the long-term prospects (say the next 3~5 years), but investors really need a strong nerve to stomach short-term setbacks and extreme stock price swings.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Analyst’s Disclosure:I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

As you can tell, our core style is to provide actionable and unambiguous ideas from our independent research. If your share this investment style, check out Envision Early Retirement. It provides at least 1x in-depth articles per week on such ideas.

We have helped our members not only to beat S&P 500 but also avoid heavy drawdowns despite the extreme volatilities in BOTH the equity AND bond market.

Join for a 100% Risk-Free trial and see if our proven method can help you too.